Pay Off Car Loan Early Calculator

Pay Off Car Loan Early Calculator Carloan.Guidemechanic.com

Pay Off Car Loan Early Calculator: Your Ultimate Guide to Financial Freedom and Savings

Pay Off Car Loan Early Calculator

The gleaming allure of a new car often comes with a financial companion: a car loan. For many, this auto loan represents a significant monthly obligation, sometimes stretching over five, six, or even seven years. While necessary, carrying this debt can feel like a heavy anchor, impacting your financial flexibility and long-term goals. But what if you could shed that burden sooner, saving a substantial amount of money in the process?

This is where the power of a Pay Off Car Loan Early Calculator comes into play. It’s more than just a simple online tool; it’s a strategic compass that can illuminate your path to debt freedom, revealing the true cost of your loan and showing you exactly how much you can save by accelerating your payments. In this super comprehensive guide, we’ll dive deep into why paying off your car loan early is a smart financial move, how to use this invaluable calculator effectively, and practical strategies to make it a reality. Prepare to unlock a future with more financial breathing room and less debt stress!

Why Pay Off Your Car Loan Early? The Compelling Benefits

Before we delve into the mechanics of the calculator, let’s establish why you should even consider paying off your car loan early. The reasons are compelling and often overlooked, but based on my extensive experience in personal finance, they can significantly alter your financial trajectory.

1. Save a Significant Amount on Interest

This is arguably the most impactful benefit. Car loans, like most loans, accrue interest over time. The longer you carry the debt, the more interest you pay. By making extra payments or increasing your monthly contribution, you reduce your principal balance faster. This, in turn, means less interest is calculated on the remaining balance over the loan’s life.

Think of it this way: every extra dollar you put towards the principal directly reduces the amount your lender can charge interest on. Over several years, even small, consistent extra payments can translate into hundreds or even thousands of dollars saved in interest. This money stays in your pocket, not the bank’s.

2. Achieve Financial Freedom Faster

Debt, by its very nature, limits your choices. A car loan payment is a fixed expense that eats into your monthly budget, potentially preventing you from saving for a down payment on a house, investing, or even enjoying a comfortable vacation. Eliminating this debt frees up a significant portion of your income.

Once your car loan is paid off, that monthly payment amount becomes disposable income. You can then redirect it towards other financial goals, such as building an emergency fund, contributing more to retirement, or tackling other higher-interest debts like credit cards. This accelerated path to debt freedom provides a tremendous sense of accomplishment and control.

3. Reduce Monthly Financial Burden and Stress

Having fewer monthly bills simply feels good. The weight of recurring debt payments can contribute to financial stress and anxiety. Paying off your auto loan early removes one significant source of this burden, leaving you with more peace of mind.

Imagine a month where you don’t have to factor in that car payment. This reduced financial pressure can improve your overall well-being and allow you to breathe a little easier, especially during unexpected financial challenges. It creates a buffer in your budget that wasn’t there before.

4. Free Up Cash Flow for Other Goals

That monthly car payment can be a substantial chunk of change. Once it’s gone, that cash flow is liberated. This newfound liquidity can be a game-changer for your financial planning.

Perhaps you’ve been wanting to start a side hustle, save for your child’s education, or finally invest in that home renovation. Paying off your car loan early provides the capital to pursue these aspirations without incurring additional debt or straining your current budget. It’s a strategic move to reallocate funds to areas that offer greater personal or financial returns.

5. Improve Your Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is a crucial metric lenders use to assess your ability to manage monthly payments and repay debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI ratio indicates less risk to lenders.

By paying off your car loan, you reduce your total monthly debt payments, thereby improving your DTI ratio. This can be particularly beneficial if you plan to apply for a mortgage or another significant loan in the near future, as a healthier DTI can lead to better interest rates and loan approval chances.

Understanding the "Pay Off Car Loan Early Calculator": Your Ultimate Financial Tool

Now that we’ve established the compelling reasons, let’s focus on the star of the show: the Pay Off Car Loan Early Calculator. This tool is your strategic partner in visualizing the impact of accelerating your car loan payments. It transforms abstract numbers into tangible savings and an earlier payoff date.

What It Is and How It Works

At its core, an early car loan payoff calculator is an online application designed to estimate how much interest you can save and how much faster you can pay off your car loan by making additional payments towards the principal. It uses a series of inputs to perform complex amortization calculations in a matter of seconds.

The magic happens behind the scenes, where the calculator recalculates your loan’s amortization schedule with your proposed extra payments factored in. It essentially simulates a new loan term and total cost based on your accelerated repayment plan. This immediate feedback makes it an incredibly powerful planning tool.

Key Inputs Required

To get accurate results from a car loan early payoff calculator, you’ll typically need to provide a few pieces of information about your current loan. Based on my experience, gathering these details before you start will make the process smooth and efficient:

- Current Loan Balance: This is the outstanding amount you still owe on your car. You can usually find this on your latest loan statement or by logging into your lender’s online portal.

- Original Loan Amount (sometimes optional): While some calculators ask for this, it’s often more critical to have your current balance.

- Original Loan Term (in months): This is how long you initially agreed to pay back the loan (e.g., 60 months, 72 months).

- Remaining Loan Term (in months): How many months are left until your loan is fully paid off under the original schedule.

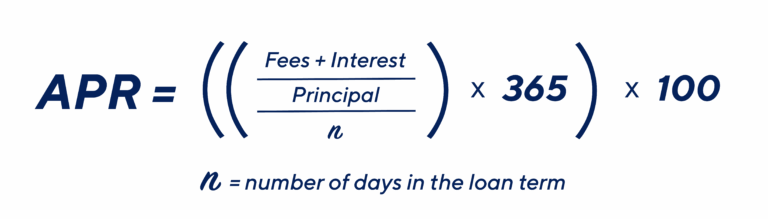

- Interest Rate (APR): The annual percentage rate of your loan. This is crucial for calculating interest savings.

- Current Monthly Payment: The standard amount you pay each month.

- Desired Extra Payment Amount: This is the "what if" factor. How much additional money are you considering paying each month? Or, if it’s a one-time lump sum, you’d input that.

Key Outputs Provided

Once you input your data, the auto loan early payoff calculator will quickly generate a wealth of valuable information, helping you make an informed decision:

- New Payoff Date: This shows you exactly how many months sooner you could be debt-free.

- Total Interest Saved: This is often the most eye-opening output, revealing the substantial amount of money you avoid paying to the lender.

- New Total Cost of Loan: The overall amount you will have paid for your car, including principal and interest, with your accelerated payments.

- Number of Payments Remaining: The revised count of how many payments are left until the loan is paid off.

These outputs allow you to clearly see the direct financial impact of your early payment strategy. It makes the abstract concept of "saving money" concrete and motivates you to take action.

How to Effectively Use a Car Loan Early Payoff Calculator (Step-by-Step Guide)

Using a Pay Off Car Loan Early Calculator is straightforward, but employing it strategically can maximize its benefits. Follow these steps for an optimal experience:

Step 1: Gather Your Loan Details

Before you even open the calculator, have all your current car loan information handy. This includes your exact remaining balance, interest rate (APR), original loan term, remaining loan term, and current monthly payment. Accuracy here is paramount for reliable results.

Pro tips from us: Don’t guess these numbers. Log into your loan servicer’s website or pull out your latest statement. Even a slight inaccuracy in the interest rate can significantly skew your projected savings.

Step 2: Enter Your Current Information

Input the gathered data into the corresponding fields of the calculator. Double-check each entry to ensure there are no typos. This initial entry establishes your baseline—what your loan looks like if you continue with your current payment schedule.

Some calculators might show you your current projected payoff date and total interest paid based on these inputs. This is your starting point for comparison.

Step 3: Experiment with Extra Payment Scenarios

This is where the real fun begins! Start by entering a realistic extra payment amount you believe you can consistently afford each month. For instance, if you can comfortably add an extra $50, $100, or even $200 to your payment, input that figure.

Then, try different scenarios:

- What if you make a one-time lump sum payment?

- What if you round up your payment to the nearest $50 or $100?

- What if you switch to bi-weekly payments?

Play around with these figures to see the varying impact on your payoff date and interest savings.

Step 4: Analyze the Results

Carefully review the outputs generated by the calculator for each scenario. Compare the new payoff date and total interest saved against your original loan terms. You’ll likely be surprised by how much even a small, consistent extra payment can accelerate your debt freedom and put money back in your pocket.

Common mistakes to avoid are focusing solely on the payoff date without considering the interest savings, or vice-versa. Both are crucial metrics. Look for the balance that best fits your financial goals and capabilities.

Step 5: Make an Informed Decision and Create a Plan

Based on your analysis, decide on an early payoff strategy that aligns with your budget and financial priorities. Once you have a target, create a concrete plan. This might involve setting up automatic extra payments with your lender, scheduling a one-time lump sum, or adjusting your budget to free up more funds.

Remember, the calculator is a tool for planning; consistent action is what brings the results. My professional advice would be to start with an amount you know you can sustain, and then gradually increase it as your financial situation improves.

Strategies to Accelerate Your Car Loan Payoff

Having a Pay Off Car Loan Early Calculator is fantastic for planning, but it’s the execution of smart strategies that truly brings your car loan payoff date closer. Here are several effective methods you can employ:

1. Make Extra Principal Payments

This is the most direct and effective strategy. Any amount you pay over your standard monthly payment should be designated as an extra principal payment. This means the money goes directly to reducing the outstanding loan balance, not towards future interest.

Pro tips from us: Always verify with your lender that extra payments are being applied directly to the principal. Some lenders automatically advance your due date if you pay extra without specific instructions, which doesn’t accelerate the payoff or save interest as effectively.

2. Implement Bi-Weekly Payments

Instead of making one monthly payment, divide your monthly payment in half and pay that amount every two weeks. Since there are 52 weeks in a year, this results in 26 bi-weekly payments, which equals 13 full monthly payments per year instead of 12.

This "extra" payment each year goes directly to reducing your principal, significantly shaving time and interest off your loan. Many auto loan early payoff calculators have a specific feature to model this strategy.

3. Round Up Your Payments

This is a simple yet effective psychological trick. If your payment is $347, round it up to $350 or even $375. The extra few dollars each month might seem insignificant, but they add up over time and go straight to the principal, accelerating your payoff.

This strategy often goes unnoticed in your budget, making it an easy habit to adopt without feeling a major pinch. Use the calculator to see the cumulative effect of even a small, consistent round-up.

4. Utilize Windfalls Wisely

Did you receive a tax refund, a work bonus, an inheritance, or a generous gift? Instead of spending it all, consider allocating a portion or even the entirety of these windfalls towards your car loan principal.

A single lump-sum payment can have a dramatic effect on your total interest paid and your payoff date. Run these scenarios through your car loan early payoff calculator to see the immediate impact.

5. Refinance to a Lower Interest Rate (If Applicable)

If interest rates have dropped since you took out your loan, or if your credit score has significantly improved, you might be eligible to refinance your car loan at a lower interest rate. This reduces the total interest you’ll pay over the life of the loan.

However, be cautious: ensure the new loan doesn’t extend your repayment period unnecessarily, which could negate some of the interest savings. Use a refinance calculator in conjunction with an early payoff calculator to assess the best strategy. For official information on consumer credit and auto loans, you can always refer to reputable sources like the Consumer Financial Protection Bureau (CFPB).

6. Sell Unused Assets or Cut Discretionary Spending

Look around your home for items you no longer need or use that could be sold online or at a garage sale. The proceeds can be applied as a lump sum towards your car loan. Additionally, scrutinize your budget for areas where you can temporarily cut back on discretionary spending (e.g., dining out, subscriptions).

Every dollar saved and redirected to your car loan acts as an accelerant. This requires discipline but can lead to significant progress.

Common Mistakes to Avoid When Paying Off Your Car Loan Early

While paying off your car loan early is generally a smart move, there are pitfalls to avoid. Based on my observations, these are the common mistakes people make that can undermine their efforts or even put them in a worse financial position:

1. Not Checking for Prepayment Penalties

Some loan agreements, though less common with auto loans than mortgages, include prepayment penalties. This is a fee charged by the lender if you pay off your loan ahead of schedule. Always review your loan documents or contact your lender to confirm whether such a penalty exists.

If a significant penalty applies, it might diminish or even negate the financial benefits of early payoff. In such cases, you’d need to weigh the penalty against the interest savings carefully using your calculator.

2. Not Specifying Extra Payments Go to Principal

As mentioned earlier, simply sending in extra money might not automatically apply it to the principal. Some lenders will "advance your due date," meaning your next payment isn’t due for a longer period, but you’re not saving as much interest as you could be.

Always explicitly state, in writing if possible, that any additional funds are to be applied directly to the principal balance. This ensures your efforts are maximized.

3. Prioritizing Car Loan Over High-Interest Debt

While freeing yourself from a car loan is great, it’s usually not the highest-interest debt you might have. Credit card debt, for example, often carries much higher interest rates (18-25% or more). From a purely mathematical perspective, tackling the highest-interest debt first saves you the most money.

Common mistakes I’ve seen people make are focusing on the car loan when they have revolving credit card balances. My professional advice would be to use a debt snowball or debt avalanche strategy, prioritizing high-interest debts before making significant extra payments on a lower-interest car loan.

4. Draining Your Emergency Fund

An emergency fund, typically 3-6 months of living expenses, is your financial safety net. Depleting this fund to pay off your car loan leaves you vulnerable to unexpected expenses like job loss, medical emergencies, or home repairs.

Never sacrifice your emergency savings for debt repayment. Ensure your emergency fund is robust before aggressively tackling your car loan.

5. Ignoring Other Financial Goals

While getting rid of your car loan is a worthy goal, it shouldn’t come at the expense of other critical financial objectives, such as contributing to your retirement accounts (especially if you’re missing out on employer matches) or saving for a down payment on a house.

It’s about balance. Use your Pay Off Car Loan Early Calculator to understand the impact, but also consider how it fits into your broader financial picture. For a deeper dive into creating a robust budget that balances debt repayment with other goals, check out our comprehensive guide on .

The Psychological Benefits of Being Debt-Free

Beyond the tangible financial savings, the psychological benefits of paying off your car loan early are profound and often underestimated.

Reduced Stress and Anxiety

Carrying debt can be a constant source of underlying stress. Knowing you owe money and have a recurring payment can weigh on your mind. Eliminating that obligation lifts a significant mental burden, leading to greater peace of mind and reduced anxiety.

The feeling of not having that particular payment looming over you each month is incredibly liberating and can positively impact your overall mental well-being.

Increased Confidence and Empowerment

Successfully paying off a loan early is a testament to your financial discipline and strategic planning. This achievement builds confidence in your ability to manage your money effectively and achieve your financial goals.

It’s an empowering feeling to take control of your finances rather than feeling controlled by them. This newfound confidence can spill over into other areas of your financial life, encouraging you to tackle more ambitious goals.

Sense of Accomplishment

There’s a genuine sense of accomplishment that comes with eradicating a debt. It’s a milestone worth celebrating, reinforcing positive financial habits and motivating you to continue on your path to complete financial freedom.

This feeling of success can be a powerful motivator, providing the momentum needed to tackle other debts or pursue new savings and investment opportunities.

Real-World Scenario: Seeing the Calculator in Action

Let’s illustrate the power of a Pay Off Car Loan Early Calculator with a quick example:

Imagine you have a car loan with these details:

- Original Loan Amount: $25,000

- Original Term: 60 months

- Interest Rate (APR): 6%

- Current Monthly Payment: ~$483

- Remaining Balance: $20,000

- Remaining Term: 48 months

If you continue with your current payment, you’ll pay off the loan in 48 months and pay approximately $2,000 in remaining interest.

Now, let’s use the calculator and add an extra $100 to your monthly payment, making it $583.

The calculator reveals:

- New Payoff Date: You could pay off your loan in just 34 months instead of 48! (14 months sooner)

- Total Interest Saved: You would save approximately $700 in interest.

- New Total Cost: The overall cost of your remaining loan would be significantly less.

This simple example demonstrates how even a relatively small extra payment can dramatically accelerate your payoff and put hundreds of dollars back in your pocket.

Integrating Early Payoff into Your Broader Financial Plan

Paying off your car loan early is an excellent step, but it’s crucial to view it as part of your overall financial strategy. It should complement, not hinder, your other financial goals.

Consider how the freed-up cash flow from an early payoff can be redirected:

- Building Your Emergency Fund: If it’s not fully funded, this should be a top priority.

- Paying Down Other Debts: Tackle credit cards, student loans, or other higher-interest consumer debt. If you’re looking to understand more about managing different types of debt, we recommend reading our article on .

- Increasing Retirement Contributions: Maximize your 401(k) or IRA contributions, especially if you’re getting an employer match.

- Saving for a Down Payment: If homeownership is a goal, this extra cash can build your down payment fund faster.

- Investing: Once your essential financial bases are covered, consider investing in the stock market or other assets for long-term wealth growth.

My professional advice is to create a comprehensive financial plan that outlines your short-term and long-term goals. An early car loan payoff can be a powerful catalyst for achieving many of these objectives.

Conclusion: Take Control with the Pay Off Car Loan Early Calculator

The journey to financial freedom can feel daunting, but tools like the Pay Off Car Loan Early Calculator empower you to take concrete steps towards that goal. By understanding the compelling benefits of early payoff – from significant interest savings to reduced stress and increased financial flexibility – you can transform your relationship with debt.

This calculator isn’t just about numbers; it’s about possibilities. It allows you to visualize a future where a major monthly obligation is gone, freeing up your income for what truly matters to you. So, don’t just dream about being debt-free; use this powerful tool to plan your escape route. Gather your loan details, experiment with extra payment scenarios, and commit to a strategy. Your future self, with more money in the bank and less debt on their shoulders, will thank you. Start exploring the power of a Pay Off Car Loan Early Calculator today and pave your way to a more financially secure tomorrow.