Navigating Your $20,000 Car Loan Payment: A Comprehensive Guide to Affordability & Smart Choices

Navigating Your $20,000 Car Loan Payment: A Comprehensive Guide to Affordability & Smart Choices Carloan.Guidemechanic.com

The dream of a new car – or a reliable pre-owned vehicle – often begins with a specific budget in mind. For many, a price point around $20,000 represents an ideal balance of quality, features, and affordability. However, turning that dream into a reality usually involves securing a car loan. Understanding the intricacies of a $20,000 car loan payment is paramount to making a financially sound decision.

It’s not just about the monthly payment figure; it’s about grasping the factors that influence it, how to secure the best terms, and what hidden costs might arise. This comprehensive guide will demystify the entire process, providing you with actionable insights and expert tips. Our goal is to empower you to navigate your $20,000 car loan with confidence, ensuring you get a great deal and a payment that truly fits your budget.

Navigating Your $20,000 Car Loan Payment: A Comprehensive Guide to Affordability & Smart Choices

Understanding the Anatomy of Your $20,000 Car Loan Payment

When you take out a car loan for $20,000, your monthly payment isn’t just a random number. It’s a carefully calculated sum influenced by several critical components. Grasping these elements is the first step toward smart financial planning for your vehicle.

What Makes Up Your Monthly Payment?

Your monthly car payment is primarily composed of two main parts: the principal and the interest. The loan term, or the duration of your repayment, then dictates how these components are spread out over time.

The principal is the actual amount of money you borrowed, which in this case, is $20,000. Each payment you make gradually reduces this principal amount. The interest is the cost you pay for borrowing that money. It’s essentially the lender’s profit for providing you with the funds.

The loan term dictates how long you have to pay back the principal and interest. A shorter term means higher monthly payments but less interest paid overall, while a longer term results in lower monthly payments but more interest accumulating over the life of the loan. Based on my experience, many people focus solely on the monthly payment without considering the total cost of interest over the loan term, which can be a costly mistake.

The Impact of Interest Rates

Interest rates are arguably one of the most significant factors affecting your $20,000 car loan payment. A small percentage difference can translate into hundreds or even thousands of dollars over the life of your loan. These rates are determined by a combination of factors, including your credit score, the overall economic market conditions, and even the type of vehicle you’re financing.

For example, a $20,000 loan at 5% interest over 60 months will have a different total cost than the same loan at 8%. The higher the interest rate, the more expensive your loan becomes. This is why it’s crucial to understand how interest rates work and how to secure the lowest possible rate for your situation.

Pro tip from us: Always shop around for interest rates from multiple lenders before you even step foot in a dealership. Getting pre-approved can give you a strong negotiating position and help you identify the best rates available to you.

The Power of the Loan Term

The loan term, or the length of time you have to repay your $20,000 car loan, has a direct and substantial impact on your monthly payment. Common terms range from 36 months (3 years) to 84 months (7 years), or even longer in some cases.

A shorter loan term, like 36 or 48 months, will result in higher monthly payments. However, you’ll pay off the loan faster and incur significantly less interest over time. Conversely, a longer loan term, such as 72 or 84 months, will offer lower monthly payments, making the car seem more affordable in the short term. The trade-off, though, is that you’ll pay substantially more in interest over the life of the loan.

A common mistake to avoid is stretching out the loan term simply to achieve the lowest possible monthly payment without considering the long-term financial implications. This can lead to paying much more than the car is worth and potentially facing negative equity.

Factors Influencing Your $20,000 Car Loan Approval & Payment

Securing a $20,000 car loan and getting favorable terms isn’t just about the vehicle itself. A range of personal financial factors play a critical role in how lenders assess your application. Understanding these elements can significantly improve your chances of approval and help you secure a manageable payment.

Your Credit Score: The Ultimate Game Changer

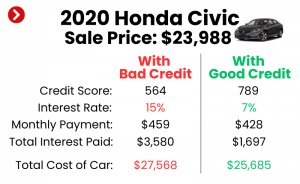

Your credit score is perhaps the single most important factor lenders consider when you apply for a $20,000 car loan. This three-digit number represents your creditworthiness, reflecting your history of managing debt. A higher credit score signals to lenders that you are a low-risk borrower, making you eligible for better interest rates and more favorable loan terms.

For a $20,000 loan, a good to excellent credit score (generally 670 and above) can unlock the lowest advertised interest rates. Conversely, a lower credit score might still get you approved, but likely at a much higher interest rate, significantly increasing your monthly payment and the total cost of the loan. Before applying, it’s wise to check your credit score and report for any errors.

The Importance of a Down Payment

Making a down payment on your $20,000 car loan is a powerful strategy that offers multiple benefits. Firstly, it directly reduces the amount of money you need to borrow, which in turn lowers your monthly payments. Secondly, a larger down payment demonstrates financial responsibility to lenders, potentially making you a more attractive borrower.

Furthermore, a substantial down payment can help you avoid becoming "upside down" on your loan, where you owe more than the car is worth. This is particularly relevant for new cars, which depreciate rapidly.

Pro tip: Aim for at least 10-20% of the vehicle’s purchase price as a down payment for a $20,000 car. This would mean putting down $2,000 to $4,000, which can significantly impact your monthly payment and total interest paid.

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio (DTI) is another crucial metric lenders use to assess your ability to take on additional debt. It’s calculated by dividing your total monthly debt payments (including rent/mortgage, credit cards, student loans, etc.) by your gross monthly income. Lenders typically prefer a DTI of 43% or lower, though some might accept slightly higher ratios depending on other factors.

A high DTI could indicate that you are already overextended financially, making lenders hesitant to approve a new $20,000 car loan, or they might offer less favorable terms. Improving your DTI can involve paying down existing debts or increasing your income.

Income Stability and Employment History

Lenders want assurance that you can consistently make your $20,000 car loan payments. This is why they carefully review your income stability and employment history. They look for a steady job history, ideally with the same employer for a significant period. Consistent income, supported by pay stubs or tax returns, proves your capacity to repay the loan.

For self-employed individuals, lenders might require additional documentation, such as several years of tax returns, to verify income. A stable financial situation is key to lender confidence.

Vehicle Age and Type (Collateral)

The car itself plays a role in the lending decision, as it serves as collateral for the loan. Lenders consider the vehicle’s age, mileage, make, and model. Newer, more reliable vehicles generally pose less risk to lenders, as they hold their value better and are easier to resell if you default.

Some lenders might have restrictions on financing older vehicles or those with very high mileage. This is because such cars are seen as higher risk due to potential maintenance issues and rapid depreciation. For a $20,000 car, whether it’s new or used will influence the loan terms offered.

Calculating Your $20,000 Car Loan Payment & Affordability

Before you fall in love with a specific car, it’s essential to understand what you can truly afford. This goes beyond just looking at the monthly payment. A realistic assessment involves estimating your loan payments and considering all the associated costs of vehicle ownership.

Estimating Your Monthly Payment

While exact calculations can be complex due to varying interest compounding methods, you can get a very good estimate of your $20,000 car loan payment using online calculators. These tools typically require three pieces of information: the principal amount ($20,000), the estimated interest rate, and the desired loan term.

By plugging in different scenarios for interest rates and loan terms, you can quickly see how your monthly payment changes. For example, a $20,000 loan at 6% interest over 60 months might be around $387 per month, while stretching it to 72 months could drop it to approximately $332, but with more total interest paid. These calculators are invaluable for budgeting.

For a deeper dive into car loan calculators, see our guide on ‘Mastering Car Loan Calculators: Your Key to Financial Control’.

What Can You Truly Afford?

Focusing solely on the monthly car payment is a common pitfall. The true cost of owning a $20,000 car extends far beyond that single figure. You need to factor in several other ongoing expenses to get a complete picture of affordability. These include car insurance, fuel costs, routine maintenance, potential repairs, and annual registration fees.

Pro tip: A good rule of thumb often cited in financial circles is the "20/4/10" rule. This suggests a 20% down payment, a loan term no longer than 4 years, and keeping your total car expenses (payment, insurance, fuel) under 10% of your gross monthly income. While a bit conservative for some, it’s a great guideline for true affordability.

Creating a realistic budget that accounts for all these variables is crucial. Don’t let the excitement of a new car blind you to the long-term financial commitment.

Pre-Approval: Your Secret Weapon

Getting pre-approved for your $20,000 car loan before you even visit a dealership is one of the smartest moves you can make. Pre-approval means a lender has already reviewed your financial information and determined how much they are willing to lend you, at what interest rate, and for what term. This effectively gives you a "cash offer" in hand.

The benefits are immense. Firstly, it gives you a clear budget, so you know exactly what you can afford. Secondly, it separates the financing discussion from the car price negotiation. You can focus on getting the best price for the vehicle, knowing your financing is already secured. From my experience, pre-approval transforms your car buying journey from a stressful negotiation to an empowered shopping experience. It forces dealerships to compete for your business, rather than you being at their mercy.

Smart Strategies for Securing and Managing Your $20,000 Car Loan

Once you understand the fundamentals, it’s time to equip yourself with strategies that will help you secure the best possible $20,000 car loan and manage it effectively throughout its term. These tips can save you significant money and stress.

Shopping for the Best Loan

Just as you shop for the best car, you should shop for the best loan. Don’t simply accept the first offer, especially from a dealership. Explore various lending institutions: traditional banks, local credit unions, and online lenders. Each might offer different rates, terms, and fees based on their specific criteria and your financial profile.

Credit unions, in particular, often provide very competitive rates to their members. Online lenders have streamlined application processes and can sometimes offer quick approvals. The key is to compare the Annual Percentage Rate (APR), which includes both the interest rate and any fees, across all offers. This ensures you’re comparing apples to apples.

A common mistake is only looking at one lender, usually the one offered by the dealership. This can lead to missing out on significantly better terms elsewhere.

Negotiating Your Car Price

Remember that the price of the car and the terms of your loan are two separate negotiations. Always aim to settle on the vehicle’s purchase price before discussing financing or monthly payments. If you start by talking about monthly payments, a salesperson can manipulate the loan term or add-ons to reach your desired payment, ultimately costing you more.

By negotiating the price first, you ensure you’re getting the best deal on the vehicle itself. Once that’s settled, you can then present your pre-approved loan offer or discuss financing options with the dealership, comparing them to your existing offer.

Considering Add-ons and Extras

When you’re finalizing the purchase of your $20,000 car, dealerships often present a range of add-ons and extras. These can include extended warranties, GAP insurance, paint protection, fabric protection, and service packages. While some might offer genuine value, others can significantly inflate your loan amount and, consequently, your monthly payment.

Carefully evaluate each add-on. Do you truly need it? Can you get it cheaper elsewhere? For example, GAP insurance might be crucial if you have a small down payment, but an extended warranty might not be necessary if the car comes with a robust manufacturer warranty. Always question these additions and don’t be afraid to decline them if they don’t align with your budget or needs.

Refinancing Your $20,000 Car Loan

Even after you’ve secured your $20,000 car loan, your financial journey isn’t over. Refinancing is a strategy worth considering if market interest rates have dropped, your credit score has improved significantly since you took out the original loan, or you simply want to adjust your monthly payments.

Refinancing involves taking out a new loan to pay off your existing car loan. If you qualify for a lower interest rate, you can reduce your monthly payment or save a substantial amount on total interest over the life of the loan. It’s also an option if you initially received a high-interest rate due to poor credit and have since improved your financial standing.

Learn more about refinancing options and whether they’re right for you from the Consumer Financial Protection Bureau (CFPB).

Making Extra Payments

One of the most effective ways to save money on your $20,000 car loan is by making extra payments whenever possible. Even small additional payments can significantly accelerate your repayment schedule and reduce the total interest you pay over the loan term. This is because every extra dollar goes directly towards reducing your principal balance.

Before making extra payments, always confirm with your lender that there are no prepayment penalties. Most standard car loans do not have them, but it’s always best to check your loan agreement. Whether it’s an extra $50 a month, a lump sum from a bonus, or rounding up your payment, these efforts add up quickly.

Beyond the Payment: Total Cost of Ownership for a $20,000 Vehicle

While the $20,000 car loan payment is a major consideration, it’s just one piece of the puzzle. To truly understand the financial commitment, you must look at the total cost of ownership. Overlooking these additional expenses can quickly derail your budget.

Insurance Costs

Car insurance is a mandatory expense that can vary dramatically based on your location, age, driving history, and the specific make and model of your $20,000 vehicle. A high-performance car will generally cost more to insure than a more economical model. It’s crucial to get insurance quotes before you finalize your car purchase.

Don’t assume your current insurance rates will remain the same. A new vehicle, even one in the same price range, can have different repair costs or safety ratings, impacting your premiums. Factor this into your overall monthly budget.

Maintenance & Repairs

Every car, whether new or used, requires maintenance. This includes routine oil changes, tire rotations, fluid checks, and brake inspections. For a used $20,000 car, potential repair costs can be higher, especially if it’s out of warranty. Research the reliability of the specific model you’re considering.

Allocating a small amount each month to a "car maintenance fund" is a smart financial habit. This way, unexpected repairs won’t throw your budget into chaos.

Fuel & Registration

These are the ongoing, often overlooked, expenses. Fuel costs will depend on the car’s fuel efficiency, current gas prices, and how much you drive. A vehicle with lower miles per gallon (MPG) will naturally cost more to operate.

Annual registration fees, state inspections, and property taxes (in some states) are also recurring costs. While they might not be monthly, they are significant annual expenditures that need to be accounted for in your financial planning for a $20,000 car.

Depreciation

Depreciation is the hidden cost of car ownership – the loss in value of your vehicle over time. Cars start to depreciate the moment they leave the dealership lot. While you don’t write a check for depreciation, it impacts your financial standing, especially if you ever need to sell or trade in the vehicle.

For a $20,000 car, understanding its depreciation rate can help you make a smarter long-term investment. Some cars hold their value better than others. This is particularly important if you plan to trade in your car in a few years, as it affects your equity.

Conclusion

Navigating a $20,000 car loan payment requires a blend of careful planning, financial savvy, and a willingness to do your homework. It’s more than just finding a car you like; it’s about making an informed decision that aligns with your overall financial health. By understanding the core components of your loan, leveraging your credit score, making a smart down payment, and diligently comparing offers, you can secure the best possible terms.

Remember to look beyond the monthly payment and consider the total cost of ownership, including insurance, maintenance, and fuel. Utilizing tools like pre-approval and consistently reviewing your options, such as refinancing, ensures you remain in control. With these strategies, you can confidently drive away in your $20,000 vehicle, knowing you’ve made a smart and sustainable financial choice. Start planning today, and empower your car buying journey!