Navigating Your Finances: What ‘Pat Has A Savings Account And A Car Loan’ Really Means

Navigating Your Finances: What ‘Pat Has A Savings Account And A Car Loan’ Really Means Carloan.Guidemechanic.com

In the intricate world of personal finance, understanding your own situation is the first step towards achieving financial freedom. Many individuals find themselves in a common scenario, much like "Pat Has A Savings Account And A Car Loan." On the surface, this might seem contradictory – holding savings while simultaneously owing money on a car. However, this dual financial state is far more common and, often, more strategic than it appears.

This comprehensive guide will delve deep into Pat’s financial situation, exploring the nuances, the strategic advantages, the potential pitfalls, and most importantly, the actionable steps Pat – and you – can take to optimize this position. Our goal is to provide a pillar content piece that empowers you with the knowledge to make informed decisions, ensuring your money works harder for you.

Navigating Your Finances: What ‘Pat Has A Savings Account And A Car Loan’ Really Means

Understanding Pat’s Financial Dualism: Savings and Debt

When we say "Pat Has A Savings Account And A Car Loan," we’re describing a financial snapshot where Pat possesses liquid assets in a savings account while also carrying a liability in the form of an auto loan. At first glance, some might wonder why Pat doesn’t simply use the savings to pay off the car loan immediately. However, this perspective often overlooks the strategic reasoning and financial wisdom behind such a choice.

This isn’t necessarily a sign of poor financial management. In many cases, it reflects a deliberate strategy to balance immediate liquidity with long-term financial goals. It’s about understanding the different roles savings and debt play in one’s overall financial health.

The Strategic Reasons Behind Pat’s Choice

There are several compelling reasons why an individual, like Pat, might choose to maintain a savings account even while carrying a car loan. These reasons often revolve around risk management, financial flexibility, and maximizing overall financial well-being.

Building a Robust Emergency Fund: The Bedrock of Financial Security

Based on my experience in financial counseling, one of the primary drivers for maintaining a savings account, even with debt, is the necessity of an emergency fund. Life is unpredictable, and unexpected expenses — a medical emergency, a sudden job loss, or home repairs — can arise at any moment.

Having a readily accessible emergency fund acts as a crucial safety net, preventing you from falling into deeper debt or selling off assets during a crisis. It provides peace of mind and financial resilience. For many, this fund is non-negotiable, regardless of other debts.

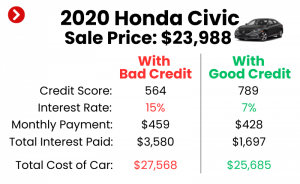

Low-Interest Debt: When Debt Isn’t Always the Enemy

Not all debt is created equal. Car loans, especially for individuals with good credit, often come with relatively low interest rates. If the interest rate on Pat’s car loan is low (e.g., 2-4%), and Pat’s savings are earning some interest or are earmarked for higher-return investments, then paying off the low-interest debt might not be the most financially optimal move.

The concept here is known as opportunity cost. If the money in savings could generate a higher return elsewhere, or if its primary role is to protect against high-interest emergency debt, then maintaining both makes strategic sense. We’ll delve deeper into this calculation shortly.

Saving for Future Goals: Beyond the Immediate

Pat’s savings might not just be an emergency fund; it could be designated for other significant life events or goals. Perhaps Pat is saving for a down payment on a house, a child’s education, or a long-term investment. Diverting these funds to pay off a car loan, even if it saves some interest, could derail more substantial, long-term aspirations.

This foresight is a hallmark of good financial planning. It’s about balancing immediate debt reduction with the pursuit of larger financial milestones.

Psychological Comfort: The Peace of Mind of Liquidity

Beyond the purely mathematical calculations, there’s a significant psychological benefit to having liquid savings. Knowing that you have cash readily available can reduce stress and anxiety related to financial instability. This sense of security can be invaluable, allowing Pat to make calmer, more rational financial decisions rather than being driven by panic.

Common mistakes to avoid are underestimating the psychological impact of having a buffer. Draining all savings to pay off a loan can leave one feeling exposed and vulnerable.

The Advantages of Pat’s Balanced Approach

Embracing this dual strategy offers several distinct advantages that contribute to overall financial health and security. It’s not just about managing money; it’s about building a resilient financial life.

Enhanced Financial Resilience and Preparedness

As discussed, an emergency fund is paramount. By keeping savings separate from the car loan, Pat ensures immediate access to funds for unforeseen circumstances. This resilience prevents the need to take on new, potentially high-interest debt (like credit card debt) when an emergency strikes.

It’s a proactive defense mechanism against financial shocks. Without this buffer, a minor setback could quickly escalate into a major financial crisis.

Flexibility and Liquidity

Having cash in a savings account provides unmatched flexibility. Pat can access these funds quickly without penalties, unlike certain investments or retirement accounts. This liquidity is crucial for seizing unexpected opportunities or responding to urgent needs.

For instance, if a limited-time investment opportunity arises or an unexpected expense requires immediate attention, Pat’s liquid savings are ready. Without them, Pat might miss out or face difficult choices.

Potential for Investment Growth (If Done Right)

Pro tips from us: If Pat’s car loan interest rate is low, and Pat is disciplined, a portion of the savings beyond the emergency fund could potentially be invested in instruments that offer a higher return. This strategy, known as "arbitrage," means making money on the difference between borrowing at a low rate and investing at a higher one.

However, this requires careful consideration of risk and market conditions. It’s not for everyone, but it highlights the potential for wealth accumulation even with debt.

Potential Pitfalls and Common Mistakes to Avoid

While maintaining both savings and a car loan can be strategic, it’s not without its potential drawbacks and common missteps. Understanding these can help Pat – and you – navigate this financial landscape more effectively.

Opportunity Cost of Idle Savings

One significant pitfall is the opportunity cost of holding too much money in a low-interest savings account when it could be used to pay off higher-interest debt. If Pat’s car loan has a high interest rate (e.g., 7% or more), and the savings account is only earning 0.5%, Pat is effectively losing money by not paying down the debt.

This is where the math becomes critical. Every dollar sitting idle in a low-yield account, while high-interest debt accrues, is a missed opportunity to save money on interest payments.

High-Interest Debt vs. Low-Interest Savings

This is a critical distinction. If Pat’s car loan is considered "high-interest debt," then prioritizing its repayment over maintaining excess savings (beyond an adequate emergency fund) is usually the smarter move. Conversely, if the car loan is "low-interest debt," the decision becomes more nuanced.

Pro Tip: Always compare the interest rate on your debt with the interest rate your savings are earning. If your debt rate significantly exceeds your savings rate, you’re likely better off paying down the debt first.

Lack of a Clear Strategy

A common mistake is simply having both a savings account and a car loan without a deliberate plan. This can lead to inefficient use of funds. Without a clear strategy, Pat might be accumulating savings without purpose while simultaneously paying unnecessary interest.

Effective financial management requires intentionality. Every dollar should have a job, whether it’s for emergencies, debt repayment, or future investments.

Ignoring Debt Acceleration

While maintaining savings, some individuals overlook the benefits of accelerating debt repayment. Even low-interest debt can add up over time. If Pat consistently makes only minimum payments, the total interest paid over the life of the loan can be substantial.

Ignoring the possibility of making extra payments when financially feasible means prolonging the debt burden unnecessarily. This is where a balanced approach is key – not just having savings, but actively deploying them.

Actionable Strategies for Pat (and You) to Optimize This Situation

Now that we’ve explored the "why" and "what," let’s focus on the "how." Here are actionable strategies for anyone in Pat’s situation to optimize their financial position, turning a seemingly contradictory state into a powerful financial advantage.

Step 1: Assess Your Current Financial Landscape with Precision

The first crucial step is to gain absolute clarity on your current financial standing. This means more than just knowing you have savings and a loan; it means understanding the specifics of each.

- Detailed Analysis of Your Savings Account:

- What is the exact balance?

- What is the annual percentage yield (APY) it’s earning?

- How quickly and easily can you access these funds without penalty?

- Is it designated as an emergency fund, or for another specific goal?

- Detailed Analysis of Your Car Loan:

- What is the exact outstanding balance?

- What is the interest rate (APR)?

- What are the remaining terms (number of payments, end date)?

- Are there any prepayment penalties? (These are rare for car loans but worth checking).

Understanding these precise figures is the foundation for making informed decisions. Without them, you’re essentially flying blind.

Step 2: Define Your Emergency Fund Threshold Clearly

Based on my experience, a fully funded emergency account is non-negotiable for true financial security. Before considering any debt repayment strategies, ensure this vital safety net is robust.

- How Much Is Enough? Generally, financial experts recommend 3 to 6 months’ worth of essential living expenses. For those with less job security or dependents, 6-12 months might be more appropriate.

- Where Should It Be Kept? Your emergency fund should be in a highly liquid, easily accessible account, like a high-yield savings account (HYSA). While the returns might not be stellar, the priority is accessibility and safety, not aggressive growth.

- Pro Tip: Don’t confuse your emergency fund with other savings goals. It has one job: to protect you from unexpected financial shocks.

Step 3: Evaluate Your Car Loan for Optimization Opportunities

Once your emergency fund is solid, turn your attention to the car loan itself. There might be opportunities to reduce its burden.

- Is Refinancing an Option? If your credit score has improved since you first took out the loan, or if interest rates have dropped, refinancing could significantly lower your interest rate and monthly payments. This is particularly effective for high-interest car loans.

- Accelerated Payments vs. Minimum Payments: If your loan’s interest rate is higher than what your non-emergency savings are earning, consider making extra payments. Even a small additional amount each month can reduce the principal faster, saving you substantial interest over the life of the loan.

- Common Mistakes to Avoid: Don’t refinance without comparing total costs and new terms carefully. Sometimes, a lower monthly payment can mean a longer loan term and more interest paid overall. Always look at the total cost.

Step 4: The Debt vs. Savings Dilemma: Where to Prioritize?

This is the core decision point for Pat. With an emergency fund in place, how should any additional surplus savings be allocated?

- The "Interest Rate Rule" Explained:

- If your car loan interest rate is higher than the return you can reasonably expect from your savings (or other low-risk investments), prioritize paying down the car loan. The guaranteed return from avoiding high interest is often the safest "investment."

- If your car loan interest rate is lower than the return you can reasonably expect from other investments (e.g., a diversified stock market portfolio), then you might consider investing your surplus savings rather than accelerating loan payments. This strategy, however, comes with investment risk.

- Debt Snowball vs. Debt Avalanche for Car Loans:

- Debt Avalanche: Mathematically, this is superior. You pay off the debt with the highest interest rate first, saving the most money. For a car loan, if it’s your highest interest debt (which is unlikely if you have credit card debt, but possible), this is the method to use.

- Debt Snowball: This method prioritizes paying off the smallest debt first, regardless of interest rate. It provides psychological wins, building momentum. While less mathematically efficient, it can be very effective for those who need motivation.

Pro Tip: Don’t forget the psychological aspect. While the debt avalanche is mathematically superior, the debt snowball’s quick wins can be powerful motivators for some individuals. Choose the method that you are most likely to stick with.

Step 5: Beyond the Car Loan: Future Financial Planning

Once the car loan is under control, or if its terms are favorable, Pat’s attention should shift to broader financial goals. This is where true wealth building begins.

- Investing Surplus Savings: After your emergency fund is secure and high-interest debts are tackled, consider investing your additional savings. This could be in retirement accounts (401k, IRA), brokerage accounts, or other long-term growth vehicles.

- Retirement Planning: Ensure you are contributing enough to your retirement accounts, especially if your employer offers a matching contribution (which is essentially free money!).

- Other Debt Considerations: If Pat has other debts (e.g., student loans, mortgage), integrate them into the overall strategy. The same interest rate rule applies: tackle the highest interest debts first. For more strategies on managing multiple debts, you might find our article on helpful.

Step 6: Maintain Vigilance and Adapt

Financial planning is not a one-time event; it’s an ongoing process. Life changes, and so should your financial strategy.

- Regular Financial Reviews: Set aside time quarterly or semi-annually to review your savings balances, debt outstanding, interest rates, and overall budget.

- Adjusting to Life Changes: A new job, a raise, a new family member, or unexpected expenses should all trigger a review of your financial plan. Be flexible and willing to adapt.

- External Link: For more general guidance on personal finance, resources like the Consumer Financial Protection Bureau (CFPB) offer excellent, unbiased advice on managing money and debt. You can find valuable information on their official website.

Real-World Scenarios and Case Studies (Conceptual)

Let’s briefly consider two hypothetical "Pats" to illustrate these points:

- Pat A: The High-Interest Car Loan: Pat A has a car loan at 8% APR and a savings account earning 0.75%. In this scenario, Pat A should prioritize paying down the car loan aggressively after securing an emergency fund. The 7.25% difference in interest is a significant drain.

- Pat B: The Low-Interest Car Loan: Pat B has a car loan at 2.5% APR and is contributing to a retirement account earning an average of 7% historically. Pat B’s emergency fund is robust. Here, it makes more sense for Pat B to continue investing in the retirement account rather than prepaying the low-interest car loan, as the potential investment returns outweigh the interest saved on the car.

These examples highlight why a blanket "pay off all debt" approach isn’t always the best advice. Nuance and specific numbers matter.

Conclusion: Mastering the Art of Financial Balance

The situation where "Pat Has A Savings Account And A Car Loan" is a microcosm of modern personal finance. It underscores the delicate balance between liquidity, debt management, and long-term financial growth. By understanding the strategic reasons behind this position, acknowledging potential pitfalls, and implementing a clear, actionable plan, Pat – and indeed, anyone in a similar situation – can transform this dual state into a powerful foundation for financial success.

Remember, the goal isn’t just to eliminate debt or accumulate savings; it’s to build a resilient, flexible, and prosperous financial future. Through careful assessment, strategic planning, and ongoing vigilance, you can master the art of financial balance and achieve your unique financial aspirations. Start by reviewing your own numbers today, and take the first step towards a more optimized financial journey.