Navigating Your Car Loan After Purchase: A Comprehensive Guide to Financial Freedom on Four Wheels

Navigating Your Car Loan After Purchase: A Comprehensive Guide to Financial Freedom on Four Wheels Carloan.Guidemechanic.com

The exhilarating feeling of driving a new or new-to-you car off the lot is unmatched. The scent of fresh upholstery, the purr of the engine, the open road ahead – it’s a moment of pure joy. Yet, beneath that excitement lies a significant financial commitment: your car loan. Many drivers focus intensely on securing the best deal before the purchase, but what happens after?

Managing your car loan after purchase is just as crucial, if not more so, than the initial negotiation. It’s a journey that can lead to significant savings, peace of mind, or, if mismanaged, unnecessary financial stress. This in-depth guide is designed to empower you with the knowledge and strategies to not just manage, but master your automotive financing post-purchase. We’ll explore everything from understanding your agreement to advanced strategies for early payoff and navigating unexpected challenges.

Navigating Your Car Loan After Purchase: A Comprehensive Guide to Financial Freedom on Four Wheels

The Post-Purchase Reality: What Happens After You Drive Off?

The ink is dry on the paperwork, and the keys are in your hand. While the initial excitement is palpable, it’s essential to shift your focus to the practicalities of your car loan after purchase. This is where the long-term commitment truly begins. Many people mistakenly believe their work is done once they leave the dealership, but that’s far from the truth.

Your car loan agreement is a legally binding contract. It outlines your responsibilities, the lender’s terms, and the financial trajectory of your vehicle ownership. Taking the time to thoroughly review every detail of this document is paramount.

Understanding your loan terms means knowing your interest rate, the total amount financed, the monthly payment, and the duration of the loan. Don’t forget to identify any fees, such as late payment penalties or prepayment clauses. A clear grasp of these elements forms the foundation of effective post-purchase loan management.

Mastering Your Monthly Payments: Strategies for Smooth Sailing

Consistent and timely payments are the cornerstone of responsible loan management. Falling behind can quickly snowball into serious financial trouble, impacting your credit score and potentially leading to repossession. Proactive strategies can help ensure your payments are always on track.

Pro tips from us: Automate your car loan payments. Setting up automatic deductions from your checking account ensures you never miss a due date. This simple step eliminates the risk of human error and helps build a strong payment history, which is crucial for your credit health.

Another vital strategy involves creating a detailed personal budget. Integrate your car payment seamlessly into your monthly financial plan. Understanding exactly where your money goes allows you to allocate funds effectively, preventing payment surprises.

It’s also beneficial to understand your loan’s amortization schedule. This schedule illustrates how your payments are divided between principal and interest over the life of the loan. In the early stages, a larger portion of your payment typically goes towards interest.

Common mistakes to avoid are making only the minimum payment and not understanding the long-term cost. While minimum payments keep you compliant, they often prolong the loan duration and maximize the total interest paid. Aiming to pay more than the minimum, even a small amount, can significantly reduce your overall cost and shorten your loan term.

The Power of Refinancing Your Car Loan: A Game Changer

One of the most impactful strategies available for managing your car loan after purchase is refinancing. This involves taking out a new loan to pay off your existing car loan, often with more favorable terms. It’s a powerful tool that can significantly alter your financial landscape.

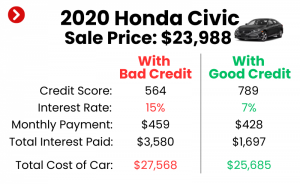

Refinancing can be a game-changer if your financial situation has improved since you first secured the loan. Perhaps your credit score has increased, or interest rates have dropped. Both scenarios could qualify you for a lower annual percentage rate (APR) on a new loan.

The primary benefits of refinancing are compelling. A lower interest rate translates directly into saving hundreds, or even thousands, of dollars over the life of the loan. It can also lead to lower monthly payments, freeing up cash flow for other expenses or savings goals. Alternatively, you might choose to shorten your loan term, paying off the car faster and saving on total interest.

Based on my experience, refinancing is often overlooked by car owners, yet it’s one of the most effective ways to optimize your car loan. Many clients I’ve worked with have seen substantial savings by simply exploring refinancing options. It’s not just about getting a new loan; it’s about seizing an opportunity to improve your financial standing.

The refinancing process typically involves a few key steps:

- Check your credit score: A good score is crucial for better rates.

- Shop around: Don’t just go with your current lender; compare offers from multiple banks, credit unions, and online lenders.

- Gather documents: You’ll need your current loan information, proof of income, and vehicle details.

- Submit your application: The new lender will review your application and provide an offer.

- Finalize the new loan: If approved, the new loan pays off your old one, and you start making payments to your new lender.

Common mistakes to avoid when refinancing are extending the loan term too much, which can negate interest savings, and not thoroughly comparing all fees associated with the new loan. Always consider the total cost of the new loan, not just the monthly payment.

Accelerating Your Payoff: Strategies to Beat Your Loan

Beyond refinancing, actively working to pay off your car loan after purchase earlier than scheduled offers immense benefits. The sooner you eliminate that debt, the more interest you save, and the faster you achieve financial freedom. It’s a proactive approach that puts you in control.

Why pay off your car loan early? The most significant advantage is the substantial savings on interest charges. Every extra dollar you pay towards the principal reduces the amount of interest accrued over time. Furthermore, becoming debt-free sooner reduces your monthly financial obligations, freeing up funds for investments, savings, or other financial goals.

There are several effective methods to accelerate your payoff:

- Making Extra Payments: Even small, consistent extra payments can make a big difference. Consider paying half your monthly payment every two weeks (bi-weekly payments). This results in 13 full payments per year instead of 12, effectively shaving off a significant portion of your loan term.

- Round-Up Payments: If your payment is, say, $327, consider rounding it up to $350 or $375. The small additional amount directly attacks the principal.

- Lump Sum Payments: Utilize unexpected windfalls, such as tax refunds, work bonuses, or inheritance, to make a substantial lump-sum payment towards your principal. This can dramatically reduce the remaining balance and future interest.

- Applying Extra Income: If you pick up a side hustle or receive a raise, dedicate a portion of that new income specifically to your car loan.

Pro tip from us: Always double-check with your lender to ensure any extra payments are applied directly to the principal balance, not towards future payments. This ensures your efforts are truly accelerating your payoff. Also, be aware of any prepayment penalties. While less common on auto loans these days, some older or subprime loans might still have them. Always review your loan agreement carefully for such clauses.

For more insights on managing your finances to make extra payments, you might find our guide on Smart Budgeting for Car Owners particularly helpful.

Dealing with Financial Hurdles: When Life Throws a Curveball

Life is unpredictable, and sometimes, despite our best efforts, financial difficulties arise that make managing your car loan after purchase challenging. Losing a job, an unexpected medical emergency, or other unforeseen circumstances can make it difficult to meet your monthly payments. It’s crucial to know your options and act quickly.

Based on my experience, the worst thing you can do when facing financial hardship is to ignore the problem. Open and honest communication with your lender is absolutely key. Most lenders would rather work with you to find a solution than go through the costly and time-consuming process of repossession.

Here are potential options if you find yourself struggling:

- Contact Your Lender Immediately: Explain your situation. They may offer solutions such as:

- Payment Deferment: Temporarily pausing payments for a short period, with the understanding that payments will resume later, often with accumulated interest.

- Loan Modification: Adjusting the terms of your loan, such as lowering your interest rate or extending the loan term, to make payments more manageable. Be cautious with extending the term, as it can increase total interest paid.

- Understand Repossession Risks: If you consistently miss payments without communicating with your lender, they have the right to repossess your vehicle. This can severely damage your credit score and leave you without transportation.

- Selling the Car with an Outstanding Loan: If your financial situation is dire, selling the car might be an option. This is known as selling a car with a lien. You’ll need to pay off the outstanding loan balance with the proceeds from the sale. If the car’s value is less than what you owe (you’re "upside down" or have negative equity), you’ll need to pay the difference out of pocket.

Always assess the long-term implications of any solution. While deferment offers temporary relief, it often means higher payments or more interest later. A loan modification can provide stability, but ensure the new terms are genuinely sustainable.

Protecting Your Investment: Beyond the Loan

Managing your car loan after purchase isn’t solely about the payments; it’s also about protecting the asset that the loan is tied to. Your car is a significant investment, and its value directly impacts your financial security, especially if you ever need to sell it or if it gets totaled.

One critical consideration is Guaranteed Asset Protection (GAP) insurance. This coverage is highly recommended, especially if you made a small down payment or financed a rapidly depreciating vehicle. GAP insurance covers the difference between what you owe on your car loan and the car’s actual cash value (ACV) if it’s stolen or totaled. Without it, you could be left owing money on a car you no longer have.

Maintaining your vehicle properly is another non-negotiable aspect of protecting your investment. Regular oil changes, tire rotations, and scheduled maintenance not only ensure your car runs smoothly but also helps retain its resale value. A well-maintained car will fetch a better price if you decide to sell it, making it easier to cover any remaining loan balance.

Understanding depreciation is also key. Cars typically lose a significant portion of their value in the first few years. This depreciation curve means that in the early stages of your loan, you might owe more than the car is worth, a situation known as being "upside down" or having "negative equity." GAP insurance specifically addresses this risk.

Future-Proofing Your Finances: Long-Term Car Loan Wisdom

Effectively managing your current car loan after purchase is not just about the present; it’s about building a stronger financial future. The lessons learned and habits formed now will serve you well for years to come, impacting future vehicle purchases and overall financial health.

One of the most valuable outcomes of responsible loan management is building excellent credit. Every on-time payment contributes positively to your credit score, which is a powerful asset. A higher credit score translates into better interest rates on future loans—whether for a home, another car, or personal financing—saving you thousands over your lifetime.

Start saving for your next car now, even if it’s years away. By having a substantial down payment for your next vehicle, you can reduce the amount you need to finance, potentially secure a lower interest rate, and decrease your monthly payments. This proactive saving breaks the cycle of constantly being in significant car debt.

Finally, always consider the total cost of ownership, not just the purchase price and loan payments. Factor in insurance, maintenance, fuel, and potential repairs. A car might seem affordable on paper, but its ongoing costs can quickly add up. Understanding this holistic view helps you make smarter choices for future vehicle purchases. For more detailed information on understanding auto loan terms and your rights, refer to trusted external resources like the Consumer Financial Protection Bureau’s guide on auto loans: Consumer Financial Protection Bureau – Auto Loans.

If you’re looking to supercharge your financial standing, we also recommend exploring our guide on The Ultimate Guide to Improving Your Credit Score to unlock even more financial opportunities.

Conclusion: Take the Driver’s Seat of Your Car Loan

Driving off the lot with a new car is just the beginning of your financial journey. Managing your car loan after purchase is a continuous process that requires attention, strategy, and proactive decision-making. From understanding your initial agreement to exploring refinancing options, accelerating your payoff, and preparing for unforeseen challenges, every step you take contributes to your financial well-being.

By embracing these strategies – automating payments, diligently budgeting, exploring refinancing opportunities, and making extra payments when possible – you’re not just paying off a debt. You’re building financial discipline, saving money, and ultimately, gaining true financial freedom. Don’t let your car loan drive you; take the driver’s seat and steer your finances towards a brighter, more secure future. Your diligence today will pave the way for a smoother road ahead.