Navigating Your Dream Car Purchase: A Deep Dive into the SchoolsFirst Car Loan Calculator

Navigating Your Dream Car Purchase: A Deep Dive into the SchoolsFirst Car Loan Calculator Carloan.Guidemechanic.com

The excitement of buying a new car is undeniable. Whether it’s the sleek lines of a brand-new sedan, the rugged capability of an SUV, or the eco-friendly appeal of an electric vehicle, the thought of hitting the open road in your ideal ride is thrilling. However, beyond the initial excitement lies a crucial financial decision: how will you finance it? This is where the SchoolsFirst Car Loan Calculator becomes an indispensable tool, transforming a potentially complex process into a clear, manageable journey.

Securing the right auto loan is about much more than just finding a car you like. It’s about understanding the financial commitment, ensuring it aligns with your budget, and ultimately, making a choice that brings peace of mind rather than financial strain. As an expert blogger and professional SEO content writer, I understand the importance of making informed decisions, especially when it comes to significant purchases like a vehicle. This comprehensive guide will meticulously walk you through every aspect of the SchoolsFirst Car Loan Calculator, empowering you with the knowledge to make smart, strategic choices for your next auto loan.

Navigating Your Dream Car Purchase: A Deep Dive into the SchoolsFirst Car Loan Calculator

Why Smart Car Financing Matters for Your Financial Health

Buying a car is one of the most significant financial commitments many individuals make, often second only to purchasing a home. A car loan can impact your monthly budget for several years, influencing everything from your ability to save to your capacity to handle unexpected expenses. Without proper planning, a seemingly affordable monthly payment can quickly become a burden, leading to financial stress and even impacting your credit score.

Many people fall into the trap of focusing solely on the monthly payment without considering the total cost of the loan over its entire term. This short-sighted approach can result in paying significantly more in interest than necessary, essentially overspending on your vehicle. Smart car financing, on the other hand, involves a holistic understanding of all the variables at play – the purchase price, interest rates, loan terms, and additional costs – ensuring your car purchase is a sound financial decision.

The goal isn’t just to get approved for a loan; it’s to secure the best loan for your specific financial situation. This means finding a balance between an affordable monthly payment and minimizing the total interest paid over the life of the loan. A powerful tool like the SchoolsFirst Car Loan Calculator is your first line of defense in achieving this balance, offering clarity and control before you even step foot in a dealership.

Understanding the SchoolsFirst Car Loan Calculator: Your Financial Co-Pilot

At its core, the SchoolsFirst Car Loan Calculator is an online interactive tool designed to help prospective car buyers estimate their potential monthly loan payments. It takes various financial inputs and quickly provides an estimated payment, allowing you to budget effectively and understand the implications of different financing scenarios. But it’s more than just a simple calculator; it’s a strategic planning instrument.

What makes the SchoolsFirst calculator particularly valuable is its ability to offer insights specific to a trusted financial institution known for its member-centric approach. SchoolsFirst Credit Union, with its long-standing reputation for serving the educational community, often provides competitive rates and favorable terms. Utilizing their specific calculator helps you get a more realistic picture of what you might expect from them, rather than relying on generic estimates from a random online tool. It serves as your personal financial co-pilot, guiding you through the often-complex landscape of auto financing before you commit.

This calculator empowers you to run various scenarios, adjust different parameters, and see the immediate impact on your estimated monthly payment and total loan cost. This foresight is invaluable, allowing you to fine-tune your expectations and negotiate with confidence, knowing exactly what you can comfortably afford. It’s a proactive step towards financial literacy and a smart car purchase.

Key Components of the SchoolsFirst Car Loan Calculator

To effectively use any car loan calculator, you must understand the individual variables that influence the outcome. The SchoolsFirst Car Loan Calculator, like most robust tools, requires specific pieces of information to provide an accurate estimate. Let’s break down each crucial component in detail.

1. The Purchase Price / Loan Amount

This is arguably the most straightforward input: the total price of the vehicle you intend to buy. However, it’s not always just the sticker price. The "loan amount" is the portion of the purchase price you actually need to borrow after any down payment or trade-in value has been applied.

It’s vital to remember that the purchase price is often negotiable with the dealership. Doing your research on fair market value for the specific make and model you’re interested in can give you significant leverage. A lower purchase price directly translates to a smaller loan amount, which in turn reduces your monthly payments and the total interest you’ll pay over the loan term. Always aim to negotiate the best possible price for the vehicle itself before even discussing financing options.

2. The Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay upfront towards the purchase of your vehicle, reducing the total amount you need to borrow. This is a critical factor in determining your monthly payments and the overall cost of your loan.

Based on my experience, a substantial down payment is one of the most effective strategies for securing a favorable auto loan. Not only does it lower your monthly payment, but it also reduces the principal amount on which interest accrues, leading to significant savings over the life of the loan. Lenders also view borrowers who make larger down payments as less risky, which can sometimes translate into better interest rates. Aim for at least 10-20% of the vehicle’s purchase price if possible.

3. Trade-in Value: Leveraging Your Current Vehicle

If you’re replacing an existing vehicle, its trade-in value can act similarly to a down payment. When you trade in your old car, the dealership applies its value directly towards the purchase of your new one, effectively reducing the amount you need to finance.

To maximize your trade-in value, do your homework beforehand. Use online valuation tools like Kelley Blue Book (KBB) or Edmunds to get an estimated value for your vehicle based on its condition, mileage, and features. Having this information empowers you during negotiations and ensures you get a fair price for your trade. Sometimes, selling your old car privately might yield a higher return, but the convenience of a trade-in can be appealing.

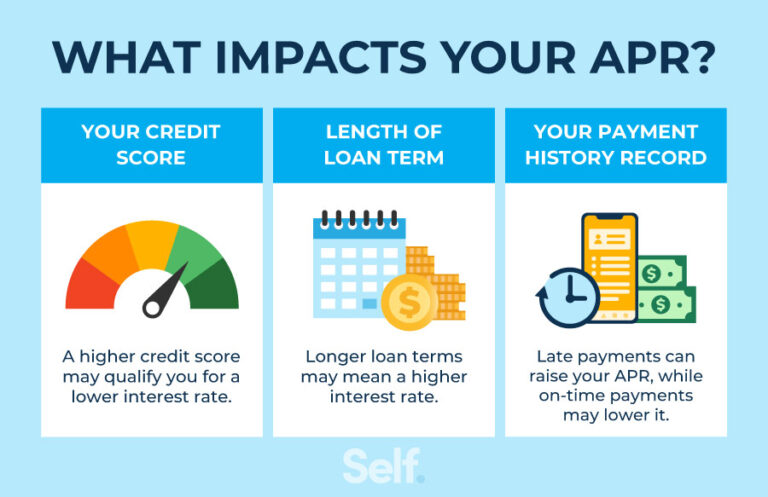

4. The Interest Rate: The Cost of Borrowing

The interest rate is arguably the most impactful variable in your car loan calculation. Expressed as a percentage, it’s the cost you pay to borrow the money. A lower interest rate means less money paid back to the lender over time, translating into lower monthly payments and significant savings.

Your credit score is the primary determinant of the interest rate you’ll be offered. Borrowers with excellent credit scores (typically 700+) usually qualify for the lowest rates, while those with lower scores will face higher rates to offset the perceived risk to the lender. Pro tips from us: Check your credit score before applying for any loan. Rectify any errors on your credit report and try to improve your score by paying bills on time and reducing other debts. Even a small reduction in your interest rate can save you hundreds, if not thousands, of dollars over the loan term.

5. Loan Term (Duration): Balancing Monthly Payments and Total Cost

The loan term, or duration, is the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). This factor directly impacts your monthly payment and the total interest you will pay.

A longer loan term will result in lower monthly payments, making the car seem more affordable on a month-to-month basis. However, this convenience comes at a cost: you’ll pay significantly more in total interest over the life of the loan. Conversely, a shorter loan term means higher monthly payments, but you’ll pay less interest overall and own your car outright sooner. Common mistakes to avoid are stretching out the loan term simply to achieve the lowest possible monthly payment without considering the long-term financial implications. Always balance affordability with the total cost of the loan.

6. Sales Tax, Fees, and Other Costs: Don’t Forget the Extras

Beyond the vehicle’s price, several additional costs contribute to the total amount you finance or pay upfront. These include:

- Sales Tax: Varies by state and locality, often a percentage of the vehicle’s purchase price.

- Registration and Licensing Fees: Required to legally operate your vehicle.

- Documentation Fees (Doc Fees): Charged by dealerships for processing paperwork.

- Extended Warranties or Add-ons: Often offered at the point of sale, these can significantly increase your loan amount if financed.

It’s crucial to factor these into your overall budget. While some of these fees might be paid out of pocket, many are often rolled into the total loan amount, increasing your principal and, consequently, your interest payments. Always ask for a detailed breakdown of all fees before signing any agreements.

Step-by-Step: How to Effectively Use the SchoolsFirst Car Loan Calculator

Using the SchoolsFirst Car Loan Calculator is straightforward, but understanding how to interpret its results and leverage its power is key. Here’s a practical guide:

-

Gather Your Information: Before you start, have a good estimate of your desired car’s purchase price, your available down payment, and any potential trade-in value. You might also want to have an idea of your credit score, as this will influence the interest rate you input.

-

Access the Calculator: Navigate to the SchoolsFirst Credit Union website and locate their auto loan calculator. (I will include a placeholder for an external link to their actual calculator page here: SchoolsFirst Auto Loan Calculator).

-

Input the Purchase Price: Enter the estimated negotiated price of the car you are considering.

-

Enter Your Down Payment: Input the amount you plan to pay upfront. If you have a trade-in, add its value to your cash down payment here.

-

Select Your Desired Loan Term: Choose a loan duration, starting with one you think is reasonable (e.g., 60 months).

-

Estimate the Interest Rate: This is where knowing your credit score helps. If you don’t have a specific rate from SchoolsFirst yet, use a realistic estimate based on current market rates for someone with your credit profile. You can often find average rates for different credit tiers online.

-

Calculate! Click the "Calculate" or "Submit" button to get your estimated monthly payment.

-

Interpret the Results: The calculator will display your estimated monthly payment. It might also show the total interest you’ll pay over the loan term and the total cost of the vehicle (purchase price + total interest).

-

Run Scenarios: This is where the real power lies.

- Adjust the Down Payment: See how increasing your down payment by a few hundred or thousand dollars impacts your monthly payment and total interest.

- Change the Loan Term: Compare a 60-month loan to a 72-month or even a 48-month loan. Notice how the monthly payment changes, but more importantly, observe the significant difference in total interest paid.

- Vary the Interest Rate: If you’re unsure about the exact rate you’ll qualify for, test a few different rates (e.g., your estimated rate, plus 0.5% and minus 0.5%) to understand the range of potential payments.

By running multiple scenarios, you gain a clear understanding of the financial levers at your disposal and can pinpoint the sweet spot that aligns with both your budget and your long-term financial goals.

Beyond the Calculator: Strategic Car Loan Planning

While the SchoolsFirst Car Loan Calculator is a phenomenal tool, it’s just one piece of a larger puzzle. Comprehensive financial planning for a car purchase involves several other strategic considerations.

Budgeting for Your New Ride

Before you even start looking at cars, integrate a potential car payment into your overall household budget. Don’t just consider the monthly loan payment; factor in insurance, fuel, maintenance, and potential repair costs. A good rule of thumb is that your total car-related expenses (payment, insurance, fuel, maintenance) shouldn’t exceed 10-15% of your net monthly income. Using a tool like our Budgeting for Success: Your Guide to Financial Freedom (internal link placeholder) can help you allocate funds effectively.

Credit Score: Your Golden Ticket

As mentioned earlier, your credit score is paramount. A higher score unlocks lower interest rates, saving you substantial money. Aim for a score of 700 or above for the most competitive offers. If your score isn’t where you want it to be, take steps to improve it before applying for a loan: pay all bills on time, reduce credit card balances, and avoid opening new lines of credit just before applying.

The Power of Pre-Approval

Getting pre-approved for an auto loan with a credit union like SchoolsFirst before you visit the dealership offers several distinct advantages. Pre-approval means a lender has reviewed your financial information and provisionally agreed to lend you a specific amount at a certain interest rate, subject to final verification.

With a pre-approval in hand, you walk into the dealership as a cash buyer. You know exactly how much you can spend, which gives you immense negotiating power on the vehicle’s price, rather than being swayed by monthly payment figures. It also streamlines the purchasing process, as a significant portion of the financing is already handled.

Understanding the Fine Print: APR vs. Interest Rate

When comparing loan offers, always pay attention to the Annual Percentage Rate (APR) rather than just the stated interest rate. The APR represents the true annual cost of borrowing money, including the interest rate plus any additional fees or charges associated with the loan (like origination fees). While the interest rate is a component of the APR, the APR gives you a more accurate picture of the total cost of borrowing.

Considering Additional Costs: The True Cost of Ownership

Beyond the loan payment, remember the other significant costs that come with car ownership. Auto insurance premiums can vary wildly based on your vehicle, driving record, and location. Maintenance, such as oil changes, tire rotations, and scheduled services, is a recurring expense. Fuel costs can add up, especially with rising gas prices. Always factor these into your overall budget to avoid any financial surprises down the road. Our guide on Understanding Car Insurance: A Comprehensive Overview (internal link placeholder) can help you prepare.

SchoolsFirst Credit Union: A Partner in Your Journey

SchoolsFirst Credit Union stands out as a financial institution committed to its members. Specifically founded to serve the educational community, they operate with a member-first philosophy, often translating into more favorable loan terms and personalized service compared to traditional banks. Their focus isn’t just on making a profit but on empowering their members with financial tools and resources.

When you use the SchoolsFirst Car Loan Calculator, you’re not just plugging numbers into a generic formula. You’re leveraging a tool provided by an institution that understands the unique financial needs of its community and strives to offer competitive rates and transparent processes. This dedication to service and financial well-being is why many trust SchoolsFirst for their auto loan needs, making their calculator a highly relevant and trustworthy resource.

Common Mistakes to Avoid When Using an Auto Loan Calculator

While an auto loan calculator is a powerful tool, misusing it can lead to inaccurate expectations and poor financial decisions.

- Ignoring the Down Payment: Many users input a zero down payment, leading to a higher estimated monthly payment than necessary. Always factor in what you can put down, as it significantly impacts your loan.

- Focusing Only on Monthly Payment: This is perhaps the biggest pitfall. A low monthly payment achieved by extending the loan term often means paying far more in total interest. Always look at the total cost of the loan, not just the monthly figure.

- Not Factoring in Total Cost of Ownership: As discussed, the loan payment is just one piece. Forgetting about insurance, fuel, and maintenance can lead to being "car-poor."

- Not Checking Your Credit Score First: Without an accurate idea of your credit score, the interest rate you input will be a guess, making your estimated payment potentially unrealistic.

- Using Generic Calculators for Specific Lender Rates: While generic calculators are fine for a rough estimate, using a lender-specific tool like the SchoolsFirst Car Loan Calculator provides a more accurate picture of what you might actually qualify for with that institution.

Pro Tips for Optimizing Your Car Loan with SchoolsFirst

To truly maximize your financial advantage when buying a car and using the SchoolsFirst Car Loan Calculator, consider these expert tips:

- Get Pre-Approved with SchoolsFirst: As highlighted, this gives you immense power at the dealership and helps you understand your budget before falling in love with a car outside your price range.

- Maximize Your Down Payment: The more you put down upfront, the less you borrow, the less interest you pay, and the lower your monthly payments will be. It also gives you instant equity in your vehicle.

- Consider a Shorter Loan Term If Affordable: If your budget allows for a higher monthly payment, opt for a shorter loan term. You’ll save significantly on interest and pay off your car much faster.

- Shop Around for Insurance Quotes Early: Insurance costs vary dramatically. Get quotes for the specific vehicle you’re considering before you buy it, as a high premium could impact your overall affordability.

- Understand Your Credit Score and Work to Improve It: Even a few points on your credit score can make a difference in your interest rate. Regularly monitor your credit and take steps to enhance it.

Conclusion: Drive Away with Confidence and Financial Clarity

The journey to owning your next vehicle should be exciting, not stressful. By leveraging the SchoolsFirst Car Loan Calculator, you equip yourself with an invaluable tool for informed decision-making. This calculator isn’t just about crunching numbers; it’s about gaining clarity, understanding the financial implications of your choices, and empowering you to secure an auto loan that genuinely fits your budget and financial goals.

Remember, a car purchase is a significant investment. Taking the time to understand the key components of a loan, strategically planning your approach, and utilizing reliable resources like the SchoolsFirst Car Loan Calculator will pave the way for a smooth, confident, and financially sound vehicle acquisition. Drive away not just with your dream car, but with the peace of mind that comes from making a truly smart financial decision.