Navigating the Waters: Your Ultimate Guide to Securing a Great Lakes Car Loan

Navigating the Waters: Your Ultimate Guide to Securing a Great Lakes Car Loan Carloan.Guidemechanic.com

The open road, the fresh breeze off the vast freshwater expanses, and the promise of adventure – owning a car in the Great Lakes region is more than just a convenience; it’s often a necessity and a gateway to exploring the stunning beauty surrounding these inland seas. But before you hit the highways of Michigan, the bustling streets of Chicago, or the scenic routes of Ontario, securing the right financing is crucial. This is where understanding the intricacies of a Great Lakes car loan becomes paramount.

As an expert blogger and professional SEO content writer, I’ve spent years analyzing the auto financing landscape. Based on my experience, navigating car loans can feel like a complex journey. However, with the right knowledge, you can steer clear of common pitfalls and drive away with a deal that truly benefits you. This comprehensive guide is designed to be your ultimate resource, offering in-depth insights into securing a car loan specifically tailored to the unique economic and environmental factors of the Great Lakes states and provinces.

Navigating the Waters: Your Ultimate Guide to Securing a Great Lakes Car Loan

The Unique Landscape of Car Loans in the Great Lakes Region

The Great Lakes region – encompassing states like Michigan, Ohio, Illinois, Indiana, Wisconsin, Minnesota, Pennsylvania, New York, and the Canadian province of Ontario – is a dynamic area with a diverse economy. From bustling industrial hubs to expansive rural communities, the financial profiles of residents vary significantly. This diversity directly impacts the availability and terms of Great Lakes car loans.

Understanding these regional nuances is your first step towards smart auto financing. For instance, the demand for reliable vehicles, especially those equipped for harsh winters, often influences market prices and, consequently, loan amounts. Lenders in this area are generally attuned to these local demands and economic conditions.

What Makes This Region Different for Auto Financing?

Several factors make securing a car loan in the Great Lakes region distinct. Firstly, the strong automotive manufacturing presence, particularly in Michigan and Ontario, means a vibrant new and used car market. This can translate into competitive pricing and a broader selection of vehicles.

Secondly, the variable climate, with its intense winters and humid summers, influences vehicle choice. Many residents prioritize all-wheel drive (AWD) or four-wheel drive (4WD) vehicles, which might carry a higher price tag. Lenders are accustomed to financing these types of vehicles, understanding their necessity for local conditions.

Finally, the economic health of individual states and provinces within the region can affect interest rates and loan eligibility. A strong local economy generally leads to more favorable lending conditions. Conversely, areas experiencing economic downturns might see tighter credit requirements.

Deciphering the Different Types of Car Loans

Before you even begin your search for a Great Lakes car loan, it’s essential to understand the various financing options available. Each type of loan caters to different needs and financial situations. Choosing the right one can significantly impact your monthly payments and overall cost of ownership.

1. New Car Loans

When you purchase a brand-new vehicle from a dealership, you’ll typically be offered a new car loan. These loans often come with the lowest interest rates, especially for buyers with excellent credit. This is because new cars generally hold their value better initially and are seen as less risky collateral by lenders.

Manufacturers often provide promotional financing offers, such as 0% APR for a limited period, to incentivize new car sales. While these deals can be attractive, always read the fine print. They usually require a top-tier credit score and might mean sacrificing other incentives like cash rebates.

2. Used Car Loans

Used car loans are for vehicles that have had previous owners. While interest rates for used car loans are generally higher than new car loans, the overall purchase price is considerably lower, making them a popular choice for budget-conscious buyers. The interest rate disparity reflects the higher risk associated with an older vehicle’s potential for mechanical issues and faster depreciation.

When considering a used car loan in the Great Lakes, remember that vehicles exposed to harsh winters might have more rust or wear. Lenders consider the age and mileage of the used vehicle when determining loan terms. A pre-purchase inspection is highly recommended for any used vehicle.

3. Refinancing Your Car Loan

Refinancing involves replacing your existing car loan with a new one, often with more favorable terms. This can be an excellent strategy if interest rates have dropped since you originally financed, your credit score has improved, or you want to lower your monthly payments. Many Great Lakes lenders offer competitive refinancing options.

Based on my experience, many people overlook the power of refinancing. It can save you hundreds, even thousands, of dollars over the life of your loan. We’ll delve deeper into this later, but keep it in mind as a powerful financial tool.

4. Private Party Car Loans

Buying a car directly from an individual seller (private party) can often lead to a lower purchase price compared to a dealership. However, financing a private party purchase can be a bit more challenging. Many traditional auto lenders are hesitant to offer loans for private sales due to the lack of a dealership’s warranty or inspection process.

Nonetheless, some banks and credit unions in the Great Lakes region do offer specific private party auto loans. These loans might require a higher down payment or come with slightly higher interest rates. It’s crucial to get a pre-approved loan before you start shopping to ensure you have the funds ready.

Key Factors Lenders Consider for Your Car Loan

Securing a favorable Great Lakes car loan hinges on several critical factors that lenders meticulously evaluate. Understanding these elements allows you to prepare adequately and present yourself as a reliable borrower.

Your Credit Score: The Cornerstone of Approval

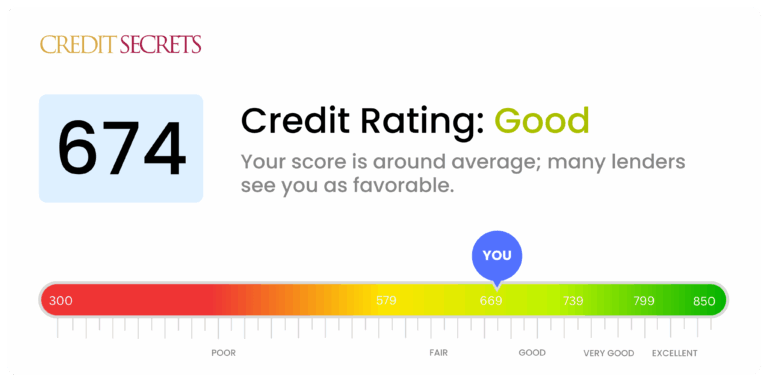

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score (generally above 670 for "good" credit) indicates a lower risk to lenders, often resulting in lower interest rates and more flexible terms.

Conversely, a lower credit score can lead to higher interest rates, stricter loan terms, or even denial. Common mistakes to avoid are not checking your credit score and report before applying. Any inaccuracies can negatively impact your score. Pro tips from us: review your credit report from all three major bureaus annually for free at AnnualCreditReport.com.

Income and Employment Stability

Lenders want assurance that you have a consistent and sufficient income to make your monthly car loan payments. They will typically ask for proof of income, such as pay stubs, tax returns, or bank statements. Employment stability, meaning a consistent work history, also plays a crucial role.

A long-standing employment history with the same employer demonstrates reliability. If you’ve recently changed jobs or are self-employed, be prepared to provide more extensive documentation to prove your income stability. Lenders in the Great Lakes region are familiar with various employment sectors, from manufacturing to tourism, and will assess your income accordingly.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another vital metric. It compares your total monthly debt payments (including your prospective car loan payment) to your gross monthly income. Lenders typically prefer a DTI ratio below 43%, though some may accept higher ratios depending on other factors.

A high DTI ratio indicates that a significant portion of your income is already allocated to existing debts, potentially leaving less for a new car payment. Calculating your DTI before applying helps you understand where you stand and whether you might need to reduce other debts first.

Down Payment: Your Financial Commitment

A down payment is the initial sum of money you pay towards the purchase of a vehicle, reducing the amount you need to borrow. Making a substantial down payment offers several benefits. It lowers your monthly payments, reduces the total interest paid over the life of the loan, and helps you avoid being "upside down" on your loan (owing more than the car is worth).

Based on my experience, a down payment of at least 10-20% for a new car and 20% or more for a used car is advisable. Even a small down payment shows lenders your financial commitment and can improve your chances of securing a better interest rate on your Great Lakes car loan.

Preparing for Your Great Lakes Car Loan Application

Preparation is key to a smooth and successful car loan application process. By taking a few proactive steps, you can significantly improve your chances of approval and secure more favorable terms for your Great Lakes car loan.

1. Check Your Credit Score and Report

As mentioned, this is non-negotiable. Obtain your credit reports from Equifax, Experian, and TransUnion. Review them thoroughly for any errors or discrepancies that could be dragging down your score. Disputing inaccuracies can take time, so do this well in advance.

Understanding your score also helps you set realistic expectations. If your score is low, consider taking steps to improve it before applying, such as paying down existing debts or addressing collections. For more detailed advice, you might find our article on How to Improve Your Credit Score for a Car Loan particularly helpful. (Internal Link Placeholder)

2. Determine Your Budget

Before falling in love with a specific car, establish a realistic budget. This involves more than just the monthly loan payment. Factor in insurance, fuel, maintenance, and potential registration fees, which can vary across Great Lakes states and provinces. Use online car loan calculators to estimate payments based on different interest rates and loan terms.

Pro tips from us: Don’t just focus on the lowest monthly payment. A longer loan term (e.g., 72 or 84 months) will have lower monthly payments but will result in paying significantly more interest over time. Aim for a shorter term if possible, usually 60 months or less, to minimize overall costs.

3. Gather Necessary Documentation

Lenders will require various documents to verify your identity, income, and residency. Having these ready will streamline the application process.

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Recent pay stubs (2-3 months), W-2 forms, tax returns (for self-employed), bank statements.

- Proof of Residency: Utility bill, lease agreement, mortgage statement.

- Social Security Number (US) / Social Insurance Number (Canada).

- Vehicle Information (if you’ve already chosen a car): VIN, make, model, year.

Navigating the Great Lakes Car Loan Application Process

Once you’ve done your homework, it’s time to apply. The application process for a Great Lakes car loan can be approached in a few ways, each with its own advantages.

Get Pre-Approved First

Based on my experience, one of the smartest moves you can make is to get pre-approved for a loan before you step onto a dealership lot. Pre-approval involves a lender reviewing your financial information and offering you a loan amount and interest rate based on your creditworthiness. This gives you several significant advantages:

- Negotiating Power: You walk into the dealership knowing exactly how much you can spend and what interest rate you qualify for. This empowers you to negotiate the car’s price more effectively, rather than getting caught up in monthly payment discussions.

- Budget Clarity: Pre-approval sets a clear spending limit, helping you avoid overspending.

- Time Savings: The financing aspect is largely sorted, allowing you to focus on finding the right vehicle.

Many banks, credit unions, and online lenders serving the Great Lakes region offer pre-approval services. This process usually involves a "soft inquiry" on your credit report, which doesn’t affect your credit score.

Applying at a Dealership

Dealerships often have established relationships with multiple lenders, including captive finance companies (e.g., Ford Credit, GM Financial) and local banks. They can submit your application to several institutions, potentially finding you a competitive rate. However, remember that the dealership’s primary goal is to sell you a car and maximize their profit, which may include markups on interest rates.

Pro tips from us: Always compare the dealership’s financing offer with your pre-approved loan. If the dealership can beat your pre-approved rate, that’s great! But never assume their first offer is the best one. Be prepared to walk away if the terms aren’t favorable.

Exploring Credit Unions and Local Banks

Credit unions are member-owned financial institutions known for offering competitive interest rates and personalized service. They often have more flexible lending criteria than larger banks, which can be beneficial if your credit isn’t perfect. Local banks in the Great Lakes area also understand the regional market well and can be great sources for car loans.

Common mistakes to avoid are only applying at one place. It’s always wise to shop around. Compare offers from at least three different lenders to ensure you’re getting the best possible rate and terms.

Common Mistakes to Avoid When Getting a Car Loan

Even with careful preparation, it’s easy to make missteps during the car loan process. Based on my experience, these are some of the most common mistakes people make when securing a Great Lakes car loan:

- Focusing Only on Monthly Payments: While important, fixating solely on the lowest monthly payment can lead to longer loan terms and significantly higher total interest paid. Always consider the total cost of the loan.

- Skipping the Pre-Approval: As discussed, not getting pre-approved leaves you vulnerable to dealership markups and less negotiating power.

- Ignoring the APR: The Annual Percentage Rate (APR) is the true cost of borrowing, including interest and other fees. Don’t just look at the interest rate; compare APRs across different loan offers. For more insights on this, refer to our article on Understanding Auto Loan Interest Rates. (Internal Link Placeholder)

- Not Reading the Fine Print: Loan agreements can be complex. Always read every line, understanding all fees, terms, and conditions before signing. Ask questions if anything is unclear.

- Falling for Add-Ons You Don’t Need: Dealerships often push extended warranties, GAP insurance (Guaranteed Asset Protection), and other add-ons. While some might be beneficial, many are overpriced or unnecessary. Research these products independently and decide if they fit your needs and budget.

- Lying on Your Application: Never provide false information on a loan application. This is considered fraud and can have severe legal consequences.

Pro Tips for Securing the Best Great Lakes Car Loan Rates

Getting a car loan is a significant financial decision. Here are some pro tips from us to help you secure the most advantageous terms for your Great Lakes car loan:

- Improve Your Credit Score: If time permits, boosting your credit score by paying bills on time, reducing credit card balances, and correcting report errors will directly translate to lower interest rates.

- Make a Larger Down Payment: The more you put down upfront, the less you need to borrow, reducing your loan-to-value (LTV) ratio and making you a less risky borrower in the eyes of lenders.

- Choose a Shorter Loan Term: While monthly payments will be higher, a shorter term (e.g., 36 or 48 months) means less interest paid over the life of the loan.

- Consider a Co-Signer: If you have limited credit history or a low credit score, a co-signer with excellent credit can help you qualify for a better rate. Remember, the co-signer is equally responsible for the debt.

- Shop Around Extensively: Don’t settle for the first offer. Get quotes from multiple banks, credit unions, and online lenders. Aim for at least three to five different offers.

- Negotiate the Car Price Separately: Always negotiate the price of the car first, then discuss financing. Don’t let the dealership combine these discussions, as it can confuse the true cost of each.

Special Considerations in the Great Lakes Region

Beyond general financing advice, the Great Lakes area presents specific factors that might influence your car loan decisions.

Vehicle Type and Environmental Impact

The region’s climate often necessitates vehicles with specific features like AWD/4WD, robust heating systems, and durable tires. While these vehicles might be pricier, their necessity means lenders are accustomed to financing them. Consider also the impact of road salt on vehicle longevity. Some lenders might offer specific insurance packages or extended warranties tailored to protect against common regional wear and tear.

Furthermore, with a growing emphasis on environmental consciousness, electric vehicles (EVs) and hybrids are becoming more popular. Many Great Lakes states and provinces offer incentives for purchasing these vehicles, which can indirectly affect the total loan amount needed. Research local government websites for potential rebates.

Local Dealerships and Community Lenders

The Great Lakes region boasts a strong network of local dealerships and community-focused financial institutions. These entities often have deep roots in their communities and can offer personalized service and understanding of local economic conditions. Building relationships with these local lenders can sometimes lead to more flexible loan options.

Common mistakes to avoid are overlooking smaller, local credit unions in favor of national banks. These smaller institutions often offer highly competitive rates and exceptional customer service.

The Power of Refinancing Your Great Lakes Car Loan

As mentioned earlier, refinancing is a powerful tool that shouldn’t be underestimated. Even after you’ve secured your initial Great Lakes car loan, market conditions or your personal financial situation can change, making refinancing a smart move.

When to Consider Refinancing

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan, you’re likely eligible for a lower interest rate.

- Lower Interest Rates: General interest rates in the market might have dropped, allowing you to secure a better deal.

- Lower Monthly Payments: Refinancing can extend your loan term, reducing your monthly payments (though potentially increasing total interest paid). This can provide immediate relief if your budget is tight.

- Getting Rid of a Co-Signer: If your credit has improved, you might be able to refinance the loan in your name only, releasing your co-signer from their obligation.

- Changing Loan Terms: You might want to switch from a variable interest rate to a fixed rate for more predictable payments.

Pro tips from us: Always calculate the total savings over the life of the loan when considering refinancing. Don’t just look at the monthly payment reduction. Ensure the savings outweigh any potential refinancing fees.

Building a Strong Financial Future with Your Car Loan

Securing a Great Lakes car loan is more than just getting approved; it’s an opportunity to build or strengthen your financial foundation. Paying your car loan responsibly can significantly impact your credit history, opening doors to other financial products in the future.

Pay on Time, Every Time

This is the golden rule of credit building. Every on-time payment reflects positively on your credit report. Set up automatic payments to avoid missing due dates, especially if you have a busy schedule.

Consider Extra Payments

If your budget allows, making extra payments or rounding up your monthly payment can help you pay off your loan faster. This reduces the total interest paid and frees up your budget sooner for other financial goals. Even small, consistent extra payments can make a big difference over time.

Monitor Your Credit Regularly

Continue to monitor your credit score and report even after securing your loan. This helps you track your progress and quickly identify any potential issues or identity theft.

Conclusion: Your Journey to a Great Lakes Car Loan Success

Navigating the world of car loans can seem daunting, but armed with the in-depth knowledge and expert tips provided in this guide, you are well-equipped to secure a Great Lakes car loan that perfectly fits your needs and budget. From understanding the regional nuances to meticulously preparing your application and avoiding common pitfalls, every step you take contributes to a smoother, more financially sound vehicle purchase.

Remember, the goal is not just to get a car loan, but to get the right car loan. By focusing on your credit, shopping around for the best rates, and making informed decisions, you’ll not only drive away in your desired vehicle but also build a stronger financial future. So go ahead, embark on your car-buying journey with confidence, knowing you have the insights of a seasoned professional backing you every mile of the way. Happy driving in the beautiful Great Lakes region!