Navigating the Road to Your Next Vehicle: A Comprehensive Guide to Securing a $23,000 Car Loan

Navigating the Road to Your Next Vehicle: A Comprehensive Guide to Securing a $23,000 Car Loan Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or pre-owned vehicle often involves securing an auto loan. For many, a $23,000 car loan represents a sweet spot, offering access to a wide range of reliable and feature-rich cars without an exorbitant monthly payment. However, navigating the world of auto financing can feel complex. This in-depth guide is designed to demystify the process, providing you with the essential knowledge, strategies, and insights needed to confidently secure a $23,000 car loan.

Our goal is to equip you with the expertise to not only get approved but also to secure the best possible terms for your specific financial situation. We’ll delve into everything from understanding lender expectations to managing your loan responsibly, ensuring you drive away with peace of mind.

Navigating the Road to Your Next Vehicle: A Comprehensive Guide to Securing a $23,000 Car Loan

Understanding the $23,000 Car Loan Landscape

A $23,000 car loan isn’t just a number; it’s a significant financial commitment that requires careful consideration. This amount is quite common, allowing buyers to finance a respectable selection of vehicles, from well-equipped compact cars and mid-size sedans to capable SUVs and even some entry-level luxury models. Understanding what this loan entails is the first step toward smart financing.

When you take out a $23,000 car loan, you’re essentially borrowing money from a lender to purchase a vehicle, agreeing to repay that amount, plus interest, over a predetermined period. The total cost of your loan extends beyond the principal amount; it includes the interest accrued over the loan term, which can significantly increase your overall expenditure.

Factors Influencing Your Monthly Payment

Several critical elements come into play when calculating your monthly payment for a $23,000 car loan. Each factor directly impacts how much you’ll pay each month and the total cost of the loan over its lifetime.

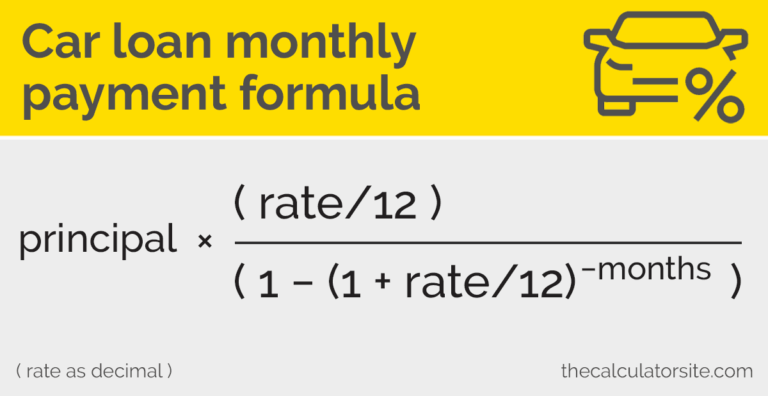

Firstly, the interest rate is arguably the most impactful factor. This percentage represents the cost of borrowing the money. A lower interest rate means less money paid back to the lender over time, resulting in lower monthly payments and substantial savings overall. Your creditworthiness, the economy, and the lender’s policies all influence the interest rate you’re offered.

Secondly, the loan term, or the length of time you have to repay the loan, also plays a crucial role. Common terms range from 36 to 84 months. A shorter loan term typically means higher monthly payments but less interest paid over the life of the loan. Conversely, a longer term offers lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll end up paying significantly more in interest over time.

Finally, the down payment you make upfront significantly affects your monthly payments and the total amount financed. A larger down payment reduces the principal loan amount, which in turn lowers your monthly payments and the total interest you’ll pay. It also shows lenders you’re serious about the purchase and have a financial stake in the vehicle.

Key Factors Lenders Consider for Approval

When you apply for a $23,000 car loan, lenders evaluate a range of criteria to assess your creditworthiness and your ability to repay the debt. Understanding these factors is paramount to preparing a strong application and increasing your chances of approval.

Credit Score: The Cornerstone of Car Loan Approval

Your credit score is often the first and most critical piece of information lenders look at. It’s a three-digit number that summarizes your credit history, indicating your reliability as a borrower. A higher credit score signals lower risk to lenders, often leading to better interest rates and more favorable loan terms.

Based on my experience, lenders typically categorize applicants into tiers based on their FICO or VantageScore. Excellent credit (720+) will unlock the most competitive rates, while good credit (660-719) still offers solid options. Fair credit (620-659) might see higher rates, and poor credit (below 620) will present significant challenges, often resulting in much higher interest rates or requiring a co-signer. It’s crucial to check your credit score and report before applying.

Income Stability: Proof of Steady Employment

Lenders want assurance that you have a consistent and sufficient income stream to comfortably afford your monthly car payments. They’ll typically request proof of income, such as pay stubs, W-2s, or tax returns if you’re self-employed. Steady employment history, ideally with the same employer for at least a year or two, strengthens your application.

Your income needs to be enough to cover your existing expenses, other debt obligations, and the new car payment without causing financial strain. Lenders aren’t just looking at the number; they’re assessing the reliability and sustainability of your earnings.

Debt-to-Income (DTI) Ratio: How Much Debt You Carry

Your Debt-to-Income (DTI) ratio is a vital metric that lenders use to determine your ability to manage monthly payments and take on additional debt. It’s calculated by dividing your total monthly debt payments by your gross monthly income. For instance, if your monthly debt payments (rent/mortgage, credit card minimums, student loans) are $1,000 and your gross monthly income is $4,000, your DTI is 25%.

Most lenders prefer a DTI ratio below 40-45%, including the proposed car payment. A lower DTI indicates that you have more disposable income available to cover your new car loan, making you a less risky borrower. It’s a clear indicator of your financial health.

Down Payment: The Impact of Putting Money Down

Making a down payment on your $23,000 car loan is highly advantageous. It reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan. From a lender’s perspective, a down payment also signifies your commitment to the purchase and reduces their risk.

Pro tips from us: Aim for at least a 10-20% down payment, especially for a new car. For used cars, a smaller percentage might be acceptable, but a larger down payment is always better. It can often be the deciding factor in getting approved, especially if your credit isn’t stellar, and can secure you a better interest rate.

Loan Term: Shorter vs. Longer Terms

The length of your loan term (e.g., 36, 48, 60, 72, or 84 months) significantly impacts both your monthly payment and the total interest paid. While a longer term makes monthly payments more manageable, it dramatically increases the total cost of the loan due to prolonged interest accumulation.

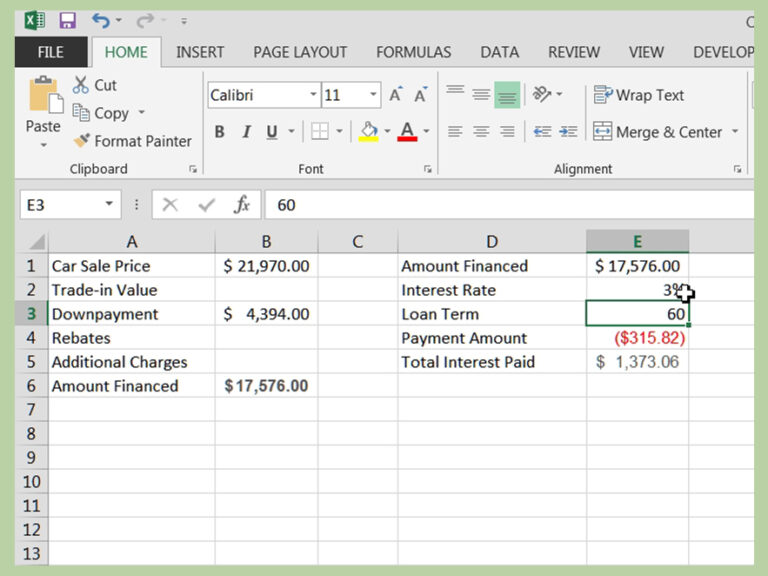

For example, a 72-month loan on $23,000 will have a lower monthly payment than a 48-month loan, but you could end up paying thousands more in interest. Lenders generally prefer shorter terms because they represent less risk over time. Always balance affordability with the total cost of ownership.

The Application Process: Step-by-Step Guide

Securing a $23,000 car loan doesn’t have to be daunting. By following a structured process, you can approach lenders confidently and make informed decisions.

Preparation: Checking Your Credit and Budgeting

Before you even look at cars, check your credit report from all three major bureaus (Experian, Equifax, TransUnion). Look for any errors and dispute them immediately. Understand your credit score, as this will heavily influence the rates you’re offered. Simultaneously, create a realistic budget. Determine how much you can comfortably afford each month for a car payment, including insurance, fuel, maintenance, and registration. Don’t let the car payment alone dictate your budget; factor in all associated costs.

Gathering Documents

Lenders will require several documents to verify your identity, income, and residency. Typical documents include a valid driver’s license, proof of income (pay stubs, W-2s, tax returns), proof of residence (utility bill, lease agreement), and potentially bank statements. Having these ready will streamline the application process.

Shopping for Lenders: Don’t Settle for the First Offer

This is a crucial step. Do not limit yourself to dealership financing alone. Explore options from various sources:

- Banks: Traditional banks often offer competitive rates, especially if you have an existing relationship with them.

- Credit Unions: These member-owned financial institutions are known for offering some of the lowest interest rates due to their non-profit status.

- Online Lenders: Companies like Capital One Auto Finance, LightStream, and Carvana offer convenient online application processes and can provide quick pre-approvals.

- Dealership Financing: While convenient, always compare their offers with pre-approvals you’ve secured elsewhere. Dealerships often work with multiple lenders, but their initial offer might not always be the best.

Get pre-approved from at least 2-3 different lenders before you visit a dealership. This gives you a strong negotiating position and a benchmark for comparison.

Submitting Your Application

Once you’ve chosen a few potential lenders, submit your formal application. Be honest and accurate with all information provided. Most applications can be completed online or in person. The lender will then perform a hard credit inquiry, which might slightly ding your credit score temporarily. However, multiple inquiries for the same type of loan within a short period (typically 14-45 days, depending on the scoring model) are usually treated as a single inquiry, so rate shopping won’t significantly harm your score.

Understanding the Offer

When you receive loan offers, carefully review all terms: the interest rate (APR), the loan term, the total amount to be repaid, and any fees. Don’t just focus on the monthly payment. A lower monthly payment might be attractive, but it could come with a longer term and significantly more interest over the life of the loan. Compare offers side-by-side to determine which one truly provides the best value for your $23,000 car loan.

Strategies for Boosting Your $23,000 Car Loan Approval Chances

Even if your financial situation isn’t perfect, there are proactive steps you can take to significantly improve your chances of securing a favorable $23,000 car loan.

Improve Your Credit Score

This is fundamental. Paying bills on time, reducing existing credit card balances, and avoiding new credit applications in the months leading up to your car loan application can boost your score. Even a few points can make a difference in your interest rate. For a deeper dive, check out our article on .

Save for a Larger Down Payment

As discussed, a substantial down payment reduces the risk for lenders and lowers your loan amount. Aim for at least 10% of the car’s price, and ideally 20% or more. This not only makes you a more attractive borrower but also decreases your monthly financial burden.

Consider a Co-signer

If your credit score is low or your income is borderline, a co-signer with excellent credit and a stable income can significantly strengthen your application. The co-signer essentially guarantees the loan, taking on equal responsibility for repayment if you default. This can unlock approval and potentially better interest rates, but it’s a serious commitment for both parties.

Pay Down Existing Debt

Reducing your overall debt, especially high-interest credit card debt, improves your debt-to-income ratio. This shows lenders that you manage your finances responsibly and have more available income to dedicate to a new car payment. Prioritizing debt reduction before applying is a smart financial move.

Be Realistic About the Car You Can Afford

While a $23,000 car loan opens up many options, ensure the car you choose truly fits your budget. Remember to factor in not just the loan payment, but also insurance, fuel, maintenance, and registration. Don’t stretch your finances to the limit; leave some wiggle room for unexpected expenses.

Common Mistakes to Avoid When Seeking a $23,000 Car Loan

Securing an auto loan is a significant financial decision, and making the wrong moves can cost you hundreds or even thousands of dollars. Common mistakes to avoid are crucial to understand before you commit.

Firstly, not checking your credit report before applying is a major oversight. Errors on your report can unfairly lower your score, leading to higher interest rates or even denial. Always review your report for accuracy and dispute any discrepancies.

Secondly, only applying to one lender (typically the dealership’s finance department) limits your options. You might miss out on significantly better interest rates from banks or credit unions. Always shop around for pre-approvals to compare offers.

Another pitfall is ignoring the total cost of the loan and focusing solely on the monthly payment. A low monthly payment might seem appealing, but if it’s spread over 84 months with a high interest rate, you’ll pay much more in the long run. Always ask for the total amount repaid over the loan term.

Furthermore, extending the loan term too much (e.g., 72 or 84 months) to achieve a lower monthly payment is a common trap. While it reduces your immediate burden, it drastically increases the total interest paid and can put you in an "upside-down" position where you owe more than the car is worth, especially in the early years.

Finally, buying more car than you can afford is a mistake many buyers make. Just because you’re approved for a $23,000 car loan doesn’t mean you should spend that much. Stick to your budget, including all associated costs, to avoid financial strain down the road.

Managing Your $23,000 Car Loan After Approval

Once you’ve secured your $23,000 car loan and driven off the lot, the financial journey isn’t over. Responsible loan management is key to maintaining your financial health and ensuring a smooth repayment process.

Making Timely Payments

This is the most critical aspect of managing any loan. Set up automatic payments or create calendar reminders to ensure you never miss a due date. Late payments can incur fees, negatively impact your credit score, and potentially lead to default. Consistent, on-time payments will build positive credit history and make future borrowing easier.

Understanding Your Loan Agreement

Before you sign, meticulously read and understand every clause in your loan agreement. Pay attention to the Annual Percentage Rate (APR), the total amount financed, the payment schedule, any prepayment penalties, and what constitutes a default. Knowing your rights and obligations is paramount. If anything is unclear, ask questions until you fully comprehend the terms.

Refinancing Options

Life circumstances change, and so do interest rates. If your credit score has significantly improved since you first took out your $23,000 car loan, or if market interest rates have dropped, you might be able to refinance. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can save you a substantial amount of money over the life of the loan.

The Importance of Insurance

Auto insurance is not just a legal requirement; it’s a critical component of protecting your investment. If your car is damaged or stolen, comprehensive and collision coverage will protect both you and the lender. Most lenders require full coverage insurance on financed vehicles. Factor the cost of insurance into your overall budget, as it can be a significant monthly expense.

Special Considerations for a $23,000 Car Loan

While the core principles of auto financing remain consistent, certain situations warrant specific attention when seeking a $23,000 car loan.

Bad Credit Options

If your credit score is less than ideal, securing a $23,000 car loan can be more challenging, but it’s not impossible. Expect higher interest rates, as lenders perceive a greater risk. You might need to make a larger down payment, accept a shorter loan term to reduce risk, or consider a co-signer. Some lenders specialize in bad credit auto loans, but be wary of predatory rates and terms. Always compare offers carefully and ensure you can genuinely afford the payments.

New vs. Used Cars

A $23,000 car loan can finance a new entry-level vehicle or a well-appointed used car. New cars typically come with lower interest rates (especially with manufacturer incentives) but depreciate rapidly. Used cars, while having potentially higher interest rates, offer more value for your money as they’ve already taken the biggest depreciation hit. The choice depends on your priorities: the latest features and warranty of a new car versus the cost savings and potentially better features of a used one for the same price.

The Role of Trade-ins

If you have an existing vehicle, trading it in can act as a down payment for your new $23,000 car loan. This reduces the amount you need to borrow and can simplify the transaction. Get an appraisal for your trade-in from multiple sources (dealerships, online valuation tools like Kelley Blue Book or Edmunds) to ensure you’re getting a fair price. A good trade-in value can significantly ease the financial burden of your new car.

For external insights into managing your credit, you can refer to resources like the Consumer Financial Protection Bureau (CFPB) or reputable credit reporting agencies such as Experian for detailed guides on understanding and improving your credit score.

Conclusion: Driving Towards Financial Confidence

Securing a $23,000 car loan is a significant step, but with the right knowledge and preparation, it can be a smooth and rewarding experience. By understanding the factors lenders consider, diligently preparing your application, and proactively managing your loan, you empower yourself to make sound financial decisions. Remember, the goal isn’t just to get approved, but to secure terms that align with your financial health and future goals.

Take the time to research, compare offers, and ask questions. A well-informed borrower is a confident borrower. With these strategies in hand, you’re now better equipped to navigate the complexities of auto financing and drive away with a vehicle that perfectly fits your needs and budget. Happy driving!