Ok Credit Car Loans: Navigating the Future of Car Ownership with Digital Financing

Ok Credit Car Loans: Navigating the Future of Car Ownership with Digital Financing Carloan.Guidemechanic.com

The dream of owning a car is a powerful one, representing freedom, convenience, and a significant personal milestone. For many, this dream often involves securing a car loan, a financial bridge that makes vehicle ownership accessible. In an increasingly digital world, the way we approach financing is evolving rapidly. Gone are the days of endless paperwork and multiple bank visits; today, the emphasis is on speed, convenience, and transparency, much like the efficiency seen in digital platforms.

When we talk about "Ok Credit Car Loans," we’re often thinking about the convenience and digital-first approach that modern platforms bring to financial transactions. While Ok Credit is primarily known as a leading digital ledger and bookkeeping app for small businesses, simplifying their financial records, the phrase itself has come to symbolize the broader shift towards accessible, streamlined digital finance. This article will delve deep into the world of car loans, exploring how modern digital principles – akin to the ease Ok Credit offers its users – are reshaping the landscape of car financing, making it simpler, faster, and more transparent for everyone. We aim to equip you with the knowledge to navigate this exciting new era of car ownership.

Ok Credit Car Loans: Navigating the Future of Car Ownership with Digital Financing

Understanding the Modern Car Loan Landscape: The Digital Revolution

The financial sector has undergone a profound transformation, with digital platforms leading the charge. This revolution is not just about online banking; it’s about reimagining how credit is accessed, approved, and managed. For car loans, this means moving away from traditional, often cumbersome processes towards a more agile, user-friendly experience.

Traditional vs. Digital Lending: A Paradigm Shift

Historically, securing a car loan involved a lengthy process. You’d visit multiple banks or dealerships, fill out extensive paper forms, and wait days, sometimes weeks, for approval. This traditional model, while still available, is gradually being overshadowed by digital alternatives. Digital lending leverages technology to streamline every step, from application to disbursement.

Based on my experience in the financial content space, the biggest advantage of this shift is speed. What once took days can now often be completed in hours, or even minutes, for pre-approvals. This rapid turnaround is invaluable in a fast-paced market where desirable vehicles can sell quickly.

How Digital Platforms are Changing Access to Credit

Digital platforms have democratized access to credit. By using sophisticated algorithms and data analytics, lenders can assess creditworthiness more efficiently, often reaching a broader demographic. This means that individuals who might have found traditional channels challenging now have more avenues to explore.

The convenience factor cannot be overstated. Applying for a car loan from the comfort of your home, at any time of day, has become the new norm. This flexibility empowers borrowers to make informed decisions without feeling rushed or pressured.

The "Ok Credit" Philosophy Applied to Car Loans: Speed, Simplicity, Accessibility

While Ok Credit primarily serves businesses with its digital ledger, the spirit of what it offers – simplicity, speed, and accessibility in managing finances – is precisely what modern car loan seekers are looking for. Imagine applying for a car loan with the same ease you might track your daily business transactions on an app. This vision drives the evolution of car financing.

The goal is to make the entire car loan journey as seamless as possible. This includes clear communication, minimal documentation, and quick processing times. By embracing these principles, lenders are making car ownership more attainable for a wider audience, aligning with the "Ok Credit" ideal of straightforward financial management.

Who is Eligible? Decoding Car Loan Eligibility Criteria

Before you even start dreaming about your new wheels, understanding the eligibility criteria for a car loan is paramount. Lenders use specific metrics to assess your ability to repay the loan, ensuring a responsible lending process. Meeting these requirements is the first step towards securing your car.

Key Eligibility Factors: Age, Income, and Credit Score

Age: Most lenders require applicants to be between 18 or 21 years and 60 or 65 years of age at the time of loan maturity. This ensures that the borrower has a stable working life to repay the debt. Specific age limits can vary slightly between different financial institutions.

Income: Your income is a crucial indicator of your repayment capacity. Lenders will typically have a minimum monthly or annual income requirement. This threshold ensures that your disposable income is sufficient to cover the monthly equated monthly installment (EMI) without undue financial strain. Both salaried and self-employed individuals have different income proof requirements.

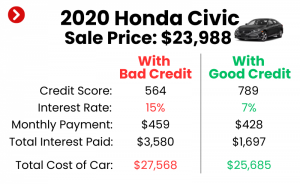

Credit Score (CRB/CIBIL): This is arguably the most critical factor. Your credit score is a numerical representation of your creditworthiness, based on your past borrowing and repayment history. A higher score (generally 750+) indicates responsible financial behavior and significantly increases your chances of approval, often at more favorable interest rates. A low score can lead to rejection or higher interest rates.

Employment Status: Salaried vs. Self-Employed

Salaried Individuals: If you are a salaried employee, lenders will look for stability in your employment. This typically means having a minimum work experience, often one to two years, with your current employer. Your salary slips, bank statements showing salary credits, and employment verification letters will be key documents.

Self-Employed Individuals: For self-employed applicants, the focus shifts to business stability and income consistency. Lenders will require proof of business existence (e.g., business registration), income tax returns (ITR) for the past few years, and bank statements reflecting business transactions. The length of time your business has been operational is also a significant factor, usually requiring a minimum of two to three years.

Debt-to-Income Ratio: Balancing Your Finances

Your debt-to-income (DTI) ratio is another important metric. This ratio compares your total monthly debt payments (including the proposed car loan EMI) to your gross monthly income. Lenders prefer a lower DTI ratio, as it indicates you have enough income left after paying existing debts to comfortably manage new loan obligations. A high DTI might signal potential repayment difficulties.

Pro Tip from Us: Before even applying for a car loan, take proactive steps to improve your eligibility. Pay off smaller debts, avoid new credit applications, and check your credit score regularly for any discrepancies. A little preparation goes a long way in securing better loan terms.

Types of Car Loans: Finding Your Perfect Match

The world of car loans isn’t one-size-fits-all. Different types of vehicles and financial situations call for different loan products. Understanding these distinctions is key to choosing the option that best suits your needs and budget.

New Car Loans: Driving Off the Lot with Confidence

New car loans are designed specifically for purchasing brand-new vehicles directly from a dealership. These loans typically come with more attractive interest rates and longer repayment tenures compared to used car loans. This is because new cars are considered less risky collateral due to their higher initial value and warranty coverage.

When opting for a new car loan, you often have a wide array of choices from various banks and financial institutions, along with financing options provided directly by car manufacturers. It’s crucial to compare these offers diligently to secure the most competitive rates and flexible terms.

Used Car Loans: Smart Financing for Pre-Owned Vehicles

Used car loans are for purchasing pre-owned vehicles. While they offer the advantage of a lower purchase price for the car itself, the loan terms might be slightly different. Interest rates for used car loans are generally a bit higher than new car loans, and the maximum loan tenure might be shorter. This reflects the higher depreciation rate and potential maintenance costs associated with older vehicles.

However, used car loans present an excellent opportunity for budget-conscious buyers or those looking for a specific model at a more affordable price point. When applying for a used car loan, the age and condition of the vehicle will significantly influence the loan amount and terms offered by the lender.

Refinancing Car Loans: Optimizing Your Existing Debt

Car loan refinancing involves taking out a new loan to pay off your existing car loan. This strategy is often employed to secure a lower interest rate, reduce monthly payments, or change the loan tenure. It can be particularly beneficial if your credit score has improved significantly since you first took out the loan, or if market interest rates have dropped.

Refinancing can save you a substantial amount over the life of the loan. It’s a smart financial move for those looking to optimize their current debt obligations and improve their cash flow. Always calculate the potential savings against any processing fees for the new loan.

Secured vs. Unsecured Loans: Understanding the Collateral

Most car loans fall under the category of secured loans. This means the car itself acts as collateral for the loan. In simpler terms, if you fail to make your payments, the lender has the right to repossess the vehicle to recover their losses. This security allows lenders to offer lower interest rates because their risk is mitigated.

Unsecured loans, on the other hand, are not backed by any collateral. While personal loans can be unsecured and used for various purposes, including buying a car, they typically come with much higher interest rates due to the increased risk for the lender. For car financing, secured loans are the standard and generally more economical option.

Loans for Electric Vehicles (EVs): A Modern Touch

As the automotive industry shifts towards sustainability, specific loan products for Electric Vehicles (EVs) are becoming increasingly common. Many banks and financial institutions now offer "Green Car Loans" or "EV Loans" that often come with preferential interest rates or unique benefits. These incentives are designed to encourage the adoption of environmentally friendly transportation.

These specialized loans recognize the government push for EVs and the potential long-term savings in fuel and maintenance costs for the borrower. If you’re considering an EV, make sure to inquire about these tailored financing options, as they could offer a significant advantage.

The Application Process: A Step-by-Step Digital Journey

The days of cumbersome, paper-heavy loan applications are swiftly becoming a relic of the past. Today, securing a car loan, much like the streamlined processes on platforms like Ok Credit, is increasingly digital. This shift offers unparalleled convenience, allowing you to navigate your car ownership journey with greater ease and speed.

1. Researching Lenders & Rates: Your First Digital Dive

The initial step in your car loan journey is thorough research. Don’t settle for the first offer you receive. Use online comparison portals, visit bank websites, and check out financial aggregators to compare interest rates, processing fees, and loan terms from various lenders. This digital reconnaissance empowers you to find the most competitive deal tailored to your financial profile.

Based on my experience, taking the time to compare can save you thousands over the life of the loan. Even a small difference in the interest rate can have a significant impact on your total repayment amount.

2. Pre-approval: The Digital Advantage

Many lenders now offer a pre-approval process, which is a fantastic digital advantage. You can often get an initial approval based on basic information without a hard credit check. This gives you a clear idea of how much you can borrow and at what potential interest rate, all before you even step into a dealership.

A pre-approved loan acts as a strong negotiation tool at the dealership, as it shows you are a serious buyer with confirmed financing. It also simplifies your car shopping, allowing you to focus on vehicles within your budget.

3. Document Preparation: Your Digital Checklist

Even in a digital world, documents are essential. The good news is that most can now be submitted digitally. Prepare scanned copies or high-quality photographs of all necessary documents. This includes:

- Proof of Identity (PAN card, Aadhaar card, Passport, Driving License)

- Proof of Address (Utility bills, Bank statements, Rent agreement)

- Proof of Income (Salary slips for last 3-6 months, Bank statements for last 6-12 months, Latest ITR for self-employed)

- Vehicle-related documents (Proforma invoice from dealer, registration certificate if used car)

Common Mistake to Avoid: Incomplete or unclear documentation is a primary reason for application delays. Double-check that all required documents are clear, legible, and up-to-date before submission.

4. Online Application Submission: A Few Clicks Away

Once you’ve chosen a lender and gathered your documents, the application process is often entirely online. You’ll fill out a digital form with your personal, financial, and employment details, then upload your prepared documents. Many platforms also offer live chat support if you encounter any issues during this stage.

The convenience of applying from anywhere, at any time, truly embodies the "Ok Credit" philosophy of accessible digital solutions. It removes geographical barriers and rigid operating hours.

5. Verification & Approval: The Digital Review

After submission, the lender’s team will review your application and documents. This stage involves verifying your information, conducting a credit check (this is usually when a hard inquiry occurs), and assessing your repayment capacity. Thanks to advanced algorithms, this process is often much quicker than traditional methods.

You might receive calls from the lender for additional verification or clarification. Be prompt and accurate in your responses to ensure a smooth process.

6. Disbursement: The Final Step Towards Ownership

Upon approval, the loan amount will be disbursed. Typically, the funds are transferred directly to the car dealership or, in some cases, to your bank account if you are purchasing a used car from a private seller. The lender will then finalize the hypothecation of the vehicle in their favor.

Congratulations! You’re now ready to drive home your new car. The digital journey has successfully concluded, turning your car ownership dream into a reality.

Key Factors Affecting Your Car Loan Approval & Interest Rates

Securing a car loan isn’t just about meeting basic eligibility; several crucial factors significantly influence whether your application gets approved and, more importantly, the interest rate you’ll pay. Understanding these elements can empower you to strengthen your position as a borrower.

Credit Score: The Ultimate Game-Changer

As mentioned earlier, your credit score is paramount. It’s a three-digit number that tells lenders how responsibly you’ve handled credit in the past. A high score (typically 750 or above) signals low risk, making you a desirable borrower. Lenders are more likely to approve your loan and offer you the most competitive interest rates.

Conversely, a low credit score indicates a higher risk. This can lead to loan rejection, or if approved, significantly higher interest rates to compensate the lender for the perceived risk. Based on my observations, consistently paying bills on time and managing existing credit wisely are the best ways to build and maintain a strong credit score.

Down Payment: How It Impacts EMI and Interest

The down payment is the initial amount of money you pay upfront for the car. A larger down payment reduces the total amount you need to borrow. This has several advantages:

- Lower EMI: A smaller loan amount means lower monthly installments, making your budget more manageable.

- Reduced Interest Burden: You pay interest only on the borrowed amount, so a smaller loan translates to less interest paid over the loan tenure.

- Improved Approval Chances: A substantial down payment shows the lender your financial commitment and reduces their risk, potentially improving your chances of approval.

Pro tips from us suggest aiming for at least 15-20% of the car’s value as a down payment if possible.

Loan Tenure: Short vs. Long

Loan tenure refers to the period over which you repay the loan.

- Shorter Tenure: Means higher EMIs but less total interest paid over time. You become debt-free quicker.

- Longer Tenure: Means lower EMIs, making monthly payments more affordable. However, you’ll end up paying more in total interest over the longer period.

It’s a balancing act between affordability and the total cost of the loan. Carefully consider your budget and future financial goals when choosing a tenure.

Relationship with the Lender: A Hidden Advantage

If you have a long-standing relationship with a particular bank – perhaps your salary account is there, or you have other loans/investments with them – they might offer you preferential rates or faster processing. They already have a history with you, which can streamline the credit assessment process.

While not always a guarantee, it’s always worth checking with your existing bank first, as they might have special offers for loyal customers.

Vehicle Type and Value: Collateral Assessment

The type of vehicle you intend to purchase also plays a role. Lenders assess the market value and resale value of the car, especially for used car loans. High-demand models with good resale value are often viewed more favorably.

For new cars, the proforma invoice from the dealer confirms the vehicle’s value. For used cars, an independent valuation or inspection might be required to determine its current market worth, which directly impacts the maximum loan amount the lender is willing to provide.

Calculating Your Car Loan EMI: Financial Planning Made Easy

Understanding your Equated Monthly Installment (EMI) is fundamental to responsible car ownership. The EMI is the fixed amount you pay to your lender each month until your loan is fully repaid. Accurately calculating and budgeting for your EMI is crucial for maintaining financial stability.

Understanding the EMI Formula (Briefly)

While you don’t need to be a mathematician, knowing the components of the EMI formula helps you grasp how it works:

EMI = /

Where:

- P = Principal Loan Amount

- R = Monthly Interest Rate (Annual Rate / 12 / 100)

- N = Loan Tenure in Months

This formula ensures that a portion of your EMI goes towards paying the interest, and the remainder reduces your principal amount. In the initial months, a larger portion goes to interest, gradually shifting towards principal repayment as the loan progresses.

Importance of Online EMI Calculators

Thankfully, you don’t need to manually crunch these numbers. Every major bank and financial institution, as well as numerous financial portals, offer free online car loan EMI calculators. These tools are incredibly user-friendly. You simply input the principal loan amount, the interest rate, and the desired loan tenure, and the calculator instantly provides your estimated monthly EMI.

Pro Tip from us: Use these calculators extensively during your research phase. Experiment with different loan amounts, interest rates, and tenures to see how they impact your monthly payment. This helps you determine an EMI that comfortably fits within your budget.

Budgeting for Your Monthly Payments

Once you have a realistic EMI figure, it’s vital to integrate it into your overall monthly budget. Don’t just look at the EMI in isolation. Consider all your other monthly expenses – rent/mortgage, utilities, groceries, existing loan payments, and savings.

Your car loan EMI should be a manageable percentage of your disposable income. Common mistakes to avoid include overestimating your repayment capacity, which can lead to financial stress down the line. A good rule of thumb is that your total debt payments, including the car loan, should not exceed 30-40% of your net monthly income.

Pro Tip: Factor in More Than Just the EMI

Beyond the EMI, responsible car ownership involves several other recurring costs. When budgeting, always factor in:

- Car Insurance: Mandatory and a significant annual or monthly expense.

- Fuel Costs: Will vary based on usage and fuel type.

- Maintenance & Servicing: Regular upkeep is essential for your car’s longevity and performance.

- Parking Fees & Tolls: If applicable in your daily commute.

- Unexpected Repairs: It’s wise to set aside a small contingency fund.

By considering these additional expenses, you get a truly comprehensive picture of the financial commitment involved in owning a car, allowing for more robust financial planning. This holistic approach ensures your car ownership journey remains joyful and free from unexpected financial burdens.

Documents Required for a Seamless Application

Even in the most digital of environments, documentation remains a cornerstone of the loan application process. However, the modern approach, much like the convenience Ok Credit offers for business ledgers, emphasizes digital submission and clarity. Having all your documents ready and organized is key to a smooth and rapid approval.

1. Proof of Identity

This category confirms who you are. Lenders need to verify your identity to comply with KYC (Know Your Customer) regulations.

- PAN Card: A mandatory document for most financial transactions in India.

- Aadhaar Card: Widely accepted as a primary identity and address proof.

- Passport: Another valid proof of identity and address.

- Driving License: Often accepted as both identity and address proof.

Ensure the name on all your identity documents matches exactly to avoid any discrepancies.

2. Proof of Address

This confirms your residential address. Lenders need this to ensure you have a stable residence and for communication purposes.

- Utility Bills: Electricity bill, water bill, or gas bill (not older than 2-3 months).

- Bank Statements: Statements from your savings or current account, showing your address.

- Rent Agreement: If you are living in rented accommodation.

- Passport/Aadhaar: Can often serve as both identity and address proof.

It’s common for lenders to require at least two different proofs of address for verification.

3. Proof of Income

This is critical for assessing your repayment capacity. The documents required vary based on your employment status.

For Salaried Individuals:

- Salary Slips: Latest 3 to 6 months’ salary slips.

- Bank Statements: Last 6 to 12 months’ bank statements showing salary credits.

- Form 16 / Latest Income Tax Returns (ITR): For the last 1-2 financial years.

- Employment Certificate / Appointment Letter: To confirm your employment and tenure.

For Self-Employed Individuals / Professionals:

- Latest Income Tax Returns (ITR): For the last 2-3 financial years, along with computation of income.

- Audited Financial Statements: Balance sheet and Profit & Loss account for the last 2-3 years.

- Bank Statements: Last 6 to 12 months’ bank statements (personal and business accounts).

- Proof of Business Existence: Shop & Establishment Act Certificate, GST registration, partnership deed, etc.

Common Mistakes to Avoid: Submitting outdated income proofs or statements with insufficient balance. Ensure your bank statements clearly show consistent income and responsible financial habits.

4. Bank Statements

Separate from income proof, lenders often ask for your bank statements to understand your spending habits, existing EMIs, and overall financial health. These typically cover the last 6 to 12 months.

5. Vehicle-Related Documents

These are specific to the car you intend to purchase.

- Proforma Invoice / Quotation: From the car dealership for a new car.

- Copy of Registration Certificate (RC) and Insurance: For a used car, along with the seller’s KYC documents.

- Valuation Report: For certain used cars, an independent valuation might be required.

By meticulously gathering and organizing these documents, ideally as clear digital copies, you significantly expedite the car loan application process. This prepared approach aligns perfectly with the efficiency promised by digital finance solutions.

Advantages of Opting for Digital Car Loans (Like the "Ok Credit" Model)

The shift towards digital platforms in lending is not just a trend; it’s a fundamental improvement in how we access financial services. When we consider "Ok Credit Car Loans," we’re really talking about the significant benefits that come from applying the principles of digital ease and efficiency to vehicle financing.

1. Speed and Convenience: Loan on Your Terms

One of the most compelling advantages of digital car loans is the unparalleled speed and convenience they offer. You can apply from anywhere – your home, office, or even a car dealership – at any time, without being restricted by bank operating hours. The application process, from filling out forms to uploading documents, is streamlined and often takes mere minutes.

Based on my experience, this speed is a game-changer, especially when you’ve found your dream car and don’t want to risk it being sold. Digital pre-approvals mean you can walk into a dealership with financing already sorted.

2. Minimal Paperwork: Go Green, Go Digital

The traditional loan application often involved stacks of paper forms and photocopies. Digital car loans, on the other hand, significantly reduce paperwork. Most documents can be uploaded as scanned copies or digital photographs. Some advanced platforms even use APIs to fetch data directly with your consent, further minimizing the need for physical documents.

This not only makes the process environmentally friendly but also reduces the chances of errors or lost documents. It embodies the "Ok Credit" principle of simplifying record-keeping.

3. Wider Access to Lenders/Options: A Marketplace at Your Fingertips

The digital landscape connects you to a vast network of lenders, not just the local bank branches you might physically visit. Online comparison platforms and financial aggregators allow you to compare multiple loan offers simultaneously, including those from smaller, specialized lenders that might offer more competitive rates or flexible terms.

This increased visibility empowers you to make a more informed decision and find a loan that truly fits your financial profile, rather than settling for the first available option.

4. Transparency: Clearer Terms, Fewer Surprises

Digital platforms often provide a higher degree of transparency regarding loan terms, interest rates, fees, and repayment schedules. EMI calculators are readily available, and loan agreements are often presented in a clear, easy-to-understand format online.

This clarity helps borrowers understand their financial commitments upfront, reducing the likelihood of hidden charges or unexpected surprises later on. The "Ok Credit" model thrives on clear, accessible information, and this principle is equally valuable in digital lending.

5. Potential for Competitive Rates: The Power of Comparison

With easy access to compare offers from numerous lenders, the digital car loan market fosters healthy competition. This competition often translates into more attractive interest rates and better deals for borrowers. Lenders know you have options, prompting them to put their best foot forward.

By leveraging the power of digital comparison, you stand a much better chance of securing a car loan with terms that are genuinely favorable, potentially saving you a significant amount over the loan’s tenure.

Disadvantages & Considerations of Digital Car Loans

While digital car loans offer undeniable advantages, it’s crucial to approach them with a balanced perspective. Like any financial product, they come with certain considerations and potential drawbacks that borrowers should be aware of to ensure a secure and satisfying experience.

1. Digital Literacy Required: Bridging the Tech Gap

The convenience of digital applications relies heavily on the borrower’s digital literacy. Navigating online portals, uploading documents, understanding digital agreements, and using online calculators all require a certain level of comfort with technology. For individuals less familiar with digital tools, this can present a barrier or a learning curve.

Common mistakes to avoid include rushing through online forms or not understanding the interface, which can lead to errors in the application. Always take your time and seek assistance if needed.

2. Risk of Scams: Vigilance is Key

The digital world, unfortunately, is also fertile ground for scams and fraudulent activities. Unscrupulous entities might mimic legitimate lenders to trick applicants into sharing personal information or making upfront payments for non-existent loans.

Pro Tip from us: Always verify the authenticity of a lending platform. Look for secure website connections (HTTPS), read reviews, and never share sensitive information like OTPs or bank passwords. Legitimate lenders will never ask for upfront "processing fees" outside of standard, clearly disclosed charges.

3. Data Privacy Concerns: Protecting Your Information

When you apply for a digital loan, you share a significant