Navigating Your Wheels: The Ultimate Guide to Bank of the West Car Loans

Navigating Your Wheels: The Ultimate Guide to Bank of the West Car Loans Carloan.Guidemechanic.com

The dream of a new car often begins long before you even step onto a dealership lot. It starts with a crucial question: how will you finance it? For many, securing a reliable and affordable car loan is the cornerstone of making that dream a reality. When considering financial partners, established institutions like Bank of the West often come to mind. They offer a range of auto financing solutions designed to get you behind the wheel.

This comprehensive guide will walk you through everything you need to know about securing a Bank of the West car loan. We’ll delve deep into their offerings, eligibility criteria, the application process, and provide expert tips to maximize your chances of approval. Our goal is to equip you with the knowledge and confidence to make informed decisions, ensuring a smooth journey from application to ownership.

Navigating Your Wheels: The Ultimate Guide to Bank of the West Car Loans

Why Consider Bank of the West for Your Car Loan?

Choosing the right lender for your auto loan is a significant decision. It impacts your monthly budget, the total cost of your vehicle, and your overall financial well-being. Bank of the West, with its long-standing presence and commitment to customer service, presents a compelling option for many borrowers.

Reputation and Trust:

Based on my experience in the financial landscape, working with an established bank like Bank of the West offers a certain level of reassurance. They operate under strict regulations and have a proven track record of serving communities. This institutional stability can translate into a more predictable and transparent lending experience.

Competitive Rates and Terms:

Bank of the West often provides competitive interest rates and flexible loan terms. These are critical factors that directly influence your monthly payment and the total amount of interest you’ll pay over the life of the loan. They aim to structure loans that fit various financial situations.

Variety of Loan Options:

Whether you’re eyeing a brand-new model, a reliable used vehicle, or looking to refinance an existing auto loan, Bank of the West typically offers solutions. This versatility means you can often find a product tailored to your specific needs, rather than a one-size-fits-all approach. Their offerings can cover various vehicle types and price points.

Personalized Customer Service:

Many borrowers appreciate the ability to speak with a loan officer directly, either in person at a branch or over the phone. This personalized approach can be invaluable, especially if you have unique financial circumstances or questions that a purely online lender might not address as thoroughly. They can guide you through the complexities.

Understanding Bank of the West Car Loan Eligibility

Before you even begin the application process, it’s crucial to understand the general eligibility requirements. Meeting these criteria will significantly improve your chances of securing a Bank of the West car loan. Lenders evaluate several key factors to assess your creditworthiness and ability to repay the loan.

Credit Score Requirements:

Your credit score is perhaps the most critical factor in auto loan approval and the interest rate you’ll receive. Lenders use FICO scores or similar models to gauge your credit risk. Generally, a score in the "good" to "excellent" range (typically 670 and above) will open doors to the most favorable rates. However, Bank of the West may offer options for those with less-than-perfect credit, though potentially at higher rates.

Income and Employment Stability:

Lenders want to ensure you have a consistent and sufficient income stream to comfortably make your monthly payments. They will typically ask for proof of employment and income, such as recent pay stubs or tax returns. Your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income, is also a significant consideration. A lower DTI ratio indicates you have more disposable income available for new debt.

Down Payment Considerations:

While not always strictly required, making a down payment on your vehicle can greatly benefit your loan application. A substantial down payment reduces the amount you need to borrow, lowers your monthly payments, and often results in a better interest rate. It also demonstrates your financial commitment to the purchase.

Vehicle Requirements:

The vehicle itself plays a role in the loan approval process. Lenders often have requirements regarding the age, mileage, and type of car they are willing to finance. For example, very old or high-mileage vehicles might be considered higher risk. The loan amount will also be based on the vehicle’s appraised value.

Residency and Age:

You will need to be a legal resident of the United States and meet the minimum age requirement, which is typically 18 years old in most states, to enter into a loan contract. Providing valid identification is a standard part of the application.

The Step-by-Step Application Process for a Bank of the West Car Loan

Applying for a Bank of the West car loan doesn’t have to be a daunting task. By understanding each step, you can approach the process with confidence and efficiency. Preparing in advance is key to a smooth experience.

1. Pre-qualification vs. Full Application:

Many lenders, including Bank of the West, offer a pre-qualification option. This allows you to get an estimate of your potential loan amount and interest rate without a hard inquiry on your credit report, which won’t impact your score. It’s a great way to gauge affordability before committing to a full application. A full application, however, will involve a hard credit pull.

2. Gather Required Documentation:

This is where preparation pays off. Having all your documents ready streamlines the process.

- Personal Identification: Valid government-issued ID (driver’s license, state ID, passport).

- Proof of Income: Recent pay stubs (typically 1-2 months), W-2 forms, or tax returns if self-employed.

- Proof of Residency: Utility bill or lease agreement with your current address.

- Bank Account Information: For setting up automatic payments.

- Vehicle Information (if already chosen): Make, model, year, VIN, and sale price.

3. Choose Your Application Method:

Bank of the West generally offers several ways to apply:

- Online: Convenient and often the fastest method. You can typically complete the application from home.

- In-Branch: Visiting a local branch allows you to speak with a loan officer directly, which can be helpful for questions or complex situations.

- Through a Dealership: Many dealerships have partnerships with various lenders, including Bank of the West, and can facilitate the application on your behalf.

4. What Happens After You Apply?

Once your application is submitted, the bank will review your financial information, pull your credit report, and assess your eligibility. This process can take anywhere from a few hours to a few business days. You will then be notified of their decision. If approved, you’ll receive details about your loan offer, including the interest rate, loan term, and monthly payment.

Maximizing Your Chances of Bank of the West Car Loan Approval

Securing the best possible terms for your Bank of the West car loan involves more than just meeting the basic requirements. Proactive steps can significantly enhance your application and lead to a more favorable outcome.

Pro Tips from Us:

- Boost Your Credit Score: Before applying, take steps to improve your credit. Pay down existing debts, especially high-interest credit card balances. Make all payments on time and avoid opening new credit accounts. For more details on improving your credit score, check out our in-depth article: .

- Save for a Down Payment: Even a small down payment can make a big difference. It reduces the loan amount, lowers your monthly payments, and makes you a less risky borrower in the eyes of the bank. Aim for at least 10-20% of the vehicle’s purchase price if possible.

- Gather All Documents in Advance: As mentioned earlier, having all your necessary paperwork ready prevents delays and shows the lender you are organized and serious about the loan.

- Shop for the Right Vehicle: Research car prices to ensure the vehicle you’re interested in is within a reasonable range for its make, model, and condition. Lenders typically won’t finance a car for more than its appraised value.

- Consider a Co-signer (When Appropriate): If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. Ensure both parties understand the responsibilities involved.

Common Mistakes to Avoid Are:

- Applying to Too Many Lenders: Each full loan application results in a "hard inquiry" on your credit report. Too many inquiries in a short period can negatively impact your credit score. Do your research and target a few specific lenders.

- Ignoring Your Credit Report: Always review your credit report for errors before applying for a loan. Incorrect information could unfairly lower your score and hinder your approval chances. You can get a free copy annually from each of the three major credit bureaus.

- Underestimating Vehicle Costs: Remember that the car’s price is just one component. Factor in insurance, registration, maintenance, and fuel costs when determining your budget. Don’t borrow more than you can comfortably afford.

- Misrepresenting Information: Always be honest and accurate on your loan application. Providing false information can lead to immediate denial, legal consequences, and damage to your financial reputation.

Beyond Approval: Understanding Your Bank of the West Car Loan Terms

Getting approved for a Bank of the West car loan is a fantastic first step, but the journey doesn’t end there. Understanding the specifics of your loan agreement is crucial for managing your finances effectively and avoiding any surprises down the road.

Interest Rates (APR):

The interest rate is the cost of borrowing money, expressed as a percentage. You’ll often hear the term APR (Annual Percentage Rate), which includes the interest rate plus any additional fees charged by the lender, giving you a truer picture of the loan’s total cost. A lower APR means less money paid over the life of the loan.

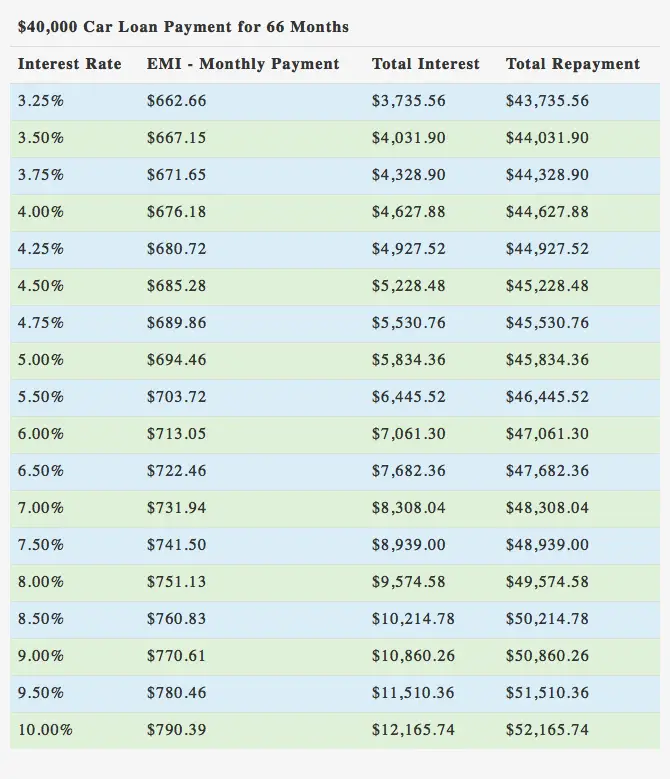

Loan Term Length:

This refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A shorter loan term means higher monthly payments but less total interest paid. Conversely, a longer term offers lower monthly payments but results in more interest paid over time. If you’re weighing the pros and cons of new vs. used cars, our guide ‘Making the Right Choice: New vs. Used Car Buying’ offers valuable insights that might influence your preferred loan term.

Monthly Payments:

Your monthly payment is the fixed amount you’ll pay to the bank each month until the loan is fully repaid. It’s vital to ensure this payment fits comfortably within your budget, alongside all your other expenses. Overextending yourself can lead to financial strain.

Additional Fees:

While Bank of the West strives for transparency, be aware of any potential fees. These could include origination fees, documentation fees, or late payment fees if you miss a due date. Always read your loan agreement carefully to understand all associated costs.

Prepayment Penalties:

Some loans include a prepayment penalty, meaning you’re charged a fee if you pay off your loan early. Thankfully, many modern auto loans, including those from reputable institutions, do not include such penalties. This allows you to pay down your principal faster and save on interest without extra charges. Confirm this detail in your loan agreement.

Refinancing Your Bank of the West Car Loan (or a loan with another lender)

Even after you’ve secured a car loan, your financial situation can change. Refinancing offers an opportunity to adjust your loan terms to better suit your current needs. It’s a strategy worth considering if certain conditions align.

When is Refinancing a Good Idea?

You might consider refinancing if interest rates have dropped since you took out your original loan, if your credit score has significantly improved, or if you need to lower your monthly payments by extending the loan term. It can also be beneficial if you want to remove a co-signer or change lenders for better service.

The Process of Refinancing:

Refinancing essentially means taking out a new loan to pay off your existing car loan. The process is similar to applying for an original loan: you’ll submit an application, provide documentation, and the lender will assess your creditworthiness. If approved, the new loan will pay off the old one, and you’ll begin making payments under the new terms.

Benefits of Refinancing with Bank of the West:

If you already have a Bank of the West car loan or are considering them for a refinance, they might offer benefits like competitive rates, familiar customer service, or streamlined processing if they already have your financial history. Always compare their refinance offers with those from other lenders to ensure you’re getting the best deal.

Bank of the West vs. Other Lenders: A Quick Comparison

While Bank of the West is a strong contender, it’s wise to understand the broader lending landscape. Different types of lenders offer distinct advantages and disadvantages.

- Traditional Banks (like Bank of the West): Often offer competitive rates for well-qualified borrowers, in-person support, and a wide range of financial products. They can be slower to approve and may have stricter eligibility requirements.

- Credit Unions: Member-owned, often known for highly competitive rates, lower fees, and personalized service. You usually need to be a member to apply, which might involve specific eligibility criteria.

- Online Lenders: Known for quick approvals, streamlined digital processes, and sometimes more flexible options for various credit profiles. They might lack the in-person support of traditional banks.

- Dealership Financing: Convenient, as you can arrange financing directly at the point of sale. Dealerships often work with multiple lenders. However, rates might not always be the most competitive, and there can be less transparency in the process.

Pro tips from us suggest always getting pre-approved from at least one or two independent lenders (like Bank of the West) before heading to the dealership. This gives you leverage and a benchmark rate to compare against any offers the dealer provides. For more general advice on car loans, you can consult trusted external sources like the Consumer Financial Protection Bureau (CFPB) auto loan guide.

Conclusion: Driving Forward with Confidence

Securing a Bank of the West car loan can be a straightforward and rewarding experience when approached with knowledge and preparation. From understanding eligibility criteria and streamlining your application to diligently comparing loan terms, every step you take contributes to a more favorable outcome. By following the advice outlined in this comprehensive guide, you’re not just applying for a loan; you’re investing in your financial future and the freedom that comes with reliable transportation.

Remember, a car loan is a significant financial commitment. Take the time to research, compare, and ask questions. Bank of the West, with its established presence and commitment to service, stands as a strong option for many. By being an informed borrower, you can confidently navigate the path to car ownership, securing a loan that truly works for you. Start your journey today by exploring their options and taking the first step towards getting behind the wheel.