Need A Car Loan? Your Ultimate Guide to Navigating Auto Financing with Confidence

Need A Car Loan? Your Ultimate Guide to Navigating Auto Financing with Confidence Carloan.Guidemechanic.com

The open road beckons, promising freedom, convenience, and new adventures. For many, a car isn’t just a luxury; it’s a vital part of daily life, connecting them to work, family, and opportunities. However, the path to vehicle ownership often involves a significant financial decision: securing a car loan.

If you find yourself thinking, "I need a car loan," you’re in good company. Millions of people finance their vehicles every year. Navigating the world of auto financing can feel daunting, filled with unfamiliar terms, varying interest rates, and a multitude of options.

Need A Car Loan? Your Ultimate Guide to Navigating Auto Financing with Confidence

This comprehensive guide is designed to demystify the entire process, empowering you with the knowledge to make informed decisions. We’ll explore everything from understanding your financial readiness to securing the best possible loan terms. Our goal is to transform your apprehension into confidence, ensuring you get behind the wheel with a clear understanding of your auto loan.

Understanding Why You Might Need A Car Loan

The decision to purchase a vehicle is a major one, often representing the second-largest purchase most individuals make after a home. While paying cash upfront might seem ideal, it’s simply not a realistic option for the vast majority of car buyers. This is where car loans step in, bridging the gap between your immediate financial resources and the cost of your desired vehicle.

A car loan allows you to acquire a vehicle today while spreading its cost over an extended period. This financial tool makes vehicle ownership accessible, enabling you to manage payments through manageable monthly installments. Essentially, you’re borrowing money from a lender and agreeing to repay it, plus interest, over a predetermined loan term.

Based on my experience, many people need a car loan not just for convenience, but as a necessity for employment, family responsibilities, or simply maintaining a decent quality of life. Understanding that auto financing is a common and legitimate financial strategy is the first step toward approaching it with confidence. It’s a structured way to achieve a significant goal without depleting your savings.

The Pre-Loan Checklist: Are You Ready to Apply?

Before you even begin looking at cars or speaking with lenders, taking a crucial step back to assess your financial readiness is paramount. This proactive approach will save you time, reduce stress, and significantly improve your chances of securing favorable car loan approval. Skipping this vital stage is a common mistake that can lead to disappointment.

Assessing Your Financial Health

First, take an honest look at your current financial situation. This involves evaluating your income, existing debts, and monthly expenses. You need to determine how much car payment you can comfortably afford each month without straining your budget. Remember, the car payment is just one piece of the puzzle.

You also need to factor in potential increases in car insurance, fuel costs, maintenance, and registration fees. A common mistake to avoid is focusing solely on the monthly car payment. Pro tips from us: create a detailed budget that includes all potential car-related expenses to get a true picture of affordability.

Understanding Your Credit Score

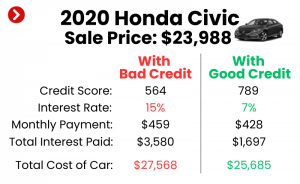

Your credit score is arguably the most critical factor lenders consider when you need a car loan. It’s a three-digit number that reflects your creditworthiness and your history of managing debt. A higher credit score typically translates to lower interest rates and better loan terms.

Before applying, obtain a free copy of your credit report from one of the three major credit bureaus (Experian, Equifax, TransUnion). Review it carefully for any errors that could negatively impact your score. If you find discrepancies, dispute them immediately to ensure your report is accurate. Understanding your score helps you anticipate the type of car loan interest rates you might qualify for.

Different Types of Car Loans: Finding Your Best Fit

Not all car loans are created equal. Understanding the various options available is crucial for making an informed decision that aligns with your financial goals and the type of vehicle you intend to purchase. Your choice of loan type can significantly impact your interest rate, monthly payment, and overall cost.

New vs. Used Car Loans

The most fundamental distinction lies between loans for new vehicles and those for pre-owned ones. New car loans often come with slightly lower interest rates due to the lower perceived risk for lenders; new cars typically hold their value better initially and have fewer immediate mechanical issues. Lenders see them as more secure collateral.

Conversely, used car loans can have slightly higher interest rates, especially for older models or those with high mileage. This is because used cars carry a higher risk of depreciation and potential mechanical problems. However, the overall purchase price of a used car is lower, which means you might borrow less money, making the monthly payments more manageable. When you need a car loan for a used vehicle, lenders might also impose age or mileage restrictions.

Dealer Financing vs. Bank/Credit Union Loans

When considering car financing, you generally have two main avenues: obtaining a loan directly from the dealership or securing one through an independent financial institution like a bank or credit union.

Dealer financing offers convenience, as you can complete the purchase and financing in one location. Dealerships often work with multiple lenders and may offer special promotional rates, but these are not always the best deals for every buyer. It’s their job to sell you a car and financing.

Banks and credit unions, on the other hand, can offer competitive rates, especially if you have an existing relationship with them. Pro tips from us: getting pre-approved car loan offers from a few banks or credit unions before visiting a dealership gives you significant leverage. This allows you to walk into the dealership knowing your financing options and prevents you from accepting a less favorable rate on the spot. Credit unions, in particular, are known for their customer-centric approach and often provide excellent rates.

Personal Loans vs. Secured Auto Loans

Most car loans are secured loans, meaning the vehicle itself acts as collateral. If you default on the loan, the lender can repossess the car. This reduces the lender’s risk, often leading to lower interest rates.

A personal loan, conversely, is typically unsecured. While you could use a personal loan to buy a car, its interest rates are usually much higher because there’s no collateral backing the loan. Based on my experience, it’s generally not advisable to use a personal loan for a car purchase unless you have no other options or are buying a very inexpensive car and have an excellent credit score.

The Application Process: What Lenders Look For

Once you’ve done your homework and understand your options, it’s time for the auto loan application. This stage requires precision and preparation. Lenders have specific criteria they use to assess your eligibility and determine the terms of your loan. Understanding these factors will significantly improve your chances of car loan approval.

Key Factors for Car Loan Approval

Lenders scrutinize several key areas to gauge your ability and willingness to repay the loan:

- Credit Score: As mentioned, this is paramount. A higher score (generally 670 and above) indicates a lower risk, leading to better car loan interest rates. Scores below this might still get approval but with higher rates, sometimes categorized as bad credit car loan options.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. Lenders prefer a lower DTI, typically below 43%, as it indicates you have enough disposable income to handle additional loan payments. A high DTI suggests you might be overextended financially.

- Income Stability: Lenders want assurance that you have a steady and reliable income source. This often means consistent employment history and sufficient income to cover the proposed monthly payments. They look for predictability in your financial situation.

- Down Payment: Making a significant down payment reduces the amount you need to borrow and lowers the lender’s risk. A larger down payment can often lead to better loan terms and a lower monthly payment. Pro tips from us: aim for at least 10-20% of the vehicle’s purchase price if possible.

- Vehicle Type and Age: The car itself plays a role. Newer, more reliable vehicles are often seen as better collateral than older, high-mileage cars. This is particularly relevant if you need a car loan for a vintage or specialty vehicle, where lenders might be more cautious.

Essential Documents You’ll Need

Having your documents organized beforehand will streamline the car loan application process. Lenders will typically require:

- Proof of Identity: Government-issued photo ID (driver’s license, passport).

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2 forms, or tax returns (if self-employed).

- Proof of Residency: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Vehicle Information (if applicable): Make, model, year, VIN, and purchase price of the car you intend to buy.

Common mistakes to avoid are showing up without all necessary paperwork, which can cause significant delays. Gather these documents early to present a complete and professional application.

Navigating Interest Rates and Terms: What to Expect

When you need a car loan, the interest rate and loan term are two of the most critical components that determine the total cost of your financing. Understanding how these factors interact is essential for making a sound financial decision. It’s not just about the monthly payment; it’s about the entire financial commitment.

How Interest Rates Are Determined

Your car loan interest rates are influenced by several factors, primarily your credit score, the loan term, the specific lender, and current market conditions. Individuals with excellent credit scores will typically qualify for the lowest rates because they pose the least risk to lenders. Conversely, those with lower scores, especially in bad credit car loan scenarios, will face higher rates to compensate lenders for the increased risk.

The loan term also plays a role; shorter terms often have slightly lower rates than longer ones. Additionally, different lenders, whether banks, credit unions, or captive finance companies (associated with car manufacturers), will offer varying rates based on their own risk assessments and business models.

Fixed vs. Variable Rates

Most auto loans come with a fixed interest rate, meaning your rate and monthly payment remain constant throughout the loan term. This provides stability and predictability for your budget. While less common for car loans, some lenders might offer variable rates, where the rate can fluctuate with market conditions. Based on my experience, fixed-rate loans are almost always preferred for auto financing due to their stability.

Loan Term (36, 48, 60, 72 Months)

The loan term, expressed in months, dictates how long you have to repay the loan. Common terms range from 36 to 72 months, with some extending even longer.

- Shorter Terms (e.g., 36-48 months): These result in higher monthly payments but mean you pay less interest over the life of the loan. You own the car outright faster.

- Longer Terms (e.g., 60-72 months+): These offer lower monthly payments, making the car seem more affordable upfront. However, you’ll pay significantly more in total interest over the longer period. You also risk owing more than the car is worth (being "upside down") for a longer time, especially with rapid depreciation of new cars.

Pro tips from us: don’t just look at the monthly payment. Calculate the total cost of the loan, including all interest, for different terms. This will reveal the true financial impact of extending your loan.

APR vs. Interest Rate

While often used interchangeably, the Annual Percentage Rate (APR) provides a more comprehensive picture than the simple interest rate. The interest rate is the cost of borrowing money. The APR includes the interest rate plus any additional fees charged by the lender, such as origination fees or processing fees, expressed as an annual percentage. Always compare APRs when evaluating loan offers, as it gives you the truest measure of the total annual cost of the loan.

Special Considerations: Bad Credit Car Loans

Having a less-than-perfect credit score doesn’t automatically mean you can’t get a car loan. It simply means the process might be different, and you’ll need to be more strategic. If you need a car loan but have a low credit score, understanding your options is key to avoiding predatory lending and securing the best possible terms.

Lenders view a low credit score as an indicator of higher risk. Consequently, bad credit car loan options typically come with higher interest rates to compensate the lender for that increased risk. This means your monthly payments and the total cost of the loan will be higher compared to someone with excellent credit.

Here are some strategies for securing a car loan with bad credit:

- Co-signer: A co-signer with good credit can significantly improve your chances of approval and help you secure a lower interest rate. The co-signer essentially guarantees the loan, taking on equal responsibility for repayment if you default.

- Larger Down Payment: Offering a substantial down payment reduces the amount you need to borrow and lessens the lender’s risk. This can make you a more attractive borrower, even with a lower credit score.

- Subprime Lenders: There are lenders who specialize in working with individuals with bad credit. While their rates will be higher, they might be your best option for approval. Be sure to research these lenders thoroughly and read reviews.

- Secured Auto Loans: As discussed, most car loans are secured. This is particularly beneficial for bad credit borrowers as the collateral (the car) reduces the lender’s risk.

- Improve Your Credit First: If possible, take some time to improve your credit score before applying. Paying down existing debts, disputing errors on your credit report, and making all payments on time can make a significant difference. For a deeper dive into improving your credit score, check out our guide on .

Remember, a bad credit car loan can be an opportunity to rebuild your credit if you make all payments on time. However, carefully consider the higher costs involved and ensure the payments are truly affordable within your budget.

Pro Tips for Securing the Best Car Loan Deal

Navigating the car loan market requires strategy and preparation. Don’t simply accept the first offer you receive. Based on my years in the industry, taking a proactive approach can save you thousands of dollars over the life of your loan. Here are some expert tips to help you get the most favorable terms when you need a car loan:

- Get Pre-Approved Before Visiting a Dealership: This is perhaps the most crucial tip. Obtain pre-approved car loan offers from banks, credit unions, and online lenders before you even step foot on a car lot. This gives you a clear understanding of the interest rate and loan amount you qualify for. You’ll know your buying power and can negotiate with the dealership from a position of strength, treating their financing offer as a comparison rather than your only option.

- Shop Around for Lenders: Don’t limit yourself to just one lender. Apply to several financial institutions – banks, credit unions, and online lenders. Each lender has different criteria and risk assessments, leading to varying interest rates and terms. Comparing multiple offers allows you to choose the best deal available for your specific situation.

- Negotiate the Car Price Separately from the Financing: Dealerships often try to bundle the car price and financing into one discussion. Insist on negotiating the vehicle’s purchase price first. Once you’ve agreed on a price, then discuss financing. This prevents them from manipulating numbers to make a less favorable financing deal seem attractive by adjusting the car’s price.

- Understand All Fees: Beyond the interest rate, car loans can come with various fees, such as origination fees, documentation fees, or processing fees. Always ask for a complete breakdown of all costs associated with the loan. These fees can add to your total loan amount and impact your effective APR.

- Read the Fine Print: Before signing any loan agreement, meticulously read every detail. Understand the full loan term, the APR, any prepayment penalties (though rare for auto loans), and late payment fees. Ensure there are no hidden clauses or unexpected charges. If anything is unclear, ask for clarification. Don’t be rushed.

- Consider a Shorter Loan Term (If Affordable): While longer terms offer lower monthly payments, they significantly increase the total interest paid over time. If your budget allows, opting for a shorter loan term will save you money in the long run. Use online calculators to compare total costs for different terms.

The Consumer Financial Protection Bureau offers excellent resources on understanding auto loans and provides tools to help consumers make informed decisions. Visit their website at https://www.consumerfinance.gov/consumer-tools/auto-loans/ for more valuable information.

Common Car Loan Mistakes to Avoid

Even with all the information available, certain pitfalls seem to catch borrowers off guard repeatedly. Based on my years in the industry, these are recurring mistakes that can cost you significant money and stress when you need a car loan. Being aware of them is the first step toward avoiding them.

- Not Checking Your Credit Score: As emphasized, your credit score is the foundation of your loan offer. Failing to check it means you go into negotiations blind. You won’t know if an offer is fair or if there are errors on your report that could be easily fixed. This oversight can lead to higher interest rates than you deserve.

- Focusing Only on the Monthly Payment: This is perhaps the most common mistake. Salespeople are experts at making a car seem affordable by stretching out the loan term to achieve a low monthly payment. While the monthly figure is important for budgeting, it’s crucial to also consider the total cost of the loan, including all interest paid over the entire term. A low monthly payment on a long term often means paying significantly more overall.

- Skipping Pre-Approval: Going to a dealership without a pre-approved car loan offer puts you at a disadvantage. Without knowing what you qualify for elsewhere, you’re more likely to accept whatever financing the dealership offers, which may not be the best rate. Pre-approval gives you negotiating power and a benchmark.

- Not Comparing Offers: Never settle for the first loan offer you receive. Just as you’d shop for the best car price, you should shop for the best loan. Different lenders will have different rates and terms based on their risk assessment and business models. Comparing multiple offers ensures you’re getting the most competitive rate available to you.

- Buying More Car Than You Can Afford: It’s easy to get swept up in the excitement of a new vehicle and stretch your budget beyond what’s comfortable. Remember to factor in not just the loan payment, but also insurance, fuel, maintenance, and potential repairs. Overextending yourself financially can lead to stress and potential default. Pro tips from us: stick to your pre-determined budget.

- Not Understanding the Terms and Conditions: Rushing through the paperwork and signing without fully understanding the loan agreement can lead to unwelcome surprises later. Always ask questions, clarify anything confusing, and ensure you comprehend every clause before committing.

By consciously avoiding these common errors, you can navigate the car loan process more effectively and secure financing that truly works in your favor.

Conclusion: Drive Away with Confidence

The journey to vehicle ownership, particularly when you need a car loan, doesn’t have to be a stressful ordeal. By equipping yourself with knowledge, understanding the various options, and approaching the process strategically, you can transform a complex financial decision into a confident and empowered one. From assessing your credit score to comparing lender offers and understanding the fine print, every step you take contributes to securing a loan that fits your financial landscape.

Remember, a car loan is a significant commitment, and taking the time to prepare and make informed choices will benefit you greatly in the long run. You now have the tools to navigate interest rates, understand loan terms, and avoid common pitfalls. Drive away not just with a new vehicle, but with the peace of mind that comes from a well-understood and carefully chosen financial decision.

If you’re also considering whether to buy new or used, read our comprehensive article on for more insights before making your final purchase decision. Happy driving!