Navigating Your Journey to a New Ride: The Ultimate Guide to a Car Loan with First National Bank

Navigating Your Journey to a New Ride: The Ultimate Guide to a Car Loan with First National Bank Carloan.Guidemechanic.com

The open road, the gleam of a freshly polished hood, the exhilarating scent of a new car – for many, it’s a dream waiting to be realized. However, turning that dream into a tangible reality often involves a crucial step: securing the right financing. In the vast landscape of auto lenders, First National Bank (FNB) stands out as a prominent and trusted institution. But how do you navigate their offerings to secure the best car loan for your needs?

As an expert blogger and professional SEO content writer with extensive experience in the financial sector, I’ve seen firsthand the difference informed decisions can make. This comprehensive guide is designed to be your ultimate resource, meticulously detailing everything you need to know about securing a car loan with First National Bank. We’ll dive deep into their options, the application process, key factors influencing your loan, and expert tips to ensure a smooth, successful journey from application to keys in hand.

Navigating Your Journey to a New Ride: The Ultimate Guide to a Car Loan with First National Bank

Why First National Bank Should Be On Your Radar for Car Financing

When it comes to significant financial commitments like a car loan, choosing a lender you can trust is paramount. First National Bank, with its long-standing history and reputation, offers several compelling reasons why it should be a top contender for your auto financing needs. Their established presence in the financial market speaks volumes about their stability and commitment to customer service.

A Legacy of Trust and Reliability:

First National Bank has built its reputation over many years, serving communities and individuals with a diverse range of financial products. This deep-rooted history instills confidence, assuring prospective borrowers that they are dealing with a stable and reputable institution. When you choose FNB, you’re not just getting a loan; you’re partnering with a bank that understands the nuances of personal finance.

Competitive Rates and Flexible Terms:

One of the most attractive aspects of securing a car loan through a major bank like FNB is the potential for competitive interest rates and flexible repayment terms. They often have the capacity to offer rates that smaller lenders might struggle to match, especially for well-qualified borrowers. This translates directly into lower monthly payments and reduced overall interest costs throughout the life of your loan.

Diverse Range of Loan Options Tailored to You:

Whether you’re eyeing a brand-new vehicle, a dependable used car, or looking to refinance an existing loan to save money, First National Bank typically offers a suite of options designed to meet various needs. Their product offerings are usually broad, ensuring that most car buyers can find a suitable financing solution. This flexibility is a significant advantage, allowing you to tailor the loan to your specific situation.

Accessible Customer Service and Robust Digital Tools:

In today’s fast-paced world, convenience is key. First National Bank often combines the personalized touch of local branch support with sophisticated online banking platforms and mobile apps. This means you can manage your loan, make payments, and access customer service whether you prefer face-to-face interaction or the ease of digital tools. Based on my experience, a bank that offers multiple touchpoints for support greatly enhances the borrower’s journey.

Deconstructing First National Bank Car Loan Options

Understanding the different types of car loans available at First National Bank is the first step toward making an informed decision. Each option is designed for specific scenarios, and knowing the distinctions will empower you to choose wisely.

1. New Car Loans: Driving Off the Lot with Confidence

For many, the allure of a brand-new vehicle is irresistible. New car loans from First National Bank are specifically designed to finance vehicles fresh off the dealership lot. These loans typically come with certain advantages due to the lower perceived risk associated with new cars.

When considering a new car loan, you can often expect more favorable interest rates compared to used car loans. This is because new vehicles generally hold their value better in the initial years and present less risk to the lender. FNB will assess your creditworthiness, income, and the vehicle’s value to determine your eligibility and the terms of the loan.

2. Used Car Loans: Smart Savings on Pre-Owned Vehicles

Opting for a used car can be a financially savvy decision, offering significant savings on depreciation. First National Bank provides robust financing options for pre-owned vehicles, helping you secure a reliable ride without the new car price tag. However, there are typically some differences compared to new car loans.

Used car loans might have slightly higher interest rates due to the increased risk associated with older vehicles, which can have higher maintenance costs and less predictable depreciation. FNB will often have specific criteria for used cars, such as age and mileage limits, to ensure the vehicle remains a sound investment for both you and the bank. It’s crucial to verify these limits before you fall in love with a particular car.

3. Refinancing Your Existing Car Loan: Unlocking Potential Savings

Perhaps you’ve had your car loan for a while, and your financial situation or credit score has improved. Or maybe you simply found a better rate. Refinancing your existing car loan with First National Bank can be a strategic move to reduce your monthly payments, lower your interest rate, or even shorten your loan term.

This process involves taking out a new loan with FNB to pay off your current loan. Pro tips from us: refinancing is particularly beneficial if interest rates have dropped since you initially financed your car, or if your credit score has significantly improved. A lower interest rate means you’ll pay less over the life of the loan, freeing up funds for other priorities. FNB will evaluate your current loan terms, the vehicle’s value, and your credit profile to determine if refinancing is a viable and beneficial option for you.

4. Lease Buyout Loans: Transitioning from Lease to Ownership

If you’re currently leasing a vehicle and have decided you want to keep it at the end of your lease term, First National Bank may offer lease buyout loans. This type of loan finances the residual value of your leased vehicle, allowing you to purchase it outright. It’s a convenient option for those who have grown attached to their leased car and want to avoid the hassle of finding a new one.

FNB will assess the vehicle’s buyout price, your credit history, and your ability to repay the loan, just as they would with a traditional car loan. This provides a clear path to ownership if your lease agreement allows for a buyout and you find the terms favorable.

The Application Process: Your Step-by-Step Road Map to Approval

Applying for a car loan, especially with a reputable institution like First National Bank, doesn’t have to be daunting. With the right preparation, you can navigate the process smoothly and increase your chances of approval.

Step 1: The Power of Pre-Approval

One of the most valuable steps you can take is getting pre-approved for a car loan before you even set foot on a dealership lot. This process involves FNB reviewing your financial information to determine how much you can borrow and at what interest rate.

Benefits of Pre-Approval:

- Budget Clarity: You’ll know your exact budget, preventing you from falling in love with a car you can’t afford.

- Negotiating Power: Dealers often view pre-approved buyers as serious, cash-equivalent customers, giving you leverage in price negotiations.

- Streamlined Dealership Experience: Once you find the car, the financing is already largely handled, speeding up the purchase process.

Step 2: Gathering Essential Documentation

Preparation is key. Before applying, ensure you have all necessary documents readily available. This will significantly expedite the application process.

Common Required Documents Include:

- Proof of Identity: Valid government-issued ID (driver’s license, passport).

- Proof of Income: Recent pay stubs, W-2 forms, tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): For refinancing or specific car purchases, you’ll need the VIN, make, model, and mileage.

Step 3: Understanding Your Credit Score’s Impact

Your credit score is arguably the most significant factor in determining your car loan’s interest rate and approval chances. FNB, like all lenders, uses it to assess your creditworthiness.

A higher credit score signals lower risk to the bank, often resulting in lower interest rates and more favorable terms. Conversely, a lower score might lead to higher rates or require a larger down payment. Common mistakes to avoid are applying with multiple lenders simultaneously, which can temporarily ding your score, and not checking your credit report for errors beforehand.

Step 4: Online vs. In-Branch Application

First National Bank typically offers both online and in-branch application options, each with its own advantages.

- Online Application: Offers convenience and speed, allowing you to apply from anywhere at any time. It’s ideal if you’re comfortable with digital processes and have all your documents in digital format.

- In-Branch Application: Provides a more personalized experience, allowing you to speak directly with a loan officer who can answer questions and guide you through the process. This is beneficial if you prefer face-to-face interaction or have complex financial circumstances.

Key Factors Influencing Your FNB Car Loan Approval and Rates

Beyond simply applying, several critical elements play a pivotal role in how First National Bank assesses your loan application and determines the terms you’ll receive. Understanding these factors can help you position yourself for the most favorable outcome.

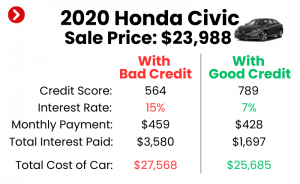

1. Your Credit Score: The Cornerstone of Lending

As mentioned, your credit score is paramount. It’s a three-digit number that summarizes your credit history and your ability to manage debt responsibly. FNB will use this score to gauge the risk of lending to you.

- Excellent Credit (750+): Likely to secure the lowest interest rates and most flexible terms.

- Good Credit (700-749): Still qualifies for very competitive rates, though perhaps not the absolute lowest.

- Fair Credit (650-699): May qualify, but with slightly higher rates to offset perceived risk.

- Poor Credit (Below 650): Approval is still possible, but often with higher interest rates, stricter terms, or requiring a larger down payment. For a deeper dive into improving your credit score, be sure to read our comprehensive guide on .

2. Debt-to-Income Ratio (DTI): Your Financial Balance

FNB will also scrutinize your Debt-to-Income (DTI) ratio. This ratio compares your total monthly debt payments to your gross monthly income. It helps the bank understand if you have enough disposable income to comfortably afford an additional car payment.

A lower DTI ratio indicates you have less existing debt relative to your income, making you a less risky borrower. Conversely, a high DTI might signal that you’re already stretched thin financially, potentially affecting your approval or leading to less favorable loan terms.

3. Loan Term: The Duration of Your Commitment

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). This choice significantly impacts your monthly payment and the total interest paid.

- Shorter Loan Terms: Result in higher monthly payments but less total interest paid over the life of the loan. This means you pay off the car faster and save money.

- Longer Loan Terms: Offer lower monthly payments, making the car more "affordable" on a month-to-month basis. However, you’ll pay significantly more in total interest over the longer duration. From an expert perspective, always choose the shortest term you can comfortably afford to minimize interest costs.

4. Down Payment: Your Upfront Investment

A down payment is the initial amount of money you pay upfront toward the purchase of the vehicle. While not always mandatory, making a substantial down payment can greatly improve your loan terms.

Benefits of a Larger Down Payment:

- Lower Loan Amount: Reduces the amount you need to borrow, thus lowering your monthly payments and total interest.

- Reduced Risk for FNB: A larger down payment means the bank has less capital at risk, potentially leading to better interest rates.

- Positive Equity Sooner: Helps you avoid being "upside down" on your loan, where you owe more than the car is worth.

5. Vehicle Type and Age: FNB’s Assessment of Collateral

The specific car you’re buying also plays a role. FNB considers the vehicle as collateral for the loan.

- Newer, More Reliable Vehicles: Generally pose less risk, as they are less likely to require immediate costly repairs that could strain your finances.

- Older Vehicles: Might be viewed as higher risk due to potential maintenance issues and faster depreciation, potentially leading to stricter terms or limits on the loan amount. FNB will often use resources like Kelley Blue Book or NADA Guides to assess the vehicle’s market value.

Maximizing Your Chances of Approval and Securing the Best Rates

Now that you understand the factors, here are actionable strategies to enhance your car loan application with First National Bank. My advice to you would be to approach this process strategically, not impulsively.

- Prioritize Credit Score Improvement: Before applying, check your credit report for errors and dispute any inaccuracies. Pay down existing debts, especially high-interest ones, and make all payments on time. A few months of diligent credit management can make a significant difference.

- Reduce Existing Debt: Work to lower your DTI ratio by paying off credit card balances or other outstanding loans. This demonstrates to FNB that you have ample capacity for a new car payment.

- Save for a Larger Down Payment: Even an extra 5% down can noticeably improve your loan terms. Begin saving early to accumulate a substantial down payment.

- Gather All Documents Proactively: Don’t wait until the last minute. Having all your financial paperwork organized and ready will make the application process much smoother and faster.

- Utilize Pre-Approval Wisely: Get pre-approved by FNB. This not only gives you a clear budget but also provides a benchmark for comparison if a dealership offers its own financing. You can use FNB’s pre-approval as leverage.

- Maintain Steady Employment: Lenders prefer stability. A consistent employment history reassures them of your ongoing income.

Beyond Approval: Responsibly Managing Your FNB Car Loan

Securing your car loan is a significant achievement, but the journey doesn’t end there. Responsible management of your loan with First National Bank is crucial for maintaining good credit and ensuring a smooth financial experience.

Convenient Payment Options:

First National Bank typically offers a variety of ways to make your monthly payments. These often include:

- Online Banking: Easily transfer funds from your FNB account or another bank.

- Automatic Payments (AutoPay): Set up recurring deductions from your checking or savings account to ensure payments are always on time, avoiding late fees and credit score damage.

- Mobile App: Make payments on the go using FNB’s mobile banking application.

- In-Branch Payments: Pay in person at any FNB branch.

- Mail: Send a check or money order through postal service.

Understanding Your Loan Statements:

Regularly review your monthly loan statements. These documents provide crucial information such as:

- Your current loan balance.

- The amount applied to principal vs. interest.

- Next payment due date and amount.

- Any fees incurred.

- Your payment history.

Understanding these details helps you track your progress and manage your finances effectively.

Considerations for Early Payoff:

If you find yourself with extra funds, paying off your car loan early can save you a substantial amount in interest. Always check your loan agreement with FNB for any prepayment penalties, though these are uncommon for consumer auto loans. If there are no penalties, making extra payments or larger lump-sum payments can accelerate your path to ownership.

Navigating Financial Hardship:

Life is unpredictable. If you encounter unexpected financial difficulties that might affect your ability to make payments, it’s critical to contact First National Bank immediately. Ignoring the problem will only exacerbate it. FNB may have options such as deferment or modified payment plans, depending on your situation and their policies. Open communication is key to finding a solution.

First National Bank’s Digital Tools and Dedicated Customer Support

In today’s digital age, a bank’s technological capabilities and customer service infrastructure are as important as its financial products. First National Bank typically excels in both these areas, making your car loan management experience seamless.

Robust Online Banking Portal:

FNB’s online banking platform usually offers a comprehensive suite of features. You can view your loan details, check payment history, schedule future payments, and even enroll in paperless statements. This central hub provides 24/7 access to your loan information, empowering you with control and convenience.

Intuitive Mobile App:

For those on the go, the First National Bank mobile app brings the power of online banking to your smartphone or tablet. Features often include mobile check deposit, payment scheduling, account balance checks, and secure messaging with customer service. This ensures you can manage your car loan from virtually anywhere.

Accessible Customer Service Channels:

While digital tools are convenient, sometimes you need to speak with a human. FNB typically provides multiple avenues for customer support:

- Phone Support: Dedicated lines for loan inquiries and general banking assistance.

- Online Chat: Instant messaging with a representative for quick questions.

- In-Branch Assistance: Local branches offer personalized support for more complex issues or if you prefer face-to-face interaction.

Real-World Scenarios and Expert Advice

From my vantage point, the key to successful car financing with First National Bank lies in preparation and understanding your unique situation. Let’s look at a few common scenarios.

Scenario 1: The First-Time Car Buyer:

- Challenge: Limited credit history.

- Expert Advice: Focus on building credit before applying. Consider a smaller down payment to keep the loan amount manageable, and potentially a co-signer if a parent or trusted individual has good credit. FNB may offer programs for first-time buyers, but a solid credit foundation is always best.

Scenario 2: Buyer with Less-Than-Perfect Credit:

- Challenge: Higher interest rates, potential for denial.

- Expert Advice: Prioritize improving your credit score first. If that’s not possible, be prepared for a larger down payment. Explore FNB’s secured loan options (if available) or consider a co-signer. A used car that is less expensive might also be a more viable option to start.

Scenario 3: Refinancing to Save Money:

- Challenge: Unsure if it’s worth the effort.

- Expert Advice: Always run the numbers. Use FNB’s online calculators or speak to a loan officer. Consider refinancing if your credit score has improved, current interest rates are lower, or you want to adjust your monthly payment (either lower it or shorten the term to save interest). It’s an excellent way to optimize your existing loan.

Your Journey Starts Here: Partnering with First National Bank

Securing a car loan is a significant financial decision, but with the right knowledge and preparation, it can be a smooth and rewarding experience. First National Bank offers a robust suite of auto financing options, backed by a strong reputation, competitive rates, and excellent customer service. By understanding their loan products, meticulously preparing your application, and proactively managing your loan, you can confidently drive off in your new vehicle.

Remember, an informed borrower is an empowered borrower. Take the time to assess your financial situation, gather your documents, and explore the options available through First National Bank. Your dream car is within reach, and FNB can be the trusted partner that helps you get there. You might also find our article on beneficial if you’re still weighing your vehicle options. For general consumer financial protection and guidance, the Consumer Financial Protection Bureau (CFPB) offers a wealth of information and resources. Visit their website to learn more about your rights as a consumer and make confident financial decisions.