Navigating the World of Car Loans: Your Comprehensive Guide with Car Loan Co

Navigating the World of Car Loans: Your Comprehensive Guide with Car Loan Co Carloan.Guidemechanic.com

The dream of owning a new car often begins with excitement, but the reality of financing it can quickly become overwhelming. Understanding car loans is crucial for making a smart financial decision that impacts your budget for years to come. Many people jump into a loan without fully grasping the terms, leading to stress and unexpected costs down the road.

At Car Loan Co, we believe in empowering our customers with knowledge. This in-depth guide is designed to demystify the car loan process, providing you with the insights and confidence needed to secure the best financing for your next vehicle. We aim to be your trusted partner, offering clarity in a complex financial landscape.

Navigating the World of Car Loans: Your Comprehensive Guide with Car Loan Co

What is a Car Loan, Really? Beyond the Basics

At its core, a car loan is a sum of money borrowed from a lender to purchase a vehicle. You agree to repay this amount, known as the principal, over a set period, typically with added interest. This interest is essentially the cost of borrowing the money, compensating the lender for their service.

Most car loans are "secured" loans. This means the car itself acts as collateral. Should you fail to make your payments, the lender has the legal right to repossess the vehicle to recover their losses. Understanding this fundamental aspect highlights the importance of responsible borrowing and thorough planning.

The loan agreement will detail several key elements. These include the principal amount, the interest rate, the loan term (duration), and your monthly payment. Each of these components plays a significant role in the total cost of your loan and your financial commitment.

The Journey to Your Dream Car: Navigating the Car Loan Process

Securing a car loan is a multi-step process, and each stage offers opportunities to save money and make informed choices. Based on my extensive experience in vehicle financing, approaching this journey systematically can significantly reduce stress and improve your outcome. Let’s break down each critical step.

Step 1: Assessing Your Financial Readiness – What Can You Truly Afford?

Before you even start browsing cars, the first and most crucial step is to look at your own finances. Many people make the mistake of falling in love with a car they can’t comfortably afford, leading to financial strain. This initial assessment involves a realistic look at your budget and credit health.

Budgeting for Your Car Loan

Consider your monthly income and all your existing expenses. This includes housing, utilities, groceries, insurance, and any other debt payments. A common metric lenders use is your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio generally indicates a healthier financial standing.

Pro tips from us: Don’t just consider the monthly loan payment. Factor in ongoing costs like insurance, fuel, maintenance, and potential repairs. A car is more than just its purchase price; it’s an ongoing financial commitment.

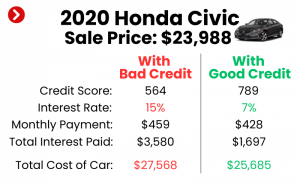

Understanding Your Credit Score

Your credit score is a three-digit number that profoundly impacts the interest rate you’ll be offered. Lenders use it to assess your creditworthiness – your likelihood of repaying the loan on time. A higher credit score signals lower risk to lenders, often resulting in more favorable interest rates and better loan terms.

Common mistakes to avoid are applying for a loan without checking your credit report first. It’s wise to review your credit report for any errors and understand your score. If your score is lower than you’d like, take steps to improve it, such as paying down existing debts or making all payments on time, before applying for a car loan. External Link: Understanding Your Credit Score – Experian

The Power of a Down Payment

Making a significant down payment is one of the smartest moves you can make when financing a car. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. It also helps create equity in your vehicle from day one.

Based on my experience, a down payment of at least 10-20% of the car’s purchase price is ideal. For used cars, a larger down payment can be even more beneficial, as used cars typically depreciate faster initially. It immediately reduces your loan-to-value (LTV) ratio, making you a less risky borrower.

Step 2: Pre-Approval – Your Secret Weapon

Once you have a clear picture of your finances, the next step is to get pre-approved for a car loan. This is a preliminary approval from a lender that tells you how much you can borrow, at what interest rate, and under what terms. It’s an incredibly powerful tool in the car-buying process.

What is Pre-Approval?

Pre-approval involves submitting a loan application to a lender before you’ve even chosen a specific car. The lender reviews your credit history, income, and other financial details to determine your eligibility and loan parameters. They will provide you with a conditional offer, outlining the maximum loan amount and estimated interest rate.

This process typically involves a "hard inquiry" on your credit report, which can slightly ding your score temporarily. However, multiple hard inquiries for car loans within a short period (usually 14-45 days, depending on the credit scoring model) are often treated as a single inquiry, so shopping around for pre-approvals is encouraged.

Benefits of Pre-Approval

Having a pre-approval in hand gives you significant advantages. Firstly, it provides a firm budget, so you know exactly what you can afford, preventing you from overspending. Secondly, it turns you into a cash buyer at the dealership. You can focus on negotiating the car’s price, rather than being swayed by confusing payment calculations.

Furthermore, pre-approval gives you leverage. You can compare the dealer’s financing offer against your pre-approved loan, ensuring you get the most competitive rate. It puts you in the driver’s seat during negotiations, allowing you to walk away if the dealer’s offer isn’t up to par.

Step 3: Finding the Right Vehicle (and Negotiating Smartly)

With your budget and pre-approval ready, you can now confidently shop for a car. This stage is about balancing your desires with your financial realities, and knowing how to negotiate effectively.

New vs. Used: Pros and Cons

Deciding between a new or used car significantly impacts your loan. New cars come with the latest features and a full warranty but depreciate rapidly in the first few years. Used cars are more budget-friendly and depreciate slower, but might have higher mileage or require more immediate maintenance.

Consider your long-term needs and financial goals. A new car might mean higher payments but fewer immediate repair costs, while a used car could offer lower payments but potentially more upkeep.

Negotiation Tips Beyond the Sticker Price

When at the dealership, always negotiate the car’s purchase price first, separate from the financing. Dealerships often try to blend these discussions, making it harder for you to see the true cost. Focus on getting the lowest possible price for the vehicle itself.

Common mistakes to avoid are getting fixated solely on the monthly payment. A dealer might offer a low monthly payment by extending the loan term significantly, which means you pay much more in total interest. Always ask for the "out-the-door" price, which includes all fees and taxes.

Step 4: Understanding Loan Offers and Terms

Once you’ve settled on a car and have financing options (from your pre-approval and potentially the dealership), it’s critical to meticulously compare the loan offers. The details of the loan agreement can dramatically affect your total cost.

Interest Rates: Fixed vs. Variable

Most car loans feature a fixed interest rate, meaning your rate and monthly payment remain constant throughout the loan term. This provides predictability, which is highly beneficial for budgeting. Variable rates, while rare for standard car loans, can fluctuate with market conditions, making payments unpredictable.

Always pay attention to the Annual Percentage Rate (APR), not just the interest rate. The APR includes the interest rate plus certain fees, giving you a more accurate representation of the true annual cost of borrowing. A lower APR is always better.

Loan Term: Shorter vs. Longer

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 84 months. A shorter loan term means higher monthly payments but significantly less total interest paid over the life of the loan. Conversely, a longer loan term leads to lower monthly payments but a much higher total interest cost.

Based on my experience, shorter loan terms (e.g., 36-60 months) are often financially smarter if you can comfortably afford the payments. They save you money in the long run and allow you to build equity faster. However, choose a term that aligns with your financial comfort zone, ensuring you don’t overextend yourself.

Fees and the Fine Print

Be vigilant about any additional fees. These can include origination fees, documentation fees, processing fees, and even early payoff penalties. Some lenders charge a penalty if you pay off your loan ahead of schedule, so always check for this clause if you anticipate paying off your car early.

Carefully read the entire loan agreement before signing. Ensure that all the terms you discussed are accurately reflected in the document. Don’t hesitate to ask questions about anything you don’t understand. It’s your right to be fully informed.

Step 5: Finalizing Your Loan and Driving Away

With all the details confirmed, the final step is to sign the paperwork and take possession of your new vehicle. This is the culmination of your careful planning and research.

Reviewing Documents One Last Time

Before putting pen to paper, do a final review of all documents. Confirm the loan amount, interest rate, monthly payment, loan term, and any additional fees. Ensure there are no unexpected add-ons or changes from what you agreed upon.

It’s wise to have a copy of all signed documents for your records. This includes the purchase agreement, loan agreement, and any warranty information. These documents are vital for future reference or if any disputes arise.

Post-Loan Responsibilities

Once the loan is finalized, your responsibility is to make your monthly payments on time, every time. Timely payments are crucial for maintaining a good credit score and avoiding late fees or, worse, repossession. Set up reminders or automatic payments to ensure you never miss a due date.

Keep your vehicle properly insured as required by your loan agreement and state law. Lenders typically require full coverage (comprehensive and collision) until the loan is paid off, as the car is their collateral.

Common Car Loan Mistakes to Avoid

Even with the best intentions, it’s easy to fall into common traps when financing a vehicle. Avoiding these pitfalls can save you significant money and stress.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you lose significant negotiation power and might accept the first, less-than-ideal financing offer from the dealership. Always secure outside financing options before stepping onto the lot.

- Focusing Only on Monthly Payments: Dealers often highlight low monthly payments. While important, a low payment can mask a very long loan term and a high total interest cost. Always look at the total cost of the car and the loan over its entire duration.

- Ignoring the Total Cost: Beyond the loan, consider insurance, registration, maintenance, and fuel. A "cheap" monthly payment might not be so cheap when all other ownership costs are factored in.

- Rolling Negative Equity into a New Loan: If you owe more on your current car than it’s worth (negative equity), some dealers might offer to roll that amount into your new car loan. This means you’re paying interest on a car you no longer own, starting your new loan underwater. It’s a financial trap to avoid at all costs.

- Not Understanding Depreciation: Cars lose value over time, a process called depreciation. Some cars depreciate faster than others. Understanding this can help you choose a vehicle that retains more value, which is important if you plan to trade it in or sell it later.

Pro Tips for a Smooth Car Loan Experience

Based on my experience helping countless individuals secure their ideal vehicle financing, here are some invaluable tips to ensure your car loan journey is as smooth and advantageous as possible.

- Shop Around for Rates: Don’t settle for the first loan offer you receive. Lenders, including banks, credit unions, and online lenders like Car Loan Co, offer varying rates and terms. Comparing multiple offers is the most effective way to secure the best deal.

- Improve Your Credit Score Before Applying: A higher credit score translates directly into lower interest rates. If you have time before needing a loan, focus on paying bills on time, reducing credit card balances, and checking your credit report for errors.

- Consider a Larger Down Payment: As discussed, a substantial down payment reduces your loan amount, lowers monthly payments, and decreases the total interest paid. It also gives you instant equity in the vehicle.

- Negotiate the Car Price Separately from the Loan: This is a golden rule of car buying. Secure the best possible price for the vehicle first. Only after you’ve agreed on the car’s price should you discuss financing options.

- Understand All Add-ons: Be wary of extended warranties, GAP insurance, paint protection, or other add-ons that dealers might push. While some might be beneficial, they add to your loan amount and total cost. Research their value and necessity before agreeing.

- Explore Refinancing Options: If interest rates drop after you’ve secured your loan, or if your credit score significantly improves, consider refinancing your car loan. This could potentially lower your interest rate, reduce your monthly payments, or shorten your loan term, saving you money.

The Car Loan Co Difference: Your Partner in Vehicle Financing

At Car Loan Co, we are committed to making the car loan process transparent, understandable, and accessible. We understand that every individual’s financial situation is unique, and a one-size-fits-all approach simply doesn’t work. Our mission is to provide tailored solutions that align with your budget and financial goals.

We pride ourselves on offering competitive rates, clear terms, and a straightforward application process. Our team of experts is dedicated to guiding you through each step, ensuring you feel confident and informed. We believe that securing a car loan should be an empowering experience, not a confusing one.

Conclusion: Drive Towards Your Future with Confidence

Securing a car loan doesn’t have to be a daunting task. By understanding the process, preparing your finances, and knowing what to look for, you can make an informed decision that benefits your financial health. Remember, knowledge is your most powerful tool in the car-buying journey.

From assessing your readiness and getting pre-approved to understanding the intricate details of loan terms, each step plays a crucial role. Avoid common mistakes, leverage expert tips, and always prioritize your long-term financial well-being.

At Car Loan Co, we’re here to help you navigate these waters with ease. We encourage you to explore our resources and connect with our team for personalized advice. Your dream car is within reach, and with the right car loan, you can drive towards your future with confidence.