Navigating Your Wheels: A Deep Dive into Car Loans from the Former TCF Bank (Now Huntington National Bank)

Navigating Your Wheels: A Deep Dive into Car Loans from the Former TCF Bank (Now Huntington National Bank) Carloan.Guidemechanic.com

Securing the right car loan is a cornerstone of responsible vehicle ownership. For many years, TCF Bank was a familiar name in the lending landscape, providing auto financing to countless individuals. However, the financial world is dynamic, and understanding where to turn for a "Tcf Bank Car Loan" today requires a keen awareness of recent industry shifts.

As an expert blogger and professional SEO content writer specializing in financial guidance, I’ve seen firsthand how important it is to have accurate and up-to-date information when making significant financial decisions. This comprehensive guide will not only delve into the legacy of TCF Bank’s auto loan offerings but, crucially, explain where those services have transitioned, providing you with a clear path forward for your car financing needs with Huntington National Bank. Our ultimate goal is to equip you with the knowledge to make informed choices, secure favorable terms, and drive away with confidence.

Navigating Your Wheels: A Deep Dive into Car Loans from the Former TCF Bank (Now Huntington National Bank)

The Legacy of TCF Bank Car Loans: A Look Back

For decades, TCF Bank played a significant role in helping consumers finance their vehicles. They offered a range of auto loan products designed to cater to various credit profiles and financial situations. Their approach was often characterized by accessible customer service and a presence in many communities.

Based on my experience observing regional banks, TCF Bank typically offered both new and used car loans. They also provided refinancing options, which allowed existing car owners to potentially lower their interest rates or monthly payments. These services were fundamental in assisting individuals with their transportation needs.

Many customers appreciated the personalized touch and local presence TCF Bank provided. They built relationships with loan officers, which often made the car buying process feel less daunting. This human element was a distinguishing factor for many regional financial institutions.

The Major Shift: TCF Bank’s Acquisition by Huntington National Bank

A pivotal moment for anyone searching for a "Tcf Bank Car Loan" occurred when TCF Bank was acquired by Huntington National Bank. This significant merger, finalized in 2021, fundamentally changed the landscape of TCF’s banking services, including their auto loan division. Understanding this acquisition is paramount to navigating your current car financing options.

When two large financial institutions merge, their products and services are integrated. This means that TCF Bank’s auto loan programs, processes, and customer accounts were absorbed and transitioned under the Huntington National Bank umbrella. It’s no longer possible to apply for a TCF Bank Car Loan as a standalone product.

This transition aimed to create a larger, more robust banking entity with an expanded service area and enhanced financial offerings. For former TCF customers, their existing loans and accounts were seamlessly migrated to Huntington’s system. For new applicants, all inquiries and applications for car loans are now directed through Huntington National Bank.

Navigating Car Loans with Huntington National Bank: Your Current Path

With TCF Bank’s auto loan services now integrated into Huntington National Bank, your focus should shift to understanding Huntington’s current offerings. Huntington National Bank is a well-established and reputable financial institution that continues to provide comprehensive auto financing solutions. They offer a robust suite of options for individuals looking to purchase a new or used vehicle, or to refinance an existing auto loan.

As an expert in financial content, I always advise looking at the current offerings of the successor institution. Huntington Bank provides competitive rates and flexible terms designed to meet diverse financial needs. Their goal, like any major lender, is to make vehicle ownership accessible and affordable for their customers.

Understanding their specific products, eligibility criteria, and application process is your next crucial step. This ensures you are approaching your car financing journey with the most accurate and actionable information.

Eligibility Requirements for Auto Loans at Huntington National Bank

To qualify for an auto loan from Huntington National Bank, like most lenders, you’ll need to meet specific eligibility criteria. These requirements are in place to assess your creditworthiness and your ability to repay the loan. Meeting these criteria increases your chances of approval and can lead to more favorable loan terms.

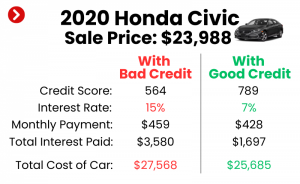

One of the primary factors is your credit score. A strong credit history, typically indicated by a higher FICO score, demonstrates a history of responsible borrowing and repayment. Lenders view this as a lower risk, often resulting in lower interest rates.

Your income and employment stability are also critical considerations. Lenders want to ensure you have a consistent source of income to make your monthly payments. They will typically ask for proof of income, such as pay stubs or tax returns.

Furthermore, your debt-to-income (DTI) ratio plays a significant role. This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates that you have more disposable income available to cover new loan payments, which is favorable to lenders.

The Application Process: What to Expect

Applying for an auto loan with Huntington National Bank is a streamlined process, designed for convenience. You typically have several options for initiating your application, catering to different preferences and needs. This flexibility makes securing financing more accessible.

You can apply online directly through Huntington’s website, which is often the quickest method. The online application allows you to submit your information from the comfort of your home, at any time. This digital approach has become increasingly popular for its efficiency.

Alternatively, you can visit a Huntington National Bank branch in person. This option is ideal if you prefer face-to-face interaction or have specific questions you’d like to discuss with a loan officer. In-branch applications allow for personalized guidance throughout the process.

When applying, you’ll need to provide personal information such as your name, address, Social Security number, and employment details. You’ll also need financial information, including income verification and details about any existing debts. Having these documents ready beforehand can significantly expedite the application process.

Types of Auto Loans Offered by Huntington National Bank

Huntington National Bank offers a variety of auto loan products to suit different purchasing scenarios. Whether you’re eyeing a brand-new vehicle or a reliable pre-owned car, they have financing options tailored to your needs. This range of products ensures that most car buyers can find a suitable solution.

New Car Loans: These loans are specifically designed for financing vehicles purchased directly from a dealership that have never been previously titled. New car loans often come with slightly lower interest rates due to the vehicle’s higher resale value and typically lower risk. They also tend to have longer loan terms available.

Used Car Loans: For those looking at pre-owned vehicles, Huntington provides used car loans. These loans can be used for purchases from dealerships or even private sellers, though specific requirements might apply for private party sales. Interest rates for used car loans can be slightly higher than new car loans, reflecting the vehicle’s depreciation and potential age.

Auto Loan Refinancing: If you already have a car loan with another lender, Huntington offers refinancing options. Refinancing allows you to replace your current car loan with a new one, potentially with a lower interest rate, a shorter or longer loan term, or reduced monthly payments. This can be an excellent strategy to save money over the life of your loan or to better manage your budget.

Understanding Interest Rates and Loan Terms

Interest rates and loan terms are two of the most critical factors influencing the total cost of your auto loan. Grasping how they work together is essential for making an informed financial decision. A seemingly small difference in interest rate can translate to significant savings over time.

Interest Rates: The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. Your interest rate is primarily determined by your credit score, the loan term, the vehicle’s age, and market conditions. A higher credit score generally qualifies you for a lower interest rate, which means less money paid in interest over the life of the loan.

Loan Terms: The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term usually results in higher monthly payments but less interest paid overall. Conversely, a longer loan term means lower monthly payments but more interest paid over the life of the loan.

Pro tips from us: Always consider the total cost of the loan, not just the monthly payment. Sometimes, a slightly higher monthly payment on a shorter term can save you thousands in interest. Use an auto loan calculator to compare different scenarios.

Pro Tips for Securing the Best Auto Loan

Securing the best possible auto loan goes beyond simply filling out an application. It involves strategic planning and understanding how lenders assess your profile. As an expert in financial planning, I’ve seen countless individuals benefit from a proactive approach.

Here are some pro tips to help you navigate the process and maximize your chances of getting a favorable deal. These insights are based on years of observing lending practices and helping consumers make smart financial choices.

1. Boost Your Credit Score Before Applying

Your credit score is arguably the single most important factor in determining your interest rate. Lenders use it as a quick snapshot of your financial reliability. A higher score signals less risk, which translates to better terms.

Start by checking your credit report from all three major bureaus (Equifax, Experian, TransUnion) well in advance of applying. Look for any errors or discrepancies that could be dragging your score down. Disputing inaccuracies can lead to a quick bump in your score.

Focus on paying down high-interest debt, especially credit card balances, as this improves your credit utilization ratio. Make sure all your payments are on time; even one late payment can significantly impact your score. For a deeper dive into improving your credit score, check out our article on .

2. Understand Your Budget and What You Can Truly Afford

Before you even start looking at cars, determine your absolute maximum affordable monthly payment and total vehicle cost. This involves looking at your income, existing expenses, and other financial commitments. Don’t just rely on a lender’s pre-approval amount; that’s often the maximum you could borrow, not necessarily what you should borrow.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of ownership. Remember to factor in insurance, maintenance, fuel, and registration fees into your overall budget. These additional costs can quickly add up and strain your finances if not properly accounted for.

A good rule of thumb is that your total car expenses (payment, insurance, fuel, maintenance) should not exceed 10-15% of your net monthly income. This ensures you have financial flexibility for other needs and emergencies.

3. Get Pre-Approved from Multiple Lenders

Don’t limit yourself to the dealership’s financing options right away. Obtaining pre-approval from several different lenders, including Huntington National Bank, gives you a powerful negotiating tool. Pre-approval means a lender has conditionally agreed to lend you a certain amount at a specific interest rate, based on a preliminary review of your credit.

Having multiple offers in hand allows you to compare interest rates, loan terms, and any associated fees. This competition among lenders often results in you securing a better deal. It also empowers you to focus on negotiating the car price at the dealership, rather than simultaneously worrying about the financing.

Pro tips from us: Most pre-approvals are "soft inquiries" that don’t impact your credit score. Once you’re ready to finalize, a "hard inquiry" will occur. Multiple hard inquiries for the same type of loan within a short period (typically 14-45 days) are often grouped as a single inquiry by credit bureaus, minimizing the impact on your score.

4. Make a Significant Down Payment

A larger down payment offers several substantial benefits. Firstly, it reduces the total amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan. It’s simple math: less borrowed equals less interest.

Secondly, a substantial down payment can help you avoid being "upside down" on your loan. This occurs when you owe more on the car than it’s worth, which is common with vehicles that depreciate quickly. A larger down payment creates immediate equity in the vehicle.

Finally, lenders often view a larger down payment as a sign of financial commitment and responsibility. This can sometimes lead to more favorable loan terms, even if your credit score isn’t perfect. Aim for at least 10-20% of the vehicle’s purchase price, if possible.

5. Be Mindful of Loan Terms and Total Cost

While a longer loan term might offer a lower monthly payment, it almost always means paying more in total interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but significant interest savings. It’s a trade-off that needs careful consideration.

Always ask for the Annual Percentage Rate (APR), which includes the interest rate plus any additional fees, giving you a more accurate picture of the total cost of borrowing. Don’t be swayed solely by a low monthly payment; focus on the total amount you will pay back.

Based on my experience, many buyers regret extending their loan term just to reduce the monthly payment by a small amount. This often leads to paying thousands more in interest. Balance your monthly budget with the long-term cost.

Beyond the Loan: Managing Your Car Loan Responsibly

Securing an auto loan is just the beginning of your journey. Responsible loan management is crucial for maintaining your financial health and ensuring a smooth repayment period. Poor management can lead to penalties, damage your credit score, and even result in vehicle repossession.

As an expert, I emphasize that proactive management can save you stress and money. Understanding your obligations and utilizing available tools can make a significant difference in your long-term financial well-being.

Payment Strategies and Avoiding Late Fees

The most fundamental aspect of responsible loan management is making your payments on time, every time. Late payments not only incur fees from the lender but also negatively impact your credit score. A single late payment can remain on your credit report for years, making it harder to secure future loans.

Consider setting up automatic payments from your checking account. This eliminates the risk of forgetting a payment date and ensures consistency. Many lenders, including Huntington National Bank, offer this convenient service.

Another smart strategy is to pay a little extra each month if your budget allows. Even a small additional amount applied directly to the principal can significantly reduce the total interest paid and shorten the loan term. This accelerates your path to debt freedom.

Refinancing Considerations

Life circumstances change, and so might your financial situation or market interest rates. Refinancing your car loan can be a powerful tool to adapt to these changes. It’s not just for those struggling with payments; it can also be a smart financial move for those seeking to optimize their loan.

You might consider refinancing if interest rates have dropped since you took out your original loan. A lower rate can lead to substantial savings. Similarly, if your credit score has significantly improved, you might qualify for a better rate than you initially received.

If you’re considering refinancing, our guide to can provide more insights. It’s always wise to compare your current loan terms with potential new offers to see if refinancing makes financial sense for your unique situation.

What to Do If You Face Financial Hardship

Life throws curveballs, and sometimes financial hardship can make it difficult to meet your loan obligations. The worst thing you can do in this situation is ignore the problem. Proactive communication with your lender is key.

If you anticipate difficulties in making a payment, contact Huntington National Bank immediately. They may offer options such as deferment, forbearance, or a temporary payment reduction. These options are typically granted on a case-by-case basis and are designed to help you get back on track.

Common mistakes to avoid are waiting until you’re already delinquent. Lenders are often more willing to work with borrowers who communicate their challenges early. Being transparent about your situation can prevent more severe consequences like repossession and significant damage to your credit.

Conclusion: Your Path to Smart Car Financing Continues with Huntington National Bank

The journey to financing your next vehicle, while no longer involving a direct "Tcf Bank Car Loan," is as accessible and robust as ever through Huntington National Bank. Understanding the transition from TCF Bank to Huntington is the first crucial step in navigating your auto loan options today. By focusing on Huntington National Bank’s current offerings, you can leverage their extensive financial services to secure a loan that fits your budget and lifestyle.

We’ve explored the importance of a strong credit score, the various types of loans available, and critical strategies like making a down payment and getting pre-approved from multiple lenders. Remember, securing the best auto loan is about preparation, understanding your financial capacity, and making informed decisions. By following these expert insights, you’re well-equipped to drive away with not just a new vehicle, but also a smart financial agreement.

Always remember to research, compare offers, and communicate openly with your chosen lender. Your financial future depends on it. For more detailed information on Huntington National Bank’s current auto loan offerings, you can visit their official website at . Drive safe, and drive smart!