Navigating the World of Large Car Loans: Your Ultimate Guide to Financing Your Dream Vehicle

Navigating the World of Large Car Loans: Your Ultimate Guide to Financing Your Dream Vehicle Carloan.Guidemechanic.com

The allure of a brand-new luxury sedan, a powerful sports car, or a spacious, high-end SUV is undeniable. For many, these vehicles represent more than just transportation; they embody aspirations, achievements, and a desired lifestyle. However, such dream cars often come with a significant price tag, making a "large car loan" an essential step in acquiring them.

But what exactly constitutes a large car loan, and how does it differ from a standard auto loan? More importantly, how can you navigate this complex financial landscape to secure the best terms and avoid common pitfalls? This comprehensive guide will equip you with the knowledge and expert insights needed to finance your high-value vehicle wisely and confidently. We’ll delve deep into every aspect, from preparation to approval and beyond, ensuring you make an informed decision that aligns with your financial well-being.

Navigating the World of Large Car Loans: Your Ultimate Guide to Financing Your Dream Vehicle

What Exactly Constitutes a "Large Car Loan"?

When we talk about a "large car loan," we’re generally referring to a substantial financing amount required for a high-value vehicle. This isn’t about the physical size of the car, but rather the monetary value. While the exact threshold can vary, a loan typically begins to be considered "large" when it exceeds $40,000, and often extends well into the $60,000, $80,000, or even $100,000+ range.

These loans are distinct from standard auto loans for economy or mid-range vehicles. The higher principal amount introduces a different set of challenges and considerations for both borrowers and lenders. You’ll find these loans commonly used to finance luxury brands like Mercedes-Benz, BMW, Audi, Lexus, or high-performance vehicles from manufacturers like Porsche and Corvette. They also frequently cover large, fully-loaded SUVs, bespoke custom builds, or even classic and collector cars that hold significant value.

The Unique Challenges and Considerations of Large Car Loans

Securing a large car loan isn’t simply a scaled-up version of a smaller loan. The stakes are higher, and the financial implications are far-reaching. Understanding these unique challenges is the first step toward a successful borrowing experience.

Firstly, the most apparent factor is the higher principal amount. This directly translates into a significantly larger total interest payment over the life of the loan, even if the interest rate seems modest. A small difference in your APR can mean thousands of dollars saved or spent over several years.

Lenders, understanding the increased risk associated with such substantial sums, typically impose stricter eligibility criteria. They will scrutinize your financial health with a magnifying glass, looking for impeccable credit, stable income, and a manageable debt-to-income ratio. Your financial history needs to tell a story of reliability and capability.

Another key consideration is the potential impact on your debt-to-income (DTI) ratio. A large car loan can significantly elevate this ratio, potentially affecting your ability to secure other forms of credit in the future, such as a mortgage. It’s crucial to assess how this new debt will fit into your overall financial picture.

Furthermore, borrowers often consider longer loan terms to make the higher monthly payments more affordable. While this might seem appealing, it comes with a trade-off: you’ll pay more interest over time, and the car will depreciate significantly while you’re still paying it off. We’ll explore the pros and cons of loan terms in detail later.

Finally, owning a high-value vehicle also means higher associated costs beyond the loan payment. Expect higher insurance premiums due to the car’s value and repair costs. Depreciation is also a significant factor; expensive cars can lose value quickly, and it’s important not to owe more on the car than it’s worth.

Preparing for a Large Car Loan Application: Laying the Groundwork for Success

Success in securing a large car loan, and doing so on favorable terms, begins long before you even step into a dealership or submit an application. Thorough preparation is paramount. Based on my experience, the more diligently you prepare, the stronger your position will be.

A. Credit Score is King (or Queen)

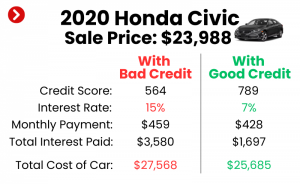

For large car loans, your credit score isn’t just important; it’s often the determining factor for approval and the interest rate you’ll receive. Lenders use your credit score as a quick snapshot of your creditworthiness and your history of managing debt. For a substantial loan, they are looking for an excellent score, typically 720 and above, with the best rates often reserved for scores in the 760-800+ range.

A high credit score signals to lenders that you are a low-risk borrower, reliable in making payments on time. Before applying, obtain your credit reports from all three major bureaus (Equifax, Experian, and TransUnion) and check for any errors. Dispute anything inaccurate. Focus on reducing existing debt, paying bills on time, and avoiding new credit applications in the months leading up to your car loan application. Common mistakes to avoid are applying for too much credit too quickly, which can temporarily ding your score, or missing payments on existing accounts.

B. Income and Debt-to-Income (DTI) Ratio

Lenders need assurance that you can comfortably afford the significant monthly payments associated with a large car loan. This is where your income and debt-to-income (DTI) ratio become critical. You’ll need stable, verifiable income that can be proven through pay stubs, tax returns, and bank statements. Lenders typically prefer a DTI ratio below 36%, meaning your total monthly debt payments (including the new car loan) should not exceed 36% of your gross monthly income.

Understanding your DTI is crucial because it gives lenders a clear picture of your financial capacity. A high DTI suggests you might be overextended, making you a riskier borrower. Pro tips from us include actively reducing existing debt, such as credit card balances or other personal loans, before you apply. This will lower your current DTI and present a more favorable financial profile to lenders.

C. Down Payment Power

For large car loans, a substantial down payment is not just beneficial; it’s often a necessity. A significant down payment immediately reduces the principal amount you need to borrow, which means lower monthly payments and less interest paid over the life of the loan. From a lender’s perspective, a large down payment also signals your commitment to the purchase and reduces their risk, making them more willing to offer competitive rates.

Based on my experience, aiming for at least 20% of the vehicle’s purchase price as a down payment is a strong strategy for any car loan, but it becomes even more critical for high-value vehicles. Some experts even recommend higher percentages, especially for luxury cars that depreciate quickly. A solid down payment also helps mitigate the risk of being "upside down" on your loan, where you owe more than the car is worth.

D. Budgeting Beyond the Monthly Payment

Many prospective buyers make the common mistake of focusing solely on the monthly loan payment. However, the true cost of owning a high-value vehicle extends far beyond this single figure. You must create a comprehensive budget that accounts for the total cost of ownership.

This includes significantly higher insurance premiums, which can be thousands of dollars annually for luxury or performance cars. Maintenance costs for specialized vehicles can also be considerably more expensive than for standard cars. Don’t forget fuel costs, registration fees, and potential repair expenses for complex systems. Pro tips from us: Factor in a contingency fund for unexpected repairs. You don’t want to get "car poor," where your vehicle ownership costs consume too much of your income, leaving little for other necessities or savings.

Where to Secure Your Large Car Loan: Exploring Your Options

Just as important as preparing yourself is knowing where to look for your large car loan. Different lenders offer varying rates, terms, and customer service experiences. Exploring all your options ensures you find the best fit for your financial situation.

A. Banks and Credit Unions

Traditional banks and local credit unions are often excellent places to start your search for a large car loan. They are generally well-established, reputable, and can offer competitive interest rates, especially to customers with whom they have an existing relationship. If you’ve been a long-time member of a credit union, you might find particularly favorable terms due to their member-focused structure.

It’s a good idea to check with your current bank or credit union first, as they may offer loyalty benefits or streamline the application process. However, don’t limit yourself to just one institution. Comparing offers from several banks and credit unions is a smart move to ensure you’re getting the most competitive rate available.

B. Dealership Financing

Most dealerships offer in-house financing options, often working with a network of lenders. The convenience of a one-stop shop can be appealing; you can choose your car and arrange financing all in one place. Dealerships also frequently have access to manufacturer incentives, such as low APR offers on new vehicles, which can be very attractive.

However, a common mistake to avoid is not comparing the dealership’s offer with pre-approvals you’ve secured elsewhere. While convenient, dealership financing isn’t always the cheapest option. Always come armed with outside offers to use as leverage for negotiation.

C. Online Lenders

The digital age has brought a plethora of online lenders specializing in auto loans. These platforms often offer a streamlined application process, quick approval times, and the potential for a wider range of loan options. They can be particularly useful for comparing rates from multiple lenders without having to visit each one physically.

When considering online lenders for a large car loan, it’s crucial to vet their reputation thoroughly. Look for reviews, check their standing with consumer protection agencies, and ensure they are transparent about all fees and terms. Reputable online lenders can be a fantastic resource for competitive rates and convenience.

D. Specialty Lenders for Luxury/Classic Cars

For extremely high-value vehicles, classic cars, or exotic models, you might find that mainstream banks are less willing to finance or offer less favorable terms. This is where specialty lenders come into play. These institutions understand the unique asset values, depreciation curves, and specific market dynamics of luxury and collector vehicles.

They often provide tailored products and more flexible terms for these niche markets, sometimes even considering the vehicle itself as collateral in a different light. If you’re pursuing a truly unique or high-end car, exploring these specialized avenues could be beneficial.

The Application Process: Step-by-Step Guidance

Once you’ve done your homework and explored your lending options, it’s time to tackle the application process for your large car loan. Approaching this systematically can save you time, stress, and potentially money.

A. Pre-Approval: Your Secret Weapon

Based on my experience, securing pre-approval for a large car loan is perhaps the most powerful step you can take. What is it? Pre-approval means a lender has provisionally agreed to lend you a specific amount at a certain interest rate, based on a preliminary review of your credit and financial situation. It’s not a final loan offer, but it’s very close.

Why is it vital? Pre-approval transforms you into a cash buyer at the dealership. You walk in knowing exactly how much you can spend and what your interest rate will be, empowering you to negotiate the car’s price without the added stress of financing. It separates the car negotiation from the loan negotiation, often leading to a better overall deal. Furthermore, multiple pre-approval applications within a short window (typically 14-45 days) are usually treated as a single hard inquiry on your credit report, minimizing the impact.

B. Gathering Documentation

Lenders for large car loans require extensive documentation to verify your financial standing. Being prepared with all necessary paperwork will significantly speed up the application process. You’ll typically need:

- Proof of Income: Recent pay stubs (3-6 months), W-2 forms, and potentially tax returns (especially if self-employed or for higher loan amounts).

- Proof of Residency: Utility bills, lease agreements, or mortgage statements.

- Identification: Driver’s license or other government-issued ID.

- Bank Statements: To verify assets and financial stability.

- Credit History: While lenders pull this themselves, it’s good to have checked your own reports.

- Trade-in Information (if applicable): Title, registration, and payoff amount.

Having these documents organized and readily available will make the application seamless and demonstrate your preparedness.

C. Understanding Loan Terms

Before signing any agreement, you must fully understand all the terms of your large car loan. This includes several key components:

- Interest Rate (APR): This is the cost of borrowing money, expressed as an annual percentage rate. The APR includes the interest rate plus any fees, giving you the true annual cost. A lower APR means lower total cost.

- Loan Term: This is the length of time you have to repay the loan, typically expressed in months (e.g., 60, 72, 84 months). Longer terms mean lower monthly payments but more interest paid over time.

- Fees: Be aware of any origination fees, application fees, or documentation fees. While less common for auto loans than other loan types, they can exist.

- Prepayment Penalties: Though rare in auto loans, always check if there’s a penalty for paying off your loan early. You want the flexibility to pay it down faster if your financial situation allows.

D. Reading the Fine Print: What to Watch Out For

Never rush through the loan agreement. This is a legally binding document for a significant amount of money. Common mistakes to avoid include skimming the terms or feeling pressured to sign quickly. Look for clauses related to:

- Balloon Payments: A large lump-sum payment due at the end of the loan term. While common in some financing structures, ensure you’re aware of it and prepared.

- Hidden Fees: Ensure all fees are clearly disclosed and understood.

- Complex Clauses: If you don’t understand something, ask for clarification. Based on my experience, reputable lenders are happy to explain every detail. Don’t be afraid to ask for a copy to review at home or even consult with a financial advisor before committing.

Navigating Interest Rates and Loan Terms for Large Car Loans

The interest rate and loan term are the two most significant factors determining the total cost of your large car loan. Understanding how they interact and how to optimize them is crucial for smart borrowing.

A. Fixed vs. Variable Rates

When considering a large car loan, you’ll typically encounter two types of interest rates:

- Fixed-Rate Loans: The interest rate remains the same for the entire duration of the loan. This provides predictability and stability in your monthly payments, making budgeting easier. For large, long-term loans, fixed rates are often preferred as they protect you from potential interest rate hikes.

- Variable-Rate Loans: The interest rate can fluctuate over the loan term, usually tied to a benchmark index. While they might start lower than fixed rates, they carry the risk of increasing, which would raise your monthly payments. For the security and predictability needed with a large car loan, a fixed rate is generally the safer choice.

B. The Impact of Loan Term

The loan term, or the length of time you have to repay the loan, significantly impacts both your monthly payment and the total interest you’ll pay.

- Shorter Terms (e.g., 36-60 months): These typically result in higher monthly payments but substantially less interest paid over the life of the loan. You pay off the car faster, build equity sooner, and are less likely to be upside down on your loan.

- Longer Terms (e.g., 72-84 months, sometimes even 96 months for very large loans): These offer lower monthly payments, which can make a high-value car seem more affordable. However, the trade-off is a much higher total interest cost. The car also depreciates significantly during a longer term, increasing the risk of negative equity. Pro tips from us: Balance affordability with the total cost. Common mistakes to avoid are extending the loan term too much just to get a lower payment, without considering the long-term financial implications.

C. How Your Credit Score Influences Rates

As mentioned, your credit score is paramount. Lenders use a tiered system, offering the lowest interest rates to borrowers with excellent credit scores (typically 760+). As your score decreases, the interest rate you’re offered will generally increase, reflecting the higher perceived risk to the lender. Even a difference of 0.5% or 1% on a large car loan can translate into thousands of dollars over several years. This underscores the importance of credit score optimization before you apply.

D. Negotiation Strategies

Equipped with knowledge and pre-approvals, you’re in a strong position to negotiate.

- Use Your Pre-Approval: Present your pre-approval offer to the dealership. They may try to beat it to keep the financing in-house, potentially saving you money.

- Compare Multiple Offers: Don’t settle for the first offer. Compare rates from banks, credit unions, online lenders, and the dealership.

- Negotiate the Car Price Separately: First, agree on the car’s purchase price, then discuss financing. Blurring the two can lead to confusion and less favorable terms on either front.

Managing Your Large Car Loan: Post-Approval Best Practices

Getting approved for your large car loan is a significant achievement, but the journey doesn’t end there. Effective management of your loan is crucial to maintain financial health and protect your investment.

A. On-Time Payments Are Non-Negotiable

This might seem obvious, but consistently making your large car loan payments on time is paramount. Late payments can severely damage your credit score, incur late fees, and potentially lead to repossession. Building a solid payment history on such a substantial loan will also significantly boost your credit profile, benefiting you in future financial endeavors.

B. Consider Auto-Pay

To ensure you never miss a payment, consider setting up automatic payments from your bank account. Many lenders even offer a small interest rate discount (e.g., 0.25%) for enrolling in auto-pay. This convenience avoids human error and gives you peace of mind, knowing your payments are always handled promptly.

C. Refinancing Opportunities

Your financial situation or market interest rates might change over time, creating opportunities to refinance your large car loan. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

You might consider refinancing if:

- Your credit score has significantly improved since you took out the initial loan.

- Interest rates have dropped since your original purchase.

- You want to change your loan term (e.g., shorten it to pay less interest, or extend it for lower payments if your financial situation has changed).

However, always calculate the costs associated with refinancing to ensure it truly saves you money in the long run.

D. Protecting Your Investment

A large car loan means you’ve made a substantial investment. Protecting that investment is critical.

- Comprehensive Insurance: Ensure you have robust, comprehensive auto insurance coverage. For high-value vehicles, this is not just a recommendation but often a lender requirement. It protects against theft, damage, and liability.

- Gap Insurance: For large car loans, especially for new vehicles, Gap (Guaranteed Asset Protection) insurance is highly recommended. If your car is totaled or stolen, your standard insurance might only pay out its actual cash value, which could be less than what you still owe on your loan. Gap insurance covers this "gap," preventing you from being upside down on a car you no longer have.

- Regular Maintenance: Follow the manufacturer’s recommended maintenance schedule diligently. This preserves the vehicle’s value, ensures its longevity, and can prevent costly major repairs down the line. Remember, a well-maintained car retains more of its resale value.

Common Mistakes to Avoid When Getting a Large Car Loan

Even with thorough preparation, some common pitfalls can derail your large car loan experience. Being aware of these can help you steer clear of financial regret.

- Not Budgeting for Total Cost of Ownership: As discussed, focusing solely on the monthly payment and ignoring insurance, maintenance, fuel, and registration can lead to significant financial strain.

- Skipping Pre-Approval: This leaves you at a disadvantage during negotiations and potentially leads to higher interest rates.

- Focusing Only on the Monthly Payment: While important for affordability, a low monthly payment achieved through a very long loan term can mean paying excessive interest over time.

- Not Comparing Multiple Lenders: Relying on the first offer, especially from the dealership, often means missing out on more competitive rates elsewhere.

- Borrowing More Than You Can Comfortably Afford: Just because you’re approved for a certain amount doesn’t mean you should borrow it all. Stick to a budget that allows for other financial goals.

- Ignoring Your Credit Score: A low credit score will result in higher interest rates, significantly increasing the total cost of your large car loan. Improving it beforehand is a key strategy.

Pro Tips from an Expert Blogger

Having navigated the complexities of auto financing for years, here are some additional insights to help you secure and manage your large car loan effectively:

- Think Long-Term Value: High-value cars often depreciate quickly. While it’s your dream car, consider if you’re comfortable financing a heavily depreciating asset with a significant loan. Sometimes, a slightly used luxury vehicle can offer substantial savings.

- Emergency Fund First: Before committing to a large car loan, ensure you have a robust emergency fund (3-6 months of living expenses). This acts as a financial safety net, preventing you from missing car payments if unexpected expenses arise.

- Negotiate Everything: Don’t just negotiate the car’s price. Negotiate your trade-in value, the interest rate, and any added fees. Every dollar saved on these fronts adds up significantly on a large loan.

- Don’t Rush: This is a major financial decision. Take your time, do your research, sleep on it, and don’t feel pressured by salespeople.

- Seek Professional Advice: If you’re unsure about the financial implications of a large car loan, especially regarding your overall financial plan, consider consulting a financial advisor. They can provide personalized guidance tailored to your specific situation.

Conclusion

Securing a large car loan is a significant financial undertaking that can pave the way to owning your dream vehicle. However, it’s a process that demands meticulous preparation, thorough research, and a keen understanding of financial principles. By mastering your credit score, optimizing your income and debt-to-income ratio, making a substantial down payment, and budgeting comprehensively, you lay a solid foundation for success.

Exploring various lending options, understanding the nuances of the application process, and wisely navigating interest rates and loan terms are all critical steps. Most importantly, proactive loan management post-approval—including timely payments, considering refinancing, and diligently protecting your investment—ensures your large car loan serves as an asset, not a liability.

Remember, the goal isn’t just to get approved, but to get approved for the best possible terms that align with your long-term financial health. Armed with the insights from this guide, you are now well-equipped to make informed decisions and drive away in your dream car with confidence and financial peace of mind. What steps will you take first in your journey to securing a large car loan? Share your thoughts and experiences in the comments below!

Internal Links (Examples – assume these exist on the blog):

- How to Improve Your Credit Score: A Step-by-Step Guide

- Understanding Car Insurance: Types, Coverage, and Savings Tips

External Link (Example):

- For more detailed information on understanding your debt-to-income ratio, you can visit the Consumer Financial Protection Bureau’s guide: CFPB – Debt-to-Income Ratio