Navigating Your Drive: The Ultimate Guide to Umpqua Car Loans and Smart Auto Financing

Navigating Your Drive: The Ultimate Guide to Umpqua Car Loans and Smart Auto Financing Carloan.Guidemechanic.com

The journey to owning your dream car is an exciting one, but the path to securing the right financing can often feel like a maze. For many in the Pacific Northwest and beyond, Umpqua Bank stands out as a community-focused financial institution offering personalized solutions. If you’re considering an Umpqua car loan, you’re looking at a partner known for its tailored approach and commitment to its customers.

This comprehensive guide will demystify everything you need to know about securing an Umpqua auto loan. We’ll delve deep into the application process, explore the benefits, and arm you with expert tips to make your car financing journey smooth and successful. Our goal is to provide a pillar content piece that empowers you with knowledge, helping you confidently drive away in your new vehicle with the best possible terms.

Navigating Your Drive: The Ultimate Guide to Umpqua Car Loans and Smart Auto Financing

Understanding Umpqua Bank’s Approach to Car Loans

Umpqua Bank isn’t just another financial institution; it prides itself on being a "Human-Digital" bank, blending innovative technology with a personalized, community-centric touch. This philosophy extends directly to their Umpqua car loan offerings, aiming to make vehicle financing accessible and understandable for everyone. They understand that a car is often more than just transportation; it’s a vital part of your daily life.

Based on my experience in the financial landscape, local and regional banks like Umpqua often offer a more nuanced and flexible approach compared to larger national lenders. They tend to prioritize building lasting customer relationships, which can translate into more personalized loan terms and dedicated support throughout your financing journey. This commitment to individual service is a hallmark of their operation.

They typically offer a range of Umpqua auto loan options designed to fit various needs, whether you’re purchasing a brand-new vehicle, a reliable used car, or looking to refinance an existing loan. Their focus is on providing solutions that genuinely work for your financial situation, rather than a one-size-fits-all model. This customer-first approach is a significant advantage when seeking vehicle financing.

The Benefits of Choosing Umpqua for Your Auto Loan

Opting for an Umpqua car loan comes with several distinct advantages that can significantly enhance your car-buying experience. These benefits often stem from their unique banking model and commitment to their customers. Understanding these can help you make an informed decision about your auto financing options.

Firstly, Umpqua Bank is known for offering competitive interest rates. While rates are always influenced by market conditions and individual credit profiles, Umpqua strives to provide attractive options that can save you money over the life of your loan. They assess each application individually, working to match you with a rate that reflects your financial standing.

Secondly, their flexible loan terms are a major draw. Umpqua understands that not everyone’s financial situation is the same, so they offer various repayment schedules to suit different budgets. Whether you prefer shorter terms to pay off your loan faster or longer terms to reduce your monthly payments, they work with you to find a comfortable fit. This flexibility is crucial for managing your personal finances effectively.

Moreover, the personalized service you receive is a significant differentiator. Unlike impersonal online lenders, Umpqua loan officers are often available to discuss your specific needs, answer questions, and guide you through every step of the car loan application. This human touch can alleviate stress and ensure you fully understand all aspects of your Umpqua vehicle financing. They genuinely aim to build a relationship, not just process a transaction.

Preparing for Your Umpqua Car Loan Application

A well-prepared applicant is a strong applicant. Before you even set foot in a dealership or start browsing online, taking a few crucial steps can significantly improve your chances of securing a favorable Umpqua car loan. This preparatory phase is where you lay the groundwork for a successful auto loan experience.

Understanding Your Credit Score

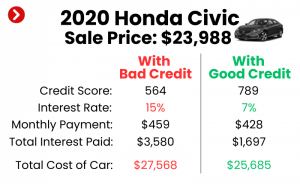

Your credit score is arguably the most critical factor influencing your Umpqua car loan interest rates and approval chances. Lenders use it to assess your creditworthiness and your likelihood of repaying the loan. A higher credit score generally translates to lower interest rates and better loan terms, saving you thousands over time.

Pro tips from us: Before you even think about applying, pull your credit report from one of the three major bureaus (Experian, Equifax, or TransUnion). You’re entitled to a free report annually from each through AnnualCreditReport.com. Review it for any inaccuracies and dispute them immediately, as errors can negatively impact your score. Improving your credit score, even slightly, can have a big impact on your Umpqua auto loan terms.

If your score isn’t where you want it to be, focus on paying bills on time, reducing existing debt, and avoiding opening too many new credit lines before applying for your Umpqua car loan. A strong credit history demonstrates reliability to lenders.

The Power of a Down Payment

Making a down payment on your vehicle purchase offers numerous benefits. It reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay over the life of the loan. A substantial down payment also signals to lenders that you are a serious and responsible borrower, potentially leading to better loan terms.

Common mistakes to avoid are underestimating the impact of a good down payment. Even 10-20% of the car’s value can make a significant difference. It also creates immediate equity in your vehicle, protecting you from being "upside down" on your loan, where you owe more than the car is worth, especially in the initial years. This financial cushion is invaluable.

Crafting Your Budget

Before committing to any Umpqua car loan, you must have a clear understanding of your personal budget. This involves more than just estimating your monthly car payment; you need to account for insurance, fuel, maintenance, and potential registration fees. A comprehensive budget ensures you can comfortably afford your new vehicle without straining your finances.

Based on my experience, many people get excited about the car itself and overlook the total cost of ownership. Use online calculators to factor in all these variables. Your debt-to-income ratio (DTI) is also important; lenders prefer a DTI below 43%, which shows you have enough disposable income to manage new debt.

Gathering Required Documents

Having all your documents in order before applying for an Umpqua car loan will streamline the process. While specific requirements may vary, generally you’ll need:

- Proof of Identity: A valid driver’s license or state ID.

- Proof of Income: Pay stubs, tax returns, or bank statements.

- Proof of Residence: Utility bills or a lease agreement.

- Vehicle Information: If you’ve already chosen a car, details like VIN, make, model, and mileage.

- Social Security Number: For credit checks.

Having these ready can prevent delays and make your car loan application much smoother.

The Umpqua Car Loan Application Process: A Step-by-Step Guide

Applying for an Umpqua car loan is designed to be straightforward, whether you prefer to apply online or in person. Understanding each step can help you navigate the process with confidence and clarity. This structured approach ensures you know what to expect.

Pre-qualification vs. Pre-approval

Before a full application, consider pre-qualification or pre-approval. Pre-qualification gives you an estimate of what you might be approved for, often with a soft credit check that doesn’t impact your score. Pre-approval is a more definitive offer, based on a hard credit pull, and provides a concrete loan amount and interest rate.

Pro tips from us: Aim for pre-approval if possible. This transforms you into a cash buyer at the dealership, giving you stronger negotiation power on the vehicle’s price, rather than just focusing on the monthly payment. Having a pre-approval from Umpqua in hand means you already know your financing terms before you even step onto the lot.

The Application Submission

You can typically apply for an Umpqua auto loan through their online portal, which offers convenience and speed. Alternatively, visiting an Umpqua Bank branch allows you to speak directly with a loan officer. This can be beneficial if you have specific questions or prefer a more personal interaction.

When applying, be prepared to provide all the documentation you gathered earlier. Accuracy and completeness are key to a quick review process. Don’t rush through the forms; double-check all your entries to avoid any potential delays.

Documentation Submission and Review

After submitting your initial application, Umpqua Bank will review your information, including your credit report and financial history. They may request additional documents to verify your income or other details. Responding promptly to these requests can expedite the approval process for your Umpqua car loan.

The loan officers are there to help, so if you’re unsure about any requested item, don’t hesitate to ask for clarification. Their goal is to help you get approved for your vehicle financing.

Loan Decision & Funding

Once your application is approved, Umpqua Bank will present you with the final loan terms, including your interest rate, loan amount, and repayment schedule. Carefully review these terms before signing. Once all documents are signed, the funds are typically disbursed directly to the dealership or, in the case of refinancing, to your previous lender.

This final stage is where your preparation pays off, as you lock in the terms of your Umpqua auto loan and move closer to driving your new car.

Understanding Umpqua Car Loan Interest Rates and Terms

The cost of your Umpqua car loan isn’t just the price of the car; it’s also heavily influenced by the interest rate and loan terms you secure. These two factors determine your monthly payment and the total amount you’ll pay over the life of the loan. A clear understanding of them is essential for smart car financing.

Factors Affecting Interest Rates

Several elements contribute to the interest rate Umpqua Bank offers you:

- Credit Score: As discussed, a higher credit score generally leads to lower rates because you represent less risk to the lender.

- Loan Term: Shorter loan terms often come with slightly lower interest rates, as the bank’s risk exposure is reduced over a shorter period.

- Loan Amount: The total amount you borrow can also play a role, with very small or very large loans sometimes having different rate structures.

- Market Conditions: Prevailing economic conditions and the federal interest rate environment significantly impact all lending rates.

- New vs. Used Vehicle: Loans for new cars often have lower interest rates than those for used cars, due to the new car’s predictable value and lower risk of mechanical issues.

Based on my experience, even a small difference in the interest rate can add up to hundreds or thousands of dollars over the loan’s duration. Always compare rates from different lenders, and ensure you understand how each factor impacts your specific offer.

Fixed vs. Variable Rates

Most Umpqua car loans are offered with a fixed interest rate. This means your interest rate remains the same throughout the entire loan term, providing predictable monthly payments. This stability makes budgeting easier and protects you from potential rate increases.

Variable rates, while less common for auto loans, fluctuate with market conditions. While they might start lower, they can increase over time, making your monthly payments unpredictable. For most car buyers, a fixed-rate Umpqua auto loan offers greater peace of mind.

Navigating Loan Terms

Loan terms refer to the length of time you have to repay your loan, typically expressed in months (e.g., 36, 48, 60, 72, or 84 months).

- Shorter Terms: A shorter loan term (e.g., 36-48 months) means higher monthly payments but less interest paid overall. You pay off the loan faster and save money in the long run. This is often ideal if your budget can accommodate the higher payments.

- Longer Terms: A longer loan term (e.g., 60-84 months) results in lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest over the life of the loan, and your car’s value may depreciate faster than you pay it off, leaving you "upside down."

Pro tips from us: Finding the right balance between a manageable monthly payment and the total interest paid is key. Don’t automatically opt for the longest term just to get the lowest payment. Consider your budget carefully and weigh the long-term cost implications.

Refinancing Your Existing Auto Loan with Umpqua

Perhaps you already have an auto loan but are looking for better terms. Refinancing your existing vehicle financing with Umpqua Bank could be a smart financial move. This involves taking out a new loan to pay off your current one, ideally with more favorable conditions.

When to Consider Refinancing

Several situations make refinancing an attractive option:

- Lower Interest Rates: If market interest rates have dropped since you took out your original loan, or if your credit score has significantly improved, you might qualify for a much lower rate.

- Improved Credit Score: A substantial improvement in your credit history means you’re now seen as a less risky borrower, potentially unlocking better rates than your initial loan.

- Desire for Lower Monthly Payments: Refinancing to a longer loan term can reduce your monthly payment, freeing up cash flow, though it may increase total interest paid.

- Change Loan Terms: You might want to switch from a variable-rate loan to a fixed-rate loan, or adjust the length of your repayment period to better suit your current financial situation.

Based on my experience, many people overlook the opportunity to refinance, assuming their current loan is set in stone. Regularly reviewing your loan terms, especially if your financial health has improved, can lead to significant savings.

The Refinancing Process

The process for refinancing an Umpqua auto loan is similar to applying for a new one. You’ll submit an application, provide financial documentation, and Umpqua will review your creditworthiness. They will also need details about your current loan and vehicle.

Once approved, Umpqua will pay off your old loan, and you’ll begin making payments to Umpqua Bank under the new, hopefully improved, terms. It’s a relatively seamless transition that can yield substantial financial benefits.

Beyond the Loan: Maximizing Your Umpqua Auto Financing Experience

Securing your Umpqua car loan is just the beginning. Maximizing your overall financing experience involves understanding the tools available and how to best manage your loan. This proactive approach ensures a smooth ownership journey.

Utilizing Auto Loan Calculators

Before, during, and after your application, make extensive use of online auto loan calculators. These tools allow you to input different loan amounts, interest rates, and terms to see how they impact your estimated monthly payment and total interest paid. This empowers you to make informed decisions and budget effectively.

Pro tips from us: Don’t just look at the monthly payment. Use calculators to compare the total cost of different loan scenarios, including various down payments and terms. This holistic view helps you truly understand the financial commitment of your Umpqua vehicle financing.

Convenient Payment Options

Umpqua Bank typically offers various convenient ways to make your car loan payments. These often include:

- Automatic Payments: Setting up auto-pay from your Umpqua account or another bank ensures you never miss a payment, which is excellent for your credit score.

- Online Banking Portal: Managing your loan, viewing statements, and making one-time payments through Umpqua’s secure online platform.

- In-Branch Payments: If you prefer, you can always make payments at any Umpqua Bank branch.

Ensuring you have a reliable payment method in place prevents late fees and helps maintain a good payment history, a cornerstone of strong credit.

Exceptional Customer Service

One of the defining characteristics of Umpqua Bank is its commitment to customer service. Should you have questions about your Umpqua car loan, need assistance with payments, or want to explore other financial products, their team is usually readily available. This personal connection is a key advantage of banking with a community-focused institution.

Common Mistakes to Avoid When Applying for an Umpqua Car Loan

Even with all the right information, some common pitfalls can derail your Umpqua car loan journey. Being aware of these can help you sidestep potential problems and ensure a smoother process. Avoiding these mistakes is crucial for successful auto financing.

- Not Checking Your Credit Score: As mentioned, ignoring your credit report can lead to unpleasant surprises or missed opportunities for better rates. Always know where you stand.

- Applying to Too Many Lenders at Once: While it’s wise to compare offers, applying to numerous lenders within a short period can negatively impact your credit score. Each "hard inquiry" can slightly lower your score. Focus on a few reputable lenders like Umpqua.

- Not Budgeting Properly: Underestimating the total cost of car ownership (including insurance, fuel, and maintenance) can lead to financial strain. Always create a comprehensive budget.

- Not Understanding All Terms and Conditions: Don’t just sign on the dotted line. Read every clause of your Umpqua auto loan agreement. Ask questions about anything you don’t understand, especially regarding fees, prepayment penalties, or specific conditions.

- Focusing Only on Monthly Payments: Dealerships often try to negotiate based solely on the monthly payment. This can hide a higher car price or unfavorable loan terms. Always negotiate the total price of the car first, then discuss the financing.

From my observations, one of the biggest pitfalls is rushing the process. Taking your time, doing your research, and understanding every aspect of your Umpqua car loan will serve you well in the long run.

Pro Tips for a Smooth Umpqua Car Loan Journey

To truly excel in your Umpqua car loan experience and secure the best possible deal, consider these expert recommendations. These tips go beyond the basics, offering insights that can make a real difference in your vehicle financing.

- Get Pre-approved: We cannot stress this enough. Having a pre-approval from Umpqua Bank before you visit the dealership gives you significant leverage. It establishes your financing power and allows you to focus purely on negotiating the car’s price.

- Negotiate the Car Price, Not Just the Monthly Payment: This is a crucial distinction. Always negotiate the total purchase price of the vehicle first, separate from the financing. A lower car price directly translates to a smaller loan amount, which means less interest paid overall.

- Read the Fine Print Thoroughly: Before signing any documents for your Umpqua auto loan, read every word. Pay attention to the interest rate, APR (Annual Percentage Rate, which includes fees), loan term, any prepayment penalties, and late payment fees. If something isn’t clear, ask for clarification.

- Be Wary of Add-ons: Dealerships often offer additional products like GAP insurance, extended warranties, and service contracts. While some may be valuable, others might be overpriced or unnecessary. Research these options independently and understand their costs before adding them to your Umpqua vehicle financing. Sometimes, you can find better deals for these services elsewhere.

- Consider Auto Loan Protection: Umpqua Bank may offer options for Payment Protection or Debt Protection. Understand what these cover and whether they align with your personal financial risk management strategy. They can provide peace of mind in unforeseen circumstances.

- Maintain a Good Relationship with Umpqua: By establishing a positive banking relationship, you may find future financial services, including subsequent auto loans or other lines of credit, even smoother. Being a valued customer often comes with its own rewards.

Conclusion: Driving Forward with Confidence and Your Umpqua Car Loan

Securing an Umpqua car loan can be a straightforward and rewarding experience when approached with knowledge and preparation. By understanding the ins and outs of credit scores, budgeting, the application process, and loan terms, you empower yourself to make intelligent financial decisions. Umpqua Bank’s commitment to personalized service and competitive offerings makes them a strong contender for your auto financing needs.

Remember, the goal is not just to get a car, but to get a car on terms that genuinely work for your financial well-being. By leveraging the insights provided in this comprehensive guide, you’re well-equipped to navigate the complexities of car financing with confidence. Whether you’re purchasing a new vehicle, buying a used one, or looking to refinance, an Umpqua auto loan could be the key to unlocking your next adventure on the road.

Ready to take the next step towards your dream car? Explore Umpqua Bank’s car loan options today and experience their personalized approach to vehicle financing. Your journey starts now.