Navigating Your Dream Ride: A Comprehensive Guide to Capital One Bank Car Loans

Navigating Your Dream Ride: A Comprehensive Guide to Capital One Bank Car Loans Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but the financing aspect can often feel daunting. For millions of Americans, securing the right car loan is a crucial step, and Capital One Bank has emerged as a significant player in simplifying this process. As an expert blogger and professional SEO content writer, I’ve delved deep into the world of auto financing, and I can confidently say that understanding Capital One’s offerings can empower you to make informed decisions.

This comprehensive guide is designed to be your ultimate resource for everything you need to know about Capital One Bank Car Loans. We’ll explore their unique approach, demystify the application process, and provide expert insights to help you secure the best possible deal. Our ultimate goal is to equip you with the knowledge to navigate your auto financing journey with confidence and ease.

Navigating Your Dream Ride: A Comprehensive Guide to Capital One Bank Car Loans

Why Capital One Stands Out in the Auto Loan Landscape

Capital One isn’t just another bank offering car loans; they’ve carved a distinct niche by focusing on accessibility, transparency, and innovation. Their approach aims to put the power back into the buyer’s hands, making the financing experience less stressful and more predictable. This commitment to customer empowerment is a major reason why many car shoppers turn to them.

Based on my experience, Capital One has invested heavily in technology to streamline the car buying process, moving it beyond traditional bank visits and endless paperwork. They understand that today’s consumers expect convenience and clear information, and their platforms are designed to deliver just that. This forward-thinking strategy sets them apart from many competitors in the auto financing space.

Transparency and Clarity in Financing

One of the most frustrating aspects of car buying can be the lack of upfront information regarding financing. Capital One tackles this head-on by providing tools that offer clear insights into what you can afford. This transparency helps eliminate unwelcome surprises at the dealership, allowing you to focus on finding the right vehicle rather than worrying about hidden costs.

They strive to make complex financial terms easy to understand, ensuring that you grasp the implications of your loan before you commit. This commitment to clarity builds trust and empowers you to negotiate confidently. You’ll know your budget and potential monthly payments before you even set foot on a car lot.

Accessibility for a Broad Range of Credit Scores

Another key differentiator for Capital One is their willingness to work with a wide spectrum of credit profiles. While many lenders primarily cater to those with excellent credit, Capital One recognizes that life happens, and not everyone has a perfect score. They offer options for individuals with good, average, and even challenged credit.

This inclusivity means that more people have the opportunity to secure reliable transportation, which is often essential for work, family, and daily life. It’s about providing a path forward for those who might otherwise feel excluded from the auto loan market. They assess more than just a single number, looking at your overall financial picture.

The Game-Changing Auto Navigator Tool

Perhaps Capital One’s most revolutionary offering is their Auto Navigator tool. This online platform is designed to transform the car buying experience from a guessing game into a well-informed decision-making process. It allows you to explore financing options and available vehicles from the comfort of your home.

The Auto Navigator provides real-time, personalized offers without impacting your credit score. This pre-qualification step is invaluable, as it gives you a clear understanding of your budget before you even begin test driving cars. It’s a tool that truly empowers the consumer.

Extensive Dealership Network

Capital One doesn’t operate in isolation; they partner with a vast network of dealerships across the country. This extensive network means that once you’re pre-qualified, you have a wide array of vehicles and locations to choose from. It simplifies the transition from online pre-qualification to in-person purchase.

This collaboration ensures that the financing offer you receive through Auto Navigator is honored at participating dealerships. It creates a seamless bridge between securing your financing and driving off in your new car. This integrated approach reduces friction and saves you valuable time.

Demystifying the Capital One Auto Navigator Tool

The Capital One Auto Navigator is more than just a pre-qualification tool; it’s a comprehensive platform designed to streamline your entire car buying journey. Understanding how it works is key to leveraging its full potential. Think of it as your personal financial assistant for car shopping.

Pro tips from us: Always start your car buying process with the Auto Navigator. It provides invaluable clarity and confidence, setting you up for success before you even visit a dealership. This initial step can save you hours of negotiation and stress.

What is Auto Navigator and How Does It Work?

The Auto Navigator is Capital One’s proprietary online platform that allows you to get pre-qualified for an auto loan and then search for vehicles that fit your budget. You simply provide some basic personal and financial information, and within minutes, you’ll receive personalized loan offers. These offers include estimated monthly payments and interest rates.

The beauty of this tool is that it uses a "soft inquiry" on your credit, meaning it won’t affect your credit score. This allows you to explore your options without any financial risk. Once you have your pre-qualification, you can browse an inventory of vehicles from participating dealerships that match your approved loan terms.

Pre-qualification vs. Pre-approval: Understanding the Difference

It’s crucial to understand the distinction between pre-qualification and pre-approval, especially when dealing with auto loans. Capital One’s Auto Navigator offers pre-qualification.

- Pre-qualification provides an estimate of what you might be approved for, based on a soft credit inquiry. It’s not a guaranteed offer, but it gives you a strong indication of your financial standing and potential loan terms. It’s a fantastic starting point for budgeting.

- Pre-approval typically involves a "hard inquiry" on your credit report and is a more firm offer of credit. While Auto Navigator leads to a very strong offer, the final terms are confirmed at the dealership during the full application process, which then becomes a hard inquiry.

Based on my experience, treating Capital One’s pre-qualification as a highly reliable estimate is the best approach. It empowers you with solid numbers to discuss with dealers.

Benefits for Car Buyers

The advantages of using the Auto Navigator are numerous:

- Know Your Budget Upfront: You’ll have a clear understanding of your spending limit and estimated monthly payments before you even start shopping. This prevents falling in love with a car you can’t truly afford.

- Save Time at the Dealership: With pre-qualification in hand, you can bypass much of the initial financing discussion at the dealership. You walk in as an informed buyer, ready to focus on the vehicle itself.

- No Impact on Credit Score: The soft inquiry ensures you can explore your options freely without worrying about dinging your credit. This is a huge advantage for careful financial planning.

- Shop with Confidence: Knowing your financing is largely sorted out allows you to negotiate car prices more effectively. You’re a cash buyer in the dealer’s eyes, even though you’re financing.

- Personalized Offers: The offers are tailored to your specific credit profile and financial situation, providing realistic expectations.

Step-by-Step Process with Auto Navigator

- Visit the Capital One Auto Navigator Website: Start by navigating to their dedicated platform.

- Enter Basic Information: Provide details such as your desired loan amount, income, housing costs, and Social Security number. This information helps them assess your financial health.

- Receive Personalized Offers: Within minutes, you’ll see multiple loan offers with varying terms (e.g., 36, 48, 60 months) and estimated monthly payments.

- Browse Vehicles: Use the tool to search for cars from participating dealerships that match your pre-qualified budget. You can filter by make, model, year, and features.

- Visit a Dealership: Print or save your pre-qualification offer and take it to a participating dealership. The dealer will then work with Capital One to finalize your loan.

This streamlined process takes much of the guesswork and anxiety out of car financing. It’s a modern approach to an often outdated system.

Who Can Get a Capital One Car Loan? (Credit Score Considerations)

One of Capital One’s strengths is its commitment to providing auto loan options for a diverse range of credit profiles. They understand that not everyone has perfect credit, and they strive to offer solutions for various financial situations. This inclusive approach makes them a go-to lender for many.

Common mistakes to avoid are assuming your credit score automatically disqualifies you. Always explore your options, as Capital One might surprise you with what they can offer. A low score doesn’t always mean no loan.

Good Credit: The Advantages

If you boast a strong credit score (typically 670+ FICO), you’re in an excellent position to secure the most favorable terms on a Capital One car loan. This means lower interest rates, which translate to lower monthly payments and less money paid over the life of the loan. Lenders view good credit as a sign of financial responsibility.

With good credit, you’ll likely have more flexibility in loan terms, such as choosing a shorter loan period to save on interest, or a slightly longer one for lower payments if desired. Capital One will see you as a low-risk borrower, which works to your advantage. You’ll likely breeze through the application process with minimal hurdles.

Average/Fair Credit: How Capital One Helps

For those with average or fair credit (typically 580-669 FICO), securing an auto loan can sometimes be a challenge with traditional lenders. However, Capital One is known for being more accommodating in this range. They understand that a fair credit score can often be a stepping stone to better financial health.

While your interest rates might be slightly higher than someone with excellent credit, Capital One often provides competitive options that are more accessible than many other banks. They look beyond just the score, considering factors like your income and debt-to-income ratio. This provides a valuable opportunity to finance a vehicle while simultaneously working to improve your credit.

Bad Credit: Options and Realistic Expectations

Even if your credit score is considered "bad" (typically below 580 FICO), Capital One may still have options available. They are one of the few major banks willing to work with individuals who have faced financial difficulties in the past. This makes them a lifeline for many who desperately need reliable transportation.

It’s important to set realistic expectations if you have bad credit. Your interest rates will likely be higher, reflecting the increased risk for the lender. However, securing an auto loan, making consistent on-time payments, and managing the debt responsibly can be a powerful way to rebuild your credit score over time. Capital One offers a path to re-establish your financial footing.

For a deeper dive into improving your credit score before applying for a loan, check out our guide on . Understanding these strategies can significantly impact your loan terms.

The Application Process: From Pre-qualification to Driving Away

Securing a Capital One car loan is a multi-step process that begins with their innovative online tools and culminates at a participating dealership. Understanding each phase will help you navigate the journey smoothly and efficiently. Preparation is key to a stress-free experience.

Pro tips from us: Gather all necessary documents before you visit the dealership. This foresight will dramatically speed up the finalization of your loan and get you into your new car faster. A little planning goes a long way.

Online Application Steps

The initial application begins with the Capital One Auto Navigator, as discussed earlier. You’ll:

- Provide Personal Details: Name, address, contact information, date of birth.

- Share Employment and Income Information: Your employer’s name, duration of employment, annual income, and any other sources of income.

- Input Housing Information: Whether you rent or own, your monthly housing payment.

- Review and Submit: Double-check all information for accuracy before submitting your request for pre-qualification.

This digital process is designed for speed and convenience, often providing an instant response. It sets the foundation for your loan journey.

Required Documents

While the initial pre-qualification doesn’t require documents, the full loan application at the dealership will. Be prepared to provide:

- Proof of Identity: Valid government-issued ID (driver’s license, state ID).

- Proof of Income: Recent pay stubs (usually two or three), bank statements, or tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement with your current address.

- Proof of Insurance: You’ll need to show proof of auto insurance before driving off the lot.

- Social Security Number: For the hard credit inquiry.

Having these documents organized and ready will expedite the final paperwork at the dealership. It’s a common step across all lenders.

Working with a Dealership

Once you have your Capital One pre-qualification offer, you’ll take it to a participating dealership. The sales team will:

- Verify Your Offer: They will review your Capital One pre-qualification.

- Select a Vehicle: Choose a car that fits your pre-qualified budget and preferences.

- Finalize the Loan: The dealership will submit your full application to Capital One. This step involves a hard credit inquiry. Capital One will then provide the final loan terms, which should closely match your pre-qualification, assuming no significant changes in your financial situation or credit score.

- Sign Paperwork: Once approved, you’ll sign all the necessary loan documents and vehicle purchase agreements.

The dealership acts as an intermediary, facilitating the final steps of your Capital One loan. Their role is to process the sale and coordinate with the bank.

Loan Terms and Conditions

When finalizing your Capital One car loan, pay close attention to the following terms:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including the interest rate and any fees.

- Loan Term: The length of time you have to repay the loan, typically 36, 48, 60, or 72 months. A shorter term means higher monthly payments but less interest paid overall.

- Monthly Payment: The fixed amount you’ll pay each month.

- Total Amount Financed: The principal amount of the loan.

- Down Payment: Any initial payment you make towards the vehicle purchase. A larger down payment can reduce your monthly payments and total interest.

Ensure you fully understand all these elements before signing on the dotted line. Don’t hesitate to ask questions.

New vs. Used Car Loans with Capital One

Capital One provides financing options for both new and used vehicles, but there are some important distinctions to keep in mind. The type of vehicle you choose can impact your loan terms and eligibility. It’s not a one-size-fits-all approach.

Common mistakes to avoid are assuming the same terms apply to both new and used cars. Always clarify the specific requirements for the vehicle you’re interested in.

Differences in Terms

Generally, new car loans tend to come with lower interest rates and potentially longer loan terms compared to used car loans. This is because new cars are seen as less of a risk to lenders; they have a higher resale value and less uncertainty about their history. Capital One reflects these industry standards in its offerings.

Used car loans, while often carrying slightly higher rates, still offer competitive options through Capital One. The terms will depend heavily on the vehicle’s age, mileage, and overall condition. Capital One aims to provide accessible financing across both categories.

Vehicle Eligibility (Age, Mileage Restrictions)

Capital One, like most lenders, has specific eligibility requirements for the vehicles they will finance. These often include:

- Maximum Vehicle Age: There’s usually an age limit for used cars. For instance, Capital One typically finances vehicles no older than 10 years from the current model year.

- Maximum Mileage: A mileage cap is also common, often around 120,000 to 150,000 miles. Vehicles with exceptionally high mileage may be considered too risky.

- Vehicle Type: Certain vehicle types, like commercial trucks, motorcycles, or recreational vehicles, may not be eligible for standard auto loans. Capital One’s focus is primarily on passenger cars, SUVs, and light trucks.

- Vehicle Condition: The vehicle must meet certain safety and mechanical standards. Salvage or rebuilt titles are usually not eligible.

Always confirm these restrictions with Capital One or your participating dealership to ensure the vehicle you’re eyeing qualifies for financing. This step is crucial before getting too far into the purchasing process.

Refinancing Your Car Loan with Capital One

Sometimes, circumstances change after you’ve already purchased a vehicle and secured a loan. Perhaps your credit score has improved, or market interest rates have dropped. In such cases, refinancing your car loan with Capital One could be a smart financial move. It’s an opportunity to potentially save money or adjust your monthly payments.

Pro tips from us: Regularly review your auto loan terms against current market rates, especially if your credit has improved. Refinancing can often lead to significant savings over the life of your loan.

When Refinancing Makes Sense

Refinancing your auto loan means replacing your existing loan with a new one, often with different terms. It typically makes sense in a few key scenarios:

- Improved Credit Score: If your credit score has significantly improved since you took out your original loan, you might qualify for a much lower interest rate.

- Lower Interest Rates: If general interest rates in the market have fallen, you could get a better deal on a new loan.

- Reduce Monthly Payments: You might want to extend your loan term to lower your monthly payments, freeing up cash flow (though this often means paying more interest overall).

- Shorten Loan Term: Conversely, if you want to pay off your loan faster and can afford higher payments, you can refinance to a shorter term, saving a substantial amount on interest.

- Remove a Co-signer: If you initially needed a co-signer but now have strong enough credit on your own, refinancing can allow you to remove them from the loan.

Capital One offers competitive refinancing options, making them a strong contender if you’re considering this move.

Benefits of Refinancing

Refinancing your auto loan can yield several tangible benefits:

- Lower Interest Rate: The most common reason, leading to substantial savings.

- Reduced Monthly Payment: Makes your budget more manageable.

- Save Money Over Time: A lower interest rate or shorter term means less money paid in total.

- Change Loan Term: Adjust the repayment period to better suit your current financial situation.

- Simplified Payments: If you have multiple loans, consolidating them can simplify your finances.

The Refinancing Process

The refinancing process with Capital One is straightforward:

- Check Your Eligibility: Use Capital One’s online tools to see if you pre-qualify for a refinancing offer. This is similar to the Auto Navigator process for new loans.

- Gather Information: You’ll need details about your current loan (lender, outstanding balance, current interest rate) and your vehicle (VIN, mileage).

- Apply Online: Submit your refinancing application. Capital One will conduct a hard credit inquiry at this stage.

- Review Offers: If approved, you’ll receive new loan terms. Compare these carefully to your existing loan.

- Finalize the Loan: If you accept the offer, Capital One will pay off your old loan, and you’ll begin making payments on your new loan with them.

It’s a process designed to be as smooth as possible, allowing you to quickly take advantage of better terms.

Beyond the Loan: Managing Your Capital One Auto Loan

Once you’ve secured your Capital One car loan and driven off in your new vehicle, the journey doesn’t end. Effective loan management is crucial for maintaining good financial health and ensuring a smooth repayment experience. Capital One provides several tools and resources to help you manage your account with ease.

Common mistakes to avoid are setting and forgetting your loan. Actively manage your account to avoid late fees and ensure timely payments.

Online Account Management

Capital One offers a robust online portal and mobile app for managing your auto loan account. Through these platforms, you can:

- View Account Details: Access your current balance, payment history, interest paid year-to-date, and remaining loan term.

- Make Payments: Schedule one-time payments or set up recurring automatic payments from your checking or savings account.

- Access Statements: View and download your monthly billing statements.

- Update Information: Change your contact information or payment preferences.

This digital access puts you in control of your loan, allowing you to manage it anytime, anywhere. It’s incredibly convenient for today’s busy world.

Payment Options

Capital One provides a variety of payment options to suit your preferences:

- Online Payments: The most convenient method, available through their website or mobile app.

- Automatic Payments: Set up recurring payments to ensure you never miss a due date. This can often help you avoid late fees and maintain a good payment history.

- Phone Payments: Make payments over the phone through their customer service line.

- Mail Payments: Send a check or money order to the designated payment address.

- In-Person Payments: In some cases, you may be able to make payments at a Capital One branch or through a partner payment center.

Choosing an option that fits your routine is important for consistent on-time payments.

Customer Service

Should you have any questions or encounter issues with your loan, Capital One provides dedicated customer service for auto loans. You can typically reach them via:

- Phone: A dedicated toll-free number for auto loan inquiries.

- Secure Message Center: Through your online account, you can send secure messages and receive responses directly.

- Mail: For formal correspondence.

Having accessible customer support is a critical component of a positive banking experience. They are there to assist you when needed.

Impact on Credit Score

Managing your Capital One auto loan responsibly can have a significant positive impact on your credit score. Here’s how:

- Payment History: Your payment history is the most important factor in your credit score. Making on-time payments consistently will build a strong positive history.

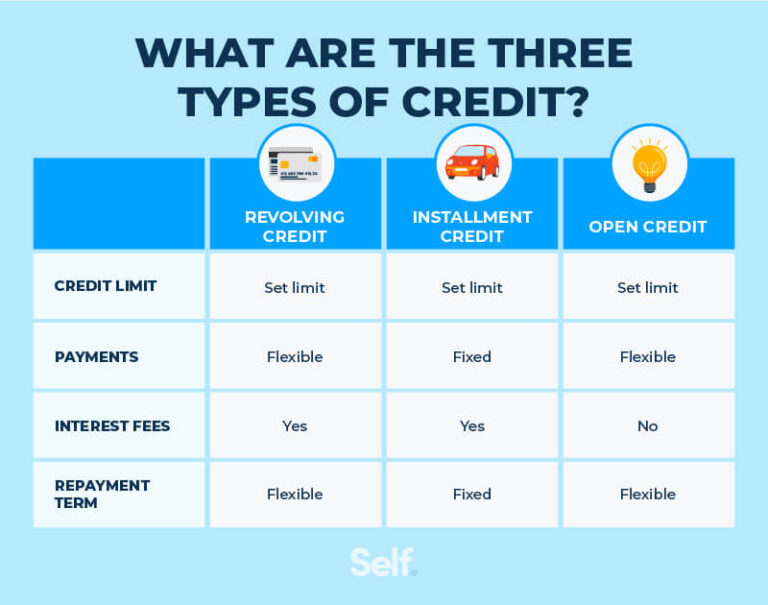

- Credit Mix: An auto loan diversifies your credit mix (revolving credit like credit cards vs. installment credit like loans), which can positively influence your score.

- Credit Utilization: An installment loan doesn’t factor into credit utilization in the same way as revolving credit, but managing the debt well shows responsible borrowing.

Conversely, missing payments or defaulting on your loan will severely damage your credit score. Responsible management is key to leveraging your auto loan as a tool for credit building. If you’re wondering about the true cost of car ownership beyond the loan, read our comprehensive article on .

Common Mistakes to Avoid When Getting a Capital One Car Loan

Even with Capital One’s user-friendly approach, common pitfalls can trip up unsuspecting car buyers. Being aware of these mistakes can save you money, time, and frustration. Forewarned is forearmed in the world of auto financing.

Pro tips from us: Always take a moment to breathe and think before making a final decision. Don’t let the excitement of a new car rush you into a bad financial choice.

- Not Pre-qualifying: The biggest mistake is skipping the Auto Navigator. Walking into a dealership without knowing your financing options puts you at a significant disadvantage. You lose negotiating power and might accept less favorable terms out of convenience.

- Focusing Only on Monthly Payments: While important, fixating solely on the monthly payment can lead to accepting longer loan terms or higher interest rates that cost you more in the long run. Always consider the total cost of the loan.

- Ignoring the Total Cost of Ownership: Beyond the loan, remember to factor in insurance, maintenance, fuel, and potential depreciation. A cheap monthly payment doesn’t always mean a cheap car overall.

- Not Comparing Offers: Even with a Capital One pre-qualification, it’s wise to briefly compare it with other lenders if you have strong credit. While Capital One is competitive, a quick check ensures you’re getting the absolute best deal.

- Falling for Dealer Add-ons: Dealerships often try to sell extended warranties, paint protection, or VIN etching. While some might be useful, many are overpriced and can be purchased elsewhere for less, or are simply unnecessary. Don’t roll them into your loan without careful consideration.

- Not Reading the Fine Print: Always thoroughly read your loan agreement before signing. Understand all terms, conditions, fees, and penalties. If something isn’t clear, ask for clarification.

- Lying on Your Application: Providing inaccurate information can lead to your loan being denied or even legal repercussions. Always be honest and transparent in your financial disclosures.

- Overlooking Your Budget: Don’t get emotionally attached to a car that stretches your budget too thin. Stick to what you can comfortably afford, not just what you’re approved for.

By avoiding these common mistakes, you can ensure a smoother, more financially sound car buying experience with Capital One.

Pros and Cons of Capital One Car Loans

To provide a balanced perspective, let’s summarize the advantages and potential drawbacks of choosing Capital One for your auto financing needs. Every financial product has its strengths and weaknesses.

Pros:

- Exceptional Pre-qualification Tool (Auto Navigator): Provides transparency and empowers buyers with upfront loan terms without impacting their credit score.

- Accessibility for Diverse Credit Scores: Offers financing options for individuals with good, average, and even challenged credit, expanding access to auto ownership.

- Extensive Dealership Network: Partners with thousands of dealerships, providing a wide selection of vehicles and convenient purchasing options.

- Streamlined Online Experience: The digital application and account management tools are modern and user-friendly.

- Competitive Rates: Often provides competitive interest rates, especially for those with good credit.

- Refinancing Options: Offers the ability to refinance existing loans, potentially saving money or adjusting payment terms.

Cons:

- Limited Dealership Network (Specific Partners): While extensive, you must purchase from a Capital One-affiliated dealership. This might restrict choices if your dream car is at a non-partner dealer.

- No Direct-to-Consumer Loans (Initially): The process always involves a dealership to finalize the loan, unlike some lenders who offer direct financing.

- Rates Can Vary for Challenged Credit: While accessible, individuals with lower credit scores will face higher interest rates, which is standard but still a cost to consider.

- Vehicle Restrictions: Age and mileage restrictions on used cars can limit options for very old or high-mileage vehicles.

For official information directly from Capital One, you can always visit their official auto loan page at .

Conclusion: Driving Forward with Confidence

Securing a car loan is a significant financial decision, and choosing the right lender can make all the difference. Capital One Bank has clearly positioned itself as a leader in auto financing, particularly through its innovative Auto Navigator tool and its commitment to serving a broad spectrum of credit profiles. By offering transparency, accessibility, and a streamlined process, they empower car buyers to make informed choices and drive away with confidence.

Whether you’re purchasing a brand-new vehicle, a reliable used car, or looking to refinance an existing loan, Capital One provides a robust framework to support your journey. Remember to leverage their pre-qualification tools, understand the terms, and manage your loan responsibly. By doing so, you’ll not only secure the transportation you need but also build a stronger financial future. Your dream ride is within reach, and Capital One is ready to help you navigate the path.