Navigating Your Car Loan Journey: A Deep Dive into Financing Through Huntington Bank

Navigating Your Car Loan Journey: A Deep Dive into Financing Through Huntington Bank Carloan.Guidemechanic.com

Securing the right car loan can feel like navigating a complex maze. With so many options available, finding a lender that aligns with your financial goals and offers competitive terms is paramount. Among the prominent financial institutions, Huntington Bank stands out as a significant player in the auto financing landscape. For many, a car loan through Huntington Bank represents a reliable pathway to owning their next vehicle, whether it’s a brand-new model or a quality used car.

This comprehensive guide is designed to be your ultimate resource. We’ll explore everything you need to know about obtaining a car loan through Huntington Bank, from understanding their offerings to navigating the application process and beyond. Our goal is to equip you with the knowledge to make informed decisions, ensuring a smooth and successful car buying experience. Let’s embark on this journey together to unlock the potential of Huntington Bank auto loan options.

Navigating Your Car Loan Journey: A Deep Dive into Financing Through Huntington Bank

Why Consider a Car Loan Through Huntington Bank?

When it comes to financing a major purchase like a car, trust and reliability are key. Huntington Bank has a long-standing history of serving communities, building a reputation for customer-centric banking and a diverse range of financial products. Their approach to auto lending often combines competitive rates with flexible terms, making them an attractive option for many car buyers.

Based on my experience in the financial sector, a key differentiator for established banks like Huntington is their commitment to customer support. They often provide accessible resources and personalized assistance, which can be invaluable, especially for first-time car loan applicants. This level of support can alleviate much of the stress associated with securing financing.

Furthermore, Huntington Bank understands that every borrower’s situation is unique. They typically offer tailored solutions rather than a one-size-fits-all approach. This flexibility can manifest in various loan terms, interest rate structures, and even options for those with less-than-perfect credit, albeit with potentially different conditions.

Understanding Huntington’s Auto Loan Offerings

Huntington Bank provides a range of auto loan products designed to meet diverse needs. Whether you’re eyeing a brand-new vehicle, a pre-owned gem, or looking to refinance an existing loan, Huntington likely has an option for you. It’s crucial to understand these offerings to determine which best suits your personal situation.

Their primary categories typically include new car loans, used car loans, and auto loan refinancing. Each category comes with its own set of considerations regarding eligibility, interest rates, and loan terms. Exploring these options in detail will help you prepare adequately for your application.

New Car Loans

For those dreaming of a brand-new vehicle straight from the dealership, Huntington Bank offers financing solutions specifically for new car purchases. These loans often come with attractive interest rates due to the lower perceived risk associated with new vehicles. Lenders generally view new cars as having a higher resale value and being less prone to immediate mechanical issues.

When considering a new car loan through Huntington, you can expect competitive terms and a straightforward application process. The bank aims to make the dream of a new car ownership a reality for its customers. This option is ideal if you prioritize the latest features, warranty coverage, and the peace of mind that comes with a vehicle fresh off the assembly line.

Used Car Loans

Purchasing a used car is a popular choice for many, offering significant savings and a wider selection. Huntington Bank understands this market and provides robust financing for pre-owned vehicles. While interest rates for used car loans might sometimes be slightly higher than new car loans, Huntington strives to keep them competitive.

The eligibility criteria for used car loans often consider the age and mileage of the vehicle. Lenders typically have limits on how old a car can be or how many miles it can have to qualify for financing. It’s wise to check these specifics with Huntington Bank directly before you fall in love with a particular used model.

Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Auto loan refinancing with Huntington Bank could be an excellent strategy. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can lead to lower monthly payments or a reduced total cost of the loan over time.

Pro tips from us: Refinancing makes sense if your credit score has significantly improved since you took out your original loan, if interest rates have dropped, or if you want to adjust your monthly payment. For example, extending your loan term could lower monthly payments, though it might increase the total interest paid. Conversely, shortening the term could save you interest, but your monthly payment would increase. Huntington can help you explore these possibilities.

The Pre-Approval Advantage with Huntington Bank

One of the smartest moves you can make before stepping onto a dealership lot is securing pre-approval for your car loan. A car loan through Huntington Bank offers a streamlined pre-approval process that provides immense benefits. It’s essentially a preliminary commitment from the bank, indicating how much they are willing to lend you, at what estimated interest rate, and under what terms.

Pre-approval transforms you from a mere shopper into a qualified buyer. It gives you significant leverage during negotiations with car dealerships. You walk in knowing your budget and your financing terms, allowing you to focus solely on the vehicle price, not the complexities of financing.

Based on my experience, having a pre-approval letter in hand saves a tremendous amount of time and stress. It eliminates the need to haggle over financing options at the dealership, which can often be less favorable than what you could secure independently. This approach ensures you maintain control over your car-buying journey.

How to Get Pre-Approved

The process for pre-approval with Huntington Bank is generally straightforward. You can often apply online, over the phone, or in person at a branch. You’ll need to provide some basic financial information, similar to a full loan application, but it’s a quicker, less committing process.

Typically, you’ll need to share details about your income, employment history, and current debts. Huntington Bank will then conduct a soft credit inquiry, which doesn’t negatively impact your credit score, to give you an estimate of your loan eligibility. Once pre-approved, you’ll receive an offer outlining the maximum loan amount and estimated interest rate.

Key Requirements for a Huntington Car Loan

To successfully secure a car loan through Huntington Bank, understanding the eligibility requirements is crucial. While specific criteria can vary slightly, there are common factors that all lenders, including Huntington, evaluate. Being prepared with this knowledge can significantly improve your chances of approval.

Common mistakes to avoid are applying without first checking your credit score or underestimating the importance of a stable income. Lenders assess your ability to repay the loan, and these factors are primary indicators of your financial health. A little preparation goes a long way in ensuring a smooth application process.

Credit Score and History

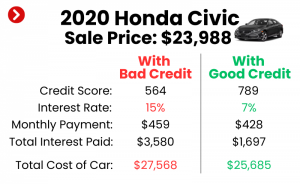

Your credit score is arguably the most critical factor in determining your loan eligibility and interest rate. Huntington Bank, like other lenders, uses your credit score to assess your creditworthiness. A higher credit score signals a lower risk to the lender, typically resulting in more favorable interest rates and loan terms.

While Huntington Bank does not publicly disclose a minimum credit score, generally, scores in the "good" to "excellent" range (typically 670 and above) will yield the best rates. Those with fair credit might still qualify but could face higher interest rates. It’s always a good idea to check your credit score before applying. For more insights into improving your credit score before applying, check out our guide on .

Income and Employment Stability

Lenders want to ensure you have a consistent and sufficient income to comfortably make your monthly car loan payments. Huntington Bank will review your employment history and current income to determine your repayment capacity. Stable employment for a reasonable period, typically six months to two years, is often preferred.

Proof of income, such as pay stubs, tax returns, or bank statements, will be required. The bank evaluates your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income to manage new debt, making you a more attractive borrower.

Debt-to-Income (DTI) Ratio

As mentioned, your DTI ratio is a critical metric. Huntington Bank will look at the percentage of your gross monthly income that goes towards debt payments, including mortgages, credit cards, and other loans. A DTI ratio below 36% is generally considered favorable, though some lenders may approve loans with a higher DTI, especially if you have a strong credit score.

A high DTI ratio can signal that you might be overextended financially, making it riskier to take on additional debt. Before applying, consider paying down some existing debts to improve this ratio if it’s on the higher side. This proactive step can significantly enhance your loan application.

Down Payment

While not always strictly required, making a down payment on your car loan can significantly improve your application and financial standing. A down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid over the life of the loan. It also shows the lender you have a vested interest in the vehicle.

Pro tips from us: Aim for at least 10% to 20% of the vehicle’s purchase price as a down payment if possible. This not only makes your loan more attractive to Huntington Bank but also helps you avoid being "upside down" on your loan, where you owe more than the car is worth, especially common with new cars due to immediate depreciation.

The Application Process, Step-by-Step

Applying for a car loan through Huntington Bank is designed to be a straightforward process, whether you prefer to apply online, over the phone, or in person. Knowing what to expect at each stage can help you prepare and move through the application efficiently.

Preparation is key. Gathering all necessary documents beforehand can prevent delays and make the experience much smoother. Huntington Bank values efficiency, and a well-prepared applicant helps them serve you better.

1. Gather Required Documents

Before you begin the application, ensure you have all necessary documentation readily available. This typically includes:

- Proof of Identity: Government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs (usually 2-3), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit check purposes.

- Vehicle Information (if already chosen): Make, model, year, VIN, mileage, and purchase price.

Having these documents organized will expedite your application significantly. It demonstrates your readiness and seriousness to Huntington Bank.

2. Choose Your Application Method

Huntington Bank offers flexibility in how you apply:

- Online Application: This is often the quickest and most convenient method. You can complete the application from the comfort of your home, typically receiving a decision within minutes or hours.

- Phone Application: You can speak with a loan officer who will guide you through the process, answer questions, and take your information over the phone.

- In-Branch Application: For those who prefer face-to-face interaction, visiting a local Huntington Bank branch allows you to discuss your options with a representative directly and complete the application with their assistance.

Common mistakes to avoid are rushing through the online form or not asking questions when applying in person or over the phone. Ensure all information is accurate and you understand every part of the application.

3. Review and Submit

Once you’ve filled out the application and provided all required documentation, carefully review everything for accuracy. Any discrepancies or errors could lead to delays or even rejection. After confirming all details, submit your application.

Huntington Bank will then process your application, which includes performing a hard credit inquiry. This inquiry will temporarily impact your credit score, typically by a few points. However, if you apply for multiple auto loans within a short period (usually 14-45 days), they are often treated as a single inquiry, minimizing the impact.

4. Receive a Decision

After submission, Huntington Bank will evaluate your application based on the information provided and your creditworthiness. You will typically receive a decision relatively quickly, especially with online applications. If approved, you’ll receive a loan offer detailing the approved amount, interest rate, and loan terms.

If your application is denied, Huntington Bank is required to provide you with the reasons for the denial. This information can be valuable for understanding areas you might need to improve for future applications. Don’t be discouraged; use it as a learning opportunity.

Interest Rates and Terms for Huntington Car Financing

Understanding the interest rates and terms associated with your car loan through Huntington Bank is crucial for managing your financial obligations effectively. These factors directly impact your monthly payments and the total cost of your loan over time.

Huntington Bank strives to offer competitive rates, but these rates are not universal. They are highly personalized, reflecting various aspects of your financial profile and the specifics of the loan. Knowing what influences these rates can help you secure the best possible deal.

Factors Influencing Your Interest Rate

Several key factors determine the interest rate you’ll receive from Huntington Bank:

- Credit Score: As mentioned, a higher credit score generally translates to a lower interest rate. It’s the primary indicator of your perceived risk as a borrower.

- Loan Term: Shorter loan terms (e.g., 36 or 48 months) often come with lower interest rates compared to longer terms (e.g., 60 or 72 months). While longer terms mean lower monthly payments, they usually result in higher total interest paid.

- Down Payment: A larger down payment reduces the loan amount and the bank’s risk, potentially leading to a lower interest rate.

- Vehicle Type: New cars often qualify for lower rates than used cars due to their lower depreciation risk and typically better condition.

- Market Conditions: Prevailing interest rates set by the Federal Reserve and the overall economic climate also play a role in the rates offered by lenders like Huntington Bank.

Pro tips from us: Always compare the Annual Percentage Rate (APR) from different lenders, not just the advertised interest rate. The APR includes both the interest rate and any fees associated with the loan, giving you a more accurate picture of the total cost.

Choosing the Right Loan Term

Selecting the appropriate loan term is a balancing act between affordable monthly payments and the total cost of the loan.

- Shorter Terms: Lower total interest paid, higher monthly payments. Ideal if you can comfortably afford the higher payments and want to pay off the loan quickly.

- Longer Terms: Lower monthly payments, higher total interest paid. Can be appealing if you need to keep monthly expenses low, but be mindful of the increased overall cost and the risk of being "upside down" on your loan for a longer period.

Based on my experience, it’s wise to choose the shortest loan term you can comfortably afford. This minimizes interest costs and gets you out of debt faster. If you’re unsure whether a new or used car is right for you, our article on can help.

Maximizing Your Approval Chances with Huntington Bank

Getting approved for a car loan through Huntington Bank isn’t just about meeting the minimum requirements; it’s about presenting yourself as the most creditworthy applicant possible. There are several proactive steps you can take to enhance your application and increase your chances of securing favorable terms.

Common mistakes to avoid are applying to multiple lenders simultaneously without understanding the impact on your credit, or not addressing any credit report errors before applying. A little strategic planning can make a big difference.

1. Improve Your Credit Score

This is perhaps the most impactful step. A higher credit score directly correlates with better loan offers.

- Pay Bills on Time: Payment history is the biggest factor in your credit score.

- Reduce Existing Debt: Lowering credit card balances improves your credit utilization ratio.

- Check for Errors: Review your credit report for any inaccuracies and dispute them immediately. You can get free copies of your credit report from AnnualCreditReport.com. (External Link to: https://www.annualcreditreport.com/index.action)

These actions demonstrate financial responsibility and make you a more attractive borrower to Huntington Bank.

2. Save for a Larger Down Payment

As discussed, a significant down payment reduces the loan amount, lowers the bank’s risk, and can lead to better interest rates. Even if you can only manage a slightly larger down payment, it shows commitment and can positively influence your approval.

Pro tips from us: Consider delaying your car purchase by a few months if it means you can save up an extra few hundred or thousand dollars for a down payment. The long-term savings in interest can be substantial.

3. Maintain Stable Employment

Lenders prefer to see consistent income and employment history. Avoid changing jobs right before applying for a loan, if possible. If you are starting a new job, having a clear offer letter and demonstrating a strong career path can sometimes mitigate concerns.

Huntington Bank assesses your ability to repay. A stable employment history provides confidence in your ongoing income stream.

4. Be Realistic About Your Budget

Don’t overextend yourself. Apply for a loan amount that you can realistically afford based on your income and existing debts. Over-applying for a larger loan than you need or can manage can raise red flags with Huntington Bank.

It’s important to factor in not just the monthly loan payment, but also insurance, maintenance, fuel, and registration costs when calculating your true car ownership budget.

Refinancing Your Existing Car Loan with Huntington Bank

Even if you already have a car loan, Huntington Bank might offer a solution to improve your financial situation through refinancing. Refinancing can be a smart move if market conditions have changed, your credit score has improved, or you simply want more favorable terms.

Many people don’t realize the potential savings refinancing can offer. It’s not just for those struggling with payments; it’s also for those looking to optimize their financial strategy. Huntington Bank provides clear guidance on their refinancing options.

When to Consider Refinancing

- Improved Credit Score: If your credit score has significantly increased since you took out your original loan, you’re likely eligible for a lower interest rate.

- Lower Interest Rates: General market interest rates may have dropped, making it a good time to secure a more favorable rate.

- Lower Monthly Payments: You might want to extend your loan term to reduce your monthly payment, freeing up cash flow (though this may increase total interest paid).

- Shorter Loan Term: Conversely, if your financial situation has improved, you might want to shorten your loan term to pay it off faster and save on interest.

- Remove a Co-signer: If you initially needed a co-signer but now have strong credit, refinancing can allow you to take sole responsibility for the loan.

The process for refinancing with Huntington Bank is very similar to applying for a new car loan, involving an application, credit check, and review of your current loan details.

Post-Approval: What Happens Next?

Congratulations, your car loan through Huntington Bank has been approved! This is an exciting step, but it’s important to understand the final stages of the process and your ongoing responsibilities. Knowing what to expect post-approval ensures a smooth transition to car ownership.

The documentation phase is critical, and understanding your loan agreement is paramount. Don’t hesitate to ask questions if anything is unclear.

1. Review and Sign Loan Documents

Carefully read all loan documents provided by Huntington Bank. Pay close attention to:

- Interest Rate (APR): Confirm it matches the offer.

- Loan Term: Ensure the duration is as agreed upon.

- Monthly Payment: Verify the exact amount.

- Total Amount Financed: Understand the total principal and interest you will pay.

- Any Fees: Look for origination fees, late payment fees, or prepayment penalties (though prepayment penalties are rare on auto loans).

Once you’re satisfied with all terms, sign the documents. This legally binds you to the loan agreement.

2. Vehicle Purchase and Funding

With the loan documents signed, Huntington Bank will typically disburse the funds directly to the car dealership if you’re purchasing a new vehicle. If you’re refinancing, the funds will be used to pay off your existing loan with the previous lender.

Ensure that all titles and registration documents are correctly processed, naming Huntington Bank as the lienholder until the loan is fully paid off.

3. Setting Up Payments

Huntington Bank offers various convenient ways to make your monthly loan payments:

- Online Banking: Set up automatic payments from your Huntington checking or savings account, or from an external bank account. This is often the easiest way to ensure on-time payments.

- Mobile App: Manage payments on the go through Huntington’s mobile banking app.

- Phone: Make payments over the phone.

- Mail: Send checks via mail.

- In-Branch: Make payments at any Huntington Bank branch location.

Pro tips from us: Always set up automatic payments if possible. This minimizes the risk of late payments, which can incur fees and negatively impact your credit score.

Common Questions About Huntington Car Loans

To further enhance your understanding, let’s address some frequently asked questions regarding car loans through Huntington Bank.

Can I get a car loan with bad credit through Huntington Bank?

While Huntington Bank primarily looks for good to excellent credit, they do consider a range of credit profiles. If you have less-than-perfect credit, you might still qualify, but expect potentially higher interest rates or the requirement for a larger down payment or a co-signer. It’s always best to apply or speak with a loan officer to understand your specific options.

Does Huntington Bank offer loans for private party car sales?

Huntington Bank typically offers financing for vehicles purchased from licensed dealerships. However, policies can change, and specific situations might be considered. It’s crucial to contact Huntington Bank directly to inquire about financing options for private party sales, as the requirements and process might differ significantly.

What is the maximum loan term for a Huntington car loan?

Loan terms can vary, but generally, auto loans can extend up to 72 or even 84 months, especially for new vehicles or larger loan amounts. Shorter terms like 36 or 48 months are also common. The best term for you depends on your financial situation and preferences for monthly payment vs. total interest paid.

Can I pay off my Huntington car loan early?

Most auto loans from reputable lenders, including Huntington Bank, do not have prepayment penalties. This means you can pay off your loan early without incurring extra fees, potentially saving you a significant amount in interest. Always confirm this detail in your loan agreement.

How long does it take to get approved for a Huntington car loan?

Many online applications for pre-approval or direct loan applications can receive an instant decision or a decision within a few hours. In some cases, if additional information or review is needed, it might take a business day or two. Applying in person can also provide quick feedback.

Conclusion: Your Road to Car Ownership with Huntington Bank

Navigating the world of car loans can seem daunting, but with the right knowledge and a trusted partner, it becomes a straightforward path to achieving your automotive goals. A car loan through Huntington Bank offers a compelling option for many, combining competitive rates, flexible terms, and a commitment to customer service that can make your car buying journey smoother and more confident.

From understanding their diverse loan offerings for new and used cars to leveraging the power of pre-approval and preparing for a robust application, this guide has provided an in-depth look at what it takes to secure financing with Huntington. Remember the importance of a strong credit profile, a healthy debt-to-income ratio, and a well-researched approach.

Whether you’re purchasing your dream car or looking to refinance for better terms, Huntington Bank provides the resources and support to help you make informed decisions. By following the advice outlined here, you’re not just getting a loan; you’re building a foundation for responsible car ownership. Drive forward with confidence, knowing you’ve made a well-informed choice for your auto financing needs.