Navigating the Road: Your Comprehensive Guide to Getting a Small Car Loan With Bad Credit

Navigating the Road: Your Comprehensive Guide to Getting a Small Car Loan With Bad Credit Carloan.Guidemechanic.com

Finding yourself in need of reliable transportation, but facing the hurdle of a less-than-perfect credit score? You’re not alone. Millions of people encounter this challenge, and the idea of securing any loan, let alone a car loan, can feel daunting when your credit history isn’t pristine. The good news? Getting a small car loan with bad credit is absolutely possible. It requires strategic planning, a clear understanding of the process, and a proactive approach.

This comprehensive guide is designed to empower you with the knowledge and strategies needed to navigate the complexities of bad credit auto financing. We’ll dive deep into everything from understanding your credit to finding the right lenders and, ultimately, driving away in a vehicle that fits your budget and needs. Our goal is to provide real value, helping you not only secure a loan but also to use this opportunity to rebuild your financial standing.

Navigating the Road: Your Comprehensive Guide to Getting a Small Car Loan With Bad Credit

Understanding Bad Credit and Its Impact on Car Loans

Before we explore solutions, it’s crucial to understand what "bad credit" signifies in the eyes of lenders and how it influences your loan prospects. Your credit score is essentially a numerical representation of your creditworthiness, a grade on how reliably you’ve managed debt in the past.

What Constitutes "Bad Credit"?

Credit scores typically range from 300 to 850. While the exact thresholds can vary slightly between credit bureaus (Experian, Equifax, TransUnion) and scoring models (FICO, VantageScore), a score below 600-620 is generally considered "bad" or "subprime." This indicates a higher perceived risk for lenders.

Based on my experience, many people misunderstand that a bad credit score isn’t a life sentence. It simply means that lenders will approach your application with more caution. They see a history that suggests a higher likelihood of missed payments or default, making them hesitant to offer standard loan terms.

Why Lenders Are Hesitant and What That Means for You

When you apply for an auto loan with bad credit, lenders perceive a greater risk of default. To offset this increased risk, they typically adjust the loan terms in a few key ways. This isn’t meant to punish you, but rather to protect their investment.

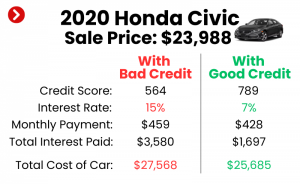

The reality is that you’ll likely face higher interest rates compared to someone with excellent credit. This translates to higher monthly payments and a greater total cost over the life of the loan. Additionally, lenders might require a larger down payment, a shorter loan term, or even a co-signer to mitigate their risk. Understanding these implications upfront will help you set realistic expectations and prepare effectively.

Is Getting a Small Car Loan with Bad Credit Truly Possible? (Yes, and Here’s How)

The short answer is a resounding "yes." While challenging, securing a small car loan with bad credit is a common scenario that many individuals successfully navigate. The key differentiator here is often the small car loan aspect.

A smaller loan amount for an affordable vehicle significantly reduces the risk for lenders. This makes them more willing to consider applicants with less-than-perfect credit. You’re demonstrating a practical approach by seeking a functional, cost-effective car rather than an expensive, high-risk purchase. This focus on a smaller, more manageable loan is your first strategic advantage in this process.

Essential Preparatory Steps Before You Apply

Preparation is paramount when seeking a car loan with bad credit. Rushing into applications without understanding your financial standing or what lenders expect can lead to multiple rejections, further damaging your credit score through hard inquiries.

Know Your Credit Score and Report Inside Out

This is the absolute first step you must take. Don’t guess; know. Your credit report contains detailed information about your borrowing history, and your credit score is derived from this data.

Pro tips from us: You are legally entitled to a free copy of your credit report from each of the three major credit bureaus once every 12 months. Visit AnnualCreditReport.com – it’s the only federally authorized source for free credit reports. Don’t use look-alike sites.

Once you have your reports, review them meticulously. Look for any inaccuracies, errors, or outdated information. Even a single error, like a wrongly reported late payment or an account that isn’t yours, can negatively impact your score. Disputing these errors and having them removed can provide a quick, albeit sometimes slight, boost to your credit score, making a difference in your loan eligibility and interest rate. Understanding what lenders see will help you anticipate their concerns.

Define Your Budget Realistically

It’s tempting to dream about a shiny new car, but with bad credit, realism is your best friend. Your budget needs to encompass more than just the monthly car payment. Consider insurance costs, fuel expenses, routine maintenance, and potential repair costs, especially for a used vehicle.

Common mistakes to avoid are overestimating what you can truly afford each month. Lenders will look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A high DTI can signal that you’re already overextended, making lenders hesitant. Create a detailed monthly budget to determine how much you can comfortably allocate to a car loan without straining your finances. This demonstrates financial responsibility and helps you avoid future payment struggles.

Save for a Down Payment

A down payment is one of the most powerful tools you have when applying for a car loan with bad credit. It directly reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

More importantly, a significant down payment signals to lenders that you are serious about the purchase and have a vested interest in keeping up with payments. It reduces their risk exposure, making them much more likely to approve your application and potentially offer a better interest rate. While 10-20% of the car’s value is often recommended for those with good credit, for bad credit applicants, aiming for as much as you can comfortably afford – even 25% or more – can significantly improve your chances. Every dollar you put down lessens the burden on the lender and on your future self.

Strategies to Increase Your Approval Chances

With your preparation complete, it’s time to explore specific strategies that can bolster your loan application and make you a more attractive borrower, even with bad credit. These approaches demonstrate your commitment and help mitigate the lender’s perceived risk.

Consider a Co-signer

A co-signer can be a game-changer for individuals with bad credit seeking an auto loan. A co-signer is someone, typically with good credit, who legally agrees to take responsibility for the loan if you fail to make payments.

Who makes a good co-signer? Ideally, it’s a trusted family member or friend with a strong credit history and stable income. Their good credit essentially "backs" your application, making lenders feel more secure. This can significantly increase your chances of approval and often lead to a lower interest rate than you’d get on your own. However, it’s vital to understand the risks for both parties. If you default, the co-signer’s credit will be negatively impacted, and they will be legally obligated to repay the loan. Ensure you both fully understand this commitment before proceeding.

Explore Dealership Financing (Buy Here, Pay Here vs. Subprime Lenders)

Dealerships often have various financing options, and understanding the differences is crucial.

- Subprime Lenders (through dealerships): Many larger dealerships work with a network of traditional banks and specialized subprime lenders who are more willing to approve loans for borrowers with bad credit. While the interest rates will be higher, these loans can still offer reasonable terms and help you rebuild credit. The dealership acts as an intermediary, submitting your application to multiple lenders to find the best possible offer. From my observations, many consumers gravitate towards this option because it’s convenient and offers a range of vehicles.

- Buy Here, Pay Here (BHPH) Dealerships: These dealerships act as both the seller and the lender, meaning you make your payments directly to them. They are often a "last resort" option for those with very poor credit, as they focus less on your credit score and more on your income and ability to pay. While they offer high approval rates, common mistakes to avoid are the extremely high interest rates, limited vehicle selection, and often less transparent terms. Always read the fine print carefully and understand the total cost before committing to a BHPH loan.

Seek Out Online Lenders Specializing in Bad Credit Auto Loans

The digital age has brought forth a multitude of online lenders who specialize in bad credit auto loans. These platforms often have a broader reach and can connect you with lenders who might not be accessible through traditional banks or local dealerships.

The advantages include convenience, the ability to compare multiple offers from various lenders from the comfort of your home, and potentially more flexible lending criteria. Many online lenders use alternative data points beyond just your credit score to assess your creditworthiness. Pro tip: Always check reviews and Better Business Bureau (BBB) ratings for any online lender before providing personal information or committing to a loan. Look for transparency in their rates and terms to avoid predatory lenders.

Focus on a More Affordable, Used Small Car

This strategy ties directly into reducing lender risk and increasing your approval odds. Common mistakes to avoid are trying to finance a brand-new, expensive vehicle with bad credit. The higher the car’s price tag, the larger the loan amount, and consequently, the greater the risk for the lender.

By focusing on a reliable, used small car, you significantly lower the principal loan amount. This makes your monthly payments more manageable and signals to lenders that you are making a financially responsible decision. A smaller loan is inherently less risky for them, making them more inclined to approve your application. Prioritize practicality and reliability over luxury when you have bad credit; this purchase is primarily about getting from point A to point B and rebuilding your credit.

Improve Your Credit Score (Even Slightly)

While getting a loan with bad credit is the goal, taking steps to improve your credit score, even modestly, before you apply can yield better loan terms. Every point counts!

Short-term strategies:

- Dispute errors: As mentioned earlier, correcting inaccuracies on your credit report can provide a quick boost.

- Pay down small debts: If you have any outstanding small balances on credit cards or other loans, paying them off can reduce your credit utilization ratio, which positively impacts your score.

- Become an authorized user: If a trusted family member has excellent credit, they might add you as an authorized user on one of their credit cards. Their positive payment history can then reflect on your report.

Long-term strategies: Consistent on-time payments for all your existing debts are the most effective way to rebuild credit. Even a few months of perfect payment history can make a difference. For more detailed steps on improving your credit, check out our guide on .

The Application Process: What to Expect

Once you’ve done your homework and chosen your strategy, it’s time to apply. Understanding this phase will help you navigate it smoothly and confidently.

The Importance of Pre-approval

Seeking pre-approval is a smart move. It allows you to get an idea of how much you can borrow, the potential interest rate, and the loan terms before you even step foot on a dealership lot. This gives you significant leverage during negotiations and helps you set realistic expectations for your car search.

Pre-approval often involves a soft credit inquiry, which doesn’t harm your credit score. Once you’re ready to commit, the lender will perform a hard inquiry. Having pre-approval in hand transforms you from a speculative buyer into a qualified one, which is particularly beneficial when dealing with bad credit.

Required Documents

Lenders need to verify your identity, income, and residence to assess your ability to repay the loan. Be prepared to provide:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (typically 1-3 months), bank statements, or tax returns if self-employed.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- References: Sometimes required, especially for subprime or BHPH lenders.

Having these documents organized and ready will streamline the application process and show the lender you are prepared and serious.

Understanding Loan Terms: APR, Loan Term, and Fees

When you receive a loan offer, it’s critical to understand every component.

- APR (Annual Percentage Rate): This is the true cost of borrowing, expressed as a yearly percentage. It includes the interest rate plus any fees. For bad credit loans, APRs will be higher, so compare offers carefully.

- Loan Term: This is the length of time you have to repay the loan, typically in months (e.g., 36, 48, 60 months). A longer loan term means lower monthly payments but results in paying more interest over time. A shorter term means higher monthly payments but less overall interest paid.

- Fees: Be aware of any origination fees, processing fees, or other charges that might be added to the loan amount. These can significantly increase the total cost.

Reading the fine print is not just a suggestion; it’s a necessity. Don’t hesitate to ask questions about anything you don’t understand. Ensure you’re comfortable with all terms before signing.

Post-Approval: Managing Your Loan and Rebuilding Credit

Getting approved for a small car loan with bad credit is a significant achievement. However, the journey doesn’t end there. This loan is a powerful tool for credit rebuilding, but only if managed correctly.

Make Payments On Time, Every Time

This cannot be stressed enough. Your payment history is the single most influential factor in your credit score. Every on-time payment you make will be reported to the credit bureaus and will gradually improve your score.

Set up automatic payments if possible, or create reminders to ensure you never miss a due date. This consistency is the cornerstone of rebuilding your credit and demonstrating financial responsibility.

Avoid Missing Payments

Conversely, missing payments can severely damage your credit score, undoing all your hard work. Even a single late payment can stay on your credit report for up to seven years and negatively impact your score for months or even years. If you anticipate difficulty making a payment, contact your lender immediately to discuss your options. They may be willing to work with you, but only if you communicate proactively.

Consider Refinancing Later

Once you’ve made 6-12 months of consistent, on-time payments, your credit score will likely have improved. At this point, you might be eligible to refinance your car loan at a lower interest rate. Refinancing can significantly reduce your monthly payments and the total amount of interest you pay over the life of the loan. It’s a smart strategy to save money and continue your credit rebuilding journey. Learn more about the benefits of refinancing in our article: .

Common Pitfalls and How to Avoid Them

Even with all the preparation, the car buying and loan process can have hidden traps. Being aware of these common pitfalls will help you protect yourself.

High-Pressure Sales Tactics

Dealerships, especially those catering to bad credit, might employ high-pressure sales tactics to rush you into a decision. They might push you towards a car you can’t truly afford or add unnecessary extras. Remember, you have the right to take your time, ask questions, and walk away if you feel uncomfortable. Don’t let emotion override sound financial judgment.

Hidden Fees and Unnecessary Add-ons

Always scrutinize the final contract for hidden fees, extended warranties, paint protection, or other add-ons you didn’t ask for or don’t need. These can inflate the total loan amount and increase your monthly payments. Negotiate these items individually and only accept what truly adds value.

Ignoring the APR

Focusing solely on the monthly payment can be misleading. A lower monthly payment might simply mean a longer loan term and a much higher total interest paid over time. Always compare the APR (Annual Percentage Rate) across different loan offers. The APR gives you the most accurate picture of the true cost of borrowing. For an in-depth understanding of loan terms, refer to the Consumer Financial Protection Bureau’s guide on .

Not Reading the Contract Thoroughly

This is perhaps the most crucial advice. Before you sign anything, read the entire loan agreement and purchase contract from start to finish. Understand every clause, every number, and every commitment. If something is unclear, ask for clarification. A signed contract is legally binding, so ensure you fully comprehend what you’re agreeing to.

Conclusion: Your Path to a Small Car Loan and Better Credit

Securing a small car loan with bad credit is not merely about getting a vehicle; it’s a strategic step towards financial recovery and establishing a stronger credit profile. While the journey presents unique challenges, it is absolutely achievable with careful planning, diligent research, and a commitment to responsible financial management.

By understanding your credit, preparing thoroughly, exploring all available lending avenues, and making every payment on time, you can transform a necessary purchase into an opportunity to rebuild your credit. This journey requires patience and persistence, but the rewards of reliable transportation and an improved financial future are well worth the effort. Start preparing today, drive smart, and pave your way to better credit.