Navy Fed Used Car Loan

Navy Fed Used Car Loan Carloan.Guidemechanic.com

Navigating the Road Ahead: Your Ultimate Guide to Navy Federal Used Car Loans

Navy Fed Used Car Loan

For the brave men and women who serve, and their dedicated families, financial decisions require a partner who truly understands their unique circumstances. When it comes to financing a used car, navigating the myriad of options can feel like a complex mission. Fortunately, for those affiliated with the military, Navy Federal Credit Union (NFCU) stands out as a beacon of support, offering some of the most competitive and member-centric used car loan solutions available.

Based on my extensive experience in consumer finance and working closely with military families, I’ve seen firsthand the difference a supportive lender can make. A Navy Fed Used Car Loan isn’t just a transaction; it’s a tailored financial tool designed to put you in the driver’s seat of a reliable vehicle without unnecessary stress. This in-depth guide will unravel everything you need to know, from eligibility and application tips to securing the best rates, ensuring you’re fully equipped to make an informed decision.

Why Choose Navy Federal for Your Used Car Loan?

When considering a used car loan, countless institutions vie for your attention. However, for military members, veterans, and their families, Navy Federal Credit Union often emerges as the superior choice. Their commitment to service extends far beyond traditional banking, offering distinct advantages that cater specifically to their unique membership.

One of the most compelling reasons to choose NFCU is their consistently competitive interest rates. Unlike for-profit banks, credit unions like Navy Federal operate on a not-for-profit basis, meaning any earnings are typically reinvested into the credit union to benefit members through lower loan rates and higher savings yields. This member-first approach often translates into significant savings over the life of your used car loan.

Beyond favorable rates, Navy Federal offers a level of personalized service that is truly unparalleled. Their loan officers understand the nuances of military life, including deployments, PCS moves, and fluctuating income patterns. This understanding can make the application process smoother and more empathetic, ensuring you receive a fair assessment of your financial situation. They are partners, not just lenders.

Furthermore, NFCU provides flexible loan terms designed to fit a variety of budgets and needs. Whether you prefer a shorter term to pay off your vehicle quickly or a longer term to keep monthly payments low, they work with you to find a manageable solution. This adaptability is a huge benefit, especially for those with varying financial responsibilities.

Pro tips from us: Always compare Navy Federal’s offers with at least two other lenders. While NFCU is often superior, a little comparison shopping ensures you’re getting the absolute best deal for your specific circumstances. Remember, knowledge is power when it comes to financing.

Understanding Navy Federal’s Used Car Loan Options

Navy Federal Credit Union provides a range of auto loan products, but it’s crucial to understand the distinctions, especially when it comes to financing a pre-owned vehicle. They structure their loans to address different purchasing scenarios, ensuring members have access to the right financial tool.

Generally, Navy Federal differentiates between "new" and "used" car loans primarily based on the vehicle’s age and mileage. A used car loan typically applies to vehicles that are a few years old or have a certain number of miles on the odometer. It’s essential to confirm NFCU’s specific criteria for what constitutes a "used" vehicle at the time of your application, as these parameters can sometimes influence rates and terms.

For members looking to purchase a used car, NFCU offers straightforward purchase loans. These can be used whether you’re buying from a licensed dealership or a private seller. This flexibility is a significant advantage, as private party sales can sometimes offer better value. Navy Federal’s process is designed to support both types of transactions, ensuring a smooth transfer of ownership and funds.

Beyond purchasing, Navy Federal also provides excellent refinancing options for existing used car loans. If you financed your car elsewhere and your credit score has improved, or if current interest rates are lower, refinancing with NFCU could significantly reduce your monthly payments or the total interest paid over the life of the loan. This is a smart move for many members looking to optimize their financial outflow.

Common mistakes to avoid are not checking your current loan’s terms before considering a refinance. Understand any pre-payment penalties and calculate your potential savings carefully. A little homework upfront can save you a lot of money down the line.

Eligibility Requirements for a Navy Fed Used Car Loan

Securing a Navy Fed Used Car Loan begins with meeting their fundamental eligibility criteria. While Navy Federal strives to be inclusive, certain requirements ensure responsible lending practices and protect both the member and the credit union.

The primary requirement, of course, is membership with Navy Federal Credit Union. Membership is open to all Department of Defense uniformed personnel, veterans, and their families. This includes active duty, retired, and reservist personnel from all branches of the armed forces, as well as their spouses, parents, grandparents, children, grandchildren, and even household members. If you’re not yet a member, joining is a straightforward process and a necessary first step.

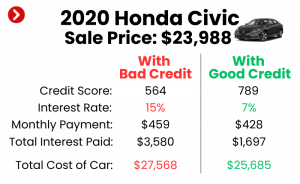

Your credit score plays a pivotal role in determining your eligibility and the interest rate you’ll receive. While NFCU considers a range of credit profiles, a higher credit score (generally 670 and above) indicates a lower risk to lenders, leading to more favorable terms. It’s wise to check your credit score and report well in advance of applying, as this gives you time to address any inaccuracies or areas for improvement.

Lenders also assess your income and debt-to-income (DTI) ratio. Your income needs to be sufficient to comfortably cover the new loan payments in addition to your existing financial obligations. A lower DTI ratio, which compares your monthly debt payments to your gross monthly income, signals a healthier financial position and increases your chances of approval.

Finally, the used vehicle itself must meet certain criteria. While specific details can vary, Navy Federal generally looks for vehicles that are not excessively old or have extremely high mileage. They also typically require a clean title, meaning the vehicle hasn’t been salvaged, rebuilt, or branded in a way that significantly diminishes its value or safety. Always confirm these vehicle-specific requirements before you fall in love with a particular car.

The Pre-Approval Advantage: Your Secret Weapon

In the world of car buying, pre-approval is not just a convenience; it’s a strategic advantage. For anyone seeking a Navy Fed Used Car Loan, securing pre-approval transforms your car shopping experience from uncertain to empowered.

What exactly is pre-approval? It’s when a lender, like Navy Federal, reviews your financial information – your credit history, income, and debt – and determines how much money they are willing to lend you for a car purchase, along with the estimated interest rate. This isn’t a final loan, but a commitment in principle, usually valid for a specific period, often 30 to 60 days.

Based on my years of guiding car buyers, pre-approval is non-negotiable for a smart purchase. It provides immense clarity, allowing you to establish a firm budget before you even step onto a dealership lot or begin searching private listings. Knowing your maximum loan amount prevents you from falling in love with a car you can’t afford, streamlining your search and saving valuable time.

The process for applying for pre-approval with Navy Federal is relatively simple. You can typically apply online, over the phone, or in person at a branch. You’ll need to provide personal information, employment details, income verification, and authorize a credit check. NFCU’s efficient system is designed to provide a quick response, often within minutes for online applications.

The benefits of pre-approval are manifold. Firstly, it gives you significant negotiating power. When a salesperson knows you have financing secured, they are more likely to offer their best price, as they understand you’re a serious buyer who can close the deal. Secondly, it speeds up the purchase process at the dealership, as you won’t be waiting for financing approval. You’re essentially shopping with cash in hand.

Pro tips from us: Even with pre-approval, always be open to the dealership’s financing offers. Sometimes, they might have special promotions or relationships with lenders that could beat your pre-approval rate. However, having your NFCU pre-approval as a baseline ensures you won’t be swayed into a less favorable deal.

Navigating the Navy Federal Used Car Loan Application Process

Applying for a Navy Fed Used Car Loan is a streamlined process designed with member convenience in mind. Whether you prefer digital efficiency or personal assistance, NFCU offers multiple avenues to submit your application.

The most common and often quickest method is the online application. Navy Federal’s secure website allows you to complete the entire application from the comfort of your home, any time of day. You’ll be prompted to enter personal details, employment history, income information, and details about the specific vehicle you intend to purchase (if you have one in mind). The online portal is user-friendly, guiding you step-by-step through the required fields.

For those who prefer a more personal touch or have questions during the process, applying over the phone is an excellent option. Navy Federal’s loan specialists are knowledgeable and can walk you through each section of the application, clarifying any doubts you might have. This method ensures you receive direct assistance and can be particularly helpful if your situation is unique or complex.

Alternatively, you can visit a Navy Federal branch in person. This allows for face-to-face interaction with a loan officer who can provide tailored advice and help you complete the application. For members who appreciate the security and reassurance of an in-person conversation, this is often the preferred choice.

Regardless of the method, you’ll need several key documents to support your application. These typically include government-issued identification (like a driver’s license), proof of income (pay stubs, W-2s, or tax returns), and potentially proof of residency. If you’ve already identified a vehicle, having its VIN (Vehicle Identification Number), mileage, and sale price ready will expedite the process.

Once you submit your application, it moves into the underwriting phase. Navy Federal’s team will review your information, credit history, and the vehicle details. This process typically moves swiftly, and you’ll receive a decision shortly thereafter. If approved, you’ll receive a loan offer detailing the interest rate, term, and monthly payment. If denied, NFCU will provide an explanation, often helping you understand what areas to improve for future applications.

Pro tips from us: To ensure a smooth application, have all your documents ready and organized before you start. This minimizes delays and ensures you can complete the process efficiently. Being prepared demonstrates your seriousness and readiness to proceed.

Getting the Best Navy Fed Used Car Loan Rates

Securing the most favorable interest rate on your Navy Fed Used Car Loan can translate into substantial savings over the life of your loan. While Navy Federal is known for competitive rates, several factors influence the specific rate you’ll be offered. Understanding these can help you position yourself for the best possible deal.

Your credit score is arguably the single most impactful factor. A higher credit score signals to Navy Federal that you are a low-risk borrower, making you eligible for their lowest advertised rates. Individuals with excellent credit (typically 740+) will almost always receive better rates than those with fair or good credit. Prioritizing credit health before applying is paramount.

The length of your loan term also plays a significant role. Generally, shorter loan terms come with lower interest rates. This is because the lender takes on less risk over a shorter period. While a longer term might offer a lower monthly payment, it almost always results in paying more interest overall. Carefully weigh your budget against the total cost of the loan.

Making a sizable down payment can also help you secure a better rate. A larger down payment reduces the amount you need to borrow, thereby decreasing the lender’s risk. It shows financial stability and commitment, which can be rewarded with more attractive interest rates. Aim for at least 10-20% of the vehicle’s purchase price if possible.

In some cases, having a co-signer or co-borrower with excellent credit can improve your chances of approval and help you qualify for a lower rate, especially if your own credit score isn’t as strong. This individual shares responsibility for the loan, mitigating risk for the lender. However, ensure both parties understand the full implications of co-signing.

Finally, keep an eye out for any special promotions or discounts Navy Federal might offer. They occasionally run limited-time offers that could further reduce rates or provide other benefits. Checking their website or speaking with a loan officer about current promotions can sometimes yield unexpected savings.

In my experience, even a slight improvement in your credit score or a strategic increase in your down payment can shave off significant interest over the life of a Navy Fed Used Car Loan. Every percentage point matters. For more details on improving your credit score, check out our guide on .

Common Mistakes to Avoid When Applying

Even with the best intentions, applicants can sometimes make missteps that hinder their chances of securing a Navy Fed Used Car Loan or lead to less favorable terms. Being aware of these common pitfalls can help you navigate the process more effectively.

One of the most common mistakes is not checking your credit score and report before applying. Many individuals underestimate the impact of their credit history. Discovering errors or negative marks only after a loan denial can be frustrating. Always pull your free credit reports from AnnualCreditReport.com and review them thoroughly. Addressing issues proactively can significantly improve your application’s outcome.

Another pitfall is applying to too many lenders in a short period. Each loan application typically results in a "hard inquiry" on your credit report, which can temporarily lower your credit score. While comparison shopping is smart, limit your applications to a few key lenders you’ve researched, such as Navy Federal, to avoid unnecessary dings to your credit.

Ignoring the fine print is another error that can lead to unexpected issues down the road. Always take the time to thoroughly read and understand the terms and conditions of your loan offer. Pay close attention to the interest rate, loan term, any fees, and prepayment penalties. If anything is unclear, ask questions until you’re fully satisfied.

Buying more car than you can truly afford is a pervasive mistake. It’s easy to get carried away by the allure of a shiny, expensive vehicle. However, sticking to a realistic budget based on your income and existing expenses is crucial. A car payment should not strain your finances or prevent you from meeting other obligations.

Finally, many applicants focus solely on the monthly payment and forget about the additional costs of car ownership. Insurance, registration fees, maintenance, and fuel all add up. One of the most common mistakes is not factoring in all the associated costs, leading to buyer’s remorse later on. Always consider the total cost of ownership when budgeting for your used vehicle.

Post-Approval: What to Do Next

Congratulations, your Navy Fed Used Car Loan is approved! This is an exciting moment, but the journey isn’t quite over. There are a few crucial steps to take after approval to ensure a smooth and successful car purchase and ownership experience.

First and foremost, if you haven’t already, arrange for a pre-purchase inspection of the used vehicle by a trusted, independent mechanic. Even if the car looks pristine, a professional inspection can uncover hidden issues, saving you from costly repairs down the line. This step is particularly vital for used vehicles, where past maintenance and accident history can significantly impact reliability.

Next, carefully review all your loan documents before signing. This includes the promissory note, disclosure statements, and any other agreements. Confirm that the interest rate, loan term, monthly payment, and total loan amount match what you were approved for. Don’t hesitate to ask your Navy Federal loan officer any lingering questions. Understanding every detail of your commitment is paramount.

Once the deal is finalized, set up your loan payments. Navy Federal often offers convenient options like automatic payments, which can help you avoid late fees and maintain a good payment history. Setting up auto-pay from your checking or savings account ensures your payments are always made on time, building your credit and financial reliability.

Finally, remember that your relationship with Navy Federal doesn’t necessarily end with your initial loan. As your financial situation evolves or market rates change, you might consider refinancing your used car loan again in the future. If your credit score improves significantly, or if interest rates drop, a refinance could lead to even greater savings. Stay informed about NFCU’s current offerings and your own financial standing.

If you’re still deciding between a new or used car, our article offers a detailed comparison to help you make the best choice for your needs. For general information about vehicle maintenance and ownership, you might find valuable resources at a trusted automotive consumer site, such as Edmunds.com, which provides extensive guides and reviews to help car owners make informed decisions.

Conclusion: Driving Forward with Confidence

Securing a Navy Fed Used Car Loan offers a clear path to vehicle ownership, backed by an institution that truly understands and supports its military members and their families. From their competitive rates and flexible terms to their member-centric service and straightforward application process, Navy Federal stands as an exemplary partner in your car-buying journey.

By understanding the eligibility requirements, leveraging the power of pre-approval, and diligently navigating the application, you can position yourself for the most favorable loan terms. Remember, proactive preparation, from checking your credit to understanding the total cost of ownership, is your strongest ally in this process.

Based on my professional insights, choosing Navy Federal for your used car financing is more than just a financial decision; it’s an investment in peace of mind. They provide the tools and support you need to drive away with confidence, knowing you’ve secured a loan that respects your service and your financial well-being. Don’t hesitate to explore their offerings today and embark on your next adventure with the right vehicle and the right financial partner.