Navigating Your First Car Loan with No Credit: A Comprehensive Guide for First-Time Buyers

Navigating Your First Car Loan with No Credit: A Comprehensive Guide for First-Time Buyers Carloan.Guidemechanic.com

The open road, the smell of a new (or new-to-you) car, and the sheer independence of having your own set of wheels – it’s a dream many first-time car buyers cherish. But for those embarking on this exciting journey without an established credit history, the path to securing a car loan can often feel like navigating a dense fog. You’re eager to make that first big purchase, but lenders seem hesitant without proof of your financial reliability.

Don’t despair! As an expert blogger and professional SEO content writer who has guided countless individuals through this very process, I can tell you this: getting a first time car buyer loan with no credit is absolutely achievable. It requires preparation, understanding, and a strategic approach. This super comprehensive guide is designed to empower you with the knowledge and actionable steps needed to confidently secure your first auto loan, even without a credit score, and set yourself up for future financial success. Let’s unlock the secrets to driving off the lot with confidence!

Navigating Your First Car Loan with No Credit: A Comprehensive Guide for First-Time Buyers

The "No Credit" Conundrum Explained: Why Lenders Hesitate

Before we dive into solutions, it’s crucial to understand the challenge. When we talk about "no credit," we’re not necessarily talking about "bad credit." Bad credit implies a history of missed payments, defaults, or bankruptcies. "No credit," on the other hand, means you simply haven’t had the opportunity to borrow money and prove your repayment habits to financial institutions.

What Exactly is "No Credit"?

Imagine a blank slate. That’s essentially what your credit report looks like without a credit history. You haven’t taken out loans, used credit cards, or had any financial accounts that report to credit bureaus like Experian, Equifax, or TransUnion. This lack of data makes you an unknown entity to lenders.

Why Lenders Care So Much About Credit History

Lenders are in the business of assessing risk. When you apply for a no credit car loan, they want to know how likely you are to repay the money you borrow. Your credit history serves as a financial report card, demonstrating your past behavior with debt.

Without this report card, lenders have no objective way to predict your repayment habits. This uncertainty translates into higher perceived risk for them, making them more cautious about approving your application or offering favorable terms.

The Challenges First-Time Buyers Face

For many young adults, recent graduates, or newcomers to the financial system, a lack of credit history is a common hurdle. You’re caught in a "catch-22": you need credit to get a loan, but you need a loan to build credit. This can feel incredibly frustrating when all you want is reliable transportation.

Based on my experience, the biggest challenge is overcoming this initial skepticism from lenders. They need more than just your word; they need tangible evidence or alternative assurances that you are a responsible borrower.

Preparing for Your First Car Loan Journey: Laying the Foundation

Success in securing a car loan for first time buyers with no credit isn’t about magic; it’s about meticulous preparation. Think of it as building a robust case for why you are a trustworthy borrower.

1. Your Financial Health Check: Know Your Numbers

Before you even look at cars, take a deep dive into your personal finances. This is perhaps the most critical step. Lenders will scrutinize your income and expenses to determine your ability to pay.

- Budgeting is Key: Create a detailed monthly budget. Track all your income sources and every single expense – rent, utilities, food, entertainment, subscriptions, and any existing debt payments. This exercise will reveal how much disposable income you genuinely have available for a car payment.

- Income Stability: Lenders prefer to see consistent, verifiable income. If you have a stable job with a steady paycheck, this is a huge plus. Be prepared to show pay stubs, bank statements, or even employment verification letters.

Pro tip from us: Don’t just estimate your budget. Use a spreadsheet or a budgeting app to get a precise picture. This clarity will not only help you secure a loan but also prevent future financial stress.

2. Knowing Your Limits: Affordability vs. Desired Car

It’s easy to get carried away by the allure of a shiny new vehicle. However, when you’re seeking an auto loan no credit history, practicality should be your guiding star.

- What Can You Truly Afford? Your car payment shouldn’t consume a disproportionate amount of your income. Financial experts often recommend that your total car expenses (payment, insurance, fuel, maintenance) not exceed 10-15% of your gross monthly income.

- Beyond the Payment: Remember, a car loan is just one part of car ownership. Factor in insurance (which can be higher for first-time drivers and those with no credit), fuel, routine maintenance, and potential repairs. These costs add up quickly.

Common mistake to avoid: Many first-time buyers focus solely on the monthly payment, overlooking the total cost of ownership. A lower monthly payment spread over a longer term often means paying significantly more in interest over the life of the loan.

3. Down Payment Power: Your Secret Weapon

For someone looking to get a buying a car with no credit, a substantial down payment is one of the most powerful tools at your disposal.

- Reducing Lender Risk: A larger down payment reduces the amount you need to borrow, which in turn lowers the lender’s risk. If you default, they have less to recover.

- Lower Monthly Payments: It directly translates to lower monthly loan payments, making the loan more affordable and increasing your chances of approval.

- Better Interest Rates: Lenders are often willing to offer slightly better interest rates when they see you have significant equity in the vehicle from day one.

Aim for at least 10-20% of the car’s purchase price as a down payment. The more you can put down, the stronger your application becomes.

4. Documents You’ll Need: Be Prepared

Gathering your documents in advance demonstrates your seriousness and readiness. This can expedite the application process significantly.

Expect to provide:

- Proof of Identity: Driver’s license, state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms, tax returns, bank statements showing direct deposits.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- References: Sometimes lenders will ask for personal references (not always credit references, but character references).

- Insurance Quote: Lenders will require proof of full coverage insurance before you drive off the lot. Get quotes beforehand to factor this into your budget.

Strategies for Securing a Car Loan with No Credit: Your Pathways to Approval

With your preparations complete, it’s time to explore the specific avenues available for getting a car loan without credit history. There isn’t a one-size-fits-all solution, but rather a combination of approaches that can increase your chances.

1. The Power of a Substantial Down Payment

As mentioned, a significant down payment acts as collateral and a strong indicator of your financial commitment. It directly mitigates the risk for the lender.

- How it Works: By putting down 20% or more, you reduce the loan amount, making the monthly payments more manageable and the overall loan less risky for the lender. This can sometimes compensate for the lack of credit history.

- Strategic Advantage: It shows lenders you have savings and are serious about your purchase, signaling financial responsibility even without a credit score.

Based on my experience, a strong down payment is often the single most impactful factor for a first-time buyer with no credit to get approved for an initial loan.

2. The Cosigner Advantage: Leveraging Trusted Relationships

Bringing a cosigner onto your loan application can dramatically improve your chances of approval and potentially secure a better interest rate.

- Who Can Be a Cosigner? A cosigner is typically a parent, guardian, or another close family member or friend with excellent credit. They agree to be legally responsible for the loan if you fail to make payments.

- Responsibilities and Risks: The cosigner’s credit score is used in the application, and they are equally liable for the debt. If you miss payments, their credit score will also be negatively impacted, and they could be pursued for repayment.

- Benefits for the No-Credit Buyer: A cosigner essentially lends their good credit to your application, reducing the lender’s risk. This can open doors to loans you wouldn’t qualify for alone, often with more favorable interest rates. It also provides an excellent opportunity for you to build your own credit history as you make on-time payments.

Pro tip from us: Ensure both you and your potential cosigner fully understand the commitment and risks involved. Open communication is paramount.

3. Dealership Financing: Exploring "Buy Here, Pay Here" Options

Many dealerships offer their own financing, especially those specializing in used cars. These are often referred to as "Buy Here, Pay Here" (BHPH) dealerships.

- Pros: BHPH dealerships are typically more lenient on credit requirements, often approving individuals with no credit or even bad credit. The approval process can be quicker, as they handle both the sale and the financing in-house.

- Cons: The trade-off often comes in the form of significantly higher interest rates compared to traditional bank loans. The car selection might be limited, and the terms can be less flexible. Crucially, some BHPH dealers do not report payments to credit bureaus, which means while you’re paying off your loan, you might not be building your credit history effectively.

Common mistake to avoid: Always ask if the dealership reports your payments to all three major credit bureaus. If they don’t, this loan won’t help you establish the credit history you need for future borrowing.

4. Credit Unions and Community Banks: A More Personal Approach

Don’t overlook local credit unions and smaller community banks. These institutions often operate differently from large national banks.

- Flexibility: Credit unions are member-owned and often have more flexible lending criteria. They may be more willing to look beyond a lack of credit history if you have a stable income, a good down payment, and can demonstrate other signs of financial responsibility.

- Relationship-Based Lending: If you’re already a member or open an account, they may take your overall financial relationship into account, rather than relying solely on a credit score.

It’s always worth starting a conversation with your local credit union to see what options they might offer for a first time car buyer loan no credit.

5. Building Credit Before Applying (A Long-Term Strategy)

While you might be eager to get a car now, taking a few months to proactively build some credit can significantly improve your loan prospects and secure better terms.

- Secured Credit Cards: These cards require a cash deposit, which acts as your credit limit. Using it responsibly and paying on time demonstrates creditworthiness.

- Credit Builder Loans: Offered by some credit unions or community banks, these loans put the money into a locked savings account, and you make payments over time. Once paid off, you get the money, and your payment history is reported.

- Authorized User Status: If a trusted family member with excellent credit adds you as an authorized user on their credit card, their positive payment history can sometimes reflect on your credit report. Just ensure they are responsible with their credit.

For more details on building your credit score from scratch, check out our guide on .

Understanding Loan Terms and Avoiding Pitfalls

Securing a loan is only half the battle; understanding its terms and avoiding common mistakes is crucial for a positive experience and future financial health.

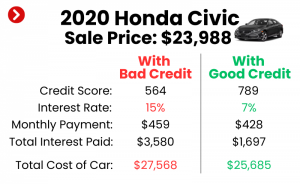

1. Interest Rates: Why They’re Higher for No Credit

When you have no credit history, lenders perceive you as a higher risk. This higher risk translates into higher interest rates on your loan.

- The Cost of Risk: A higher Annual Percentage Rate (APR) means you’ll pay more in interest over the life of the loan. While this is often unavoidable for first-time buyers with no credit, it underscores the importance of a down payment and shopping around.

- Impact on Total Cost: Even a few percentage points difference in APR can add hundreds, if not thousands, to the total cost of your car over several years.

Always compare the APRs offered by different lenders, not just the monthly payment.

2. Loan Term: Shorter vs. Longer

The loan term is the length of time you have to repay the loan.

- Shorter Terms (e.g., 36-48 months): These typically come with higher monthly payments but lower overall interest paid. They help you build equity faster and get out of debt sooner.

- Longer Terms (e.g., 60-72 months): These offer lower monthly payments, making them seem more affordable. However, you’ll pay significantly more in interest over time, and you risk owing more on the car than it’s worth (being "upside down" or "underwater") as it depreciates.

Based on my experience, for a first time car buyer loan no credit, aim for the shortest term you can comfortably afford to minimize interest costs and build equity quicker.

3. Total Cost of Ownership: Beyond the Monthly Payment

As mentioned earlier, a car loan payment is just one piece of the financial puzzle.

- Insurance: Get multiple quotes. Insurance for new drivers or those with no credit can be surprisingly expensive.

- Fuel & Maintenance: These are ongoing costs that fluctuate.

- Registration & Taxes: Don’t forget these upfront or annual fees.

Pro tip from us: Use an online calculator to estimate the total monthly cost of a car, including all these factors, before committing to a purchase. If you’re unsure about budgeting for a car, our comprehensive article on can provide invaluable insights.

4. Common Mistakes to Avoid

- Buying More Car Than You Can Afford: This is the most common pitfall. Stick to your budget, even if a more expensive car seems tempting. An unaffordable loan leads to stress and potential default.

- Ignoring the APR: Focus on the total interest you’ll pay, not just the monthly payment. A low monthly payment over a long term can hide a very expensive loan.

- Not Shopping Around: Don’t take the first offer you get. Apply to multiple lenders (credit unions, banks, dealerships) within a short window (typically 14-45 days) so it counts as a single inquiry on your credit report.

- Falling for "Guaranteed Approval" Scams: While some lenders are more lenient, truly "guaranteed approval" often comes with predatory terms, sky-high interest rates, or hidden fees. Always read the fine print.

- Not Checking If Payments Are Reported: This is critical for building credit. Ensure your lender reports your on-time payments to all three major credit bureaus. If they don’t, your efforts to build credit will be in vain.

Your First Car Loan as a Credit-Building Tool: Paving the Way for Your Future

The journey to securing a first time car buyer loan with no credit isn’t just about getting a car; it’s a golden opportunity to establish a strong financial foundation.

How On-Time Payments Build a Positive Credit History

Every single on-time payment you make on your auto loan is a positive mark on your credit report. Lenders will see that you are responsible, reliable, and capable of managing debt.

- Payment History: This is the most significant factor in calculating your credit score (accounting for 35%). Consistently paying on time will rapidly improve your score.

- Credit Mix: An auto loan diversifies your credit mix, showing you can handle different types of credit (installment loans vs. revolving credit like credit cards).

The Importance of Consistency

Building good credit is a marathon, not a sprint. Consistency is key. Make every payment on time, every month, without fail. Set up automatic payments if possible to avoid accidental misses.

Future Benefits of a Good Credit Score

Successfully managing your first car loan will open doors to better financial opportunities in the future:

- Lower Interest Rates: For future car loans, mortgages, and other loans.

- Easier Approvals: For credit cards, apartments, and even some jobs.

- Reduced Insurance Premiums: In many states, a good credit score can positively impact your car insurance rates.

This build credit car loan experience is invaluable. It’s your first major step towards financial independence and a strong credit profile.

Conclusion: Drive Off with Confidence and a Stronger Financial Future

Securing your first time car buyer loan with no credit might seem like a daunting task, but as we’ve explored, it’s entirely achievable with the right strategy and preparation. By understanding the lender’s perspective, diligently preparing your finances, exploring various loan options, and being smart about loan terms, you can confidently drive off the lot in your new vehicle.

Remember, this isn’t just about getting a car; it’s about making a smart financial decision that will serve as a powerful tool for building your credit history. Each on-time payment is an investment in your financial future, paving the way for better interest rates and easier approvals down the road.

Don’t let a blank credit slate deter you. Take the time to prepare, shop smart, ask questions, and choose a loan that fits your budget and helps you build a solid financial foundation. Your journey to car ownership and a robust credit score starts now. Good luck, and happy driving!