Navigating Your Drive: The Ultimate Expert Guide to Bank of America Car Loans

Navigating Your Drive: The Ultimate Expert Guide to Bank of America Car Loans Carloan.Guidemechanic.com

The journey to owning a new or pre-owned vehicle is an exciting one, often culminating in the freedom of the open road. For many, this journey begins with securing the right financing. Among the myriad options available, Bank of America stands out as a prominent and trusted name in the automotive lending landscape. As an expert blogger and professional SEO content writer, my mission is to provide you with a super comprehensive, in-depth look at everything you need to know about securing a Bank of America car loan.

This article isn’t just a surface-level overview; it’s a pillar content piece designed to be your definitive guide. We’ll explore the nuances of their offerings, delve into application strategies, and provide pro tips to ensure you make the most informed decision. Our ultimate goal is to empower you with the knowledge to drive away confidently, knowing you’ve secured the best possible financing for your next vehicle.

Navigating Your Drive: The Ultimate Expert Guide to Bank of America Car Loans

Why Consider Bank of America for Your Car Loan? A Trusted Partner on the Road

When it comes to significant financial commitments like a car loan, choosing a reputable lender is paramount. Bank of America, one of the largest financial institutions in the United States, brings a long-standing history of stability, extensive resources, and a broad range of financial products to the table. Their reputation often precedes them, offering a sense of security to borrowers.

Opting for a Bank of America car loan means partnering with an institution that understands the diverse needs of car buyers. They cater to a wide spectrum of credit profiles and offer various loan products designed to fit different purchasing scenarios. This flexibility, combined with their customer support infrastructure, makes them a strong contender for your auto financing needs.

Furthermore, Bank of America frequently offers competitive interest rates to qualified applicants. While rates can vary based on market conditions, individual creditworthiness, and loan terms, their position in the market allows them to remain highly competitive. For many, the convenience of managing their auto loan alongside other banking products, like checking accounts or credit cards, all within one familiar platform, is an invaluable benefit.

Decoding Bank of America Car Loan Options: Finding Your Perfect Fit

Bank of America offers a variety of car loan products, each tailored to specific purchasing situations. Understanding these options is crucial for selecting the loan that best aligns with your needs and financial goals. Whether you’re eyeing a brand-new model, a dependable used car, or looking to optimize your existing loan, Bank of America likely has a solution.

Let’s break down the primary types of auto loans they provide. Each category comes with its own set of considerations, from interest rates to loan terms and application requirements. Knowing these distinctions will help you navigate the choices effectively.

1. New Car Loans

For those seeking the thrill of a brand-new vehicle, Bank of America offers financing specifically designed for new car purchases. These loans typically come with favorable interest rates, reflecting the lower risk associated with financing a new asset. New car loans are usually available for vehicles purchased directly from dealerships.

The terms for new car loans can be quite flexible, often extending up to 72 or even 84 months. While longer terms can result in lower monthly payments, it’s essential to consider the total interest paid over the life of the loan. Based on my experience, securing a new car loan with Bank of America is often a straightforward process, especially if you have a strong credit history.

2. Used Car Loans

If a pre-owned vehicle is more your style, Bank of America also provides robust options for used car financing. These loans are designed for vehicles purchased from dealerships or even through private party sales, which we’ll discuss shortly. While rates for used cars might be slightly higher than for new ones due to factors like depreciation and potential maintenance, Bank of America strives to keep them competitive.

Eligibility for used car loans often depends on the vehicle’s age and mileage. Typically, Bank of America finances vehicles up to a certain age limit (e.g., 7-10 years old) and mileage threshold (e.g., 100,000-125,000 miles). It’s always wise to check their current specific criteria before you start shopping. Pro tips from us: Always get a pre-purchase inspection for any used car you consider, regardless of the lender.

3. Private Party Car Loans

One unique and highly valuable offering from Bank of America is their financing for private party car sales. Many lenders shy away from this type of transaction due to the perceived higher risk. However, Bank of America steps in to fill this gap, allowing you to finance a used car purchased directly from an individual seller.

This option opens up a wider market for car buyers, potentially allowing you to find better deals than at a dealership. The process involves Bank of America facilitating the payment to the private seller, often requiring specific documentation about the vehicle and the seller. Common mistakes to avoid are not thoroughly vetting the seller or the vehicle’s history before committing to this type of loan. Always conduct a title search and review a vehicle history report.

4. Auto Loan Refinancing

Perhaps you already have a car loan but are looking for better terms. Bank of America’s auto loan refinancing options can be a game-changer. Refinancing allows you to replace your existing car loan with a new one, potentially at a lower interest rate, with a different loan term, or both. This can lead to significant savings over the life of the loan or more manageable monthly payments.

Reasons for refinancing vary. You might have improved your credit score since taking out your original loan, or perhaps market interest rates have dropped. Refinancing with Bank of America can also be an opportunity to adjust your monthly payment to better suit your current budget.

Understanding Bank of America Car Loan Rates: What Drives Your Payments

Interest rates are arguably the most critical factor influencing the total cost of your car loan. Bank of America, like all lenders, determines your specific interest rate based on a variety of factors. Understanding these elements can help you take steps to secure the most favorable terms possible.

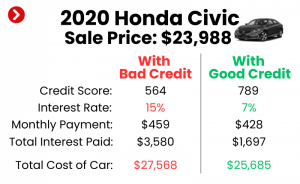

Your credit score is the primary determinant. A higher credit score signals lower risk to lenders, often resulting in lower interest rates. Conversely, a lower score typically leads to higher rates to compensate the lender for the increased risk. Bank of America considers your entire credit history when making this assessment.

Beyond your credit score, your debt-to-income (DTI) ratio also plays a significant role. This ratio compares your monthly debt payments to your gross monthly income. A lower DTI indicates that you have more disposable income to cover your loan payments, making you a more attractive borrower. Lenders want to see that you can comfortably afford the new loan payment without being overextended.

The loan term, or the length of time you have to repay the loan, also impacts your rate. Shorter loan terms often come with lower interest rates because the lender’s money is tied up for a shorter period. However, shorter terms mean higher monthly payments. Longer terms, while reducing monthly payments, typically carry slightly higher rates and result in more interest paid over time.

Finally, the vehicle itself influences the rate. New cars generally qualify for lower rates than used cars due to their higher value and lower depreciation risk. The age, mileage, and overall condition of a used car can also affect the interest rate offered.

The Bank of America Car Loan Application Process: A Step-by-Step Walkthrough

Applying for a car loan can seem daunting, but Bank of America streamlines the process to make it as user-friendly as possible. Understanding each step beforehand can help you prepare thoroughly and minimize any potential delays. The process often begins with pre-qualification or pre-approval, a crucial step for savvy car buyers.

Step 1: Get Pre-Approved (Highly Recommended)

Before you even step foot on a dealership lot, consider getting pre-approved for a Bank of America car loan. Pre-approval involves submitting an application with your financial information, allowing the bank to assess your creditworthiness and provide you with an estimated loan amount and interest rate. This step usually results in a soft credit inquiry, which doesn’t impact your credit score.

Based on my experience, a pre-approval letter gives you significant leverage at the dealership. It acts as a maximum spending limit and provides a benchmark interest rate. You’ll know exactly what you can afford, and it allows you to focus on negotiating the car’s price rather than getting caught up in financing details at the sales desk. It transforms you from a mere shopper into a qualified buyer.

Step 2: Gather Your Documents

Once you’re ready to apply for the actual loan, whether for pre-approval or a direct application, you’ll need several key documents. Having these ready will expedite the process. Common documents include:

- Proof of Identity: Driver’s license or state-issued ID.

- Proof of Income: Pay stubs, W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit verification.

- Vehicle Information (if already chosen): VIN, make, model, year, and mileage.

Pro tips from us: Make sure all your documents are current and accurately reflect your financial situation. Any discrepancies could cause delays or issues with your application.

Step 3: Complete the Application

Bank of America offers various ways to apply for a car loan. You can apply online through their secure portal, visit a local branch, or even apply directly through a participating dealership that partners with Bank of America. The online application is often the quickest and most convenient option.

The application will ask for personal details, employment history, income information, and details about the vehicle you intend to purchase (if known). Be thorough and honest in your responses. After submission, the bank will perform a hard credit inquiry, which might temporarily lower your credit score by a few points.

Step 4: Await a Decision

After you submit your application, Bank of America’s underwriting team will review your information. They’ll assess your credit report, income, debt, and the vehicle details (if applicable) to determine your eligibility and the loan terms they can offer. This decision can sometimes be immediate for pre-approvals or take a few business days for a full application, especially if additional documentation is required.

If approved, you’ll receive a loan offer outlining the interest rate, loan term, and monthly payment. This is your opportunity to review everything carefully and ensure it aligns with your expectations.

Step 5: Finalize the Loan and Purchase Your Car

Upon accepting the loan offer, you’ll proceed to finalize the paperwork. This involves signing the loan agreement and other necessary documents. If you’re purchasing from a dealership, they will often handle this process in coordination with Bank of America. For private party sales, Bank of America will guide you through the process of transferring funds to the seller and securing the vehicle title.

Once all the paperwork is complete and funds are disbursed, you’re ready to drive away in your new vehicle! Remember to set up your payment method and keep track of your loan statements.

Bank of America Car Loan Requirements: What You Need to Qualify

Meeting the eligibility criteria is fundamental to securing a Bank of America car loan. While specific requirements can vary slightly, there are common benchmarks they look for in applicants. Understanding these will help you gauge your chances of approval and prepare accordingly.

- Credit Score: This is arguably the most crucial factor. While Bank of America doesn’t publish a minimum credit score, a score in the "good" to "excellent" range (typically 670+) will give you the best chance of approval and the most competitive interest rates. Applicants with lower scores might still be approved, but often with higher rates or shorter terms.

- Income and Employment Stability: Lenders want to see a steady source of income to ensure you can make your monthly payments. Bank of America will look at your employment history, current income, and possibly your bank statements. Consistent employment for at least two years is often preferred.

- Debt-to-Income (DTI) Ratio: As mentioned earlier, your DTI ratio is a key indicator of your financial health. Bank of America generally prefers a DTI ratio below 40-45%. A lower DTI demonstrates that you have sufficient income remaining after paying existing debts to comfortably take on a new car loan.

- Down Payment: While not always strictly required, making a down payment can significantly improve your loan terms. A down payment reduces the amount you need to borrow, which lowers your monthly payments and the total interest paid. It also shows the lender your commitment and reduces their risk.

- Vehicle Eligibility: The car itself must meet certain criteria. This includes limits on age and mileage for used vehicles, as well as ensuring the vehicle’s value aligns with the loan amount. The car will serve as collateral for the loan, so its condition and market value are important.

Common mistakes to avoid are applying with a significantly high DTI or a very low credit score without addressing these issues first. It’s always better to improve your financial standing before applying if possible.

Refinancing Your Car Loan with Bank of America: Unlocking Better Terms

Many car owners overlook the power of refinancing their auto loans. If your financial situation has improved, or if market rates have dropped since you originally financed your vehicle, refinancing with Bank of America could lead to substantial savings and a more comfortable payment plan. This strategy can put more money back into your pocket each month.

When should you consider refinancing? Here are a few key scenarios:

- Improved Credit Score: If your credit score has significantly increased since you took out your original loan, you’re likely eligible for a better interest rate.

- Lower Interest Rates: The general market interest rates might have fallen, meaning you could secure a lower rate now than when you first financed.

- High Interest Rate Original Loan: Perhaps you took out your first loan with a less-than-ideal credit score, resulting in a high interest rate. Refinancing can rectify this.

- Desire for Lower Monthly Payments: By extending your loan term (though this might mean more interest paid overall), refinancing can reduce your monthly obligations, freeing up cash flow.

- Desire for Shorter Loan Term: If you want to pay off your car faster, you could refinance to a shorter term with a lower interest rate, if your budget allows for higher monthly payments.

The refinancing process with Bank of America is similar to applying for a new loan. You’ll submit an application, provide income and vehicle details, and the bank will assess your eligibility for new terms. If approved, the new loan will pay off your old loan, and you’ll begin making payments to Bank of America under the new, hopefully more favorable, terms. This is a smart financial move many people don’t utilize.

Common Mistakes to Avoid When Applying for a Bank of America Car Loan

Even with the best intentions, applicants can sometimes make missteps that hinder their chances of approval or result in less favorable loan terms. Based on my experience in the financial sector, here are some common mistakes to be aware of and actively avoid:

- Applying with Too Many Lenders Simultaneously: While rate shopping is good, applying to multiple lenders within a short period can lead to multiple hard credit inquiries. These inquiries can temporarily ding your credit score, making you appear riskier to lenders. Focus on getting pre-approvals (which are usually soft inquiries) first.

- Not Checking Your Credit Report Beforehand: Many applicants go into the process blind. Always pull your credit report from the three major bureaus (Experian, Equifax, TransUnion) before applying. Look for errors, fraudulent activity, or outdated information that could negatively impact your score. Correcting these beforehand can significantly improve your loan prospects.

- Overlooking the Total Cost of the Loan: It’s easy to get fixated on the monthly payment. However, failing to consider the total interest paid over the life of the loan can be a costly mistake. A lower monthly payment often comes with a longer loan term and more interest. Always ask for the total cost breakdown.

- Not Getting Pre-Approved: As mentioned, pre-approval gives you buying power. Walking into a dealership without it puts you at a disadvantage, as you’re reliant on the dealership’s financing options, which may not be the most competitive.

- Ignoring the Down Payment: While zero-down loans exist, making a down payment is almost always beneficial. It reduces your loan amount, lowers monthly payments, and helps you avoid being "upside down" on your loan (owing more than the car is worth).

- Not Reading the Fine Print: Loan agreements are legal documents. Don’t rush through them. Understand all terms, conditions, fees, and penalties before signing. If something is unclear, ask for clarification.

Avoiding these common pitfalls can smooth out your car loan journey and save you a significant amount of money and stress in the long run.

Pro Tips for a Smooth Bank of America Car Loan Experience

Beyond avoiding mistakes, there are proactive steps you can take to ensure a seamless and successful experience with your Bank of America car loan. These professional tips are designed to maximize your benefits and minimize any potential headaches.

- Boost Your Credit Score: Before you even think about applying, dedicate time to improving your credit score. Pay down existing debts, make all payments on time, and dispute any errors on your credit report. Even a slight increase can translate into a better interest rate.

- Save for a Down Payment: Aim for at least a 10-20% down payment on a new car and potentially more for a used car. A substantial down payment not only reduces your monthly payments but also builds immediate equity in your vehicle.

- Know Your Budget (and Stick to It): Beyond the car loan payment, factor in insurance, fuel, maintenance, and potential registration fees. A common mistake is buying "too much car." Create a realistic budget and stick to it to avoid financial strain down the road.

- Research Car Values: Whether new or used, know the market value of the car you’re interested in. Use resources like Kelley Blue Book or Edmunds. This knowledge is crucial for negotiating the purchase price, ensuring you don’t overpay for the vehicle itself.

- Consider a Co-Signer (If Necessary): If your credit score is borderline or your income is limited, a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. Ensure both parties understand the responsibilities involved.

- Set Up Automatic Payments: Once your loan is approved, set up automatic payments from your Bank of America checking account (or another linked account). This ensures you never miss a payment, helps build positive credit history, and can sometimes even qualify you for a small interest rate discount.

- Stay Informed About Your Loan: Regularly review your loan statements and keep track of your payment history. Understanding your loan’s progress can help you plan for future financial decisions, like early repayment or refinancing opportunities.

By implementing these pro tips, you’re not just getting a loan; you’re strategically managing a significant financial asset. For official details on Bank of America’s auto loan offerings and to apply, visit their dedicated page.

Bank of America Customer Service and Support for Auto Loans

Even with the best preparation, questions or issues can arise during the life of your car loan. Bank of America provides multiple channels for customer support to ensure you can get the assistance you need. Their extensive network and customer service infrastructure are significant advantages.

You can typically reach their auto loan specialists via phone during business hours. Their website also features a comprehensive FAQ section that addresses many common inquiries, from application status to payment options. For existing customers, managing your loan through online banking or the Bank of America mobile app offers convenience and quick access to account information.

Visiting a local Bank of America branch is another viable option for in-person assistance, especially for complex questions or if you prefer face-to-face interaction. The availability of diverse support channels ensures that help is always at hand, providing peace of mind throughout your loan term.

Conclusion: Driving Forward with Confidence

Securing a Bank of America car loan can be a strategic move for many prospective car owners. Their diverse range of loan products, competitive rates, and robust customer support make them a strong contender in the automotive financing market. By understanding the different loan types, preparing for the application process, and implementing our expert tips, you can navigate your car purchase with confidence and secure financing that aligns with your financial goals.

Remember, the goal isn’t just to get a loan, but to get the right loan. Armed with the comprehensive knowledge shared in this guide, you are now well-equipped to make informed decisions and embark on your next driving adventure. Happy motoring!