Navigating the Road to Your Next Ride: The Ultimate Guide to the Best Used Car Auto Loans

Navigating the Road to Your Next Ride: The Ultimate Guide to the Best Used Car Auto Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a used car is a smart financial move for many. Used vehicles often offer significant savings compared to their brand-new counterparts, primarily due to depreciation. However, the path to owning a used car isn’t always a smooth one, especially when it comes to securing the right financing. Many prospective buyers find themselves overwhelmed by the myriad of options and complexities surrounding used car auto loans.

This comprehensive guide is designed to demystify the world of used car financing, equipping you with the knowledge and strategies to secure the best used car auto loans tailored to your specific needs. From understanding the basics to navigating the application process and avoiding common pitfalls, we’ll cover every aspect to ensure you drive away with confidence, knowing you’ve made an informed and advantageous decision. Our ultimate goal is to empower you to find a loan that not only fits your budget but also provides peace of mind on the open road.

Navigating the Road to Your Next Ride: The Ultimate Guide to the Best Used Car Auto Loans

Section 1: Understanding Used Car Auto Loans – Your Foundation for Financing

Before diving into the application process, it’s crucial to grasp the fundamental concepts of used car auto loans. These financial instruments are specifically designed to help individuals purchase pre-owned vehicles, and while they share similarities with new car loans, there are distinct differences you need to be aware of.

What Exactly is a Used Car Auto Loan?

Simply put, a used car auto loan is a secured loan where the vehicle you purchase acts as collateral. This means if you fail to make your payments, the lender has the right to repossess the car. Lenders provide you with a lump sum to buy the car, and you repay them, plus interest, over a predetermined period, known as the loan term. This allows you to acquire a significant asset without having to pay the full price upfront.

The primary distinction from new car loans often lies in the loan terms and interest rates. Used cars, by their nature, have a lower resale value and can be perceived as having a higher risk by lenders. This can sometimes translate into slightly higher interest rates or shorter loan terms compared to financing a brand-new vehicle, though this isn’t always the case, especially for well-maintained, newer used models.

Key Terms You Must Know

Navigating the world of auto loans requires understanding the jargon. Here are some essential terms that will frequently come up during your search for the best used car auto loans:

- APR (Annual Percentage Rate): This is perhaps the most critical number. APR represents the true annual cost of borrowing money, including not just the interest rate but also any additional fees charged by the lender. A lower APR means lower overall costs.

- Interest Rate: This is the percentage charged by the lender for borrowing the principal amount. While related to APR, it doesn’t include other fees.

- Loan Term: This is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter term usually means higher monthly payments but less interest paid overall, while a longer term offers lower monthly payments but accrues more interest over time.

- Principal: This refers to the original amount of money borrowed, excluding interest and fees.

- Down Payment: This is the initial sum of money you pay upfront towards the purchase of the vehicle. A larger down payment reduces the amount you need to borrow, which can lead to lower monthly payments and less interest paid over the life of the loan.

- Collateral: As mentioned, the car itself serves as collateral for the loan. This reduces the risk for the lender.

Why Choose a Used Car Loan?

The decision to finance a used car rather than a new one is often driven by several compelling financial advantages. From my experience, the biggest draw is the significant savings potential that used vehicles offer.

Firstly, depreciation is a major factor. New cars lose a substantial portion of their value the moment they’re driven off the lot. Used cars, having already gone through this initial rapid depreciation phase, tend to hold their value more steadily. This means you’re often getting more car for your money. Secondly, the overall cost of ownership is typically lower. Not only is the purchase price less, but insurance premiums for used cars are also generally more affordable than for new ones. Opting for a used car loan can be a very sensible financial decision, allowing you to get a reliable vehicle without the premium price tag.

Section 2: Preparing for Your Used Car Loan Application – Laying the Groundwork

Securing the best used car auto loans isn’t just about finding a car; it’s about preparing yourself financially. Lenders assess your ability to repay the loan, and several factors play a crucial role in their decision-making process. Taking the time to prepare can significantly improve your chances of approval and help you secure more favorable terms.

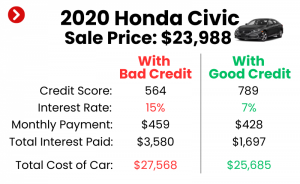

Your Credit Score is King: Understand and Improve It

Your credit score is arguably the most influential factor in determining the interest rate you’ll be offered. Lenders use it to gauge your creditworthiness – essentially, how likely you are to repay your debts. A higher credit score signals lower risk, which translates to better loan terms and lower interest rates.

- How to Check Your Score (and Report): Before you even think about applying for a loan, get a clear picture of your credit health. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months via AnnualCreditReport.com. Many credit card companies and banks also offer free credit score monitoring. Review your report carefully for any errors, as these can negatively impact your score.

- Tips for Improving Your Credit Score Before Applying: If your score isn’t where you want it to be, take steps to improve it. Pro tips from us include paying down existing debts, especially credit card balances, as high utilization can hurt your score. Make sure all your payments are on time – payment history is a huge component of your score. Avoid opening new credit accounts right before applying for a car loan, as this can temporarily lower your score. For more detailed strategies on boosting your credit score, check out our guide on .

Budgeting and Affordability: Know Your Limits

It’s easy to get carried away by the excitement of a new car, but a crucial step in securing the best used car auto loans is to realistically determine what you can afford. This goes beyond just the monthly loan payment.

- Determine What You Can Truly Afford: Consider your entire financial picture. How much disposable income do you have after all your essential expenses? Remember to factor in not just the loan payment, but also insurance, fuel costs, maintenance, and potential registration fees. A common mistake is focusing solely on the monthly payment without considering the total cost of ownership.

- The 20/4/10 Rule (or Similar Guideline): While not rigid, many financial experts suggest a guideline like the 20/4/10 rule: a 20% down payment, a loan term of no more than four years (48 months), and monthly car expenses (payment, insurance) not exceeding 10% of your gross monthly income. This rule helps ensure your car loan doesn’t become a financial burden.

- Down Payment Strategies: A larger down payment can significantly reduce your loan amount, lower your monthly payments, and decrease the total interest paid over the loan term. It also demonstrates financial responsibility to lenders. If possible, save up a substantial down payment.

Gathering Necessary Documents

Once you’ve assessed your financial health, start compiling the documents lenders will require. Having everything ready can streamline the application process.

- Essential Documents: Typically, you’ll need proof of identity (driver’s license or state ID), proof of residence (utility bill, lease agreement), proof of income (pay stubs, tax returns if self-employed, bank statements), and your Social Security number. If you have a trade-in, you’ll also need its title and registration. Being organized shows you’re a serious and prepared applicant.

Section 3: Where to Find the Best Used Car Auto Loans – Exploring Your Options

The landscape of auto loan providers is diverse, offering various advantages depending on your financial situation and preferences. To secure the best used car auto loans, it’s vital to explore all avenues and understand what each type of lender brings to the table.

Direct Lenders: Banks & Credit Unions

For many, starting with direct lenders like banks and credit unions is the most advisable first step. Based on my experience, they often offer some of the most competitive rates and transparent processes.

- Pros: Banks and credit unions are known for offering some of the lowest interest rates, especially to applicants with strong credit. They also provide a clear, direct lending process, and financing through your existing bank or credit union can strengthen your overall financial relationship with them.

- Cons: These institutions typically have stricter lending requirements regarding credit scores and income. The approval process might take a bit longer compared to some other options.

- Pro Tip: Always begin your loan search by seeking pre-approval from at least two or three different banks or credit unions. This gives you a baseline offer to compare against other options.

Online Lenders: Convenience at Your Fingertips

The digital age has brought forth a wealth of online lending platforms that specialize in auto loans. These can be incredibly convenient and often provide quick approvals.

- Pros: Online lenders offer unparalleled convenience, allowing you to apply from anywhere at any time. They often provide quick pre-approvals, sometimes within minutes, and their rates can be highly competitive due to lower overheads. Many also specialize in various credit profiles, including those with less-than-perfect credit.

- Cons: While convenient, the lack of in-person interaction might be a drawback for some. It’s crucial to thoroughly vet online lenders to ensure they are reputable and secure; common mistakes to avoid are falling for predatory lenders or scams. Always check reviews and look for established companies.

Dealership Financing: The One-Stop Shop

When you buy a car from a dealership, they will invariably offer financing options through their network of lenders. This can be a convenient choice, but it requires careful consideration.

- Pros: Dealership financing offers the ultimate convenience of a "one-stop shop" – you can test drive, buy, and finance your car all in one location. They often have access to a wide range of lenders and may even offer special promotional rates or incentives on specific vehicles.

- Cons: The biggest drawback is that dealerships may mark up the interest rate they offer you from the rate they get from their lenders. This means you could end up paying more than if you had secured financing independently. They also might push you towards certain add-ons or extended warranties that you may not need.

- Common Mistake: A common mistake to avoid is accepting dealership financing without first getting pre-approved elsewhere. Having an independent pre-approval in hand gives you negotiating power and ensures you’re getting a fair deal.

Private Party Loans: Financing from an Individual Seller

If you’re buying a used car directly from an individual seller, rather than a dealership, you’ll need a specific type of loan often referred to as a private party auto loan.

- Specific Challenges and How to Overcome Them: Many traditional lenders are hesitant to finance private party sales due to increased risk (e.g., no dealer inspection, potential for undisclosed issues). However, some banks and credit unions do offer these loans. You’ll typically need to provide more documentation, such as a bill of sale and a professional vehicle inspection report, to secure financing. Based on my experience, this type of loan requires more legwork but can often lead to better deals on the car itself.

Section 4: The Application Process: Step-by-Step Towards Approval

Once you’ve done your homework and explored your options, it’s time to navigate the application process. This stage is critical for securing the best used car auto loans, and a strategic approach can save you money and stress.

The Power of Pre-Approval

Pre-approval is not just a suggestion; it’s a non-negotiable step in the savvy car buying process. It’s one of the most powerful tools you have.

- What it is and Why It’s Crucial: Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount up to a certain limit, at a particular interest rate, before you’ve even chosen a car. This is usually valid for a set period, like 30 to 60 days. It doesn’t commit you to that lender, but it gives you a concrete offer.

- Benefits: Negotiating Power, Clarity on Budget: Armed with a pre-approval letter, you walk into a dealership as a cash buyer. You know exactly how much you can spend, and you have leverage to negotiate the car’s price without the added pressure of simultaneously securing financing. This separates the car price negotiation from the loan negotiation, often leading to a better deal on both fronts.

Comparing Loan Offers: Beyond the Interest Rate

Once you have multiple loan offers, whether from pre-approvals or dealership proposals, it’s time to compare them meticulously. Don’t just glance at the interest rate.

- APR vs. Interest Rate: Remember, the APR is the more comprehensive figure as it includes all fees. Always compare APRs, not just advertised interest rates, to get a true understanding of the loan’s cost.

- Loan Term Impact on Total Cost: While a longer loan term (e.g., 72 months) might offer lower monthly payments, it significantly increases the total interest you’ll pay over the life of the loan. Pro tips from us: Aim for the shortest loan term you can comfortably afford to minimize interest expenses.

- Fees to Watch Out For: Scrutinize the loan documents for any hidden fees, such as origination fees, application fees, or prepayment penalties. These can add to the overall cost of your loan. Some lenders charge a fee for early payoff, which can be a common mistake if you plan to pay off your loan ahead of schedule.

Reading the Fine Print: No Stone Unturned

The loan agreement is a legally binding document. It’s paramount that you understand every clause before you sign.

- Hidden Clauses and Prepayment Penalties: Look for any clauses that might seem unusual or disadvantageous. Specifically, check for prepayment penalties, which charge you a fee if you pay off your loan earlier than scheduled. While less common now, they still exist. Also, understand the implications of late payment fees and what constitutes a default.

- Understanding the Entire Agreement: Don’t hesitate to ask questions if anything is unclear. Ensure you understand the total amount you’re borrowing, the total interest you’ll pay, your monthly payment, and the exact duration of the loan. This due diligence ensures you secure the best used car auto loans without any unpleasant surprises down the line.

Section 5: Special Considerations for Used Car Auto Loans

While the general principles apply to most used car auto loans, certain situations require specific attention. Understanding these nuances can help you navigate potentially tricky waters and still secure favorable financing.

Bad Credit Used Car Loans: Options and Expectations

Having a less-than-perfect credit score doesn’t necessarily mean you can’t get a used car loan, but it does mean your options might be different, and you should manage your expectations regarding interest rates.

- Options: Co-signer, Secured Loans, Subprime Lenders: If your credit score is low, consider applying with a co-signer who has good credit. Their strong credit history can help you get approved and potentially secure a better rate. Another option is a secured loan, where you might use another asset (like savings) as collateral. Additionally, some lenders specialize in subprime auto loans for individuals with poor credit. These loans often come with higher interest rates to offset the increased risk for the lender.

- Managing Expectations: Be realistic about the interest rate you’ll receive. It will likely be higher than what someone with excellent credit would get. The goal here is to get into a reliable vehicle, make timely payments, and use this loan as an opportunity to rebuild your credit.

- Pro Tip: Focus on improving your credit for the long term. Once your score improves, you might be able to refinance your loan at a lower interest rate, saving you a significant amount of money over time. For more in-depth advice, see our article on .

Older or High-Mileage Vehicles: Lender Restrictions

Financing older vehicles or those with very high mileage can present unique challenges. Lenders often view these cars as higher risk due to potential mechanical issues and lower resale value.

- Lender Restrictions, Higher Rates: Many lenders have age and mileage restrictions for the vehicles they will finance. For instance, a car might need to be less than 10-12 years old and have under 100,000-150,000 miles. If a car falls outside these parameters, fewer lenders will be willing to finance it, and those that do might offer significantly higher interest rates or require a larger down payment.

- Importance of Vehicle Inspection: If you’re considering an older or high-mileage vehicle, a pre-purchase inspection by an independent, certified mechanic is absolutely critical. This can uncover potential issues that could lead to costly repairs down the road, making the car a poor investment regardless of the loan terms. This due diligence helps you avoid buying a "lemon."

Refinancing Your Used Car Loan: When It Makes Sense

Even after you’ve secured a loan, your financial journey isn’t necessarily over. Refinancing can be a powerful tool to improve your loan terms later on.

- When It Makes Sense (Lower Rates, Better Terms): Refinancing involves taking out a new loan to pay off your existing car loan, ideally with a lower interest rate or more favorable terms. This makes sense if your credit score has significantly improved since you first took out the loan, if interest rates have dropped, or if you initially received a high-interest loan due to bad credit. It can also be beneficial if you want to change your loan term – either shorten it to pay less interest or lengthen it to reduce monthly payments (though this often means more total interest).

- How to Do It: The process is similar to applying for your initial loan. You’ll shop around for new lenders, compare offers, and once approved, the new lender will pay off your old loan. Based on my experience, even a small reduction in APR can save you hundreds, if not thousands, of dollars over the loan’s life.

Section 6: Common Mistakes to Avoid When Securing Used Car Auto Loans

Even with all the right information, it’s easy to fall into common traps. Being aware of these pitfalls is just as important as knowing the best practices for securing the best used car auto loans.

Not Getting Pre-Approved

As discussed, this is perhaps the biggest mistake car buyers make. Walking into a dealership without pre-approval puts you at a distinct disadvantage. You lose negotiating power on the car’s price because the dealer knows you’re reliant on their financing options. Always get an independent pre-approval first.

Focusing Only on Monthly Payment

It’s tempting to fixate solely on the lowest possible monthly payment, but this can be a costly error. Lenders can easily lower your monthly payment by extending the loan term, which means you pay significantly more in interest over the life of the loan. Always consider the total cost of the loan, not just the monthly installment.

Skipping a Vehicle Inspection

Especially with used cars, appearances can be deceiving. Failing to get a pre-purchase inspection from an independent mechanic can lead to buying a car with hidden mechanical problems that could cost you thousands in repairs down the line. This negates any savings you might have made on the purchase price or loan terms. For a detailed checklist, you can refer to an external resource like the Federal Trade Commission’s guide on buying a used car.

Ignoring Total Cost of Ownership

Beyond the loan payment, remember to budget for other significant costs. This includes car insurance, fuel, routine maintenance, and potential repairs. A car might have a low purchase price and a seemingly affordable loan payment, but if its insurance is exorbitant or it’s known for expensive repairs, it might not be the best financial decision in the long run.

Falling for Add-Ons at the Dealership

Dealerships often push various add-ons like extended warranties, paint protection, fabric protection, and GAP insurance (Guaranteed Asset Protection). While some, like GAP insurance, might be beneficial in certain circumstances, others are often overpriced and unnecessary. Critically evaluate each add-on and don’t be afraid to decline them or negotiate their price. Often, you can find better deals for these services elsewhere.

Conclusion: Your Smart Path to the Best Used Car Auto Loans

Securing the best used car auto loans doesn’t have to be a daunting task. By understanding the fundamentals, preparing your finances, diligently exploring your lending options, and approaching the application process strategically, you empower yourself to make intelligent decisions. The road to your next ride should be one paved with confidence and financial prudence, not uncertainty.

Remember to prioritize your credit score, budget realistically, get pre-approved, and scrutinize every loan offer. Avoid common mistakes that can lead to unnecessary expenses. With the comprehensive knowledge provided in this guide, you are now well-equipped to navigate the complexities of used car financing. Drive forward with the assurance that you’ve secured a loan that not only fits your budget but also provides the flexibility and peace of mind you deserve. Your journey to owning the perfect used car starts with making an informed choice about your financing.