Navigating Your Auto Loan Journey: What a 726 Credit Score Means for Your Car Financing

Navigating Your Auto Loan Journey: What a 726 Credit Score Means for Your Car Financing Carloan.Guidemechanic.com

Embarking on the exciting journey of buying a new or used car often comes with the crucial step of securing financing. For many, this process can feel overwhelming, filled with complex terms and varying interest rates. However, if you’re entering this arena with a 726 credit score, you’re already in an excellent position. This isn’t just a good score; it’s a powerful asset that can unlock some of the most favorable car loan terms available.

This comprehensive guide will delve deep into what a 726 credit score signifies for your auto loan, how to leverage it, and what steps to take to ensure you get the absolute best deal. We aim to equip you with the knowledge and confidence to navigate the car financing landscape like a seasoned professional. By the end of this article, you’ll understand why your 726 credit score is a golden ticket and how to use it wisely.

Navigating Your Auto Loan Journey: What a 726 Credit Score Means for Your Car Financing

Understanding Your 726 Credit Score: A Mark of Financial Responsibility

A 726 credit score places you firmly in the "Good" to "Excellent" range, depending on the specific scoring model (FICO or VantageScore). This is a credit score that lenders genuinely appreciate. It signals that you are a responsible borrower with a strong history of managing your debts effectively.

Most lenders consider anything above 670 to be good, and scores above 740 are often categorized as excellent. Your 726 score is just shy of excellent, putting you in a very desirable tier for financial institutions. This means they view you as a low-risk borrower, which directly translates into better lending opportunities.

What Makes Up Your Credit Score?

Your 726 score is a reflection of several key financial habits, meticulously calculated by credit bureaus. Understanding these components helps you appreciate the value of your current score and how to maintain it.

- Payment History (35%): This is the most crucial factor. A 726 score indicates a consistent history of paying your bills on time, every time.

- Amounts Owed (30%): Also known as credit utilization, this refers to how much of your available credit you’re using. A low utilization ratio (ideally under 30%) contributes significantly to a good score.

- Length of Credit History (15%): The longer your accounts have been open and in good standing, the better. A mature credit profile shows stability.

- New Credit (10%): Opening too many new credit accounts in a short period can temporarily lower your score. Your 726 suggests a balanced approach to new credit.

- Credit Mix (10%): Having a healthy mix of different credit types, such as credit cards, installment loans, and mortgages, demonstrates your ability to manage various forms of credit responsibly.

A 726 credit score is a testament to your diligent financial management across these areas. It’s a badge of honor that opens many doors, especially when it comes to securing a car loan.

The Power of a 726 Credit Score for Car Loans

Your strong credit score isn’t just a number; it’s a powerful tool that significantly impacts the cost and terms of your auto loan. Lenders compete for borrowers like you because you represent minimal risk. This competitive environment works in your favor, translating into tangible benefits.

1. Access to Lower Interest Rates

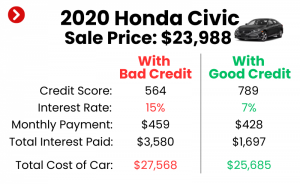

This is arguably the most significant advantage. With a 726 credit score, you’ll be offered some of the most competitive interest rates available on the market. Lenders view you as highly likely to repay your loan, so they’re willing to offer lower rates to attract your business.

Based on my experience as a financial expert, the difference between a "good" credit score rate and an "average" score rate can be substantial. Even a single percentage point difference in your Annual Percentage Rate (APR) can save you hundreds, if not thousands, of dollars over the life of a typical car loan. For instance, on a $30,000 loan over five years, a 6% APR versus an 8% APR could save you over $1,800 in total interest paid.

2. More Favorable Loan Terms

Beyond just the interest rate, a 726 credit score gives you leverage to negotiate other aspects of your loan. You might be approved for a longer loan term, which can lower your monthly payments, or a shorter term, which saves you more on interest. Lenders are often more flexible with repayment schedules and conditions for borrowers with excellent credit.

This flexibility can be crucial for aligning your car loan with your personal budget and financial goals. You’re not just taking what’s offered; you have the power to shape the deal.

3. Wider Range of Lender Options

With a 726 credit score, you’re not limited to subprime lenders or specific dealerships. You can confidently approach traditional banks, credit unions, and various online lenders, knowing you’ll be a preferred customer. This expansive choice allows you to shop around more effectively and find the lender offering the absolute best deal tailored to your needs.

Pro tips from us: Don’t just settle for the first offer. Leverage your strong credit to get multiple quotes and pit lenders against each other.

4. Reduced or No Down Payment Requirements

Lenders are more confident in your ability to repay the loan, even without a substantial upfront payment. While putting money down is always a good financial move, a 726 score means you might not have to if your budget is tight. This can free up your savings for other immediate needs or allow you to get into your desired vehicle sooner.

However, even if not required, a larger down payment is always beneficial. It reduces the total amount you finance, which in turn lowers your monthly payments and the overall interest you’ll pay.

5. Streamlined and Quicker Approval Process

Your strong credit profile simplifies the lender’s decision-making process. They spend less time assessing your risk, which often leads to quicker approvals. You might even receive instant online approval from many lenders. This efficiency can be a huge advantage, especially when you’re eager to drive off in your new car.

Based on my experience, a strong credit score often means less paperwork and fewer hoops to jump through, making the entire car-buying experience much smoother and less stressful.

Preparing for Your Car Loan Application

Even with a fantastic 726 credit score, preparation is key to ensuring a smooth process and securing the best possible terms. Don’t leave anything to chance.

1. Check Your Credit Report Thoroughly

While your score is excellent, errors can sometimes creep into your credit report. These inaccuracies, though rare with a high score, could potentially impact a lender’s decision or the rate they offer. It’s always wise to review your full credit report before applying for any significant loan.

You can get a free copy of your credit report from each of the three major bureaus (Equifax, Experian, and TransUnion) once every 12 months. Visit AnnualCreditReport.com to access yours. Scrutinize every detail for anything that doesn’t look right.

2. Determine Your Realistic Budget

Before you even start looking at cars, understand what you can truly afford. This goes beyond just the monthly loan payment. Factor in:

- Insurance costs: Premiums can vary significantly based on the car’s make, model, age, and your driving history.

- Fuel expenses: Consider the car’s fuel efficiency and your typical driving habits.

- Maintenance and repairs: All cars require upkeep. Research common maintenance costs for models you’re considering.

- Registration and taxes: Don’t forget these upfront and recurring costs.

Common mistakes to avoid are: Falling in love with a car that stretches your budget too thin, leaving no room for unexpected expenses. Always consider the total cost of ownership.

3. Save for a Down Payment (If Possible)

As mentioned, a 726 score might exempt you from a required down payment. However, making one is almost always a smart financial move.

Pro tips from us: A down payment of 10-20% of the car’s value is ideal. It reduces the principal loan amount, lowers your monthly payments, and decreases the total interest paid over time. It also helps prevent you from being "upside down" on your loan (owing more than the car is worth) early on.

4. Gather Necessary Documents

Being organized saves time and reduces stress. Have these documents ready before you start applying:

- Proof of Identity: Driver’s license, passport.

- Proof of Income: Pay stubs (recent 2-3 months), W-2s, tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a specific car (VIN, mileage, etc.).

5. Get Pre-Approved Before You Shop

This is perhaps the most powerful step you can take with a 726 credit score. Getting pre-approved means a lender has already evaluated your creditworthiness and agreed to lend you a certain amount at a specific interest rate, before you’ve even picked out a car.

Based on my experience, pre-approval transforms you into a cash buyer at the dealership. You walk in knowing your financing is secure, giving you immense negotiation power on the car’s price. It also helps you understand your budget limits clearly.

Navigating the Car Loan Process with a 726 Score

Now that you’re prepared, it’s time to leverage your 726 credit score to secure the best car loan. This involves strategic shopping for both the loan and the vehicle.

Where to Apply for Your Loan

With your excellent credit, you have a wide array of options. Explore each to find the best fit:

- Traditional Banks: Your existing bank might offer competitive rates as a loyal customer. Check national and local banks.

- Credit Unions: Often known for offering highly competitive rates and personalized service, as they are member-owned.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer quick online applications and competitive rates. They provide convenience and often quick decisions.

- Dealership Financing: While convenient, these offers are often marked up. However, dealerships sometimes have special manufacturer incentives that can be very attractive. Use their offer as a benchmark, but don’t assume it’s the best.

Pro tips from us: Apply to 2-3 different lenders for pre-approval within a short window (typically 14-45 days, depending on the credit scoring model). Multiple inquiries within this period will usually count as a single hard inquiry on your credit report, minimizing the impact on your score.

Comparing Loan Offers Effectively

Once you have a few pre-approval offers, it’s time to compare them thoroughly. Don’t just look at the monthly payment.

- Annual Percentage Rate (APR): This is the most crucial number. It represents the true cost of borrowing, including interest and certain fees. A lower APR means less money paid over the life of the loan.

- Loan Term: How long will you be paying back the loan? Shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more interest paid.

- Total Cost of the Loan: Multiply the monthly payment by the number of months in the loan term, then add any upfront fees. This gives you the full picture.

- Any Fees: Look for origination fees, application fees, or prepayment penalties. With a 726 score, you should ideally avoid loans with significant fees.

Negotiating the Best Deal

Armed with your pre-approval and comparative offers, you’re in a powerful position at the dealership.

- Negotiate the Car Price Separately: First, focus on getting the best possible price for the vehicle itself. Do your research on fair market value. Your pre-approval allows you to treat the car purchase as a cash transaction.

- Then, Compare Financing: Once you’ve agreed on a car price, then you can compare the dealership’s financing offer with your pre-approval. If the dealership can beat your pre-approved APR, great! If not, stick with your pre-approval.

- Be Ready to Walk Away: This is your ultimate negotiation tool. If you don’t feel you’re getting a fair deal on either the car or the financing, be prepared to leave. There are always other cars and other dealerships.

Common mistakes to avoid are: Letting the dealership distract you by focusing only on a low monthly payment. This can hide a higher interest rate or a longer loan term, costing you more in the long run. Always focus on the total price of the car and the APR of the loan.

Maximizing Your 726 Credit Score Advantage

Having a 726 credit score puts you in an enviable position, but there are still ways to optimize your auto loan further and maintain your financial health.

Consider a Shorter Loan Term

If your budget allows, opting for a shorter loan term (e.g., 36 or 48 months instead of 60 or 72) can save you a significant amount in interest. While your monthly payment will be higher, the total cost of the loan will be much lower.

For example, a $30,000 loan at 5% APR over 60 months results in approximately $3,950 in interest. The same loan over 36 months would incur about $2,350 in interest, saving you over $1,600.

Make a Larger Down Payment

As discussed, a larger down payment reduces the amount you need to borrow, directly lowering your monthly payments and the total interest paid. It also creates immediate equity in your vehicle, protecting you from being upside down on your loan.

Explore Refinancing Opportunities

Even with a great initial rate, market conditions can change, or your credit score might improve further (though 726 is already excellent). Keep an eye on interest rates; if they drop significantly after you’ve taken out your loan, you might consider refinancing. This could potentially lower your monthly payments or reduce the total interest you pay.

Maintain Excellent Credit Habits

Your 726 credit score is a result of consistent good financial behavior. To keep it that way, continue:

- Paying all bills on time: This is the bedrock of good credit.

- Keeping credit utilization low: Aim for under 30% on all revolving credit.

- Monitoring your credit report: Regularly check for any suspicious activity or errors.

- Being mindful of new credit applications: Only open new accounts when truly necessary.

For more detailed insights on maintaining and even boosting your credit score, you might find our article on "Boosting Your Credit Score: A Comprehensive Guide" (Internal Link Placeholder) highly beneficial.

Common Misconceptions and Pro Tips

Even with a solid credit score, there are pitfalls to avoid and smart strategies to employ.

Common Misconceptions to Avoid:

- A 726 score guarantees the absolute lowest interest rate: While your score is excellent, the absolute lowest rates (like 0% APR) are often promotional offers tied to specific new vehicles or require even higher scores and perfect financial profiles. Your rate will be very competitive, but not necessarily the lowest possible in every scenario.

- Dealership financing is always the most expensive: Not always. Sometimes, manufacturers offer special low-APR financing through their captive finance companies (e.g., Toyota Financial Services, Ford Credit) that can beat third-party lenders. Always compare their offer to your pre-approval.

- Focusing only on the monthly payment: As highlighted, this is a dangerous trap. A low monthly payment can hide a longer loan term or a higher interest rate, leading to more interest paid overall.

Pro Tips from Us:

- Shop for rates before you shop for the car: This empowers you to negotiate the car’s price more effectively and ensures you have a baseline for financing.

- Understand all the fine print: Read your loan agreement carefully. Know your APR, loan term, any fees, and what happens if you miss a payment.

- Be wary of add-ons: Dealerships often try to sell you extended warranties, GAP insurance, paint protection, and other extras. While some might be useful, they significantly increase the total cost of your loan. Evaluate each one critically and negotiate their prices separately, or decline them if unnecessary.

- Don’t forget about insurance: Get insurance quotes for cars you’re considering before you buy. A high-performance or luxury vehicle will have significantly higher premiums, which can impact your overall budget.

Beyond the Loan – Post-Purchase Considerations

Your journey doesn’t end when you drive off the lot. A responsible car owner considers the long-term implications.

Insurance: A Crucial Expense

The make, model, and year of your car, combined with your driving record, will heavily influence your insurance premiums. Always factor this into your budget. For example, a sports car will almost certainly cost more to insure than a family sedan.

Maintenance and Upkeep

Every vehicle requires regular maintenance. Budget for oil changes, tire rotations, brake inspections, and unexpected repairs. Researching the reliability and average maintenance costs of your chosen vehicle can save you headaches and money down the road.

Resale Value

While not a direct part of your loan, the car’s depreciation and potential resale value are important financial considerations. Some cars hold their value better than others. This can impact your financial position if you decide to sell or trade in the vehicle in the future.

For a deeper dive into how different financing options impact your long-term financial health, consider reading our article "Understanding Car Loan APR vs. Interest Rate: What You Need to Know" (Internal Link Placeholder).

Conclusion: Your 726 Credit Score – A Foundation for Success

Your 726 credit score is a testament to your excellent financial management and provides a solid foundation for securing a highly favorable car loan. It positions you as a low-risk, desirable borrower, opening doors to lower interest rates, flexible terms, and a wider choice of lenders.

By thoroughly preparing, shopping around for the best rates, and negotiating wisely, you can leverage your strong credit to save thousands of dollars over the life of your auto loan. Remember to focus on the overall cost, not just the monthly payment, and always read the fine print. With careful planning and the power of your 726 credit score, you’re well-equipped to make a smart, informed decision that benefits your financial future.

Don’t let this incredible financial asset go to waste. Start your car loan journey today with confidence, knowing you have a significant advantage in the market!