New Graduate Car Loans: The Ultimate Guide for Recent Grads to Drive Smart

New Graduate Car Loans: The Ultimate Guide for Recent Grads to Drive Smart Carloan.Guidemechanic.com

Congratulations, recent graduate! You’ve navigated countless exams, celebrated a hard-earned diploma, and are now ready to embark on your professional journey. For many, this exciting new chapter also brings the practical need for reliable transportation. Whether it’s commuting to your first job, visiting family, or simply enjoying the freedom of the open road, getting a car is often a top priority.

However, the path to securing a car loan as a new graduate can feel like another challenging assignment. Lenders often look for established credit history, a significant down payment, and stable employment – things many recent grads are still building. This comprehensive guide is designed to demystify the process of new graduate car loans, providing you with the knowledge and strategies to drive off the lot with confidence and a smart financial decision.

New Graduate Car Loans: The Ultimate Guide for Recent Grads to Drive Smart

We’ll dive deep into understanding your unique financial position, exploring your best loan options, and offering expert tips to secure favorable terms. Our ultimate goal is to empower you to make an informed choice that sets you up for financial success, not stress.

Why Getting a Car Loan as a New Grad is Unique

Securing an auto loan is a significant financial step for anyone, but recent graduates often face a particular set of circumstances that make their application distinct. Understanding these challenges is the first step toward overcoming them.

The "No Credit" or "Thin Credit" Dilemma

One of the most common hurdles for new graduates is the lack of a substantial credit history. Lenders rely heavily on your credit report and score to assess your trustworthiness and ability to repay debt. If you’ve only recently started building credit, or haven’t had any credit accounts in your name, you might be categorized as having "thin credit."

Based on my experience, a thin credit file means lenders have less data to evaluate your risk profile. This can lead to higher interest rates or even outright rejection for conventional loans. It’s not a reflection of your character, but simply a lack of a track record in the financial world. Many new grads haven’t had the need for credit cards or personal loans during their studies, leaving them in this challenging position.

Student Loan Debt Impact

For many, graduation comes hand-in-hand with student loan debt. While student loans are generally considered "good debt" because they’re an investment in your future, their presence on your credit report can affect your debt-to-income (DTI) ratio. Lenders calculate DTI to understand how much of your monthly income is already committed to debt payments.

A high DTI might signal to a lender that adding another monthly car payment could stretch your finances too thin. It’s crucial to demonstrate that you can comfortably manage both your student loan obligations and a new car payment. This doesn’t mean student loan debt prevents you from getting a car loan, but it does mean you need to be strategic in how you present your overall financial picture.

Income Stability vs. Job History

Lenders also want to see stable employment and a reliable income source. While you might have a fantastic new job offer in hand, a short employment history can sometimes be a red flag. They prefer to see a consistent income stream over several months or even years.

Pro tips from us: If you’ve just started a new job, having a signed offer letter, recent pay stubs, and even a letter from your employer verifying your employment and salary can be immensely helpful. This provides concrete evidence of your income stability, even if you haven’t been on the job for long. It bridges the gap between a promising future and a limited past.

Building Your Foundation for a Successful Car Loan Application

Before you even start browsing cars, it’s essential to lay a strong financial foundation. This preparation will significantly improve your chances of approval and help you secure better loan terms.

Credit Score: Your Financial Footprint

Your credit score is a three-digit number that summarizes your creditworthiness. While you might be starting with a blank slate, there are proactive steps you can take to build it quickly and responsibly.

- Understanding Credit Reports: Your credit report details your borrowing history, including credit cards, student loans, and any other lines of credit. It’s where lenders get the information to calculate your score. You are entitled to a free copy of your credit report from each of the three major bureaus (Equifax, Experian, TransUnion) once every 12 months via AnnualCreditReport.com. Review it for accuracy and dispute any errors immediately.

- How to Start Building Credit:

- Secured Credit Cards: These cards require a cash deposit, which acts as your credit limit. They are an excellent way to demonstrate responsible credit use.

- Become an Authorized User: If a trusted family member with excellent credit adds you as an authorized user on their credit card, their positive payment history can reflect on your credit report. Just ensure they are truly responsible.

- Small Installment Loans: Sometimes, a small personal loan (even for a few hundred dollars) that you pay back diligently can help establish a payment history.

- Credit-Builder Loans: Some credit unions offer these specific loans designed to help you build credit. The money is held in an account while you make payments, and you receive it once the loan is paid off.

Common mistakes to avoid are applying for too much credit at once, missing payments, or maxing out your credit cards. These actions can severely damage your nascent credit score.

Down Payment: The Power of Upfront Cash

A down payment is the initial amount of money you pay upfront for the car, reducing the total amount you need to borrow. For new graduates, a significant down payment can be a game-changer.

- Why it’s crucial for new grads: With a thin credit history, a larger down payment signals to lenders that you are serious about your purchase and have a lower risk of defaulting. It reduces the lender’s risk exposure because they have less money invested in the loan. It also means you’ll borrow less, leading to lower monthly payments and less interest paid over the life of the loan.

- How much to save: While there’s no magic number, aiming for at least 10-20% of the car’s purchase price is a strong recommendation. For a used car, 10% might be sufficient. For a new car, 20% is often ideal. If you can save more, even better! Every dollar you put down is a dollar you don’t borrow. This strategy significantly improves your chances of approval and helps you secure a more favorable interest rate.

Budgeting: Knowing What You Can Truly Afford

Buying a car involves more than just the monthly loan payment. Many first-time buyers underestimate the full cost of car ownership.

- The 20/4/10 Rule (or similar): A good guideline for car financing is to aim for a 20% down payment, a loan term no longer than four years (48 months), and car expenses (loan payment, insurance, fuel, maintenance) not exceeding 10% of your gross monthly income. This rule helps ensure you don’t overextend yourself.

- Hidden costs of car ownership:

- Insurance: Especially for young drivers, insurance premiums can be very high. Get quotes before you buy.

- Fuel: Factor in your daily commute and weekend trips.

- Maintenance: Regular oil changes, tire rotations, and unexpected repairs.

- Registration & Taxes: Annual fees vary by state.

- Parking: If you live in an urban area, this can be a significant expense.

Based on my experience, many new grads focus solely on the monthly payment. However, it’s the total cost of ownership that truly impacts your budget. Create a detailed budget that includes all these expenses to understand your true affordability.

Exploring Your Car Loan Options as a New Graduate

Once your financial foundation is solid, it’s time to explore the various avenues available for new graduate car loans. Each option has its own set of advantages and considerations.

Traditional Bank Loans & Credit Unions

These institutions are often excellent starting points for car loan applications.

- Banks: Large banks offer competitive rates and a variety of loan products. They generally have more stringent credit requirements, but if you have an existing relationship with a bank (checking/savings account), they might be more inclined to work with you.

- Credit Unions: Credit unions are non-profit organizations owned by their members. They are renowned for offering lower interest rates and more flexible terms than traditional banks, especially for members. They often have a more personalized approach and might be more understanding of a new grad’s unique financial situation.

- Pro tip: Check if your university or employer has a partnership with a credit union, or if you meet the eligibility criteria for a local one. Joining a credit union can unlock access to excellent loan products.

Dealership Financing

Most car dealerships offer in-house financing or work with a network of lenders. This option offers convenience, as you can apply for a loan and purchase the car all in one place.

- Convenience, but caution needed: While convenient, dealership financing might not always offer the best rates, especially if you haven’t secured pre-approval elsewhere. Dealers make money on financing, so they might mark up interest rates.

- Common mistakes to avoid: Don’t let the excitement of a new car rush you into signing a loan agreement without fully understanding the terms. Always compare their offer with any pre-approvals you’ve received.

Special Programs for New Grads

Many car manufacturers and some lenders recognize the potential of recent graduates and offer specific programs designed to help them. These programs often come with relaxed credit requirements or special incentives.

- Manufacturer Incentives: Brands like Toyota, Honda, Ford, and GM often have "college graduate programs" that offer rebates, low APR financing, or deferred payments for eligible graduates. These typically require proof of graduation within a certain timeframe (e.g., last two years) and proof of employment.

- Requirements: You’ll generally need your diploma or transcripts, proof of current employment or a job offer, and sometimes a minimum credit score (though often lower than standard loans). These programs can be an excellent way to secure a competitive rate despite a limited credit history.

The Co-Signer Route

If you’re struggling to get approved on your own or are offered a very high interest rate, a co-signer can be a viable option.

- When it’s a good idea: A co-signer is someone with good credit who agrees to take on legal responsibility for the loan if you fail to make payments. This significantly reduces the lender’s risk. It can help you get approved and secure a lower interest rate.

- Responsibilities: Both you and your co-signer are equally responsible for the debt. If you miss payments, it negatively impacts both your credit scores.

- Pro tips from us: Choose a co-signer (usually a parent or close relative) whom you trust implicitly and who understands the full implications of their commitment. Have an open conversation about repayment expectations and potential challenges. This is a serious financial commitment for both parties.

The Application Process: What Lenders Look For

Navigating the application process for new graduate car loans can feel daunting, but being prepared with the right documents and understanding lender expectations will streamline the experience.

Required Documents

Having all your paperwork in order before you apply will make the process much smoother. Lenders need to verify your identity, income, and financial stability.

- Proof of Identity: Driver’s license, passport, or state ID.

- Proof of Income: Recent pay stubs (typically 2-3 months), offer letter if you’ve just started a new job, bank statements showing direct deposits.

- Proof of Employment: A letter from your employer verifying your position, salary, and start date can be very helpful, especially for new hires.

- Proof of Residence: Utility bill, lease agreement, or mortgage statement with your current address.

- Credit History: While they’ll pull your report, having a general understanding of your score and any accounts will help.

- Down Payment Documentation: Proof of funds for your down payment (e.g., bank statement).

Understanding Interest Rates

The Annual Percentage Rate (APR) is the true cost of borrowing, including the interest rate and any other fees. A lower APR means less money paid over the life of the loan.

- Factors Influencing APR:

- Credit Score: Higher scores typically get lower rates.

- Loan Term: Shorter terms usually have lower rates but higher monthly payments.

- Down Payment: A larger down payment can lead to a lower rate.

- Car Type: New cars often have lower rates than used cars due to perceived risk.

- Market Conditions: Overall economic factors influence rates.

Based on my experience, even a difference of one or two percentage points in APR can save you hundreds, if not thousands, of dollars over the life of a car loan. Always compare offers from multiple lenders.

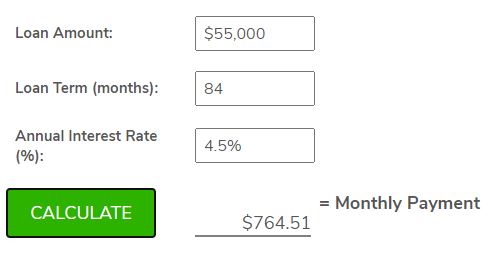

Loan Term and Monthly Payments: Finding the Right Balance

The loan term is the length of time you have to repay the loan, expressed in months (e.g., 36, 48, 60, 72 months).

- Shorter Term: Higher monthly payments, but you pay less interest overall and own the car sooner. This is generally recommended.

- Longer Term: Lower monthly payments, but you pay more interest overall, and you might owe more than the car is worth (negative equity) for a longer period.

- Common mistakes to avoid: While a longer term might make the car seem more affordable monthly, it significantly increases the total cost of the loan. Aim for the shortest term you can comfortably afford without straining your budget.

Pre-Approval vs. Application

- Pre-Approval: This is when a lender reviews your financial information and tentatively agrees to lend you a certain amount at a specific interest rate before you’ve even chosen a car.

- Advantages:

- Gives you a clear budget, so you know what you can afford.

- Empowers you to negotiate with dealerships, as you already have financing secured.

- Reduces stress at the dealership, allowing you to focus on the car, not the loan.

- Can act as leverage to get the dealership to beat your pre-approved rate.

- Advantages:

- Application: This is the formal request for a loan once you’ve selected a specific vehicle.

Pro tips from us: Always get pre-approved by at least one outside lender (bank or credit union) before stepping foot on a dealership lot. This gives you a baseline for comparison and strengthens your negotiating position.

Pro Tips for New Grads Navigating the Car Market

Securing new graduate car loans is one part of the equation; making a smart car purchase is another. Here are some expert tips to guide you through the process.

Research, Research, Research (Cars and Loans)

Knowledge is power when buying a car. Don’t rush into a purchase.

- Car Research: Determine your needs (commute, cargo space, fuel efficiency), research different makes and models, read reviews, and compare prices. Websites like Kelley Blue Book (KBB.com) and Edmunds.com are invaluable resources for car values and reviews.

- Loan Research: As discussed, shop around for loan offers from multiple banks and credit unions. Compare APRs, terms, and any fees. This due diligence can save you thousands.

Negotiating the Price

Many new buyers are intimidated by negotiation, but it’s a standard part of the car buying process.

- Focus on the Out-the-Door Price: Don’t just negotiate the monthly payment. Focus on the total purchase price of the car, including all taxes, fees, and add-ons.

- Be Prepared to Walk Away: If you’re not getting a fair deal, be ready to leave. There are always other cars and other dealerships.

- Separate Car Price from Loan Terms: Ideally, negotiate the car price first, then discuss financing. Don’t let them combine the two in a confusing way.

Beware of Add-ons

Dealerships often try to sell you additional products and services at the time of purchase, such as extended warranties, paint protection, or VIN etching.

- Scrutinize Every Add-on: While some might have value, many are overpriced and can be purchased cheaper elsewhere (or are simply unnecessary).

- Understand What You’re Buying: Don’t feel pressured. Ask for clear explanations and pricing for each add-on. Remember, these increase your total loan amount and therefore your monthly payment and total interest paid.

Understanding Car Insurance (Crucial for Young Drivers)

Car insurance is a mandatory expense, and for young, inexperienced drivers, it can be shockingly high.

- Get Quotes Before You Buy: Before finalizing your car purchase, get insurance quotes for the specific make and model you’re considering. This will give you a realistic picture of the total monthly cost of ownership.

- Factors Affecting Premiums: Your age, driving record, location, car type, and even your credit score can influence your insurance rates.

- Consider a Higher Deductible: To lower monthly premiums, you might opt for a higher deductible, but ensure you have an emergency fund to cover that amount if you need to file a claim.

– This hypothetical article on our blog would provide more detailed information on navigating insurance as a new driver.

Common Mistakes to Avoid

- Buying More Car Than You Can Afford: It’s easy to get excited, but stick to your budget. A flashy car isn’t worth financial strain.

- Focusing Only on Monthly Payments: As mentioned, look at the total cost, including interest, insurance, and maintenance.

- Not Getting Pre-Approved: This leaves you at the mercy of the dealership’s financing offers.

- Ignoring the Total Cost of Ownership: Beyond the loan, remember fuel, maintenance, and insurance.

- Skipping the Test Drive and Pre-Purchase Inspection: Always test drive thoroughly. For a used car, a mechanic’s inspection (even if it costs a bit) can save you from costly repairs down the road.

After Approval: Managing Your Car Loan Responsibly

Getting approved for new graduate car loans is a significant achievement, but the journey doesn’t end there. Responsible loan management is key to building excellent credit and securing your financial future.

Making Payments On Time

This is the most critical aspect of managing any loan.

- Impact on Credit Score: Your payment history is the single largest factor in your credit score calculation. Late payments can severely damage your credit, making it harder to get future loans or credit cards.

- Set Up Auto-Pay: To avoid missing a payment, set up automatic payments from your checking account. This ensures consistency and peace of mind.

- Payment Reminders: If auto-pay isn’t an option, use calendar reminders or apps to ensure you pay on time, every time.

The Benefits of Early Repayment

While not always feasible, paying off your loan faster than scheduled can offer significant advantages.

- Save on Interest: Because interest accrues on the outstanding principal balance, every extra dollar you pay reduces that balance, leading to less interest paid over the loan’s life.

- Build Equity Faster: You’ll own the car outright sooner, freeing up your monthly budget for other financial goals.

- Boost Credit Score: Demonstrating accelerated debt repayment can look very favorable on your credit report.

- Pro tips from us: Even small extra payments, like rounding up your monthly payment or applying tax refunds, can make a big difference over time. Just ensure your loan doesn’t have prepayment penalties (most auto loans do not, but always check).

Considering Refinancing Down the Road

As your financial situation improves and your credit score strengthens, refinancing your car loan might become an attractive option.

- When to Consider It:

- Improved Credit Score: If you’ve been diligently making payments and building your credit, you might qualify for a lower interest rate.

- Lower Interest Rates: If market interest rates have dropped since you took out your original loan.

- Change in Financial Situation: If you need to lower your monthly payments (though this often means extending the loan term and paying more interest overall).

- Benefits: Refinancing can lead to lower monthly payments, a reduced interest rate, and ultimately, significant savings over the life of the loan. It’s a great way to optimize your initial loan once you’ve established a solid credit history.

Building Future Credit

Your car loan is an excellent tool for building a robust credit profile.

- Positive Impact: Consistent, on-time payments on an installment loan demonstrate financial responsibility to future lenders.

- Diversify Credit Mix: A car loan adds to your credit mix (along with credit cards), which is another factor in your credit score.

- Long-Term Benefits: A strong credit history will make it easier to secure mortgages, personal loans, or even better rates on future car loans.

– For new graduates managing student loan debt alongside a new car loan, understanding all their federal student aid options and repayment plans is crucial.

Conclusion: Drive Smart, Plan Ahead

Navigating the world of new graduate car loans might seem complex, but with the right knowledge and a strategic approach, it’s an entirely achievable goal. You’ve worked hard for your degree, and you deserve reliable transportation that supports your new professional life without burdening your financial future.

Remember, the key is preparation: build your credit, save for a substantial down payment, and understand your budget comprehensively. Explore all your options, from credit unions to special grad programs, and don’t shy away from seeking a co-signer if it helps secure better terms. Always get pre-approved, negotiate wisely, and be vigilant about extra costs.

Your first car loan is more than just a means to get around; it’s an opportunity to establish a strong financial foundation. By making smart choices now, you’ll not only drive away in a car you love but also build a credit history that will serve you well for years to come. Drive smart, plan ahead, and enjoy the journey!