Navigating the Used Car Market: Your Ultimate Guide to the Bankrate Used Car Loan Calculator

Navigating the Used Car Market: Your Ultimate Guide to the Bankrate Used Car Loan Calculator Carloan.Guidemechanic.com

Buying a used car can be an exciting yet daunting prospect. The allure of a great deal, the reduced depreciation, and the sheer variety of options often make pre-owned vehicles a smart choice for many. However, the financial planning involved – especially securing the right loan – can quickly turn that excitement into apprehension. How do you know what you can truly afford? What will your monthly payments look like? These are critical questions that, if left unanswered, can lead to financial stress down the road.

This is precisely where the Bankrate Used Car Loan Calculator becomes your indispensable financial navigator. It’s more than just a simple tool; it’s a powerful ally designed to demystify the complexities of used car financing, empowering you to make informed decisions with confidence. In this comprehensive guide, we’ll dive deep into every facet of this calculator, showing you how to leverage its full potential to secure a used car loan that perfectly fits your budget and financial goals.

Navigating the Used Car Market: Your Ultimate Guide to the Bankrate Used Car Loan Calculator

Why a Used Car? The Smart Choice for Many

Before we delve into the numbers, let’s briefly consider why a used car often represents a prudent financial decision. New cars notoriously depreciate rapidly the moment they drive off the lot, losing a significant chunk of their value in the first few years. Opting for a used vehicle allows you to bypass this initial steep depreciation, essentially letting someone else absorb that cost.

This means you can often get more car for your money, potentially affording a higher trim level or a more luxurious model than you could if buying new. Additionally, insurance rates for used cars are typically lower, and sales tax might be less depending on your location. These combined savings free up more of your budget, making careful loan planning even more impactful.

Understanding the Used Car Loan Landscape

Securing a loan for a used car isn’t quite the same as financing a new one. Lenders often view used vehicles as having a higher risk profile due to factors like age, mileage, and potential for unforeseen repairs. This can influence the interest rates and loan terms available to you.

Several key factors will play a significant role in determining your used car loan terms:

- Your Credit Score: This is perhaps the most crucial element. A strong credit score signals reliability to lenders, often resulting in lower interest rates.

- The Car’s Age and Mileage: Older cars or those with very high mileage might be subject to higher interest rates or shorter loan terms. Lenders want to ensure the car retains enough value throughout the loan period.

- Loan Term: The length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but less total interest paid. Longer terms offer lower monthly payments but accumulate more interest over time.

- Down Payment: The amount of money you pay upfront. A larger down payment reduces the amount you need to borrow, saving you money on interest and potentially securing a better rate.

Navigating these variables manually can feel like guesswork. That’s why having a robust tool like the Bankrate Used Car Loan Calculator is so essential for accurate financial forecasting.

Introducing the Bankrate Used Car Loan Calculator: Your Financial Navigator

The Bankrate Used Car Loan Calculator is a sophisticated, yet incredibly user-friendly, online tool designed to help prospective used car buyers estimate their potential monthly loan payments. It allows you to input various financial details and instantly see how different scenarios impact your budget. Based on my experience as a financial blogger and an advocate for smart consumer choices, this calculator isn’t just a convenience; it’s a foundational step in responsible car buying.

Its primary purpose is to provide clarity. By allowing you to experiment with different loan amounts, interest rates, and terms, it helps you understand the true cost of financing a used car. This foresight is invaluable, preventing you from overcommitting financially and ensuring your car purchase remains a source of joy, not stress. It moves you from "I hope I can afford this" to "I know exactly what this will cost me."

How to Use the Bankrate Used Car Loan Calculator: A Step-by-Step Guide

Using the Bankrate Used Car Loan Calculator is straightforward, but maximizing its utility requires understanding each input field and its impact. Let’s break down the process step-by-step:

1. Input the Loan Amount

This is the core figure: how much money you actually need to borrow. It’s not simply the car’s sticker price. To arrive at an accurate loan amount, you’ll need to consider:

- The Used Car Price: This is your negotiated selling price for the vehicle.

- Your Down Payment: Subtract any money you plan to pay upfront. A larger down payment reduces the loan amount, leading to lower monthly payments and less interest paid over the life of the loan.

- Trade-in Value (if applicable): If you’re trading in your current vehicle, subtract its agreed-upon value from the car’s price.

- Sales Tax and Fees: Don’t forget these! Sales tax varies by state, and other fees might include registration, title, and dealer documentation fees. While some calculators might have separate fields for these, it’s often easiest to add them to your total purchase price before subtracting your down payment and trade-in.

Pro tip from us: Always get a solid estimate for all fees and taxes from the dealer or your local DMV before inputting your final loan amount. Overlooking these can lead to a significant difference in your actual monthly payment.

2. Enter the Estimated Interest Rate (APR)

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. For car loans, you’ll usually see this referred to as the Annual Percentage Rate (APR), which includes the interest rate plus certain fees charged by the lender.

- Your Credit Score is Key: This is the single biggest factor influencing your APR. Borrowers with excellent credit (typically 760+) will qualify for the lowest rates. Those with fair or poor credit will likely face higher rates.

- Research Current Rates: Before using the calculator, do some quick research on average used car loan rates for your credit tier. Bankrate itself offers current average rates, which can serve as a good starting point.

- Get Pre-Approved: The best way to know your actual interest rate is to get pre-approved by a few lenders (banks, credit unions, online lenders) before you go to the dealership. This gives you a concrete rate to plug into the calculator.

If you don’t have a pre-approval yet, use a realistic estimate based on your credit score. Running scenarios with slightly higher and lower rates can help you understand the range of possibilities.

3. Specify the Loan Term

The loan term is the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This choice has a significant impact on both your monthly payment and the total interest you’ll pay.

- Shorter Terms (e.g., 36-48 months): These result in higher monthly payments but significantly less total interest paid over the life of the loan. You pay off the car faster and build equity more quickly.

- Longer Terms (e.g., 60-72 months): These offer lower monthly payments, making the car seem more affordable on a month-to-month basis. However, you’ll pay substantially more in total interest over the longer period, and the car might depreciate faster than you pay it off, leading to negative equity.

Experiment with different loan terms in the calculator to see the trade-offs. Our advice is to aim for the shortest term you can comfortably afford, as this minimizes your overall cost of borrowing.

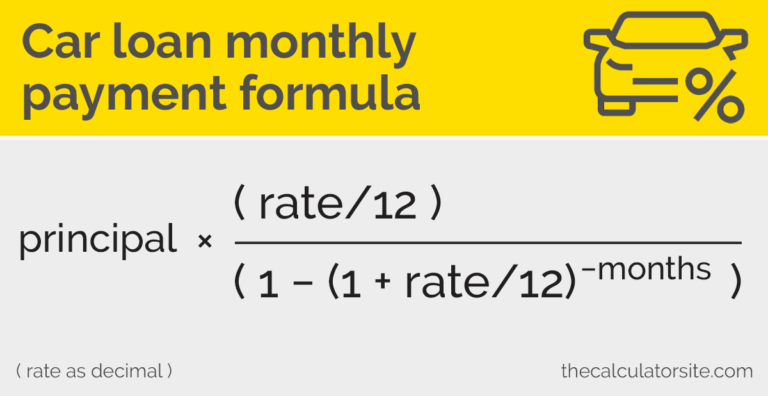

4. The Output: Your Estimated Monthly Payment and More

Once you’ve entered these details, the Bankrate Used Car Loan Calculator instantly generates your estimated monthly payment. But it doesn’t stop there. It also typically provides:

- Total Interest Paid: This is a crucial figure often overlooked. It shows you the true cost of borrowing the money, beyond just the principal amount.

- Total Cost of Loan: The sum of your principal loan amount plus the total interest paid.

Understanding these outputs thoroughly is key to making a truly informed decision. Don’t just focus on the monthly payment; consider the entire financial picture.

Beyond the Monthly Payment: What Else to Consider

While the Bankrate Used Car Loan Calculator provides an excellent foundation, a truly smart car purchase goes beyond just the loan figures. From years of observing car buyers, we know that overlooking these additional factors can quickly derail even the best-laid financial plans.

1. Total Cost of Ownership (TCO)

The monthly loan payment is just one piece of the puzzle. A car also comes with ongoing expenses:

- Insurance: Get quotes before you buy. Different makes and models, and even different years of the same model, can have wildly varying insurance premiums.

- Maintenance and Repairs: Used cars, by their nature, might require more maintenance than new ones. Factor in potential repair costs, especially for older or higher-mileage vehicles. A pre-purchase inspection by an independent mechanic is non-negotiable.

- Fuel: Consider the car’s fuel efficiency. A slightly cheaper car with poor MPG could end up costing you more in the long run.

- Registration and Licensing: Annual fees are a recurring cost.

Factor these into your overall monthly budget alongside your loan payment.

2. Your Budget & Debt-to-Income Ratio

Just because a lender approves you for a certain amount doesn’t mean you can comfortably afford it. Create a realistic monthly budget that accounts for all your income and expenses. Your car payment (plus insurance, fuel, etc.) shouldn’t consume too large a portion of your disposable income.

Lenders often look at your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A high DTI can indicate financial strain. Aim for a DTI under 36%, with your car payment making up no more than 10-15% of your gross income. This is a common mistake to avoid: letting the desire for a specific car override your financial common sense.

3. Pre-Approval vs. Dealer Financing

Always get pre-approved for a loan from your bank, credit union, or an online lender before visiting the dealership.

- Power of Negotiation: A pre-approval letter acts as cash in hand, giving you significant leverage in negotiations. You’re no longer just a "shopper" but a "buyer" with financing secured.

- Benchmark Rate: It provides a benchmark interest rate. If the dealership offers a higher rate, you know you have a better option. If they can beat it, even better!

- Focus on Car Price: With financing handled, you can focus solely on negotiating the car’s price, rather than getting tangled in a "payment shuffle" where dealers manipulate loan terms to make payments seem lower.

4. Credit Score’s Crucial Role

As mentioned, your credit score is paramount. Before you even start car shopping, pull your credit report and score.

- Check for Errors: Dispute any inaccuracies that could be dragging your score down.

- Improve Your Score: If your score is less than ideal, consider taking steps to improve it, such as paying down existing debt, making all payments on time, and avoiding new credit applications. Even a 50-point increase can significantly impact your interest rate, saving you hundreds or thousands of dollars over the life of the loan.

5. Understanding APR vs. Interest Rate

While often used interchangeably, it’s important to know the distinction. The interest rate is the percentage charged on the principal amount borrowed. The Annual Percentage Rate (APR) is the broader measure of the cost of borrowing money, including the interest rate plus any additional fees, such as origination fees. When comparing loan offers, always compare APRs for an apples-to-apples comparison.

6. The Power of a Down Payment

A solid down payment is one of your most effective tools for saving money and improving your financial position.

- Lower Monthly Payments: Reduces the amount you need to borrow.

- Less Total Interest: A smaller principal means less interest accrues over time.

- Better Loan Terms: Lenders view borrowers with larger down payments as less risky, potentially offering better interest rates.

- Avoid Negative Equity: A substantial down payment helps ensure you don’t owe more on the car than it’s worth, especially crucial with used cars that continue to depreciate.

Pro Tips for Maximizing Your Bankrate Calculator Experience

To truly harness the power of the Bankrate Used Car Loan Calculator, consider these expert strategies:

- Run Multiple Scenarios: Don’t just calculate one payment. Experiment with different down payment amounts, loan terms, and even slightly varied interest rates (if you’re unsure of your exact APR). This helps you understand the flexibility and trade-offs.

- Factor In All Costs: As we discussed, remember to add sales tax, registration fees, and any other non-negotiable charges to the car’s price before calculating the loan amount.

- Use It for Negotiation: Armed with pre-approval and various payment scenarios, you can confidently negotiate with dealers. If a dealer tries to push a higher payment, you have the data to counter.

- Don’t Forget Insurance Quotes: Before finalizing your budget with the calculator, get actual insurance quotes for the specific make and model you’re considering. This can significantly impact your true monthly car expense. For more insights on budgeting for your vehicle, check out our article on .

- Re-evaluate Periodically: If your credit score improves or interest rates drop, you might be able to refinance your used car loan. Use the calculator to see if refinancing makes sense for your current situation.

Common Mistakes to Avoid When Using Loan Calculators

Even with the best tools, it’s easy to fall into common traps. Based on my observations, here are crucial mistakes to steer clear of:

- Ignoring Total Interest Paid: Focusing solely on the lowest monthly payment can lead to longer loan terms and significantly more interest paid over time. Always look at the "Total Interest Paid" figure.

- Forgetting Additional Costs: As highlighted, neglecting sales tax, registration, and other fees will give you an inaccurate picture of your loan amount and subsequent payments.

- Not Checking Your Credit Score First: Without knowing your credit score, any interest rate you plug into the calculator is merely a guess. Get your score and pre-approval first.

- Only Focusing on the Lowest Monthly Payment: While an attractive low payment is tempting, it often comes with a longer loan term and a higher overall cost. Balance affordability with the total cost of the loan.

- Assuming the Displayed Rate is Your Rate: Online calculators often show average or "best available" rates. Your personal rate will depend on your creditworthiness and the lender. Always verify your specific APR.

The Bankrate Advantage: Why It Stands Out

Bankrate has long been a trusted name in personal finance, and their Used Car Loan Calculator upholds this reputation. Its key advantages include:

- Accuracy: Bankrate’s calculators are renowned for their precision, providing reliable estimates based on standard financial formulas.

- User-Friendliness: The interface is clean, intuitive, and easy for anyone to use, regardless of their financial expertise.

- Comprehensive Resources: Beyond the calculator, Bankrate offers a wealth of articles, guides, and current rate information, allowing you to delve deeper into various financial topics. This holistic approach empowers users with knowledge, not just numbers. For further exploration of current rates and lending trends, we highly recommend visiting .

- Reputation: Its long-standing presence and authority in the financial sector instill confidence in the tools and information it provides.

Your Journey to a Smarter Used Car Purchase Starts Here

Buying a used car is a significant financial commitment, but it doesn’t have to be a source of stress. By leveraging the power of the Bankrate Used Car Loan Calculator, you equip yourself with the knowledge and foresight needed to make an intelligent, budget-friendly decision. It’s about more than just finding a car; it’s about finding the right financing that aligns with your financial well-being.

Don’t leave your car purchase to guesswork. Take control of your finances, understand every variable, and plan with precision. Your ideal used car, financed smartly, is well within reach. For more strategies on optimizing your car buying process, explore our guide on . Start using the Bankrate Used Car Loan Calculator today, and drive away with confidence!

Conclusion

In conclusion, the Bankrate Used Car Loan Calculator is an indispensable tool for anyone considering financing a pre-owned vehicle. It empowers you to accurately estimate monthly payments, understand total interest costs, and critically evaluate different loan scenarios. By combining the calculator’s insights with a thorough understanding of your credit score, additional car ownership costs, and the benefits of pre-approval, you can navigate the used car market with unparalleled confidence. Make smart choices, avoid common pitfalls, and ensure your next used car loan is a financially sound decision. The power to plan your perfect used car purchase is literally at your fingertips with the Bankrate Used Car Loan Calculator.