Refinancing Your Car Loan Without a Cosigner: Unlocking Your Financial Independence

Refinancing Your Car Loan Without a Cosigner: Unlocking Your Financial Independence Carloan.Guidemechanic.com

Many of us start our car ownership journey with a little help from a loved one. A cosigner can be a lifesaver when you’re just starting out, helping you secure a better interest rate or even get approved for a loan in the first place. But as time goes on and your financial standing improves, that shared responsibility might start to feel less like a help and more like a lingering tie. The big question then becomes: Can you refinance a car loan without the cosigner?

The short answer is a resounding yes, it is absolutely possible! However, it’s not always a straightforward process and hinges entirely on your current financial health and creditworthiness. As an expert in personal finance and auto lending, I’ve seen countless individuals navigate this very path to achieve financial independence. This comprehensive guide will walk you through everything you need to know, from understanding lender expectations to implementing strategies for success.

Refinancing Your Car Loan Without a Cosigner: Unlocking Your Financial Independence

Why Would You Want to Remove a Cosigner from Your Car Loan?

Before we dive into the "how," let’s briefly touch upon the "why." While a cosigner provides invaluable support, there are compelling reasons why you might want to remove them from your car loan.

First and foremost, it’s about financial independence. Taking full ownership of your debts means you’re solely responsible, which can be a significant step in your personal financial journey. It signifies that you’ve matured financially and are capable of managing substantial credit on your own.

Secondly, removing a cosigner alleviates their financial obligation and liability. As long as they’re on your loan, your payment history (good or bad) affects their credit report. More importantly, if you default on the loan, they are legally responsible for the entire debt. Freeing them from this burden can significantly improve their peace of mind and your relationship.

Finally, you might be seeking better loan terms. If your credit score has improved significantly since you first took out the loan, or if interest rates have dropped, refinancing solo could lead to a lower interest rate, a reduced monthly payment, or even a shorter loan term. This can save you a substantial amount of money over the life of the loan.

The Possibility of Solo Refinancing: What Lenders Look For

When you initially secured your car loan with a cosigner, the lender was assessing both of your financial profiles. The cosigner’s good credit and stable income acted as a safety net. Now, if you want to refinance alone, the lender will focus solely on your ability to repay the loan. This means you need to demonstrate that you are a low-risk borrower on your own.

Based on my experience, lenders typically scrutinize several key factors when considering a solo refinance application. Understanding these elements is crucial for preparing your application and increasing your chances of approval.

1. Your Credit Score: The Ultimate Indicator of Risk

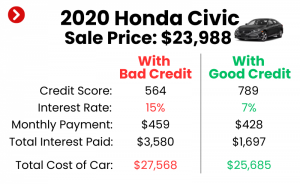

Your credit score is arguably the most critical factor lenders consider. It’s a three-digit number that summarizes your creditworthiness, reflecting your history of borrowing and repaying debt. A higher score indicates a lower risk to lenders.

When you initially applied with a cosigner, perhaps your score wasn’t strong enough. Now, for a solo refinance, you’ll need a solid score, generally in the "good" to "excellent" range (typically 670 or above), although some lenders may approve scores slightly lower depending on other factors. This score tells the lender that you are responsible with credit and have a proven track record of making on-time payments.

Pro tips from us: Before even thinking about applying, get a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion). You can do this for free annually at AnnualCreditReport.com. Review it for any errors and dispute them immediately. Even small discrepancies can negatively impact your score. For a deeper dive into improving your credit score, check out our guide on .

2. Stable Income and Employment History: Your Ability to Pay

Lenders want to be confident that you have a consistent and reliable source of income to cover your monthly car payments. They look for stability in your employment history. This typically means having a steady job for at least six months to two years with verifiable income.

They will ask for proof of income, which usually includes recent pay stubs, W-2 forms, and sometimes even tax returns. If you are self-employed, you’ll need to provide more extensive documentation, such as several years of tax returns and bank statements, to demonstrate consistent income. The goal is to show a predictable income stream that can comfortably support your existing expenses plus the new car payment.

3. Debt-to-Income (DTI) Ratio: How Much Debt You’re Already Carrying

Your Debt-to-Income (DTI) ratio is a crucial metric that illustrates how much of your gross monthly income goes towards paying your debts. Lenders use this to assess if you can handle additional debt, like a new car loan payment. A lower DTI indicates that you have more disposable income available, making you a less risky borrower.

To calculate your DTI, sum up all your monthly debt payments (car loans, student loans, credit card minimums, mortgage/rent) and divide that by your gross monthly income (before taxes). For example, if your total monthly debt payments are $1,000 and your gross monthly income is $4,000, your DTI is 25% ($1,000 / $4,000). Lenders generally prefer a DTI of 36% or lower, though some may go up to 43% depending on other strong factors.

Common mistakes to avoid are: applying for a refinance right after taking on new significant debt, like a personal loan or a new credit card. This will inflate your DTI and could lead to denial. Focus on paying down existing high-interest debts before applying for a refinance.

4. Loan-to-Value (LTV) Ratio: The Car’s Worth vs. The Loan Amount

The Loan-to-Value (LTV) ratio compares the amount you want to borrow (the outstanding balance on your current car loan) to the current market value of your vehicle. Lenders prefer a low LTV because it means they have less risk if you default. If the car’s value is significantly higher than the loan amount, it means you have positive equity.

For instance, if your car is worth $20,000 and you owe $15,000, your LTV is 75% ($15,000 / $20,000). A good LTV for refinancing is typically below 100%, ideally closer to 80-90%. Cars depreciate rapidly, so it’s possible to be "upside down" (owe more than the car is worth), which makes solo refinancing much harder. In such cases, lenders might require you to pay down a portion of the loan to achieve a more favorable LTV.

5. Your Payment History on the Current Loan: Proof of Responsibility

Perhaps the most direct evidence of your ability to manage an auto loan is your payment history on the current car loan. Lenders will carefully review your payment record for the existing loan, especially since you’re trying to remove the cosigner. A flawless history of on-time payments is absolutely critical.

This demonstrates to the new lender that even with a cosigner, you have been the one consistently making the payments without any late marks. Any late payments, especially recent ones, can be a major red flag and significantly hinder your chances of approval. This history proves your reliability and commitment to your financial obligations.

Steps to Successfully Refinance a Car Loan Without a Cosigner

Now that you understand what lenders are looking for, let’s outline the practical steps to take. Approaching this process methodically will significantly improve your chances of success.

Step 1: Assess Your Current Financial Standing

Before you even look at lenders, take an honest look in the mirror at your finances. This is where you put theory into practice.

- Check Your Credit Report and Score: As mentioned, get your reports from all three bureaus. Understand your current scores and identify any negative marks that might need addressing.

- Calculate Your DTI: Use your recent pay stubs and statements for all debts to accurately calculate your debt-to-income ratio. Be realistic about your current financial obligations.

- Determine Your Car’s Value: Use online tools like Kelley Blue Book (KBB.com) or Edmunds to get an estimate of your car’s current market value. Compare this to your outstanding loan balance to get a sense of your LTV.

This initial assessment will give you a clear picture of your strengths and weaknesses as a solo applicant. If your numbers aren’t where they need to be, you’ll know what to work on.

Step 2: Improve Your Credit Score (If Needed)

If your initial assessment reveals a less-than-ideal credit score, don’t despair. You can take proactive steps to improve it, even if it means delaying your refinance application by a few months.

- Pay All Bills On Time: This is the single most impactful action. Set up automatic payments to avoid missing due dates.

- Reduce Credit Card Balances: Keep your credit utilization (the amount of credit you’re using compared to your total available credit) below 30%. Paying down high balances can quickly boost your score.

- Avoid New Credit: Don’t open new credit accounts or apply for other loans in the months leading up to your refinance application. This can create hard inquiries and increase your DTI.

- Address Errors: Dispute any inaccuracies on your credit report immediately.

Improving your credit score not only increases your chances of approval but also helps you secure a lower interest rate, saving you money in the long run.

Step 3: Gather Necessary Documents

Being prepared with all the required documentation will streamline your application process and demonstrate your seriousness to lenders. While requirements can vary slightly, generally you’ll need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (last 2-3 months), W-2s, tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Current Loan Information: Account number, outstanding balance, lender contact details.

- Vehicle Information: Make, model, year, VIN (Vehicle Identification Number), mileage.

- Insurance Information: Proof of comprehensive and collision insurance.

Having these documents organized and readily available will make the application process much smoother and faster.

Step 4: Shop Around for Lenders

This is a critical step that many people overlook, costing them potentially thousands of dollars. Do not simply go with your current lender or the first offer you receive. Different lenders have different criteria, interest rates, and fees.

- Explore Various Lender Types: Check with traditional banks, credit unions, and online lenders. Credit unions, in particular, often offer competitive rates to their members.

- Get Pre-Approved: Many lenders offer a pre-approval process that involves a soft credit pull (which doesn’t harm your credit score). This gives you an idea of the rates and terms you might qualify for without committing.

- Compare Offers: Look beyond just the interest rate. Consider the loan term, any fees (origination fees, prepayment penalties), and the overall monthly payment.

Pro tips from us: Aim to get several quotes within a short period (typically 14-45 days). This allows all inquiries to be treated as a single hard inquiry on your credit report, minimizing the impact on your score. If you’re unsure about the pros and cons of refinancing in general, our article offers valuable insights.

Step 5: Submit Your Application

Once you’ve chosen a few promising lenders, it’s time to formally apply. Be prepared to provide all the documentation you gathered in Step 3.

- Be Honest and Thorough: Provide accurate information. Any discrepancies could lead to delays or even rejection.

- Ask Questions: If anything in the application is unclear, don’t hesitate to ask the lender for clarification.

- Understand the Hard Inquiry: Submitting a formal application will typically result in a "hard inquiry" on your credit report. This can temporarily ding your score by a few points, but the impact is usually minor and short-lived, especially if you get multiple quotes within a short window.

Step 6: Review Loan Offers

Carefully read through any loan offers you receive. Don’t rush this part.

- Interest Rate (APR): This is the most obvious factor, but also look at whether it’s fixed or variable. A fixed rate is usually preferable for predictability.

- Loan Term: A shorter term means higher monthly payments but less interest paid overall. A longer term means lower monthly payments but more interest over time.

- Fees: Check for any origination fees, application fees, or prepayment penalties.

- Total Cost of the Loan: Use an online calculator to see the total amount you’ll pay over the life of the loan with different offers. This gives you the clearest picture of what you’re truly saving.

Choose the offer that best aligns with your financial goals and current budget.

Step 7: Finalize the Deal

Once you’ve accepted an offer, the lender will guide you through the closing process. This typically involves:

- Signing the New Loan Agreement: Read every line carefully before signing.

- Paying Off the Old Loan: The new lender will send funds directly to your previous lender to pay off the existing loan.

- Updating Vehicle The new lender will take over as the lienholder on your car’s title. Ensure all necessary paperwork is completed to reflect this change and officially remove your cosigner.

Congratulations! You’ve successfully refinanced your car loan and achieved financial independence.

Common Pitfalls and How to Avoid Them

Even with the best intentions, people sometimes stumble. Based on my experience, here are some common mistakes to avoid:

- Applying with a Poor Credit Score: This is a recipe for rejection or, at best, a very high interest rate. Take the time to improve your score first.

- Not Comparing Lenders: Settling for the first offer means you’re likely leaving money on the table. Always shop around.

- Ignoring the Fine Print: Don’t just look at the monthly payment. Read the entire loan agreement for hidden fees, prepayment penalties, or unfavorable terms.

- Increasing Debt Before Applying: Taking on new credit or making large purchases right before applying for a refinance will negatively impact your DTI and credit score.

- Not Having a Clear Goal: Are you aiming for a lower monthly payment, less interest, or a shorter loan term? Know your primary objective so you can choose the right loan.

What If You Can’t Refinance Alone Right Now? Alternative Strategies

It’s possible that despite your best efforts, you might not qualify to refinance without a cosigner at this very moment. Don’t get discouraged! This just means you need a little more time and strategy.

- Wait and Improve: Continue making on-time payments on your current loan. Work diligently on improving your credit score and reducing other debts. Revisit the idea in 6-12 months. Consistency is key.

- Pay Down the Principal: If you can afford it, making extra payments towards the principal of your current loan will reduce your outstanding balance. This improves your LTV ratio and demonstrates greater financial responsibility, making you a more attractive solo borrower later.

- Negotiate with Your Current Lender: While less common for removing a cosigner, sometimes your existing lender might be willing to explore options if you have an excellent payment history. It’s always worth a conversation.

- Consider a Smaller Loan Amount (If Possible): If your LTV is the issue, and you have some cash saved, you could potentially pay down a portion of the loan upfront to make the refinance amount more appealing to lenders.

Pro Tips for a Smooth Solo Refinancing Journey

My years in the financial industry have taught me that preparation and proactive steps make all the difference. Here are a few final pro tips:

- Start Early: Don’t wait until you’re desperate. Begin assessing your finances and credit well in advance of when you hope to refinance.

- Be Transparent: When talking to lenders, be honest about your financial situation. They appreciate candor and can often offer better advice if they have the full picture.

- Don’t Be Afraid to Ask Questions: If you don’t understand a term, a calculation, or a requirement, ask! It’s your money and your future.

- Understand the Commitment: Even though you’re removing a cosigner, you are still entering into a significant financial commitment. Ensure the new payment is comfortably within your budget.

- Maintain Good Financial Habits: Once you’ve refinanced, continue to practice excellent financial habits. This will set you up for future financial success and independence across all areas of your life.

Conclusion: Your Path to Financial Freedom

Refinancing a car loan without a cosigner is a tangible goal for many, representing a significant step towards full financial independence. While it requires diligence, preparation, and a solid financial standing, it is absolutely achievable. By understanding the key factors lenders evaluate – your credit score, income stability, DTI, LTV, and payment history – and by meticulously following the steps outlined in this guide, you can successfully navigate the process.

Don’t let the thought of a cosigner hold you back from achieving your financial goals. Take control, prepare thoroughly, shop wisely, and soon you could be enjoying the freedom and responsibility of being the sole owner and obligor of your car loan. Your journey to financial autonomy starts now!