Navigating Your $50,000 Car Loan Repayments: The Ultimate Guide to Smart Financing

Navigating Your $50,000 Car Loan Repayments: The Ultimate Guide to Smart Financing Carloan.Guidemechanic.com

The allure of a brand-new car, or perhaps a pre-owned luxury vehicle, often comes with a significant price tag. For many, a $50,000 car loan is the gateway to driving their dream machine. While the excitement of a new ride is undeniable, the reality of managing substantial $50,000 car loan repayments can feel daunting. This isn’t just about monthly payments; it’s about understanding the intricate financial landscape that underpins such a significant commitment.

Securing a $50,000 car loan is a major financial decision that impacts your budget for years to come. Making informed choices from the outset can save you thousands of dollars and considerable stress. This comprehensive guide will dissect every aspect of a $50,000 car loan, equipping you with the knowledge to make smart decisions, optimize your repayments, and ensure your financial well-being. Let’s embark on this journey to master your car financing.

Navigating Your $50,000 Car Loan Repayments: The Ultimate Guide to Smart Financing

Understanding the Core Components of a $50,000 Car Loan

Before diving into repayment strategies, it’s crucial to grasp the fundamental elements that constitute any car loan, especially one of this magnitude. A $50,000 car loan isn’t just the sticker price; it’s a complex package influenced by several key variables. Ignoring any of these can lead to unexpected costs and a less favorable repayment experience.

The Principal Amount: The Foundation of Your Debt

The $50,000 is your principal, the initial amount you borrow to purchase the vehicle. This figure forms the bedrock of your loan. Every repayment you make will go towards reducing this principal, along with the accrued interest.

Understanding the principal’s role is critical because a larger principal naturally leads to higher interest charges over time. Your goal should always be to reduce the principal as efficiently as possible, whether through a down payment or accelerated repayments.

Interest Rate: The Silent Cost of Borrowing

The interest rate is arguably the most significant factor affecting your $50,000 car loan repayments. It’s the cost of borrowing money, expressed as a percentage of the principal. A seemingly small difference in interest rates can translate into thousands of dollars over the life of your loan.

Interest rates can be either fixed or variable. A fixed interest rate remains constant throughout the loan term, providing predictable monthly payments. Variable rates, however, can fluctuate with market conditions, meaning your payments could go up or down.

Loan Term: The Duration and Its Impact

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 60 months, 72 months, 84 months). This factor directly influences both your monthly payment amount and the total interest you’ll pay. A longer loan term generally results in lower monthly payments, making the car seem more affordable upfront.

However, a longer term also means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term will have higher monthly payments but will save you money on interest in the long run.

Other Fees: The Hidden Expenses

Beyond the principal and interest, car loans often come with various fees that can add to your overall cost. These might include origination fees, documentation fees, application fees, or even prepayment penalties if you pay off your loan early. Always scrutinize the loan agreement for these charges.

Understanding these fees upfront prevents unwelcome surprises later. Don’t hesitate to ask your lender for a full breakdown of all associated costs before signing any paperwork.

Factors That Significantly Influence Your $50,000 Car Loan Repayments

Securing a $50,000 car loan isn’t a one-size-fits-all scenario. Several personal and market factors profoundly influence the terms you’ll receive and, consequently, your $50,000 car loan repayments. Being aware of these elements empowers you to negotiate better terms and make more advantageous choices.

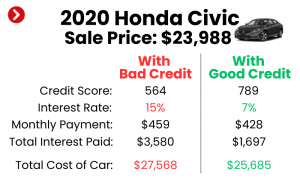

Your Credit Score: The Ultimate Rate Decider

Your credit score is perhaps the most critical determinant of the interest rate you’ll be offered. Lenders use this three-digit number to assess your creditworthiness and the risk associated with lending you money. A higher credit score (typically 700+) indicates a responsible borrower and often qualifies you for the lowest interest rates available.

Conversely, a lower credit score will likely result in a higher interest rate, as lenders perceive a greater risk. Based on my experience, a difference of even 1-2% due to credit score can mean thousands of dollars in extra interest over the life of a $50,000 loan. Improving your credit score before applying is a powerful strategy.

The Power of a Down Payment

A down payment is the initial sum of money you pay upfront towards the purchase of the car, reducing the amount you need to borrow. Making a significant down payment has several compelling benefits for your $50,000 car loan repayments. Firstly, it directly lowers your principal loan amount, which means less interest accrued over time.

Secondly, a larger down payment can make you a more attractive borrower to lenders, potentially qualifying you for better interest rates. Lastly, it helps mitigate the issue of "upside-down" loans, where you owe more on the car than it’s worth, which is common with new cars due to immediate depreciation.

Loan Term Revisited: Short vs. Long

While we touched on the loan term earlier, its impact on your repayment strategy warrants a deeper look. A shorter loan term, say 48 or 60 months, means higher monthly payments. This can be a stretch for some budgets. However, the financial benefit is substantial: you pay significantly less in total interest because you’re paying off the principal quicker.

A longer loan term, like 72 or 84 months, reduces your monthly financial burden, making the $50,000 car loan feel more manageable. The trade-off, however, is a much higher total interest paid over the extended period. You also risk owing more than the car is worth for a longer duration.

Interest Rate Type: Fixed vs. Variable

The choice between a fixed and variable interest rate carries different levels of risk and predictability. A fixed rate offers stability; your monthly payments will remain the same for the entire loan term, regardless of market fluctuations. This predictability is ideal for budgeting and peace of mind.

A variable rate, tied to an index like the prime rate, can change over time. While it might start lower than a fixed rate, there’s a risk that it could increase, raising your monthly payments. Conversely, it could also decrease. For a $50,000 car loan, most borrowers prefer the certainty of a fixed rate.

Lender Choice: Shop Around for the Best Deal

The institution you choose to borrow from can significantly affect your loan terms. Banks, credit unions, dealership financing, and online lenders all offer car loans, but their rates and terms can vary widely. Credit unions, for instance, often offer competitive rates due to their member-focused structure.

Dealership financing can be convenient, but it’s essential to compare their offers with pre-approvals from other lenders. Pro tips from us: Always get pre-approved by at least two to three different lenders before stepping foot in a dealership. This gives you leverage and a benchmark for comparison.

Calculating Your $50,000 Car Loan Repayments: Scenarios and Examples

Understanding the theoretical components is one thing; seeing them in action provides real clarity. Let’s explore some practical scenarios for a $50,000 car loan to illustrate how different factors impact your monthly payments and overall costs. While precise calculations depend on specific loan amortizations, these examples provide a strong approximation.

The basic formula for a loan payment involves the principal, interest rate, and loan term. Most online calculators utilize this formula, which is often complex to do manually. However, we can illustrate the outcomes effectively.

Scenario 1: The Favorable Borrower

Imagine you have excellent credit (e.g., 750+), make a healthy $10,000 down payment, and secure a competitive interest rate of 5% over a 60-month (5-year) loan term.

- Loan Amount: $50,000 – $10,000 (down payment) = $40,000

- Interest Rate: 5.0%

- Loan Term: 60 months

- Estimated Monthly Payment: Approximately $755

- Total Interest Paid: Around $5,300

In this scenario, your monthly payment is manageable, and the total interest paid is relatively low, demonstrating the benefits of strong credit and a substantial down payment.

Scenario 2: The Average Borrower

Now, consider a borrower with an average credit score (e.g., 650), who makes a smaller $5,000 down payment, and receives an interest rate of 8% over an extended 72-month (6-year) loan term.

- Loan Amount: $50,000 – $5,000 (down payment) = $45,000

- Interest Rate: 8.0%

- Loan Term: 72 months

- Estimated Monthly Payment: Approximately $790

- Total Interest Paid: Around $11,800

Notice the significant difference. Despite a larger loan amount in Scenario 1 ($40k vs $45k), the higher interest rate and longer term in Scenario 2 lead to higher monthly payments and more than double the total interest paid. This clearly highlights the compounding effect of interest over time.

Scenario 3: The Extended Term

Let’s look at the impact of an even longer term for the $45,000 loan at 8% interest, but stretched to 84 months (7 years).

- Loan Amount: $45,000

- Interest Rate: 8.0%

- Loan Term: 84 months

- Estimated Monthly Payment: Approximately $685

- Total Interest Paid: Around $12,700

While the monthly payment is lower in this scenario, making the car seem more affordable, the total interest paid is even higher. This clearly illustrates the trade-off between lower monthly payments and increased overall cost. Pro tips from us: Always use an online car loan calculator to get precise figures before committing. These tools provide transparency and allow you to model various scenarios.

Strategies to Optimize Your $50,000 Car Loan Repayments

Managing a $50,000 car loan effectively requires more than just making timely payments. Strategic planning and proactive measures can significantly reduce your overall cost and accelerate your path to ownership. Here are proven strategies to optimize your $50,000 car loan repayments.

Making a Larger Down Payment

As seen in our scenarios, a larger down payment is one of the most immediate and impactful ways to reduce your total loan cost. By lowering the principal amount borrowed, you directly decrease the amount of interest you’ll pay over the loan’s lifetime. Aim for at least 20% of the car’s value if possible, especially for new vehicles, to counteract initial depreciation.

This also strengthens your financial position, signaling to lenders that you’re a lower-risk borrower, which can sometimes lead to even better interest rates.

Choosing a Shorter Loan Term (If Affordable)

While lower monthly payments can be tempting, resisting the urge to stretch your loan term excessively can save you a substantial amount in interest. If your budget allows, opt for the shortest loan term you can comfortably afford. This strategy accelerates your equity building in the vehicle and frees up your monthly budget sooner.

Remember, a $50,000 car loan over 60 months will cost you significantly less in total interest than the same loan over 84 months, even if the monthly payments are higher.

Improving Your Credit Score Before Applying

Your credit score is your financial resume. Taking steps to improve it before you apply for a $50,000 car loan can unlock significantly better interest rates. Pay down existing debts, avoid opening new credit lines, and check your credit report for errors. Even a few points increase can translate into hundreds, or even thousands, of dollars saved.

Lenders are more willing to offer their most competitive rates to borrowers with excellent credit histories, viewing them as reliable.

Shopping Around for Lenders

Never settle for the first loan offer you receive. Lenders have different criteria and risk assessments, leading to varying interest rates and terms. Contact multiple banks, credit unions, and online lenders to compare offers. Get pre-approved by several institutions.

This competitive shopping allows you to identify the best possible terms for your $50,000 car loan repayments. It also gives you leverage when negotiating with a dealership, as you’ll have external offers to benchmark against.

Refinancing Your Car Loan

If market interest rates drop, your credit score has improved since you first took out the loan, or you simply found a better offer, refinancing your car loan can be a powerful strategy. Refinancing involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms.

This can significantly reduce your monthly payments or the total interest you pay. For a deeper dive into refinancing, check out our guide on .

Making Extra Payments

Even small, consistent extra payments can make a big difference over time. By paying more than your required monthly amount, you directly reduce the principal balance faster. This, in turn, means less interest accrues on the principal over the remaining loan term.

Pro tips from us: Even an extra $50-100 per month can significantly reduce your loan term and total interest paid on a $50,000 car loan. Consider setting up bi-weekly payments, which essentially add one extra monthly payment per year without feeling like a huge burden.

Common Mistakes to Avoid with a $50,000 Car Loan

While the strategies above focus on optimizing your loan, it’s equally important to be aware of pitfalls that can derail your financial plans. Avoiding these common mistakes is crucial for responsible management of your $50,000 car loan repayments.

Focusing Only on Monthly Payments

This is perhaps the most common mistake. Many borrowers fixate solely on achieving the lowest possible monthly payment without considering the total cost of the loan. As our scenarios showed, a lower monthly payment often comes with a longer loan term and significantly more interest paid over time. Always ask for the total cost of the loan, not just the monthly installment.

Not Budgeting for Additional Costs

The car loan payment is just one piece of the puzzle. A $50,000 vehicle will also come with substantial additional costs. These include higher insurance premiums, increased fuel consumption (especially for performance or luxury vehicles), routine maintenance, and potential repair costs. Failing to budget for these can strain your finances, even if your loan payments are manageable.

Skipping the Down Payment Entirely

While tempting to drive off with no money down, this is rarely a wise financial move, especially for a $50,000 vehicle. A zero-down payment means you’re financing the entire cost of the car, including taxes and fees. This immediately puts you in an "upside-down" position, where you owe more than the car is worth due to instant depreciation.

This makes it harder to sell or trade in the car later and increases your total interest paid.

Not Reading the Fine Print

Loan agreements are often long and filled with legal jargon, but it’s imperative to read every word. Overlooking details about prepayment penalties, late fees, or specific terms and conditions can lead to costly surprises down the road. If something is unclear, ask for clarification before signing.

Common mistakes to avoid are signing up for an extended loan term just to lower monthly payments without considering the long-term interest burden. Always understand what you’re agreeing to.

Ignoring Your Credit Score

Neglecting your credit score before and during the loan process is a missed opportunity. A poor credit score will undoubtedly lead to higher interest rates, costing you thousands more. Furthermore, failing to monitor your credit during the loan term means you might miss opportunities to refinance at a better rate if your score improves.

Regularly checking your credit report for accuracy and actively working to improve your score is a smart financial habit. You can access your credit report for free annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com.

The Road Ahead: Managing Your Loan and Future Planning

Once you’ve secured your $50,000 car loan and driven off the lot, your financial journey with the vehicle is far from over. Effective loan management and future planning are key to ensuring your car remains an asset, not a burden. Proactive steps can enhance your financial stability and prepare you for what lies ahead.

Budgeting: Integrating Car Payments into Your Overall Financial Plan

Your car loan payment needs to fit comfortably within your broader budget. It shouldn’t consume a disproportionate amount of your income, leaving you short for other essentials or savings. Create a detailed monthly budget that accounts for all income and expenses, including your $50,000 car loan repayments, insurance, fuel, and maintenance.

This holistic view ensures that your car doesn’t become a source of financial stress.

Emergency Fund: Your Financial Safety Net

Life is unpredictable, and unexpected expenses can arise, from job loss to sudden medical bills. Having a robust emergency fund (typically 3-6 months of living expenses) is crucial when you have significant debt like a $50,000 car loan. This fund acts as a buffer, preventing you from missing payments or racking up high-interest credit card debt if financial difficulties strike.

Reviewing Your Loan Annually: Is Refinancing Still an Option?

Don’t assume your initial loan terms are set in stone for the entire duration. Market conditions change, and your financial situation can improve. Make it a habit to review your loan annually. Check current interest rates and assess if your credit score has improved enough to qualify for a better rate through refinancing.

Even a small reduction in interest can lead to significant savings over the remaining term of your $50,000 car loan.

Selling or Trading In: Understanding Residual Value

As your loan progresses, so does your car’s depreciation. Understand your vehicle’s residual value – what it’s expected to be worth at a certain point in time. This is particularly important if you plan to sell or trade in your car before the loan is fully paid off. Knowing your car’s market value versus your remaining loan balance helps you avoid negative equity and plan your next vehicle purchase wisely. Explore more financial planning strategies in our comprehensive article on .

Conclusion: Driving Towards Financial Freedom

Navigating a $50,000 car loan repayment journey requires diligence, foresight, and a solid understanding of financial principles. It’s a significant commitment, but with the right approach, it doesn’t have to be an overwhelming one. By understanding the core components of your loan, recognizing the factors that influence your terms, and employing smart strategies, you can transform a potential burden into a manageable part of your financial life.

Remember to prioritize a strong credit score, make a healthy down payment, shop around for the best rates, and be proactive in managing your loan through extra payments or refinancing when appropriate. Avoid common pitfalls like focusing solely on monthly payments or neglecting the fine print. With these insights, you are well-equipped to make informed decisions about your $50,000 car loan repayments, ensuring a smoother ride toward financial freedom and enjoying your dream car without unnecessary stress.