Need a Used Car Loan? Unlock the Secrets to Approval, Best Rates, and Stress-Free Financing

Need a Used Car Loan? Unlock the Secrets to Approval, Best Rates, and Stress-Free Financing Carloan.Guidemechanic.com

The open road beckons, and for many, a reliable vehicle is not just a luxury but a necessity. While the allure of a brand-new car is undeniable, a used car often presents a smarter, more economical choice. It allows you to get more car for your money, often with many desirable features, without the steep depreciation hit new vehicles face.

However, even with the savings a pre-owned vehicle offers, most people still need a used car loan to make that purchase a reality. Navigating the world of automotive financing can feel daunting, filled with jargon and countless options. You might be asking: Where do I even begin? What do lenders look for? How can I secure the best rates?

Need a Used Car Loan? Unlock the Secrets to Approval, Best Rates, and Stress-Free Financing

As an expert blogger and professional SEO content writer who has guided countless individuals through the complexities of automotive financing, I understand these challenges deeply. This comprehensive guide is designed to demystify the process, providing you with the knowledge and strategies you need to secure a fantastic used car loan. Our ultimate goal is to equip you with the insights to confidently drive away in your desired vehicle, without financial stress.

Why a Used Car is a Smart Choice (and Why You’ll Likely Need a Loan)

Opting for a used car can be one of the savviest financial decisions you make. New cars lose a significant portion of their value the moment they’re driven off the lot, a phenomenon known as depreciation. This rapid decline continues for the first few years, meaning a pre-owned vehicle has already absorbed the steepest part of this cost.

This translates directly into savings for you. A used car typically comes with a lower purchase price, which can lead to lower sales tax, reduced insurance premiums, and, most importantly, a more manageable loan amount. You can often afford a higher trim level or a more premium brand as a used vehicle than you could if buying new.

Despite these significant savings, the reality is that most people still require financing to purchase a used car. The average cost of a used vehicle, while lower than new, still represents a substantial investment for many households. This is precisely where understanding how to need a used car loan comes into play. It bridges the gap between your savings and the total cost of your chosen vehicle, making car ownership accessible.

Understanding Your Used Car Loan Options

When you need a used car loan, you’re not limited to a single path. A variety of lenders offer different types of financing, each with its own set of advantages and disadvantages. Knowing your options empowers you to make an informed decision and find the best fit for your financial situation.

1. Dealership Financing:

Many car dealerships offer in-house financing or work with a network of banks and credit unions. This can be incredibly convenient, allowing you to handle the car purchase and loan application all in one place. The dealership acts as an intermediary, submitting your application to multiple lenders on your behalf.

Pros: Convenience, one-stop shopping, potential for special offers or incentives, especially if the dealership wants to move a particular vehicle. They can often work with a wide range of credit scores.

Cons: Interest rates might be higher as the dealership often adds a markup. You might feel pressured to accept the first offer, and comparing rates can be difficult if you’re not pre-approved elsewhere. Based on my experience, relying solely on dealership financing without external comparison often means missing out on potentially better rates.

2. Bank and Credit Union Loans:

Traditional banks and local credit unions are reliable sources for used car loans. They often offer competitive interest rates, especially if you have a strong credit history and an existing relationship with the institution. Credit unions, in particular, are known for their customer-centric approach and often provide excellent rates to their members.

Pros: Competitive interest rates, personalized service, clear terms and conditions. If you’re a long-standing customer, you might receive preferential treatment.

Cons: Application processes can sometimes be slower than online lenders. You may need to visit a branch, and approval can be stricter for those with less-than-perfect credit.

3. Online Lenders:

The digital age has brought forth a plethora of online lenders specializing in auto loans. These platforms offer a quick and streamlined application process, often providing instant pre-approvals. They can be particularly useful for comparing rates from multiple lenders without leaving your home.

Pros: Speed and convenience, easy rate comparison, often cater to a wider range of credit scores (including those with less-than-perfect credit). Many offer a fully online experience from application to funding.

Cons: Less personalized service, may require more self-diligence in comparing offers and understanding terms. Some lesser-known online lenders might have less transparent practices, so due diligence is crucial.

4. Personal Loans (Generally Not Ideal for Cars):

While a personal loan can provide funds for almost any purpose, it’s generally not the best choice when you need a used car loan. Personal loans are typically unsecured, meaning they don’t use the car as collateral. This higher risk for the lender usually translates into significantly higher interest rates compared to secured auto loans.

Pros: No collateral required, funds can be used for other expenses if needed.

Cons: Much higher interest rates, shorter repayment terms, leading to higher monthly payments. It’s almost always more expensive than a dedicated used car loan.

Key Factors Lenders Consider When You Need a Used Car Loan

When you approach a lender because you need a used car loan, they don’t just hand over money. They conduct a thorough assessment of your financial profile to determine your creditworthiness and the level of risk involved. Understanding these factors is crucial for preparing a strong application and improving your chances of approval.

1. Credit Score:

Your credit score is arguably the most critical factor lenders evaluate. It’s a three-digit number summarizing your credit history, including how reliably you’ve paid past debts. A higher score (generally 670 and above) indicates a lower risk to lenders, leading to better loan terms and lower interest rates.

Based on my experience, a strong credit score can save you thousands of dollars over the life of a loan. It gives you significant leverage during negotiations, allowing you to secure competitive annual percentage rates (APRs) and flexible repayment schedules. Conversely, a lower score might mean higher rates or a requirement for a larger down payment.

2. Income and Employment Stability:

Lenders want to be confident that you have a steady and sufficient income to comfortably make your monthly loan payments. They typically look for consistent employment history, often preferring at least two years in the same job or industry. Your gross monthly income will be a key figure in their assessment.

It’s not just about how much you earn, but also the reliability of that income. Self-employed individuals, for example, might need to provide more extensive documentation like tax returns to prove income stability. Lenders need assurance that your financial capacity is robust enough to handle the new debt.

3. Debt-to-Income Ratio (DTI):

Your DTI ratio is a crucial metric that shows how much of your gross monthly income goes towards debt payments. Lenders calculate this by adding up all your monthly debt obligations (mortgage/rent, credit card payments, student loans, existing car loans) and dividing it by your gross monthly income. A lower DTI (ideally below 36%) signals that you have enough disposable income to take on a new car payment.

Pro tips from us: Keep your DTI as low as possible before applying. If your DTI is high, consider paying down other debts first, even small ones. This demonstrates financial responsibility and frees up more of your income for the new car loan.

4. Down Payment:

A down payment is the initial amount of money you pay upfront towards the purchase price of the car. It directly reduces the amount you need to borrow, which can significantly impact your loan terms. A larger down payment means a smaller loan, less interest paid over time, and a lower monthly payment.

Furthermore, a substantial down payment signals to lenders that you are financially committed to the purchase and less likely to default. Common mistakes to avoid are underestimating the power of a good down payment; even 10-20% can make a huge difference in your loan approval and terms.

5. Vehicle Age and Mileage (Specific to Used Cars):

Unlike new cars, the age and mileage of a used vehicle play a significant role in its financing. Lenders often have stricter requirements for older vehicles or those with very high mileage. This is because older, higher-mileage cars are perceived as having a higher risk of mechanical issues, which could lead to a borrower defaulting if the car breaks down.

Some lenders might cap the maximum age or mileage they’ll finance, or they might offer higher interest rates for such vehicles. It’s important to research these limits if you’re looking at a much older or high-mileage car.

6. Loan Term:

The loan term refers to the length of time you have to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72 months). A longer loan term results in lower monthly payments but means you’ll pay more in total interest over the life of the loan. Conversely, a shorter term leads to higher monthly payments but less overall interest paid.

Lenders consider your preferred loan term in relation to your income and the car’s value. They want to ensure the payment is affordable for you, but also that the car’s value doesn’t depreciate faster than you’re paying it off, especially with longer terms.

Preparing for Your Used Car Loan Application: Your Pre-Approval Playbook

Success in securing a used car loan often hinges on thorough preparation. Before you even step foot on a dealership lot or browse online listings, taking a few proactive steps can significantly improve your chances of approval and help you secure the best possible terms. This is your pre-approval playbook.

1. Check Your Credit Score and Report (and Fix Errors):

This is your absolute first step. Obtain copies of your credit report from all three major credit bureaus (Equifax, Experian, TransUnion) and check your credit score. You can typically get one free report from each bureau annually via AnnualCreditReport.com.

Carefully review your reports for any inaccuracies or fraudulent activity. Errors, even small ones, can negatively impact your score. If you find discrepancies, dispute them immediately with the credit bureau; this can take time but is well worth the effort. Knowing your score upfront also helps you set realistic expectations for interest rates.

2. Determine Your Budget (Total Cost, Monthly Payment):

Before you fall in love with a car you can’t truly afford, establish a realistic budget. Consider not just the potential monthly loan payment, but also other car ownership costs: insurance, fuel, maintenance, and potential repairs for a used vehicle. A good rule of thumb is that your total car expenses (loan, insurance, fuel) shouldn’t exceed 10-15% of your net monthly income.

Use online loan calculators to estimate monthly payments based on different loan amounts, interest rates, and terms. This helps you understand what you can comfortably afford, preventing you from becoming "car poor."

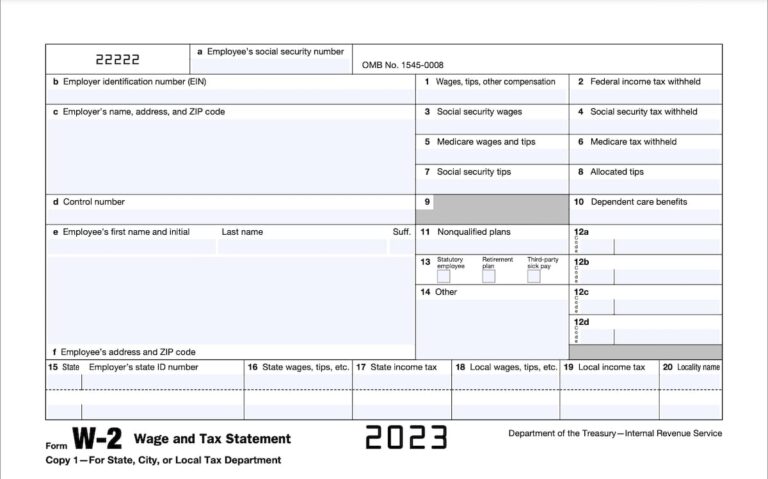

3. Gather Necessary Documents:

Lenders will require specific documents to verify your identity, income, and residence. Having these prepared in advance will streamline your application process. Common documents include:

- Proof of identity (Driver’s license, Social Security card)

- Proof of income (Recent pay stubs, W-2s, tax returns for self-employed)

- Proof of residence (Utility bill, lease agreement)

- Bank statements

- References (sometimes required)

4. Get Pre-Approved (The Importance of Pre-Approval):

Perhaps the most powerful tool in your pre-purchase arsenal is getting pre-approved for a loan. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate, pending a final vehicle selection. This is distinct from pre-qualification, which is a softer estimate.

Why is pre-approval so vital?

- Empowerment: You walk into the dealership knowing exactly how much you can spend, transforming you into a cash buyer. This removes the focus from the monthly payment and allows you to negotiate on the car’s price.

- Negotiating Power: Dealers are more likely to offer their best price when they know you already have financing secured.

- Budget Clarity: It firmly establishes your spending limit, preventing you from overextending yourself.

- Rate Comparison: You can compare the pre-approved rate from your bank/credit union with any financing offers from the dealership, ensuring you get the best deal.

Navigating the Application Process: Step-by-Step Guide

Once you’ve done your homework and prepared your documents, the actual application process for your used car loan becomes much smoother. Following these steps will help ensure a seamless experience and a successful outcome.

1. Research Lenders:

Don’t just go with the first lender you find. Research banks, credit unions, and reputable online lenders. Look at their advertised rates, customer reviews, and any special programs they might offer. Some lenders specialize in used car loans or offer better terms for certain credit profiles.

2. Compare Offers:

If you’ve received pre-approvals from multiple lenders, compare them side-by-side. Look beyond just the interest rate; consider the annual percentage rate (APR), which includes fees, the loan term, and any prepayment penalties. A difference of even a half-percentage point can save you hundreds over the life of the loan.

3. Submit Application:

Once you’ve chosen a lender, complete their full loan application. This will typically involve providing all the documents you’ve gathered and authorizing a hard credit inquiry. Be honest and thorough in your application; any discrepancies can delay or jeopardize your approval.

4. Review Loan Documents Carefully:

Before signing anything, meticulously review all loan documents. Understand the total loan amount, the interest rate (APR), the monthly payment, the loan term, and any fees (origination fees, late payment fees, prepayment penalties). If anything is unclear, ask questions until you fully understand every clause.

5. Finalize the Deal:

Once you’re satisfied with the loan terms and have chosen your used vehicle, the lender will disburse the funds directly to the dealership or to you, depending on the arrangement. At this point, you’ll sign the final paperwork and officially become the proud owner of your used car!

Common Challenges and How to Overcome Them

Life throws curveballs, and not everyone has a perfect financial history. If you need a used car loan but face certain challenges, don’t despair. There are often strategies and specialized lenders that can help you navigate these hurdles.

1. Bad Credit:

Having a low credit score (typically below 600-620) is a common challenge. While it can lead to higher interest rates, it doesn’t make a loan impossible.

- Strategies for Approval: Focus on making a larger down payment, which reduces the lender’s risk. Consider a shorter loan term to demonstrate your commitment to faster repayment.

- Subprime Lenders: These lenders specialize in working with borrowers with lower credit scores. While their rates will be higher, they can provide an opportunity to finance a vehicle and rebuild your credit.

- Improve Your Credit First: If possible, take some time to improve your credit score before applying. Pay down existing debts, make all payments on time, and dispute any errors on your credit report.

2. No Credit History:

If you’re young or new to the country, you might have no credit history at all. This is different from bad credit but still poses a challenge as lenders have no data to assess your risk.

- Co-signer: A co-signer with good credit can significantly improve your chances of approval. They agree to be equally responsible for the loan, providing the lender with added security.

- Secured Loans: Some lenders offer secured loans where the loan is tied to an asset (like a savings account). This is less common for auto loans but can be an option for building initial credit.

- Alternative Data: Some lenders are starting to look at alternative data, like utility payment history or rent payments, to assess creditworthiness. Inquire if your chosen lender considers these.

3. High Interest Rates:

If your initial loan offers come with high interest rates, don’t immediately give up on your car buying journey.

- Negotiation: Armed with pre-approval, you can try to negotiate with the dealership or other lenders for a better rate.

- Refinancing Later: A common strategy is to accept a higher interest rate initially to get the car, and then, after 6-12 months of on-time payments, refinance the loan for a lower rate. This demonstrates responsible payment behavior, which can improve your credit score and open doors to better offers.

4. Avoiding Scams and Predatory Lenders:

The auto loan market can, unfortunately, attract unscrupulous players. Be wary of lenders who guarantee approval regardless of credit, demand upfront fees, or pressure you into signing without reading documents.

- Red Flags: Unsolicited loan offers that seem too good to be true, requests for personal information over unsecured channels, or high-pressure sales tactics.

- Research: Always check lender reviews and their standing with the Better Business Bureau. Stick to established banks, credit unions, and well-reviewed online lenders.

Pro Tips for Securing the Best Used Car Loan

Beyond the basics, there are several strategic moves you can make to significantly improve your chances of securing the most favorable used car loan terms. These are insights gleaned from years of observing successful financing outcomes.

1. Increase Your Down Payment:

This cannot be emphasized enough. A larger down payment immediately reduces the loan amount, lowers your monthly payments, and decreases the total interest paid. It also makes you a more attractive borrower in the eyes of lenders, as it signals your financial commitment and reduces their risk. Aim for at least 10-20% if possible.

2. Improve Your Credit Score:

Even a small improvement in your credit score can unlock significantly better interest rates. Before you apply, take steps to pay down credit card balances, make all payments on time, and resolve any collection accounts. Even a 30-point increase can move you into a different tier of interest rates.

3. Shorten Your Loan Term (If Affordable):

While a longer loan term means lower monthly payments, it dramatically increases the total interest you’ll pay over time. If your budget allows, opt for the shortest loan term you can comfortably afford (e.g., 36 or 48 months instead of 60 or 72). You’ll pay off the car faster and save a substantial amount in interest.

4. Negotiate the Car Price, Not Just the Loan:

Remember, the loan is for the price of the car. By negotiating a lower purchase price for the used vehicle, you automatically reduce the amount you need to borrow, which directly impacts your loan. Focus on getting the best "out-the-door" price for the car before discussing financing options in detail.

5. Consider Refinancing Down the Line:

If you couldn’t secure the absolute best interest rate initially, perhaps due to a lower credit score or market conditions, don’t worry. After 6-12 months of consistent, on-time payments, your credit score will likely improve. At that point, you can explore refinancing your used car loan to a lower interest rate, saving you money for the remainder of the loan term.

6. Don’t Settle for the First Offer:

Always compare multiple loan offers. Whether it’s from different banks, credit unions, or the dealership itself, having options empowers you. Use competing offers as leverage to negotiate for even better terms. This competitive environment works in your favor.

Common Mistakes to Avoid When You Need a Used Car Loan

Even with the best intentions, borrowers often make common missteps that can cost them money or complicate their loan journey. Being aware of these pitfalls can help you avoid them and ensure a smoother, more cost-effective experience when you need a used car loan.

1. Not Checking Your Credit:

As discussed, your credit score is paramount. Failing to check it beforehand means you’re going into the process blind, unaware of potential issues or your likely interest rate. This lack of knowledge puts you at a disadvantage during negotiations.

2. Skipping Pre-Approval:

Walking into a dealership without a pre-approval is like going grocery shopping without a list or budget. You’re more susceptible to impulse decisions and less likely to get the best deal. Pre-approval gives you financial clarity and negotiating power.

3. Focusing Only on the Monthly Payment:

It’s easy to get caught up in the allure of a low monthly payment. However, a low payment often comes with a longer loan term and a significantly higher total interest paid. Always consider the total cost of the loan over its entire duration, not just the monthly installment.

4. Buying More Car Than You Can Afford:

The temptation to stretch your budget for a slightly better car is strong. However, overextending yourself financially can lead to payment struggles, stress, and even repossession. Stick to your pre-determined budget, even if it means compromising on a few features.

5. Not Reading the Fine Print:

Loan documents can be lengthy and filled with legal jargon, but every word matters. Failing to read and understand the entire agreement can lead to unwelcome surprises, such as hidden fees, prepayment penalties, or unfavorable clauses. Always ask for clarification if something is unclear.

6. Letting the Dealer Run Too Many Credit Checks:

When you apply for financing at a dealership, they might submit your application to multiple lenders. Each "hard inquiry" can slightly ding your credit score. While credit bureaus generally group multiple auto loan inquiries within a short period (usually 14-45 days) as a single inquiry, it’s still wise to limit them. If you’re pre-approved, you only need the dealer to run your credit once for their own offer.

The Road Ahead: Responsible Loan Management

Securing your used car loan is a significant achievement, but it’s just the beginning of your journey. Responsible loan management is crucial for protecting your financial health and ensuring your new-to-you vehicle serves you well for years to come.

1. Making Payments on Time:

This is the golden rule of credit and loan management. Every single on-time payment reinforces your credit score, builds a positive payment history, and keeps you out of late fee trouble. Set up automatic payments or calendar reminders to ensure you never miss a due date.

2. Budgeting for Maintenance, Insurance, and Fuel:

Beyond your loan payment, remember to budget for the ongoing costs of car ownership. Used cars, especially older ones, might require more frequent maintenance. Factor in the cost of insurance, which can vary based on the car’s age, your driving record, and your location. Fuel costs are also a significant, recurring expense.

3. Understanding Early Payoff Options:

If your financial situation improves, you might consider paying off your loan early. Check your loan agreement for any prepayment penalties. Many auto loans do not have them, allowing you to save on future interest by making extra payments or paying off the balance completely. This can free up cash flow and reduce your overall debt burden sooner.

Conclusion: Your Journey to a Used Car Loan Starts Now

Navigating the process of securing a used car loan doesn’t have to be a source of stress. By understanding your options, preparing diligently, and approaching the application with confidence and knowledge, you can secure favorable terms that fit your budget. Remember, a used car offers incredible value, and with the right financing, it can be a smart, long-term investment.

Whether you’re improving your credit, saving for a down payment, or comparing lender offers, every step you take brings you closer to driving away in your ideal pre-owned vehicle. Don’t let the need for a used car loan intimidate you; instead, use this guide as your roadmap to a successful and financially savvy car purchase. Your journey to owning a reliable used car, backed by a smart loan, starts today!