Navigating the Rocky Roads: Your Expert Guide to Car Loans in Colorado

Navigating the Rocky Roads: Your Expert Guide to Car Loans in Colorado Carloan.Guidemechanic.com

The majestic landscapes of Colorado beckon, and for many, exploring them requires a reliable set of wheels. Whether you’re commuting through Denver’s bustling streets, hitting the slopes near Aspen, or embarking on a scenic drive through the Rockies, a car is often an indispensable part of life here. But for most Coloradans, acquiring that vehicle involves securing a car loan. This isn’t just a simple transaction; it’s a financial journey that requires careful planning, understanding, and strategic decision-making.

As an expert blogger and professional SEO content writer who has navigated the intricacies of auto financing for years, I understand the unique landscape of car loans. My mission in this comprehensive guide is to equip you with all the knowledge you need to confidently secure the best possible Car Loan in Colorado. We’ll delve deep into every facet, from understanding your credit to choosing the right lender, ensuring you’re empowered to make informed choices.

Navigating the Rocky Roads: Your Expert Guide to Car Loans in Colorado

Why Colorado Car Loans Deserve Special Attention

While the fundamental principles of car loans are universal, applying them in Colorado comes with its own nuances. State-specific taxes, registration processes, and even the types of vehicles popular here (think SUVs and trucks for mountain adventures) can subtly influence your financing journey. Understanding these local factors is crucial for a smooth and cost-effective purchase.

This article isn’t just about getting any car loan; it’s about getting the right car loan for you in Colorado. Let’s embark on this detailed exploration together.

Understanding the Anatomy of a Car Loan in Colorado

Before you even start browsing dealerships or online listings, it’s vital to grasp the core components of any auto loan. Knowing these terms will help you compare offers effectively and avoid common pitfalls.

Types of Car Loans

In Colorado, just like elsewhere, you’ll encounter several common types of auto loans:

- New Car Loans: These are for brand-new vehicles straight from the dealership. They often come with lower interest rates due to the car’s higher value and longer expected lifespan.

- Used Car Loans: For pre-owned vehicles, these loans can have slightly higher interest rates than new car loans, reflecting the vehicle’s depreciation and potential wear.

- Refinance Car Loans: If you already have a car loan but believe you can get a better rate or more favorable terms, refinancing allows you to replace your existing loan with a new one. This is a powerful tool for saving money over time.

- Private Party Car Loans: Buying from an individual rather than a dealership often requires a specific type of loan. Lenders may have stricter requirements for these loans, as the vehicle’s condition might not be professionally vetted.

Key Loan Components You Must Know

Every car loan boils down to a few fundamental elements that dictate how much you’ll pay and for how long.

- Principal: This is the actual amount of money you borrow to purchase the vehicle. It’s the car’s selling price minus any down payment or trade-in value.

- Interest Rate (APR): The Annual Percentage Rate (APR) is the cost of borrowing money, expressed as a percentage. A lower APR means you’ll pay less in interest over the life of the loan. This is one of the most critical factors to compare.

- Loan Term: This refers to the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). While longer terms mean lower monthly payments, they also mean paying more interest overall.

- Down Payment: This is the initial cash amount you pay towards the car’s purchase price. A larger down payment reduces the principal amount borrowed, which can lead to lower monthly payments and less interest paid over time.

- Fees and Charges: Be aware of potential origination fees, documentation fees, or other charges that might be added to your loan or purchase price. Always ask for a clear breakdown.

The Strategic Steps to Securing a Car Loan in Colorado

Getting a car loan isn’t a single event; it’s a multi-step process that, when executed strategically, can save you thousands of dollars. Based on my experience, rushing through these steps is a common mistake.

Step 1: Understand Your Credit Score and Report

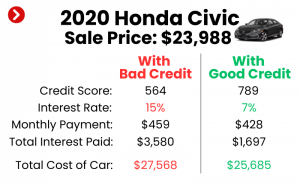

Your credit score is arguably the single most influential factor in determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness – essentially, how risky you are as a borrower.

- Why it Matters: A higher credit score (generally above 670) indicates a responsible borrowing history and will qualify you for the most competitive interest rates. Lower scores, conversely, signal higher risk and result in higher interest rates.

- How to Check: You are entitled to a free credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) once every 12 months via AnnualCreditReport.com. Reviewing these reports is crucial to identify any errors that could be dragging down your score.

- What Lenders Look For: Beyond the score, lenders examine your payment history, the amount of debt you carry, the length of your credit history, and your credit mix. A consistent record of on-time payments across various credit types is ideal.

Step 2: Budgeting and Determining Affordability

Before falling in love with a specific car, establish a realistic budget. This involves more than just the monthly loan payment.

- Beyond the Monthly Payment: Consider insurance costs, fuel, maintenance, and potential registration fees unique to Colorado. A car loan payment might seem manageable, but the total cost of ownership can quickly add up.

- The 20/4/10 Rule (A Pro Tip from Us!): A common guideline suggests a 20% down payment, a loan term no longer than four years (48 months), and car expenses (payment, insurance, fuel) not exceeding 10% of your gross monthly income. While this is a guideline, it’s an excellent starting point for determining affordability.

- Debt-to-Income (DTI) Ratio: Lenders also look at your DTI ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%) makes you a more attractive borrower.

Step 3: Accumulate a Down Payment and Assess Trade-in Value

A substantial down payment is one of the most powerful tools you have to reduce your overall loan cost and improve your chances of approval.

- Benefits of a Down Payment: It lowers the amount you need to borrow, reduces your monthly payments, and decreases the total interest paid. It also helps avoid being "upside down" on your loan, meaning you owe more than the car is worth, a common scenario with rapidly depreciating assets.

- Trade-in: If you have an existing vehicle, getting an accurate trade-in value is essential. Research its value on sites like Kelley Blue Book or Edmunds before heading to the dealership. Knowing its worth puts you in a stronger negotiating position.

Step 4: Get Pre-Approved for Your Car Loan

This step is perhaps the most overlooked yet critical phase of the car buying process. Common mistakes to avoid are walking into a dealership without a pre-approval in hand.

- Empowerment through Pre-Approval: Pre-approval gives you a clear understanding of how much you can borrow, at what interest rate, and for what term before you even set foot on a car lot. This turns you into a cash buyer, shifting the focus from "Can I afford this?" to "Do I want this?"

- Shopping for Rates: Apply for pre-approval with multiple lenders – banks, credit unions, and online lenders. This allows you to compare offers without obligation. Because credit inquiries for auto loans within a short period (typically 14-45 days, depending on the credit bureau) are often treated as a single inquiry, it won’t significantly harm your score to shop around.

Step 5: Choose the Right Lender for Your Needs

Colorado offers a diverse landscape of lending options, each with its own advantages.

- Banks: Large national and regional banks often provide competitive rates, especially for borrowers with excellent credit. They offer convenience and a wide range of financial services.

- Credit Unions: Pro tips from us: Don’t overlook credit unions! They are member-owned, often offer lower interest rates, and can be more flexible, especially for those with less-than-perfect credit. Many Colorado communities have excellent local credit unions worth exploring.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer streamlined online applications and quick decisions. They can be very competitive and convenient.

- Dealership Financing: While convenient, dealership financing (often through captive lenders like Ford Credit or GM Financial) may not always offer the best rates unless they have special promotions. Always compare their offer against your pre-approvals.

Step 6: Gather Your Documents

Once you’ve chosen a lender and a vehicle, you’ll need to finalize the loan. Be prepared with the necessary documentation.

- Typical Requirements: This usually includes government-issued ID, proof of income (pay stubs, tax returns), proof of residence (utility bill), and proof of insurance. For some loans, you might also need bank statements or employment verification.

Navigating Car Loans with Different Credit Scores in Colorado

Your credit score plays a monumental role. Here’s how to approach financing based on your credit standing.

Excellent to Good Credit (700+)

If your credit score falls into this range, congratulations! You’re in a prime position to secure the lowest interest rates available.

- Strategy: Shop aggressively among banks, credit unions, and online lenders. Leverage your strong credit to negotiate not just the car price but also the loan terms. Aim for the shortest loan term you can comfortably afford to minimize interest payments.

Fair to Average Credit (600-699)

Many Coloradans fall into this category. While not stellar, it’s certainly manageable, and good rates are still within reach.

- Strategy: Focus on improving your score before applying if possible. Pay down existing debt, correct any errors on your credit report. A larger down payment can significantly help mitigate the lender’s perceived risk. Credit unions can often be more accommodating for fair credit borrowers.

Bad Credit Car Loans Colorado (Below 600)

Having bad credit doesn’t mean you can’t get a car loan in Colorado, but it will require a different approach and potentially higher costs.

- Realistic Expectations: Expect higher interest rates and potentially shorter loan terms. Your monthly payments might be higher, and the total cost of the loan will be greater.

- Options for Bad Credit:

- Subprime Lenders: These specialize in lending to borrowers with lower credit scores. While their rates are higher, they offer a path to vehicle ownership.

- Co-Signer: A co-signer with good credit can significantly improve your chances of approval and secure a better interest rate. The co-signer is equally responsible for the debt, so choose wisely.

- Larger Down Payment: This is crucial for bad credit borrowers. It reduces the loan amount and shows the lender your commitment.

- Secured Loans: Some lenders might offer "secured" auto loans where collateral (like another vehicle or savings) is used to back the loan, reducing risk for the lender.

- Buy Here, Pay Here Dealerships: These dealerships offer in-house financing, often without a credit check. However, they typically come with very high interest rates and limited vehicle selection. Use these as a last resort.

- Building Credit: Based on my experience, securing a bad credit car loan and making all payments on time is an excellent way to rebuild your credit score over time, paving the way for better rates in the future.

No Credit History

If you’re new to credit, getting your first car loan can be challenging but not impossible.

- Strategy: A co-signer is often the easiest path. Alternatively, look for lenders specializing in first-time buyers, usually requiring a substantial down payment. Some credit unions have programs for individuals building credit.

Refinancing Your Car Loan in Colorado

Even after you’ve secured a loan, your financial journey isn’t necessarily over. Refinancing can be a game-changer.

- When to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you took out your original loan.

- Lower Interest Rates: If market interest rates have dropped.

- High Original Rate: If you had bad credit initially and secured a high-interest loan.

- Desire for Lower Payments: To extend your loan term (though this means more interest overall).

- Desire for Shorter Term: To pay off your car faster and save on interest.

- Benefits: Lower monthly payments, lower total interest paid, or a shorter loan term.

- Process: Similar to the initial application, you’ll apply to various lenders for a new loan. If approved, the new lender pays off your old loan, and you begin making payments to them under the new terms.

Key Factors Influencing Your Car Loan Offer in Colorado

Beyond your credit score, several other variables play a significant role in the loan offer you receive.

- Current Interest Rate Environment: Macroeconomic factors, like the Federal Reserve’s interest rate policies, directly impact the rates lenders can offer. When rates are generally low, it’s a good time to borrow.

- Loan Term: As discussed, longer terms mean lower monthly payments but more interest paid over the loan’s life. Shorter terms mean higher payments but significant interest savings.

- Vehicle Type and Age: Lenders often view newer vehicles as less risky because they hold their value better and are less prone to immediate mechanical issues. Older, higher-mileage vehicles typically come with higher interest rates.

- Your Financial Profile: Beyond your credit score, lenders assess your income stability, employment history, and existing debt obligations. A stable job and a low DTI ratio are highly favorable.

Colorado-Specific Considerations for Car Buyers

While financing is a major hurdle, remember there are state-specific costs associated with car ownership in Colorado.

- Colorado Sales Tax: The state sales tax on vehicles is 2.9%. However, local jurisdictions (cities, counties, special districts) can add their own sales taxes, which can push the combined rate significantly higher depending on where you purchase and register the vehicle. For example, in Denver, the total sales tax rate is much higher. Always verify the exact rate for your specific location.

- Vehicle Registration Fees: Colorado’s registration fees are based on the vehicle’s taxable value, age, and weight. Newer, more expensive vehicles will incur higher registration fees. These are typically paid annually to the county clerk and recorder.

- Title Transfer Fees: There’s a small fee to transfer the vehicle’s title into your name, ensuring legal ownership.

- Emissions Testing: Vehicles registered in specific Front Range counties (like Denver, Boulder, Adams, Arapahoe, Douglas, and parts of others) are required to undergo emissions testing before registration or renewal. Factor this small cost into your budget.

- Lemon Laws: Colorado has consumer protection laws (often called "Lemon Laws") that provide recourse for buyers of new vehicles with significant, unfixable defects. While not directly related to loans, it’s an important protection to be aware of. For details, you can refer to

.

Pro Tips for Securing the Best Car Loan in Colorado

Armed with knowledge, let’s distill it into actionable advice.

- Always Shop Around for Rates: This cannot be emphasized enough. Get pre-approvals from at least 3-5 different lenders (banks, credit unions, online) before you step into a dealership. This creates competition and gives you leverage.

- Boost Your Credit Score: Even a few points can make a difference. Pay bills on time, reduce credit card balances, and dispute any inaccuracies on your report.

- Make a Substantial Down Payment: Aim for 20% or more, especially for a new car. It significantly reduces your loan amount and interest costs.

- Understand the Fine Print: Don’t just look at the monthly payment. Read the entire loan agreement, paying attention to the APR, loan term, any prepayment penalties, and late fees. Ask questions until everything is clear.

- Avoid Unnecessary Add-ons: Dealerships often offer extended warranties, GAP insurance (Guaranteed Asset Protection), and other products. While some can be valuable, others are highly marked up. Research their necessity and cost before adding them to your loan. Consider getting GAP insurance from your auto insurer or a third party, as it’s often cheaper.

Common Mistakes to Avoid When Getting a Car Loan in Colorado

Knowing what not to do is just as important as knowing what to do. Based on my experience, these are frequent missteps:

- Not Checking Your Credit Report: Neglecting to review your credit report for errors can cost you a better interest rate. A simple mistake could be impacting your eligibility.

- Focusing Only on the Monthly Payment: A low monthly payment might seem attractive, but it often comes with a longer loan term and significantly more interest paid over time. Always consider the total cost of the loan.

- Skipping Pre-Approval: Going to the dealership without a pre-approval means you’re negotiating blind. The dealership controls the financing narrative, and you lose your leverage.

- Ignoring the Total Cost of Ownership: Beyond the loan, factor in insurance, maintenance, fuel, and Colorado-specific fees. A car that seems affordable on paper might be a budget-buster in reality.

- Falling for High-Pressure Sales Tactics: Take your time. Don’t feel rushed into a decision. If a deal feels too good to be true, it probably is. Walk away if you feel pressured or uncomfortable.

- Not Budgeting for Colorado Taxes and Fees: Many people forget about the state and local sales tax, registration, and title fees, which can add hundreds or even thousands to the upfront cost.

Your Journey to a Colorado Car Loan Starts Now

Securing a Car Loan in Colorado doesn’t have to be a daunting task. By understanding the fundamentals, preparing diligently, and approaching the process strategically, you can confidently navigate the market and drive away with a vehicle that fits your needs and your budget. Remember, knowledge is your most powerful tool in this journey.

Start by checking your credit, setting a realistic budget, and getting pre-approved. With these steps, you’ll be well on your way to enjoying all the beautiful sights and adventures that Colorado has to offer, from the driver’s seat of your new (or new-to-you) car.