Navigating Your Future: The Ultimate Guide to Career Training Student Loans

Navigating Your Future: The Ultimate Guide to Career Training Student Loans Carloan.Guidemechanic.com

Embarking on a new career path through specialized training, vocational programs, or trade schools offers a powerful avenue to gain in-demand skills and enter the workforce quickly. Unlike traditional four-year degrees, these programs often provide a focused, hands-on education designed to prepare you for a specific profession. However, even with their generally lower costs compared to university degrees, funding your career training can still be a significant hurdle. This is where career training student loans come into play, offering a vital financial bridge to your professional aspirations.

This comprehensive guide will demystify the world of student loans for career training. We’ll explore various funding options, delve into the application process, and equip you with the knowledge to make smart borrowing decisions. Our goal is to empower you to pursue your educational goals without getting bogged down by financial stress, ensuring you understand every facet of securing the funds you need for a brighter future.

Navigating Your Future: The Ultimate Guide to Career Training Student Loans

Understanding Career Training and Its Value in Today’s Job Market

Career training encompasses a wide array of educational paths designed to teach specific skills for a particular job or industry. This includes vocational schools, trade schools, technical colleges, and specialized certification programs. These institutions focus on practical, hands-on learning, preparing students for fields like healthcare support, skilled trades (welding, electrical, plumbing), IT support, culinary arts, cosmetology, and much more.

The value of investing in career training is increasingly evident in today’s dynamic job market. Many industries face significant demand for skilled professionals, often with a shortage of qualified candidates. Career training programs offer a faster, more direct route to employment compared to traditional university degrees. They typically involve shorter program durations, which translates to less time out of the workforce and a quicker return on your educational investment.

Moreover, these programs are often tailored to current industry needs, ensuring that graduates possess relevant, up-to-date skills. This practical focus can lead to higher earning potential and greater job security in specialized fields. For many, career training represents a strategic move towards a fulfilling and financially stable career, making the initial investment in education a wise decision.

The Landscape of Career Training Student Loans: Federal vs. Private

When considering student loans for your career training, it’s crucial to understand the two primary categories available: federal student loans and private student loans. Each type comes with distinct eligibility requirements, interest rates, repayment terms, and borrower protections. Making an informed choice between them can significantly impact your financial well-being long after you complete your program.

Federal student loans are funded by the U.S. government and generally offer more favorable terms and borrower protections. These often include fixed interest rates, income-driven repayment plans, and opportunities for deferment or forbearance during difficult financial times. They are typically the first and best option for most students.

Private student loans, on the other hand, are offered by banks, credit unions, and other private lenders. While they can fill funding gaps when federal aid isn’t sufficient, they often come with less flexible repayment options and interest rates that can be higher and sometimes variable. Understanding these differences is the cornerstone of responsible borrowing.

Unlocking Federal Student Aid for Your Career Training

The U.S. federal government provides several forms of financial assistance that can significantly reduce the cost of career training. These programs are designed to be accessible and offer more generous terms than most private options. Always start your financial aid journey here.

Pell Grants: The Non-Repayable Foundation

Pell Grants are perhaps the most well-known form of federal student aid, and for good reason: they do not need to be repaid. These grants are awarded based on financial need, as determined by the Free Application for Federal Student Aid (FAFSA). The maximum award amount changes annually, and eligibility depends on your Expected Family Contribution (EFC), the cost of attendance at your chosen school, and your enrollment status (full-time or part-time).

Many career training programs, including those at vocational and trade schools, are eligible for Pell Grants. This can provide a substantial portion, if not all, of your tuition and fees. It’s a critical first step for anyone seeking to fund their education without accumulating debt.

Federal Direct Loans: The Government’s Lending Hand

If grants don’t cover all your educational expenses, Federal Direct Loans are often the next best option. These loans are offered directly by the U.S. Department of Education and come with several advantages, including fixed interest rates and flexible repayment plans. There are two main types relevant to career training students:

- Direct Subsidized Loans: These are available to undergraduate students with demonstrated financial need. The key benefit is that the U.S. Department of Education pays the interest on these loans while you are enrolled in school at least half-time, during your grace period, and during periods of deferment. This means your loan balance won’t grow while you’re learning.

- Direct Unsubsidized Loans: These are available to undergraduate and graduate students, regardless of financial need. Unlike subsidized loans, interest begins to accrue on unsubsidized loans immediately after disbursement, even while you are in school. You are responsible for paying all the interest, though you can choose to defer interest payments until after you leave school, allowing it to capitalize (be added to your principal balance).

Both subsidized and unsubsidized Direct Loans come with a grace period after you leave school (usually six months) before you must start repayment. They also offer a range of repayment plans, including standard, extended, graduated, and various income-driven repayment (IDR) plans, which can adjust your monthly payments based on your income and family size.

Pro tips from us: Always prioritize accepting any subsidized loans offered before considering unsubsidized loans. The government paying your interest while you’re in school is a huge financial advantage. Ensure your chosen career training program is accredited and eligible for federal financial aid. Not all programs or schools qualify, so verify this early in your research process.

Federal PLUS Loans: For Parents and Graduate Students

While less common for many entry-level career training programs, Federal PLUS Loans can sometimes be an option. These loans are available to parents of dependent undergraduate students (Parent PLUS Loans) and to graduate or professional students (Grad PLUS Loans). For career training, Parent PLUS Loans are more relevant if you are a dependent student whose parents are willing and able to borrow on your behalf.

PLUS Loans can cover the remaining cost of attendance after other financial aid has been exhausted. Eligibility for PLUS Loans generally requires a credit check, and borrowers with an adverse credit history may need an endorser (co-signer) to qualify. Interest rates on PLUS Loans are typically higher than those for Direct Subsidized or Unsubsidized Loans, and interest accrues immediately.

Exploring Private Student Loans for Career Training

When federal student aid, including grants and federal loans, isn’t enough to cover the full cost of your career training, private student loans can bridge the financial gap. These loans are offered by private financial institutions and come with different terms and conditions.

Private lenders include banks, credit unions, and specialized online loan providers. Each lender will have its own eligibility criteria, interest rates, and repayment options. Unlike federal loans, private loans typically require a credit check and often depend on the borrower’s creditworthiness and income. Many students, especially those without an established credit history, will need a co-signer to qualify for a private loan.

Key considerations when looking at private loans include:

- Interest Rates: Private loan interest rates can be fixed or variable. Fixed rates remain the same throughout the life of the loan, offering predictability. Variable rates can fluctuate with market conditions, potentially leading to higher or lower payments over time. Based on my experience, fixed rates are generally preferable for peace of mind, especially in an unpredictable economic climate.

- Repayment Terms: Private lenders offer various repayment schedules, which can range from 5 to 15 years or more. Shorter terms generally mean higher monthly payments but less interest paid overall.

- Credit Score and Co-signers: A good credit score is essential for securing favorable interest rates on private loans. If your credit is limited or poor, a co-signer with strong credit can help you qualify and potentially receive better terms. The co-signer is equally responsible for the loan, so it’s a significant commitment.

Common mistakes to avoid are: Not comparing multiple lenders. Different private lenders offer wildly different rates and terms, so shopping around can save you thousands of dollars over the life of the loan. Another mistake is borrowing more than you absolutely need. Every dollar borrowed must be repaid with interest.

Alternative Funding Options: Beyond Traditional Loans

Before committing to any student loans, it’s wise to explore all non-loan funding options. These alternatives can significantly reduce your borrowing needs, thereby minimizing your future debt burden.

Scholarships and Grants

Just like with traditional degrees, scholarships and grants are available for career training programs. These are "gift aid" that you don’t have to repay. Many are based on academic merit, financial need, specific fields of study, or even demographic factors. Sources include:

- School-specific scholarships: Many vocational and trade schools offer their own scholarships.

- Industry-specific organizations: Associations related to your chosen trade (e.g., welding associations, nursing organizations) often provide funding.

- Local community organizations: Rotary clubs, chambers of commerce, and local foundations frequently offer scholarships to area students.

- Employer-sponsored scholarships: Some companies offer scholarships to students pursuing fields relevant to their business.

Employer Tuition Assistance Programs

If you are currently employed, check with your employer about tuition assistance or reimbursement programs. Many companies are willing to invest in their employees’ education, especially if the training aligns with the company’s needs or your professional development within the organization. This can be a fantastic way to get your career training funded, often without any personal cost.

School Payment Plans

Many career training institutions offer their own interest-free payment plans. These allow you to break down the total cost of tuition into manageable monthly installments over the duration of your program. While this doesn’t reduce the total cost, it can make it more affordable without taking on a loan.

Military Benefits

For veterans, active-duty service members, and their eligible dependents, significant educational benefits are available through programs like the Post-9/11 GI Bill and the Montgomery GI Bill. These benefits can cover tuition, housing, and other costs for approved vocational and technical training programs.

State and Local Workforce Development Programs

Government agencies at the state and local levels often have programs designed to help individuals acquire new skills for in-demand jobs. Programs like the Workforce Innovation and Opportunity Act (WIOA) can provide funding for career training, job search assistance, and other support services. These initiatives aim to boost local economies by equipping residents with valuable skills.

Pro tips from us: Exhaust all grant and scholarship opportunities before even thinking about loans. Every dollar you receive that doesn’t need to be repaid is a dollar you don’t have to worry about in the future. Don’t underestimate the power of local opportunities; they often have less competition.

Navigating the Application Process for Career Training Student Loans

Applying for financial aid and student loans can seem daunting, but breaking it down into manageable steps makes the process much clearer. Diligence and accuracy are key to securing the funding you need.

The Cornerstone: Completing the FAFSA

For federal student aid, the Free Application for Federal Student Aid (FAFSA) is your starting point. This form collects detailed financial information about you (and your parents, if you’re a dependent student) to determine your eligibility for federal grants, scholarships, work-study, and federal student loans. You must complete the FAFSA every year you plan to receive federal aid.

It’s crucial to fill out the FAFSA accurately and submit it as early as possible. Some federal aid is awarded on a first-come, first-served basis, and state aid often has early deadlines. You’ll need your tax returns, W-2s, and other financial records to complete it.

School Accreditation: A Non-Negotiable Requirement

For any federal student aid, your chosen career training program and institution must be accredited by an agency recognized by the U.S. Department of Education. Accreditation ensures that the school meets certain standards of educational quality and integrity. Without it, you will not be eligible for federal grants or loans. Always verify a school’s accreditation status before applying or committing.

Gathering Required Documentation

Whether applying for federal or private loans, you’ll need to provide various documents. For federal aid, this primarily involves the FAFSA and potentially verification documents requested by your school. For private loans, lenders will require proof of income, employment history, tax returns, and possibly bank statements. If you have a co-signer, they will need to provide similar documentation.

Understanding and Comparing Loan Offers

Once you’ve applied, you’ll receive financial aid offers from your school and potential loan offers from private lenders. It’s vital to carefully review each offer. Pay close attention to:

- Loan amounts: How much are you being offered?

- Interest rates: Is it fixed or variable? What is the actual percentage?

- Fees: Are there origination fees or other charges?

- Repayment terms: When does repayment begin? What are the typical monthly payments?

- Borrower protections: What options are available for deferment, forbearance, or income-driven repayment?

Pro tips from us: Never sign a loan agreement without fully understanding all the terms and conditions. If anything is unclear, ask for clarification. Don’t be afraid to compare offers from multiple private lenders; even a small difference in interest rate can save you thousands over the loan’s life.

Responsible Borrowing and Repayment Strategies

Taking on student loan debt is a significant financial commitment. Responsible borrowing means understanding your obligations and having a plan for repayment.

Borrow Only What You Need

This is perhaps the most important advice: only borrow the absolute minimum necessary to cover your educational and essential living expenses. Every dollar you borrow must be repaid with interest, so minimizing your loan amount directly translates to less debt and lower overall costs. Create a detailed budget for your program, including tuition, fees, books, supplies, and living expenses, and borrow only to fill the gap after all other aid is applied.

Understand Your Loan Terms

Before you even start repayment, ensure you thoroughly understand your loan terms. Know your interest rate, whether it’s fixed or variable, when interest starts accruing, and your grace period. Understanding these details will help you prepare for repayment and avoid surprises.

Navigating Repayment Plans

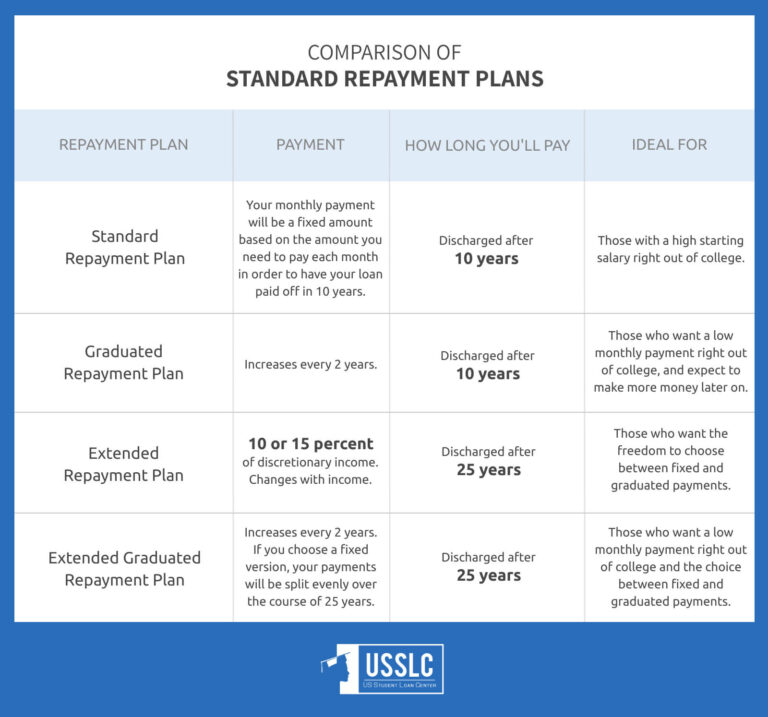

Federal student loans offer a variety of repayment plans to fit different financial situations:

- Standard Repayment Plan: Fixed monthly payments over 10 years.

- Graduated Repayment Plan: Payments start low and increase every two years, still over 10 years.

- Extended Repayment Plan: Lower monthly payments over a longer period (up to 25 years) for borrowers with larger loan balances.

- Income-Driven Repayment (IDR) Plans: Payments are based on your income and family size, typically adjusted annually. These plans can offer significant relief if your income is low after graduation, and some federal IDR plans offer loan forgiveness after 20-25 years of qualifying payments.

Private loans generally have less flexible repayment options, but it’s still worth discussing your situation with your lender if you face financial hardship.

Refinancing and Consolidation

For federal loans, consolidation combines multiple federal loans into one new loan with a single monthly payment and a weighted average interest rate. It can simplify repayment but may extend the loan term.

For private loans, or to combine federal and private loans, refinancing with a new private lender can be an option. This involves taking out a new loan to pay off existing ones, ideally at a lower interest rate or with better terms. Refinancing federal loans into a private loan means losing federal borrower protections, so this decision requires careful consideration.

Based on my experience: If you can afford it, making payments during your grace period or even while in school, particularly on unsubsidized loans, can significantly reduce the total interest paid over the life of the loan. Even small, extra payments can make a big difference.

Avoiding Default

Defaulting on a student loan has severe consequences, including damage to your credit score, wage garnishment, and loss of eligibility for future federal aid. If you anticipate difficulty making payments, contact your loan servicer immediately. They can help you explore options like changing repayment plans, deferment, or forbearance to prevent default. Common mistakes to avoid are: ignoring communications from your loan servicer or assuming your financial problems will just disappear. Proactive communication is always the best approach.

Choosing the Right Career Training Program: A Financial Perspective

The financial implications of your career training extend beyond just securing a loan. Choosing the right program can significantly impact your financial future.

Accreditation Matters for More Than Just Loans

Beyond federal aid eligibility, accreditation also signifies quality education. An accredited program is more likely to be recognized by employers and licensing boards, making your certification or diploma more valuable in the job market.

Research Job Placement Rates

Investigate the job placement rates of graduates from your prospective programs. A high placement rate suggests that the program effectively prepares students for employment and has strong industry connections. This directly impacts your ability to repay your loans.

Understand the Return on Investment (ROI)

Consider the potential earnings in your chosen field versus the cost of your training and loans. A program that costs a significant amount but leads to a low-paying job may not offer a good return on investment. Research typical starting salaries for graduates of your program and weigh that against your total estimated debt.

Pro tips from us: Don’t just look at the advertised cost; dig deeper into all fees, books, and supply costs. Also, talk to alumni of the program to get a realistic picture of career prospects and financial outcomes. Discover strategies for choosing the right vocational program in our detailed guide on career pathways.

Your Path to a Skilled Future

Embarking on career training is an investment in yourself and your future. While the financial aspect can seem complex, understanding the various options for career training student loans empowers you to make informed decisions. By prioritizing federal aid, exploring alternative funding, borrowing responsibly, and strategically planning for repayment, you can navigate the financial landscape with confidence.

Remember, your education is a powerful tool for opening doors to new opportunities. With careful planning and a clear understanding of your financial responsibilities, you can achieve your career aspirations without the burden of overwhelming debt. Start your research, fill out that FAFSA, and take the first step toward a skilled and successful future.