Navigating Your Car Loan Journey with Navy Federal: A Comprehensive Guide to Smart Auto Financing

Navigating Your Car Loan Journey with Navy Federal: A Comprehensive Guide to Smart Auto Financing Carloan.Guidemechanic.com

Buying a car is a significant life event, often marked by excitement and a touch of apprehension. For many, securing the right financing is as crucial as choosing the perfect vehicle. If you’re a member of the military community or have ties to it, you’ve likely heard of Navy Federal Credit Union. Known for its member-centric approach and competitive offerings, Navy Federal stands out as a top choice for auto loans.

This in-depth guide is designed to be your ultimate resource for understanding how to secure a car loan with Navy Federal. We’ll explore everything from eligibility and application processes to maximizing your approval chances and ensuring you get the best possible rates. Our goal is to provide you with the knowledge and confidence needed to navigate your auto financing journey successfully, making your car-buying experience smooth and rewarding.

Navigating Your Car Loan Journey with Navy Federal: A Comprehensive Guide to Smart Auto Financing

Why Choose Navy Federal for Your Car Loan? Unpacking the Member Advantage

When it comes to auto financing, the market is saturated with options. However, for those eligible, a Navy Federal car loan often presents a compelling proposition. Their unique position as a credit union serving a specific community allows them to offer distinct advantages that traditional banks might not.

One of the primary draws is their commitment to competitive auto loan rates. Navy Federal consistently strives to offer rates that are often lower than national averages, directly translating into significant savings over the life of your loan. These favorable rates are a direct benefit of their credit union structure, where profits are returned to members in the form of better rates and lower fees.

Beyond just the numbers, members often praise the flexible loan terms available. Whether you’re looking for a shorter term to pay off your vehicle quicker or a longer term to reduce monthly payments, Navy Federal provides a range of options designed to fit various financial situations. This flexibility ensures you can tailor your car loan to your specific budget and financial goals.

Exceptional member service is another hallmark of Navy Federal. Unlike larger, impersonal financial institutions, Navy Federal prides itself on personalized support. From the initial inquiry to the final signing, their team is often lauded for being knowledgeable, helpful, and genuinely invested in helping you achieve your financial objectives. This level of service can make a significant difference in what can sometimes be a complex process.

Finally, the exclusive benefits for military members truly set Navy Federal apart. As an institution founded to serve the armed forces, they understand the unique challenges and needs of military personnel and their families. This understanding often translates into tailored products, special discounts, and a deep appreciation for their service, which is reflected in their loan offerings. Based on my experience, this focus on the military community creates a sense of trust and reliability that is hard to find elsewhere.

Unlocking the Door: Understanding Navy Federal Membership Eligibility

Before you can even consider a Navy Federal Credit Union auto loan, the first and most crucial step is to become a member. Navy Federal is a credit union, meaning it’s owned by its members and operates on a principle of "people helping people." This structure limits membership to a specific field of membership.

Who can join Navy Federal? Eligibility primarily extends to individuals who have served or are currently serving in the U.S. Armed Forces. This includes the Army, Marine Corps, Navy, Air Force, Coast Guard, and Space Force. Furthermore, membership is open to all Department of Defense (DoD) civilian personnel, including retirees and annuitants.

Crucially, family members of eligible individuals also qualify for membership. This includes parents, grandparents, spouses, siblings, children (including adopted and stepchildren), and grandchildren. This broad eligibility ensures that the benefits of Navy Federal can extend across generations within military and DoD families. If your parent or grandparent was a member, or even if your sibling is, you might be eligible!

How to join Navy Federal is a straightforward process. You can apply online, over the phone, or in person at one of their branches. You’ll need to provide some personal information and details confirming your eligibility. Once your membership is established, you gain access to all of Navy Federal’s products and services, including their highly sought-after car loans. Becoming a member is not just a formality; it’s the gateway to a financial institution dedicated to serving your specific community.

The Navy Federal Car Loan Application Process: A Step-by-Step Guide

Applying for a car loan with Navy Federal is a streamlined process designed to be as efficient as possible for their members. Understanding each step can help you prepare thoroughly and increase your chances of a smooth approval. Let’s break it down.

Step 1: Get Pre-Approved for Your Car Loan

This is arguably the most critical initial step in your car-buying journey. Getting pre-approved for a Navy Federal car loan means that Navy Federal has reviewed your financial information and determined how much they are willing to lend you, along with an estimated interest rate. This pre-approval gives you immense power and confidence when you walk into a dealership.

Pro Tip from us: Always get pre-approved before you start serious car shopping. It transforms you from a regular shopper into a cash buyer in the eyes of the dealership. This leverage allows you to negotiate the car’s price more effectively, separate from the financing discussion, potentially saving you thousands. Pre-approval also helps you set a realistic budget, preventing you from falling in love with a car you can’t truly afford.

Step 2: Gather Your Essential Documents

Preparation is key to a swift application process. While Navy Federal aims for efficiency, having all your paperwork ready beforehand will prevent delays. Typically, you’ll need:

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport.

- Proof of Income: Recent pay stubs, W-2 forms, or tax returns if you’re self-employed. This helps Navy Federal assess your ability to repay the loan.

- Proof of Residence: Utility bills or a lease agreement can confirm your address.

- Vehicle Information (if applicable): If you’ve already found a car, they’ll need details like the VIN, make, model, and mileage. For new cars, a buyer’s order might be requested.

Having these documents organized and readily accessible will make the application submission much faster and smoother.

Step 3: Submit Your Car Loan Application

With your documents in hand and a clear idea of your needs, you can submit your Navy Federal car loan application. You have several convenient options:

- Online: The easiest and most common method. Navy Federal’s website has a dedicated section for auto loans where you can complete the application from the comfort of your home.

- By Phone: You can call their member service representatives, who will guide you through the application process.

- In Person: Visit a local Navy Federal branch if you prefer face-to-face assistance and have questions that require detailed explanations.

Whichever method you choose, be prepared to answer questions about your financial history, employment, and the specifics of the vehicle you intend to purchase.

Step 4: Understand the Decision on Your Auto Loan

Once you’ve submitted your application, Navy Federal will review it. This typically involves a credit check and an assessment of your financial stability. The decision usually comes relatively quickly, often within minutes for online applications, or within a business day or two for more complex cases.

- Approval: Congratulations! You’ll receive details about your approved loan amount, interest rate, and terms.

- Conditional Approval: Sometimes, Navy Federal might approve your loan with certain conditions, such as requiring a larger down payment or a co-signer.

- Denial: If your application is denied, Navy Federal will provide a reason. This is an opportunity to understand what factors led to the denial and to work on improving them for a future application. Common reasons include a low credit score or high debt-to-income ratio.

Step 5: Finalize Your Navy Federal Car Loan

Upon approval, the final step involves signing the loan documents. This is where you officially agree to the terms and conditions of your Navy Federal auto loan. Make sure you carefully read through everything, including the interest rate, loan term, monthly payment amount, and any associated fees.

If you are buying from a dealership, Navy Federal can often work directly with them to facilitate the payment. If you’re buying privately, they will guide you on how to transfer funds to the seller. Once all the paperwork is complete and signed, the funds are disbursed, and you can drive off in your new (or new-to-you) vehicle!

Key Factors Influencing Your Navy Federal Car Loan Approval & Rates

Securing the best possible terms for your car loan with Navy Federal hinges on several critical financial factors. Understanding these elements can empower you to prepare effectively and increase your chances of approval at favorable rates.

Your Credit Score: The Foundation of Your Loan

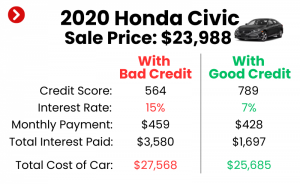

Your credit score is arguably the single most important factor Navy Federal (and any lender) considers. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repaying debt. A higher credit score signals lower risk to lenders.

Why it matters: A strong credit score, typically in the good to excellent range (e.g., FICO scores above 670), can unlock the lowest auto loan rates and most flexible terms. Conversely, a lower score may lead to higher interest rates or even loan denial. Common mistakes to avoid are not checking your credit score before applying. This can lead to surprises and missed opportunities to address inaccuracies or improve your score.

Your Debt-to-Income (DTI) Ratio: A Measure of Affordability

Your DTI ratio is a percentage that compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (credit card minimums, student loans, mortgage, etc.) is $1,000 and your gross monthly income is $3,000, your DTI is 33%.

Why it matters: Navy Federal uses your DTI to assess your ability to take on additional debt, like a car loan, without becoming financially overextended. A lower DTI ratio indicates that you have more disposable income to cover your new car payments, making you a less risky borrower. Most lenders prefer a DTI ratio below 43%, though lower is always better.

Loan-to-Value (LTV) Ratio: Vehicle Value vs. Loan Amount

The LTV ratio compares the amount you want to borrow for the car to the car’s actual market value. If a car is valued at $20,000 and you want to borrow $20,000, your LTV is 100%. If you make a $2,000 down payment, borrowing $18,000, your LTV is 90%.

Why it matters: A lower LTV ratio, often achieved through a significant down payment, reduces Navy Federal’s risk because it means you have more equity in the vehicle from the start. This can often translate into better car loan rates, especially for used cars where depreciation is a faster concern. For used car loans, a lower LTV is particularly beneficial as it mitigates the lender’s risk associated with the vehicle’s age and potential wear.

Loan Term: The Length of Your Repayment Period

The loan term refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months).

Why it matters: A shorter loan term generally means higher monthly payments but significantly less total interest paid over the life of the loan. A longer term leads to lower monthly payments, making the car more "affordable" on a month-to-month basis, but you’ll pay more in total interest. Navy Federal offers flexible terms, but choosing wisely based on your budget and financial goals is crucial.

Vehicle Type and Age: Impact on Risk Assessment

The type of vehicle you intend to purchase, particularly its age and mileage, can also influence your loan approval and interest rate.

Why it matters: New cars generally come with lower auto loan rates because they have a higher resale value and are less prone to immediate mechanical issues. Used cars, while often more budget-friendly upfront, might come with slightly higher rates due to increased risk of depreciation and potential maintenance costs. Navy Federal assesses these risks when determining your loan terms, offering competitive rates for both, but often distinguishing between them.

New Car vs. Used Car Loan with Navy Federal: What You Need to Know

Whether you’re eyeing a brand-new vehicle or a reliable pre-owned one, Navy Federal offers financing options tailored to both. Understanding the subtle differences between a new car loan and a used car loan with Navy Federal is essential for making an informed decision.

For new car loans, Navy Federal typically offers their most competitive interest rates. This is because new vehicles generally represent a lower risk to the lender. They come with manufacturer warranties, have no prior accident history, and their value depreciates more predictably initially. The terms for new car loans can also be quite flexible, often extending to longer periods like 72 or even 84 months for qualified buyers, though shorter terms are always advised to save on interest.

On the other hand, used car loans with Navy Federal are also very competitive but might come with slightly higher rates than new car loans. The risk assessment for used vehicles considers factors like the car’s age, mileage, and condition. Older cars or those with very high mileage might have more stringent requirements or slightly higher rates due to the increased potential for mechanical issues and faster depreciation. Navy Federal often has specific maximum age or mileage limits for used vehicles they will finance, so it’s wise to check these parameters before you fall in love with a specific pre-owned car.

Regardless of whether you choose new or used, getting pre-approved by Navy Federal is equally important. This step ensures you know your budget and interest rate before stepping onto a dealership lot, giving you the upper hand in negotiations for either a brand-new model or a carefully selected used vehicle.

Refinancing Your Existing Car Loan with Navy Federal

Perhaps you already have a car loan but are looking for a better deal. Refinancing your car loan with Navy Federal can be a smart financial move, potentially saving you a substantial amount of money over the life of your loan.

When to consider refinancing:

- Lower Interest Rates: If interest rates have dropped since you originally financed your car, or if your credit score has significantly improved, you might qualify for a lower rate with Navy Federal.

- Lower Monthly Payments: Refinancing to a longer term can reduce your monthly payment, freeing up cash flow. Be mindful that a longer term might mean paying more interest overall.

- Get Out of a Bad Loan: If you have an unfavorable loan from a dealership or another lender with high rates, Navy Federal’s competitive rates could provide significant relief.

The refinancing process with Navy Federal is similar to applying for a new loan. You’ll submit an application, they’ll review your credit and financial situation, and if approved, they’ll pay off your old loan. Your new loan will then be with Navy Federal under new, hopefully more favorable, terms. It’s a straightforward way to optimize your existing auto debt.

Pro Tips for Securing the Best Navy Federal Car Loan

Based on my experience in the auto financing landscape, there are several strategic moves you can make to ensure you secure the most advantageous car loan with Navy Federal. These tips go beyond the basics and delve into proactive steps for maximizing your financial position.

- Prioritize Improving Your Credit Score: Before you even think about applying, dedicate time to boost your credit score. Pay down existing debts, make all payments on time, and avoid opening new credit lines. Even a small increase in your score can translate into significantly lower auto loan rates from Navy Federal.

- Reduce Your Debt-to-Income Ratio: Actively work to lower your DTI. This means paying down credit card balances or other personal loans. A lower DTI shows Navy Federal that you have ample capacity to take on a new car payment without financial strain.

- Save for a Substantial Down Payment: While Navy Federal offers financing options with little to no down payment for qualified members, making a larger down payment is always beneficial. It reduces the loan amount, lowers your monthly payments, decreases your LTV, and often helps secure a better interest rate.

- Shop Around (Even Within Navy Federal’s Offerings): While Navy Federal offers excellent rates, it’s wise to compare their current offers with others, even if you ultimately choose them. Also, understand that rates can vary based on loan term and vehicle type, so explore all their options for car financing.

- Understand All Terms Before Signing: Never rush the paperwork. Carefully review the interest rate, APR, loan term, total cost of the loan, and any fees. If anything is unclear, ask questions until you fully understand every detail of your Navy Federal auto loan. This due diligence prevents future surprises.

Common Mistakes to Avoid When Applying for a Car Loan

Navigating the car loan process can be tricky, and certain missteps can cost you time, money, and even approval. Here are some common mistakes to avoid, drawing from frequently observed pitfalls:

- Not Getting Pre-Approved: As mentioned earlier, failing to get pre-approved by Navy Federal before visiting a dealership puts you at a significant disadvantage. You lose negotiation power and might settle for less favorable dealer financing out of convenience.

- Focusing Only on Monthly Payments: Many buyers make the mistake of fixating solely on the monthly payment amount. While important, it doesn’t tell the whole story. A low monthly payment might mean a longer loan term and a much higher total cost due to increased interest. Always consider the total amount you’ll pay over the life of the loan.

- Ignoring Your Credit Report: Not checking your credit report for errors or inaccuracies before applying is a major oversight. Even small mistakes can negatively impact your credit score and, consequently, your Navy Federal car loan rate. Get a free copy of your credit report annually and dispute any errors.

- Applying for Too Many Loans at Once: Each loan application can result in a "hard inquiry" on your credit report, which can temporarily ding your credit score. Applying to multiple lenders within a short period for the same type of loan is usually grouped as one inquiry by credit scoring models, but spreading out applications unnecessarily can be detrimental. Stick to a few well-researched options like Navy Federal.

Beyond the Loan: Navy Federal Resources & Support

Securing a car loan with Navy Federal is just one aspect of their comprehensive financial support for members. Their commitment extends beyond just lending, providing valuable resources that can further empower your financial journey.

Navy Federal offers a wealth of financial education materials and tools. These resources can help you budget for your car, understand the nuances of interest rates, and plan for future financial goals. Their aim is to equip members with the knowledge to make smart financial decisions, not just for a car loan, but for overall financial well-being.

Furthermore, their dedicated member support is always available to answer questions and provide guidance. Whether you need clarity on your loan terms, assistance with online banking, or advice on other financial products, their representatives are known for their helpfulness and expertise. This personalized support can be incredibly valuable during what can sometimes feel like a complex process.

Many members also benefit from Navy Federal’s potential partnerships or services designed to enhance the car-buying experience, such as car buying services. While specific offerings can vary, these services aim to streamline the vehicle search and negotiation process, often providing members with pre-negotiated pricing and a smoother transaction. Always check their official website for the most current information on these valuable member benefits.

Internal & External Resources for Your Journey

For even more in-depth insights into managing your finances and optimizing your auto loan experience, we recommend exploring these resources:

- For a detailed guide on improving your financial standing, especially your credit score, check out our comprehensive article on Boosting Your Credit Score for Auto Loans.

- If you’re still weighing different financing options and want to understand the various forms of auto loans available, our article on Understanding Different Auto Loan Types offers valuable perspectives.

For the most official and up-to-date information on Navy Federal Credit Union auto loan rates, terms, and eligibility, we highly recommend visiting their official website directly. This ensures you receive accurate and current details specific to their offerings: Visit Navy Federal’s Official Auto Loan Page

Conclusion: Drive Forward with Confidence with Navy Federal

Embarking on the journey to purchase a new vehicle is an exciting prospect, and securing the right financing can make all the difference. As we’ve explored, a car loan with Navy Federal offers a compelling package of competitive rates, flexible terms, and exceptional member service, all rooted in a deep understanding and commitment to the military community and their families.

By understanding the membership requirements, meticulously preparing for the application process, and being aware of the key factors that influence your loan terms, you are well-positioned to secure a favorable Navy Federal auto loan. Remember to prioritize your credit health, manage your debt, and always get pre-approved to gain significant leverage in your car-buying negotiations.

With the insights provided in this comprehensive guide, you can approach your car financing with confidence and clarity. Navy Federal is more than just a lender; it’s a financial partner dedicated to helping its members achieve their goals. So, take the wheel, make informed decisions, and drive off into your future with the peace of mind that comes from a smart car loan with Navy Federal.