Navigating the Road to Your Next Ride: Everything You Need to Know About an $8000 Car Loan

Navigating the Road to Your Next Ride: Everything You Need to Know About an $8000 Car Loan Carloan.Guidemechanic.com

Securing a reliable vehicle is a significant step for many, offering independence, convenience, and access to new opportunities. For those on a specific budget, an $8000 car loan can be the perfect bridge to ownership. It’s a common price point for quality used cars that can serve you well for years.

However, navigating the world of auto financing can feel daunting. From understanding interest rates to assessing your creditworthiness, there’s a lot to consider. This comprehensive guide will break down everything you need to know about getting an $8000 car loan, ensuring you’re well-equipped to make informed decisions and drive away with confidence. We’ll explore the approval process, tips for securing the best rates, and crucial advice to avoid common pitfalls.

Navigating the Road to Your Next Ride: Everything You Need to Know About an $8000 Car Loan

Understanding the $8000 Car Loan Landscape

An $8000 car loan typically puts you in the market for a pre-owned vehicle. This segment offers a vast array of choices, from compact sedans perfect for city driving to older SUVs ideal for families. It’s a sweet spot where you can find vehicles with solid reliability without breaking the bank.

Many first-time buyers or individuals looking for a secondary vehicle often target this price range. It allows for manageable monthly payments while still providing a significant upgrade from public transport or an older, less dependable car. Crucially, securing an $8000 car loan can also be an excellent way to build or rebuild your credit history responsibly.

Factors Influencing Your $8000 Car Loan Approval

When you apply for an $8000 car loan, lenders evaluate several key factors to determine your eligibility and the terms they’re willing to offer. Understanding these elements beforehand can significantly improve your chances of approval and help you secure more favorable rates. Let’s delve into each one in detail.

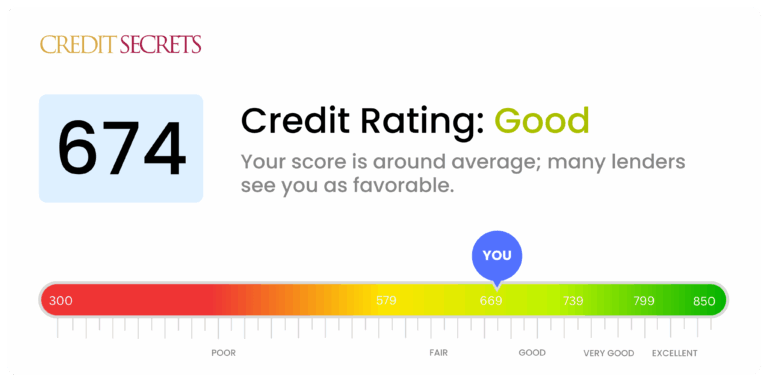

Your Credit Score: The Foundation of Approval

Your credit score is arguably the most critical factor lenders consider. It’s a numerical representation of your creditworthiness, indicating how reliably you’ve managed past debts. A higher score signals less risk to lenders.

- Excellent Credit (720+): With excellent credit, you’re likely to qualify for the lowest interest rates and the most flexible terms on your $8000 car loan. Lenders see you as a very low-risk borrower.

- Good Credit (660-719): Good credit still puts you in a strong position. You’ll generally receive competitive rates, though perhaps not the absolute lowest. Many lenders are eager to work with individuals in this range.

- Fair Credit (600-659): If your credit falls into the fair category, getting an $8000 car loan is still very possible. However, you might face slightly higher interest rates to offset the perceived higher risk. It’s often a good opportunity to improve your credit history.

- Bad Credit (Below 600): Don’t despair if you have bad credit. While challenging, securing an $8000 car loan is not impossible. Lenders specializing in subprime auto loans exist, though you should expect higher interest rates and potentially require a larger down payment or a co-signer. We’ll explore strategies for bad credit later in this article.

Based on my experience, many people underestimate the power of a few points on their credit score. Even a small improvement can translate into significant savings over the life of your loan. Checking your credit report for errors and resolving any disputes before applying is a smart move.

Income and Employment Stability: Can You Afford It?

Lenders need assurance that you have a consistent income stream to make your monthly payments. They’ll typically ask for proof of income, such as pay stubs, tax returns, or bank statements.

- Debt-to-Income (DTI) Ratio: This is a crucial metric. Lenders calculate your DTI by dividing your total monthly debt payments (including the proposed car loan) by your gross monthly income. A lower DTI ratio indicates you have more disposable income to cover your new car payments, making you a more attractive borrower. Generally, a DTI below 43% is preferred.

- Employment History: A stable employment history, typically 1-2 years at the same job, demonstrates reliability. If you’ve recently changed jobs, be prepared to explain the circumstances and show continued income.

The Power of a Down Payment: Reducing Risk and Cost

Making a down payment on your $8000 car loan offers several advantages. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the loan term.

- Lender Perspective: A down payment shows the lender you have "skin in the game," making you less likely to default. It reduces their risk, especially if the vehicle depreciates quickly.

- Recommended Amount: While not always mandatory for an $8000 car loan, a down payment of 10-20% is often recommended. For an $8000 car, that’s $800 to $1600. Even a smaller down payment can make a difference, particularly if your credit isn’t stellar.

Loan Term: The Length of Your Commitment

The loan term refers to the period over which you’ll repay your loan. Common terms range from 36 to 72 months for an $8000 car loan.

- Shorter Terms (36-48 months): These typically come with higher monthly payments but result in less total interest paid. You’ll own the car outright sooner.

- Longer Terms (60-72 months): Longer terms offer lower monthly payments, making the loan seem more affordable. However, you’ll pay significantly more in total interest over the life of the loan. For an $8000 car, a very long term might mean you owe more than the car is worth (negative equity) as it depreciates.

Pro tips from us: While lower monthly payments are appealing, always consider the total cost of the loan. A balance between affordability and minimizing interest is key.

Vehicle Age and Mileage: Lender’s Comfort Zone

For an $8000 car loan, you’re almost certainly looking at a used car. Lenders assess the vehicle itself as collateral.

- Depreciation: Older vehicles with higher mileage generally have a lower resale value and can depreciate more rapidly. This presents a higher risk for lenders.

- Lender Restrictions: Some lenders have restrictions on the maximum age or mileage of a vehicle they will finance. For example, they might not finance cars older than 10 years or with over 150,000 miles. Always check these limits when shopping for your $8000 car.

Steps to Secure Your $8000 Car Loan

Getting an $8000 car loan doesn’t have to be a complicated process. By following a structured approach, you can streamline your journey from application to ownership.

Step 1: Assess Your Financial Health and Set a Budget

Before even looking at cars, take an honest look at your finances. This initial step is crucial for responsible borrowing.

- Budgeting: Determine how much you can comfortably afford for a monthly car payment, factoring in insurance, fuel, and maintenance. Don’t just consider the loan payment.

- Check Your Credit: Obtain your free credit report from AnnualCreditReport.com. Review it for accuracy and identify any areas for improvement. This allows you to address issues before applying and gives you a realistic expectation of the interest rates you might qualify for.

- Calculate Your DTI: Use your current income and existing debts to get a clear picture of your debt-to-income ratio. This helps you understand how lenders will view your application.

Based on my experience, this is often overlooked, leading to financial strain down the road. A well-planned budget prevents you from becoming "car poor."

Step 2: Get Pre-Approved for Your $8000 Car Loan

Pre-approval is a game-changer. It means a lender has conditionally agreed to lend you a specific amount (like $8000) at a certain interest rate, subject to final verification.

- Benefits of Pre-Approval:

- Know Your Budget: You’ll know exactly how much you can spend on a car, preventing you from falling in love with a vehicle outside your price range.

- Negotiating Power: Walking into a dealership with pre-approval is like having cash in hand. You can negotiate on the car’s price, not just the monthly payment.

- Comparison Shopping: You can compare offers from multiple lenders (banks, credit unions, online lenders) without impacting your credit score multiple times. All inquiries within a 14-45 day window for auto loans are typically treated as a single hard inquiry.

- Where to Get Pre-Approved:

- Banks and Credit Unions: Your existing bank or a local credit union is often a great place to start. Credit unions, in particular, are known for competitive rates and personalized service.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others specialize in online auto loans and can offer quick decisions.

Step 3: Shop Smart for Your Vehicle

With pre-approval in hand, you’re ready to find your $8000 car. This isn’t just about finding the cheapest option; it’s about finding the best value.

- Research: Use online resources like Kelley Blue Book (KBB.com) or Edmunds to research car values and reliability ratings for vehicles in the $8000 range. Look for models known for their longevity and low maintenance costs.

- Inspection is Key: For an $8000 used car, a pre-purchase inspection by an independent mechanic is non-negotiable. This small investment can save you thousands in potential repairs down the line. It’s the most important step for a used car purchase.

- Negotiation: Don’t be afraid to negotiate the price. Having your pre-approval allows you to focus on the vehicle’s actual selling price, not just the monthly payment offered by the dealer.

Step 4: Understand the Loan Offer

Once you’ve found your car and secured your loan, carefully review all the terms and conditions.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and any fees. Always compare APRs, not just interest rates, when looking at different loan offers.

- Fees: Be aware of any origination fees, documentation fees, or prepayment penalties. Some lenders charge extra for early repayment.

- Loan Term: Reconfirm the loan term and how it impacts your total interest paid.

- Read the Fine Print: Ensure you understand every clause in the contract before signing. Don’t hesitate to ask questions if anything is unclear.

Step 5: Finalize and Drive Away

After reviewing everything, if you’re satisfied, you’ll sign the necessary paperwork. Congratulations, you’re now the proud owner of a new-to-you car! Remember to:

- Get Insurance: Ensure your new vehicle is properly insured before you drive it off the lot. Lenders typically require full coverage (collision and comprehensive) for financed vehicles.

- Keep Records: Store all your loan documents, purchase agreements, and insurance information in a safe place.

Navigating $8000 Car Loans with Less-Than-Perfect Credit

Having a low credit score might make getting an $8000 car loan seem challenging, but it’s far from impossible. Many lenders specialize in helping individuals with fair or bad credit. The key is to be prepared and explore all your options.

- Larger Down Payment: As mentioned earlier, a substantial down payment significantly reduces the lender’s risk. If you can save up 20% or more for your $8000 car loan, it will open up more opportunities and potentially lower your interest rate.

- Consider a Co-signer: A co-signer with good credit essentially guarantees the loan if you default. This significantly increases your chances of approval and can secure you a much better interest rate. Ensure your co-signer understands their responsibilities fully.

- Credit Unions: Often, credit unions are more flexible than traditional banks when it comes to lending to members with less-than-perfect credit. They operate on a member-first philosophy and may be willing to look beyond just your credit score.

- Subprime Lenders: There are lenders who specifically cater to individuals with bad credit. While their interest rates will be higher, they provide a pathway to vehicle ownership and an opportunity to rebuild your credit. Research these lenders carefully and compare their offers.

- Secured Loans: Some lenders may offer a secured car loan where the car itself acts as collateral. This can make approval easier for those with poor credit.

- Improve Your Credit First: If you’re not in a desperate rush, taking a few months to improve your credit score can save you a lot of money in interest. Pay down existing debts, make all payments on time, and dispute any errors on your report.

Common mistakes to avoid are jumping at the first offer you receive, especially if you have bad credit. Always compare at least three different loan offers. Also, avoid "buy here, pay here" dealerships without understanding their terms thoroughly, as their interest rates can be exceptionally high.

Calculating Your $8000 Car Loan Payments

Understanding how your monthly payments are calculated is vital for budgeting. For an $8000 car loan, your payment will primarily depend on three factors:

- Principal Amount: The actual amount you borrow (e.g., $8000 minus any down payment).

- Interest Rate (APR): The annual cost of borrowing, expressed as a percentage.

- Loan Term: The length of time you have to repay the loan in months.

You can use online car loan calculators to estimate your monthly payments. Simply input these three variables, and the calculator will provide an estimate. For example, an $8000 loan at 7% APR over 60 months would result in a monthly payment of approximately $158. Over 48 months, it would be around $192, but you’d save on total interest.

The True Cost of an $8000 Car Loan: Beyond Monthly Payments

It’s easy to focus solely on the monthly payment, but the true cost of car ownership extends much further. When budgeting for your $8000 car, consider these additional expenses:

- Total Interest Paid: Over the life of your loan, the interest can add hundreds or even thousands to the initial $8000 principal. This is why a lower APR and shorter term are often financially advantageous.

- Insurance: Car insurance is a non-negotiable expense. The type of car, your driving history, and your location will all influence your premiums. Get insurance quotes before you finalize your purchase.

- Registration and Taxes: These are typically one-time or annual fees required by your state. Factor them into your initial purchase budget.

- Maintenance and Repairs: Used cars, especially those in the $8000 range, will require ongoing maintenance. Budget for regular oil changes, tire rotations, and potential repairs. An emergency fund for unexpected breakdowns is crucial.

- Fuel Costs: Don’t forget the cost of gasoline! This varies based on the car’s fuel efficiency and how much you drive.

Pro tips from us: Always allocate a portion of your monthly budget specifically for car maintenance and unexpected repairs. This proactive approach can prevent financial stress when issues arise.

Pro Tips for a Smooth $8000 Car Loan Experience

To ensure your journey to car ownership is as smooth as possible, keep these expert tips in mind:

- Read Everything Carefully: Never sign a document you haven’t thoroughly read and understood. Ask for clarification on any ambiguous terms.

- Don’t Rush the Process: Car buying is a significant financial decision. Take your time, do your research, and don’t feel pressured by salespeople or tight deadlines.

- Compare Multiple Offers: Whether it’s the car price or the loan terms, always compare options from various sources. This ensures you’re getting the best deal available.

- Get a Pre-Purchase Inspection (Again!): For an $8000 used car, this cannot be stressed enough. It’s your best defense against buying a lemon.

- Consider GAP Insurance: Guaranteed Asset Protection (GAP) insurance covers the difference between what you owe on your loan and the car’s actual cash value if it’s totaled or stolen. For an $8000 car that might depreciate quickly, this can be a wise investment.

- Understand Add-ons: Be wary of extended warranties, service contracts, or other add-ons pitched at the dealership. While some may be valuable, many are overpriced and might not be necessary. Research their value independently.

For more detailed advice on car financing and budgeting, you might find our article on helpful. Additionally, understanding your credit score better can unlock better loan options; check out our guide on .

For reliable external information on managing your finances and understanding loan terms, the Consumer Financial Protection Bureau (CFPB) offers excellent resources. You can visit their website at consumerfinance.gov for unbiased advice and tools.

Conclusion: Your Road to an $8000 Car Loan Starts Here

Obtaining an $8000 car loan is a realistic and achievable goal for many, providing access to reliable transportation without a massive financial burden. By understanding the factors that influence approval, preparing your finances, and following a structured approach, you can confidently navigate the process.

Remember, smart planning, thorough research, and a clear understanding of all costs involved are your best allies. Don’t be afraid to ask questions, compare offers, and ensure every step aligns with your financial comfort. With this guide, you’re now equipped with the knowledge to secure your $8000 car loan and enjoy the freedom of the open road. Start your journey today, and drive away with peace of mind!