Navigating Your Next Ride: The Ultimate Guide to a Chase Auto Loan for a Used Car

Navigating Your Next Ride: The Ultimate Guide to a Chase Auto Loan for a Used Car Carloan.Guidemechanic.com

Buying a used car can be an exciting, and often more financially savvy, decision than purchasing a brand-new vehicle. However, securing the right financing is crucial to ensuring a smooth and affordable experience. For many, a trusted financial institution like Chase Bank comes to mind, offering a robust suite of options for your next pre-owned vehicle. Understanding the intricacies of a Chase Auto Loan Used Car is key to unlocking the best rates and terms.

This comprehensive guide will demystify the process, offering in-depth insights, expert tips, and a clear roadmap to help you confidently secure your used car financing through Chase. Whether you’re a first-time buyer or looking to upgrade, we’ll cover everything you need to know to make an informed decision. Our goal is to equip you with the knowledge to navigate the journey seamlessly, from initial research to driving off the lot.

Navigating Your Next Ride: The Ultimate Guide to a Chase Auto Loan for a Used Car

Why Consider Chase for Your Used Car Loan?

When it comes to financing a used car, the lender you choose makes a significant difference. Chase Bank, a prominent name in the financial sector, brings a wealth of experience and a reputation for stability to the auto loan market. Their long-standing presence provides a level of trust and reliability that can be incredibly reassuring for borrowers.

Based on my experience in the automotive financing landscape, Chase offers a competitive edge, particularly for existing customers. Their established infrastructure allows for efficient processing and often provides personalized service. This can translate into a more streamlined application and approval process, which is invaluable when you’re eager to get behind the wheel of your chosen used vehicle.

Furthermore, Chase often provides competitive auto loan rates for well-qualified applicants. While rates fluctuate based on market conditions and individual creditworthiness, their offerings are generally in line with, or even better than, many other traditional lenders. This makes them a strong contender for anyone seeking favorable used car financing terms.

Understanding Chase Auto Loan Options for Used Cars

Chase offers several avenues for securing a loan for a used car, catering to different buying scenarios. Knowing these options helps you choose the path that best suits your needs and purchasing strategy. Each method has its own advantages and specific requirements.

Direct Financing: Applying Directly to Chase

One of the most straightforward ways to obtain a Chase Auto Loan Used Car is by applying directly through Chase. This process involves you, the borrower, applying for a loan independent of a dealership. Once approved, you receive a loan offer, which you can then use to purchase a used car from a dealership or even a private seller, depending on Chase’s specific terms for private party sales.

Pre-approval is a critical component of direct financing. By getting pre-approved, you gain a clear understanding of how much you can borrow and at what interest rate before you even start shopping. This empowers you as a buyer, giving you the confidence to negotiate prices with dealerships, knowing your financing is already secured. It essentially puts you in the driver’s seat of the purchasing process.

Pro tips from us: Always aim for pre-approval. It not only streamlines the buying process but also helps you set a realistic budget for your used car. Without pre-approval, you might fall in love with a car outside your financial comfort zone.

Dealership Financing: Through a Chase-Affiliated Dealer

Many car dealerships partner with a network of lenders, and Chase is often one of them. When you finance through a dealership, they act as an intermediary, submitting your loan application to various banks, including Chase. This can be a convenient option, as it allows you to complete the financing and purchase in one location.

While convenient, it’s important to approach dealership financing with caution. Dealerships often add a markup to the interest rate offered by the lender to cover their costs and generate profit. This means the rate you get from the dealership might be higher than if you applied directly to Chase for the same loan. Always compare the dealership’s offer with a direct Chase auto loan pre-approval.

Common mistakes to avoid are accepting the first financing offer from a dealership without comparing it to external options. Always remember that a dealership’s primary goal is to sell you a car, and sometimes that includes a financing package that benefits them more than you. Doing your homework beforehand can save you significant money over the life of the loan.

Private Seller Financing: Specifics for Buying from an Individual

Buying a used car from a private seller can sometimes offer better value than purchasing from a dealership, as you often avoid dealership markups and fees. Chase does offer financing for private party sales, but the process has specific requirements to ensure the transaction’s security and legality. This can be a great way to save money, but it requires careful attention to detail.

When considering a private seller auto loan through Chase, expect them to have strict criteria for the vehicle. They will typically require an inspection, a clear title, and verification of the car’s value. This due diligence protects both you and the bank, ensuring the car is worth the loan amount. Make sure to have all necessary documentation ready from the seller, including the title and bill of sale.

Based on my experience, navigating a private party sale with a bank loan requires more coordination than a dealership purchase. Be prepared to gather more documents and facilitate communication between Chase and the seller. However, the potential savings often make this extra effort worthwhile for your used car financing.

The Chase Auto Loan Application Process: A Step-by-Step Guide

Applying for an auto loan can seem daunting, but breaking it down into manageable steps makes it much clearer. Chase has a structured process designed to assess your eligibility and provide you with a suitable financing option for your used car. Understanding each stage will help you prepare thoroughly.

Eligibility Requirements for a Chase Used Car Loan

Before you even start the application, it’s essential to understand what Chase looks for in a borrower. Meeting these criteria significantly increases your chances of approval and securing favorable loan terms. These requirements are standard across most financial institutions but are crucial to highlight.

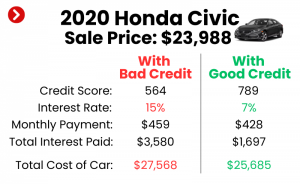

- Credit Score: This is perhaps the most critical factor. While Chase doesn’t publish a minimum score, generally, a good to excellent credit score (typically 670 and above) will yield the best rates. Lower scores might still qualify but could come with higher interest rates.

- Income: You’ll need to demonstrate a stable income sufficient to cover your monthly loan payments, in addition to your existing financial obligations. Chase wants to ensure you have the capacity to repay the loan without undue hardship.

- Debt-to-Income Ratio (DTI): Your DTI is the percentage of your gross monthly income that goes towards paying your monthly debt payments. A lower DTI (ideally below 40%) indicates that you’re not overextended financially and are a lower risk borrower.

- Vehicle Requirements: For a Chase Auto Loan Used Car, the vehicle itself must also meet certain criteria. This typically includes limitations on the car’s age (e.g., usually less than 10 years old) and mileage (e.g., often under 100,000-120,000 miles). The car must also have a clear title and a value that aligns with the loan amount, as determined by a reputable valuation service like Kelley Blue Book or NADAguides.

Gathering Essential Documents

Once you’re ready to apply, having all your documents organized beforehand will speed up the process considerably. This step is about proving your identity, income, and financial stability to Chase. Think of it as painting a complete financial picture for the lender.

- Proof of Identity: A valid government-issued ID, such as a driver’s license or passport, is always required.

- Proof of Income: Recent pay stubs (typically 2-3 months), W-2 forms, or tax returns (for self-employed individuals) demonstrate your earning capacity.

- Proof of Residency: Utility bills, lease agreements, or mortgage statements confirm your address.

- Vehicle Information (if already chosen): This includes the vehicle identification number (VIN), make, model, year, mileage, and the selling price. For private sales, a bill of sale and clear title are crucial.

Applying Online or In-Person

Chase offers convenient ways to submit your application. You can apply from the comfort of your home or visit a local branch for personalized assistance. Both methods are designed to be user-friendly, but choosing the right one for you depends on your preference for digital convenience versus face-to-face interaction.

The online application for a Chase auto loan is generally quick and efficient, guiding you through a series of questions about your personal, financial, and employment information. You’ll typically be able to upload necessary documents digitally. For those who prefer a more personal touch or have complex questions, applying in person at a Chase branch allows you to speak directly with a loan officer.

Pre-Approval vs. Full Application

While we’ve touched on pre-approval, it’s worth reiterating its importance. A pre-approval is a conditional offer of credit, based on a preliminary review of your financial information. It’s not a guarantee of the final loan, but it gives you a strong indication of what you qualify for. This step is invaluable for setting your budget and negotiating with confidence.

A full application, on the other hand, occurs when you have a specific vehicle in mind and are ready to finalize the loan. This involves a more thorough review, including a hard credit inquiry, and the finalization of all loan documents. Pre-approval typically lasts for a specific period, often 30 days, giving you ample time to shop.

Common mistakes to avoid are waiting until you’re at the dealership with the car you want to begin the application process. This puts you under pressure and reduces your leverage. Get pre-approved first; it’s a game-changer for used car financing.

Key Factors Affecting Your Chase Used Car Loan Approval & Rates

Several factors beyond your initial application influence whether your Chase Auto Loan Used Car is approved and, critically, the interest rate you’ll receive. Understanding these elements can help you optimize your financial position before applying.

Your Credit Score: The Most Significant Factor

Your credit score is essentially your financial report card, reflecting your history of borrowing and repaying debt. Chase, like all lenders, relies heavily on this number to assess your risk as a borrower. A higher score indicates a lower risk, often leading to better interest rates and more favorable loan terms.

What Chase looks for specifically includes a history of timely payments, a low credit utilization ratio, and a diverse credit mix. Any missed payments, bankruptcies, or high credit card balances can negatively impact your score and, consequently, your loan offer. Improving your credit score, even by a few points, can translate into significant savings over the life of your loan.

Debt-to-Income Ratio (DTI): Why It Matters

As mentioned earlier, your DTI ratio is a crucial indicator of your financial health. Chase uses this ratio to determine if you can comfortably afford another monthly payment without becoming overextended. A high DTI suggests that a significant portion of your income is already committed to other debts, making you a higher risk.

Lenders prefer to see a DTI that leaves you with sufficient disposable income after all your debt obligations are met. If your DTI is on the higher side, consider paying down other debts before applying for an auto loan. This proactive step can dramatically improve your chances of approval and potentially secure a better rate.

Loan Amount & Term: Finding the Right Balance

The total amount you wish to borrow and the length of your repayment period (the loan term) significantly impact your monthly payments and the total interest you’ll pay. A longer loan term means lower monthly payments, but you’ll end up paying more in interest over time. Conversely, a shorter term has higher monthly payments but saves you money on interest.

When discussing Chase auto loan rates, it’s vital to consider the entire picture. While a lower monthly payment might seem attractive, carefully evaluate the total cost of the loan. Pro tips from us: Aim for the shortest loan term you can comfortably afford. This minimizes the amount of interest you pay and helps you build equity in your used car faster.

Vehicle Specifics: Age, Mileage, and Value

Even for a used car, the vehicle itself plays a role in the financing decision. Chase needs to ensure the car serves as adequate collateral for the loan. Older cars with high mileage often present a higher risk to lenders due to increased likelihood of mechanical issues and faster depreciation.

Chase will also consider the car’s Loan-to-Value (LTV) ratio, which compares the loan amount to the car’s actual market value. If you’re borrowing significantly more than the car is worth, it can be a red flag. Be prepared for Chase to require an appraisal or rely on industry valuation guides to confirm the car’s worth.

Beyond Approval: Managing Your Chase Auto Loan

Getting approved for your Chase Auto Loan Used Car is a significant step, but effective management of your loan is equally important. Understanding your loan terms and payment options ensures a smooth repayment journey and can even save you money.

Understanding Your Loan Terms: APR, Principal, Interest

When you receive your loan documents, pay close attention to the Annual Percentage Rate (APR). This is the true cost of borrowing, encompassing not just the interest rate but also any fees associated with the loan. The principal is the original amount you borrowed, and interest is the cost of borrowing that money.

Each monthly payment you make will be split between paying down the principal and covering the interest. Early in the loan term, a larger portion of your payment often goes towards interest. As the loan matures, more of your payment will go towards reducing the principal balance. Familiarizing yourself with these components empowers you to track your progress and understand the financial commitment.

Making Payments: Online, Auto-Pay, Mail

Chase offers various convenient ways to make your monthly car loan payments. The easiest and most common method is online payment through your Chase account, allowing you to schedule one-time or recurring payments. Setting up auto-pay directly from your checking account can help you avoid missed payments and potential late fees.

You can also make payments over the phone or by mail. Choosing a payment method that aligns with your habits ensures consistency and peace of mind. Consistent, on-time payments are crucial for maintaining a good payment history and protecting your credit score.

Refinancing Options: When and Why to Consider It

Life circumstances and market conditions can change, and your initial loan terms might no longer be the best fit. Refinancing a car loan involves taking out a new loan to pay off your existing one, often with new terms. This can be beneficial if interest rates have dropped, your credit score has significantly improved since you first took out the loan, or you need to adjust your monthly payment.

Chase offers options for refinancing existing auto loans, even if they weren’t originally with Chase. Pro tips from us: Periodically review your auto loan interest rate against current market rates and your improved credit score. If there’s a significant difference, refinancing could save you hundreds or even thousands of dollars over the remaining loan term.

Early Payoff: Benefits and Considerations

If you find yourself with extra funds, you might consider paying off your Chase Auto Loan Used Car early. The primary benefit of an early payoff is saving money on interest, as interest is typically calculated on the remaining principal balance. The sooner you pay it off, the less interest accrues.

Before making an early payoff, check your loan agreement for any prepayment penalties. While less common with traditional auto loans, some lenders might charge a fee. Generally, paying off your loan early is a smart financial move, freeing up your monthly budget and reducing your overall debt burden.

Common Pitfalls and How to Avoid Them

Even with the best intentions, borrowers can sometimes fall into common traps when securing a used car loan. Being aware of these pitfalls can help you avoid costly mistakes and ensure a smoother financing experience with Chase.

- Not Getting Pre-Approved: This is perhaps the biggest mistake. Without pre-approval, you walk into a dealership blind, unsure of your borrowing power or the rates you truly qualify for. This leaves you vulnerable to high-pressure sales tactics and potentially unfavorable loan terms. Always get pre-approved first!

- Ignoring Your Credit Report: Many individuals don’t review their credit report for errors before applying for a loan. Mistakes on your report can unfairly lower your score, impacting your loan eligibility and interest rates. Obtain your free credit report from External Link: AnnualCreditReport.com and dispute any inaccuracies well in advance.

- Focusing Only on Monthly Payments: While your monthly payment is important for budgeting, fixating solely on it can lead to longer loan terms and significantly more interest paid over time. Always consider the total cost of the loan and aim for a balance between affordability and minimizing overall interest.

- Not Understanding the Fine Print: Loan agreements can be complex, but it’s crucial to read and understand every clause before signing. Pay attention to the APR, any fees, prepayment penalties (if any), and the full breakdown of your repayment schedule. If something is unclear, ask questions until you fully grasp the terms. Common mistakes to avoid are signing documents you don’t fully comprehend, which can lead to unwelcome surprises down the line.

Conclusion: Driving Forward with Confidence

Securing a Chase Auto Loan Used Car can be a straightforward and rewarding process when approached with knowledge and preparation. From understanding Chase’s various financing options to meticulously navigating the application process, every step contributes to a successful outcome. By focusing on your credit health, understanding loan terms, and avoiding common pitfalls, you empower yourself to make the best financial decisions.

Remember, a used car is a significant investment, and the right financing partner makes all the difference. With Chase, you have the backing of a reputable institution, and with the insights from this guide, you’re well-equipped to secure favorable used car financing. Drive confidently into your next adventure, knowing you’ve made an informed choice for your Chase auto loan.