Navy Federal Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Navy Federal Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect, but navigating the world of auto loans can often feel overwhelming. For military members, veterans, and their families, Navy Federal Credit Union (NFCU) stands out as a highly trusted financial institution, often celebrated for its competitive Navy Federal car loan rates. This comprehensive guide will peel back every layer, providing you with an in-depth understanding of how NFCU’s auto loans work, how to secure the best rates, and what makes them a preferred choice for so many.

Our goal is to equip you with the knowledge needed to make an informed decision, ensuring you not only understand your options but also feel confident in your pursuit of the perfect car loan. We’ll delve into everything from eligibility and application processes to rate-influencing factors and the unique benefits NFCU offers its dedicated members. Let’s hit the road!

Navy Federal Car Loan Rates: Your Ultimate Guide to Driving Away with the Best Deal

Understanding Navy Federal Car Loan Rates: The Core Mechanics

When you’re considering financing a vehicle, the interest rate is arguably the most critical factor. It directly impacts your monthly payment and the total cost of your car over the loan’s lifetime. Navy Federal Credit Union is renowned for offering rates that are often significantly lower than those found at traditional banks or dealership financing departments. This member-centric approach is a cornerstone of their mission.

The rates offered by NFCU aren’t static; they are dynamic and influenced by several key elements. These include your creditworthiness, the specific loan term you choose, whether you’re buying a new or used vehicle, and even the loan-to-value ratio. Understanding these components is your first step toward securing an optimal deal.

New vs. Used Car Loan Rates at NFCU

One of the most immediate distinctions you’ll notice when exploring Navy Federal car loan rates is the difference between financing a new car versus a used one. Generally, new car loans tend to come with slightly lower interest rates. This is primarily because new vehicles are considered less of a risk for lenders; they haven’t depreciated significantly, and their condition is pristine.

Used car loans, while still very competitive at NFCU, typically carry a slightly higher interest rate. This reflects the increased risk associated with older vehicles, which may have more mileage, potential wear and tear, and a higher chance of needing repairs. However, NFCU still strives to provide excellent used car rates, especially for well-maintained, newer model used vehicles. It’s always worth checking their current offerings for both categories.

Loan Terms and Their Impact on Your Rate

The length of your car loan, known as the loan term, plays a crucial role in determining both your monthly payment and the interest rate you receive. NFCU offers a variety of terms, typically ranging from 36 months up to 84 months, depending on the vehicle type and amount financed. Choosing a shorter loan term, such as 36 or 48 months, generally results in a lower interest rate because the lender’s risk is reduced over a shorter period.

While shorter terms mean higher monthly payments, you’ll pay significantly less in total interest over the life of the loan. Conversely, opting for a longer term, like 72 or 84 months, will reduce your monthly payment, making the car more "affordable" on a month-to-month basis. However, this convenience comes at a cost: a slightly higher interest rate and a much larger total interest paid over the extended period. Pro tips from us: Always weigh the benefits of a lower monthly payment against the long-term cost of interest.

Who Qualifies? Navy Federal Membership & Eligibility

Before you even start thinking about Navy Federal car loan rates, the absolute first step is to ensure you meet their membership eligibility requirements. Unlike traditional banks, NFCU is a credit union, meaning it’s a member-owned financial cooperative. Membership is restricted to specific groups, primarily those affiliated with the U.S. armed forces and their families.

Eligibility extends to all active duty, retired, and veteran members of the Army, Marine Corps, Navy, Air Force, Coast Guard, and Space Force. Additionally, Department of Defense (DoD) civilian employees, contractors, and even their immediate family members (parents, grandparents, spouses, siblings, children, grandchildren) are eligible to join. This broad eligibility ensures a wide community can benefit from their services. Common mistakes to avoid are assuming that any federal employee or someone without a direct military tie can join; you must fall within their specified criteria.

The Application Process: Step-by-Step for a Navy Federal Auto Loan

Applying for a Navy Federal auto loan is designed to be a straightforward and user-friendly experience, whether you choose to do it online, over the phone, or in person at a branch. Based on my experience, their online application is particularly efficient and often provides a quick decision.

Here’s a breakdown of the typical steps:

- Gather Your Information: Before you begin, have essential documents ready. This includes proof of identity (driver’s license, military ID), income verification (pay stubs, W-2s), and details about the vehicle you intend to purchase (if known). If you’re applying for pre-approval, vehicle specifics aren’t always necessary at this initial stage.

- Choose Your Application Method: You can apply directly through the NFCU website, call their member service line, or visit a local branch. Each method offers the same access to their loan products.

- Complete the Application: Fill out the required information accurately and completely. This will typically include your personal details, employment history, income, and housing information.

- Await Decision: NFCU prides itself on quick decision-making, often providing an answer within minutes for online applications. If approved, you’ll receive your loan offer, including your approved rate and maximum loan amount.

- Get Pre-Approved: Pro tips from us: Always aim for pre-approval before you step onto a dealership lot. A pre-approval letter gives you significant leverage in negotiations, allowing you to focus on the car price rather than worrying about financing. It also clearly outlines your budget, preventing you from overspending.

Key Factors Influencing Your Navy Federal Car Loan Rate

While membership gets you in the door, several critical factors will ultimately determine the specific Navy Federal car loan rates you qualify for. Understanding these can empower you to improve your standing and secure the best possible terms.

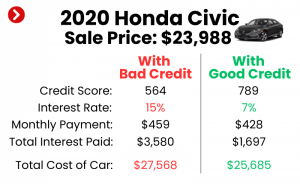

Your Credit Score: The Ultimate Indicator

Your credit score is arguably the most significant factor lenders consider. It’s a numerical representation of your creditworthiness, reflecting your history of borrowing and repayment. A higher credit score (typically FICO scores above 700) indicates to NFCU that you are a reliable borrower, leading to lower interest rates. Conversely, a lower score might result in a higher rate to offset the perceived risk.

Based on my experience, consistently paying bills on time, keeping credit utilization low, and avoiding new unnecessary credit applications in the months leading up to your loan application can significantly boost your score. It’s always a good idea to check your credit report well in advance to correct any errors.

Debt-to-Income (DTI) Ratio

Your debt-to-income (DTI) ratio is another crucial metric. It compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage additional monthly payments. A lower DTI ratio (typically below 36%) signals that you have more disposable income to cover your car loan, making you a less risky borrower. This can positively influence your approved interest rate.

Loan-to-Value (LTV)

The loan-to-value (LTV) ratio compares the loan amount to the actual value of the vehicle you’re purchasing. A lower LTV, which usually comes from making a larger down payment, is favorable to lenders. If you put down a significant amount, you’re borrowing less money relative to the car’s worth, reducing the lender’s exposure. A lower LTV can translate into a better interest rate.

Vehicle Specifics

The characteristics of the vehicle itself also play a role. Newer vehicles, especially those with lower mileage, generally pose less risk to the lender because they hold their value better and are less likely to require immediate costly repairs. Older vehicles, or those with very high mileage, might be seen as a higher risk, potentially leading to slightly higher rates or stricter lending criteria.

Beyond the Rate: Other Benefits of a Navy Federal Auto Loan

While competitive Navy Federal car loan rates are a primary draw, NFCU offers a suite of other benefits that enhance the overall value proposition for its members. These advantages often go beyond just the numbers, creating a more supportive and flexible borrowing experience.

One significant benefit is their exceptional customer service. Members frequently praise NFCU for its responsive, knowledgeable, and helpful representatives who are always ready to assist with questions or concerns throughout the loan process. This personalized support can make a big difference, especially for first-time car buyers or those new to auto financing.

NFCU also offers special programs and discounts. For instance, they might partner with car-buying services that provide pre-negotiated pricing and a streamlined purchasing experience, potentially saving members time and money on the vehicle itself. They also offer competitive rates for motorcycle, RV, and boat loans, making them a one-stop shop for various vehicle financing needs. Importantly, NFCU typically imposes no prepayment penalties, meaning you can pay off your loan early without incurring extra fees, saving you on interest.

Refinancing Your Auto Loan with Navy Federal

Even if you already have a car loan, you might be able to take advantage of competitive Navy Federal car loan rates by refinancing your existing debt. Refinancing means replacing your current auto loan with a new one, ideally with better terms.

When is the right time to consider refinancing? If interest rates have dropped since you originally financed your car, if your credit score has significantly improved, or if you want to lower your monthly payments by extending the loan term (though remember the total interest cost implications). Refinancing can also be beneficial if you’re looking to remove a co-signer or consolidate debt.

The process for refinancing with NFCU is similar to applying for a new loan. You’ll apply for a new auto loan, and if approved, NFCU will pay off your old loan, and you’ll begin making payments to them under the new, hopefully more favorable, terms. This can be a smart financial move for many members. For more in-depth insights into whether refinancing is right for you, check out our article on When is the Right Time to Refinance Your Car Loan? (Internal Link)

How to Secure the Best Navy Federal Car Loan Rates

While NFCU offers competitive rates across the board, there are strategic steps you can take to ensure you secure the absolute best Navy Federal car loan rates available to you. These actions can significantly impact your financial outcome.

- Improve Your Credit Score: As discussed, a higher credit score is your most powerful tool. Regularly monitor your credit report, dispute any inaccuracies, pay all bills on time, and reduce your credit card balances.

- Save for a Larger Down Payment: A substantial down payment reduces the amount you need to borrow, lowering your LTV ratio. This signals less risk to NFCU and can result in a better interest rate.

- Choose a Shorter Loan Term: If your budget allows, opting for a shorter loan term (e.g., 36 or 48 months) will typically secure a lower interest rate compared to longer terms, saving you considerable money in total interest.

- Consider a Co-signer: If your credit isn’t as strong as you’d like, a co-signer with excellent credit can help you qualify for a better rate. However, ensure both parties understand the responsibilities involved.

- Negotiate the Car Price: Your loan amount is directly tied to the car’s purchase price. The lower the price you negotiate with the dealer, the less you’ll need to borrow, which can indirectly influence the overall affordability and perception of risk.

- Pro Tip: Even if you’re committed to NFCU, it’s always wise to compare their offer with a few other lenders. This ensures you’re truly getting the most competitive rate available at that moment.

Common Mistakes to Avoid When Applying for a Navy Federal Car Loan

Even with the best intentions, applicants can sometimes make missteps that hinder their chances of securing optimal Navy Federal car loan rates. Being aware of these common errors can help you navigate the process smoothly.

- Not Checking Your Credit Score First: Many people apply without knowing their credit standing. This can lead to surprises, disappointment, or missed opportunities to improve their score before applying. Always get a clear picture of your credit report.

- Applying for Too Many Loans at Once: Each loan application can result in a "hard inquiry" on your credit report, which can temporarily lower your score. Spreading out applications too widely or too quickly can negatively impact your credit.

- Focusing Only on Monthly Payment: While a low monthly payment is appealing, it often comes with a longer loan term and more interest paid over time. Always consider the total cost of the loan, not just the monthly figure.

- Skipping Pre-approval: As mentioned earlier, not getting pre-approved removes your strongest negotiation tool at the dealership. You walk in less prepared and more susceptible to dealer-arranged financing, which might not be as favorable.

- Ignoring the Fine Print: Always read all loan documents carefully. Understand the terms, conditions, fees, and any potential penalties before signing. Don’t be afraid to ask questions.

Comparing Navy Federal Car Loan Rates to Other Lenders

While Navy Federal car loan rates are often exceptionally competitive, it’s a smart financial practice to comparison shop. This doesn’t mean you won’t choose NFCU, but it ensures you’ve explored all your options and are confident you’re getting the best deal.

Credit unions like Navy Federal generally offer lower rates than traditional big banks because they are non-profit organizations focused on member benefits. Dealership financing can sometimes be competitive, especially with manufacturer incentives, but these offers often come with strict eligibility requirements and may not always be the best long-term solution.

Based on my experience, NFCU consistently provides excellent value due to its combination of competitive rates, flexible terms, and outstanding member service. However, a quick comparison with one or two other reputable lenders or even an online aggregator can provide peace of mind. For a broader view of auto loan rates across different lenders, you can consult reliable financial resources like NerdWallet’s Auto Loan Guide (External Link).

Real-World Experience: What Members Say

Based on my experience and consistent feedback from numerous members, Navy Federal Credit Union consistently delivers on its promise of competitive Navy Federal car loan rates and an overall superior borrowing experience. Many members recount stories of receiving lower rates at NFCU than anywhere else, even with similar credit profiles.

The seamless application process, often culminating in a quick pre-approval, empowers members to shop for their vehicles with confidence. Furthermore, the commitment to member education and support, from understanding loan terms to exploring refinancing options, truly sets NFCU apart. It’s not just about the rate; it’s about the comprehensive support system they provide to their military community.

Driving Away with Confidence: Your Navy Federal Car Loan Journey

Navigating the world of car loans doesn’t have to be a daunting task, especially when you have a trusted partner like Navy Federal Credit Union. By understanding the factors that influence Navy Federal car loan rates, proactively managing your credit, and taking advantage of their member-centric services, you can position yourself to secure an excellent deal.

From new car purchases to refinancing an existing loan, NFCU offers a compelling suite of options tailored to the unique needs of the military community. Remember to leverage pre-approval, compare your options, and always read the fine print. With this comprehensive guide, you’re now well-equipped to make an informed decision and drive away with confidence, knowing you’ve secured one of the best possible Navy Federal car loan rates for your next vehicle. Start your journey today and experience the difference of banking with a credit union that truly serves those who serve our nation.