Rev Up Your Ride: Securing a Car Loan as a Self-Employed Individual with Good Credit

Rev Up Your Ride: Securing a Car Loan as a Self-Employed Individual with Good Credit Carloan.Guidemechanic.com

For the self-employed entrepreneur, the freedom of the open road is often synonymous with the freedom of running your own business. However, when it comes to financing that perfect vehicle, the path to a car loan can sometimes feel a little less straightforward than it is for traditionally employed individuals. While you might enjoy excellent credit, lenders often look at self-employment with a more scrutinizing eye.

But here’s the good news: having good credit is a monumental advantage! It signals financial responsibility and reliability, significantly easing the loan application process. This comprehensive guide is designed to empower self-employed individuals with good credit, providing you with the insights and strategies needed to secure the best possible car loan. We’ll break down exactly what lenders want to see, how to present your financial story effectively, and common pitfalls to avoid.

Rev Up Your Ride: Securing a Car Loan as a Self-Employed Individual with Good Credit

The Unique Landscape of Self-Employed Car Loans

As a self-employed individual, your income streams can sometimes appear less predictable to a lender compared to someone with a fixed salary and a W-2. Lenders typically prefer the stability of a regular paycheck. This doesn’t mean you’re out of luck; it just means you need to present your financial health in a way that clearly demonstrates consistency and reliability.

Your good credit score is your golden ticket in this scenario. It acts as a powerful counterweight to the perceived income volatility. A strong credit history tells lenders that you honor your financial commitments, making you a less risky borrower. It’s about showcasing your overall financial discipline, not just your monthly income figure.

What Lenders Look For: More Than Just a Credit Score

While your good credit score is a fantastic starting point, lenders assess several factors to determine your eligibility and the terms of your car loan. They want to ensure you have the capacity and willingness to repay the debt. For the self-employed, this assessment involves a deeper dive into your financial records.

A Strong Credit History (Your Foundation)

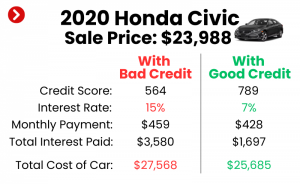

Your credit score, typically ranging from 300 to 850, is a numerical representation of your creditworthiness. A "good" credit score generally starts around 670, with excellent scores being 800 and above. This score is built upon your payment history, the amount of debt you owe, the length of your credit history, new credit inquiries, and the types of credit you use.

For self-employed individuals, a robust credit history is even more critical. It demonstrates a proven track record of managing debt responsibly, which directly addresses a lender’s primary concern: repayment risk. With good credit, you’re positioned for lower interest rates and more favorable loan terms, saving you a significant amount over the life of the loan. Based on my experience, a good credit score can often overcome initial hesitations lenders might have about non-traditional employment.

Verifiable Income: The Self-Employed Hurdle (and How to Clear It)

This is often the trickiest part for self-employed applicants. Lenders need to confirm that your income is sufficient, stable, and sustainable enough to cover the car loan payments comfortably. Unlike salaried employees who can simply provide a pay stub, you’ll need to offer a more comprehensive picture of your earnings.

The key here is consistency. Lenders want to see a history of steady income, not just a few good months. They are looking for patterns that suggest your business is thriving and capable of generating reliable income over the long term. This often means providing documentation covering the past one to two years, sometimes even longer.

Debt-to-Income (DTI) Ratio: Your Financial Health Snapshot

Your Debt-to-Income (DTI) ratio is a critical metric that lenders use to assess your ability to manage monthly payments. It’s calculated by dividing your total monthly debt payments (including the proposed car loan) by your gross monthly income. For example, if your total monthly debt payments are $1,500 and your gross monthly income is $4,000, your DTI is 37.5% ($1,500 / $4,000 = 0.375).

Lenders typically prefer a DTI ratio below 36% to 43%, though this can vary. A lower DTI indicates you have more disposable income available to handle additional debt, making you a less risky borrower. Even with excellent credit, a very high DTI can make securing a loan challenging, as it suggests you might be overextended. Pro tips from us: actively monitor and work to keep your DTI low by paying down existing debts before applying for new credit.

Down Payment: Showing Your Commitment

While not always strictly required, making a significant down payment on your car loan offers several advantages, especially for the self-employed. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the loan term.

More importantly, it signals to lenders that you are financially stable and committed to the purchase. It reduces the lender’s risk, as they have less capital at stake. Common mistakes to avoid are underestimating the power of a down payment; even 10-20% can make a substantial difference in both approval odds and loan terms.

Essential Documents for Your Car Loan Application (Self-Employed Edition)

Preparation is paramount when applying for a car loan as a self-employed individual. Gathering all necessary documents beforehand will streamline the process and present you as a responsible, organized borrower. Here’s a detailed list of what you’ll typically need:

-

Personal Identification & Proof of Residency:

- Detailed Explanation: Lenders need to verify who you are and where you live. This usually includes a valid government-issued photo ID (driver’s license, passport) and proof of your current address, such as a utility bill, bank statement, or lease agreement. Ensure these documents are up-to-date and clearly legible. This is standard for any loan application.

-

Proof of Income (The Most Crucial Element):

- Detailed Explanation: This is where self-employed individuals differ most from traditional employees. You’ll need to provide robust evidence of your consistent income.

- Tax Returns: Lenders typically request your federal income tax returns for the past two to three years (Form 1040, Schedule C for sole proprietors, Schedule K-1 for partnerships/S-corps). These documents provide an official, verifiable record of your declared income. Lenders often look at your net taxable income, so be prepared for that.

- Bank Statements: Provide personal and, if applicable, business bank statements for the most recent 6-12 months. These show consistent deposits and withdrawals, painting a picture of your cash flow. Lenders look for regularity in deposits that align with your declared income.

- Profit & Loss (P&L) Statements: If you have a formal business, professionally prepared P&L statements (sometimes called income statements) can demonstrate your business’s financial performance over specific periods. These should ideally be prepared by an accountant.

- Invoices and Contracts: For certain professions, copies of recent client invoices or long-term contracts can further support your income claims, especially if your income fluctuates seasonally.

- Detailed Explanation: This is where self-employed individuals differ most from traditional employees. You’ll need to provide robust evidence of your consistent income.

-

Business Registration/Licensing (If Applicable):

- Detailed Explanation: If your business is formally registered (e.g., LLC, Corporation), providing copies of your business license or articles of incorporation can add credibility to your self-employment status. This shows you’re operating a legitimate business entity. Even for sole proprietors, any relevant professional licenses can be beneficial.

-

Proof of Down Payment:

- Detailed Explanation: If you plan to make a down payment, lenders will want to see proof that these funds are readily available. This typically involves a bank statement showing the funds in your account, or a check that will be used for the down payment. This verifies that the funds are indeed liquid and accessible.

-

Credit Report Access:

- Detailed Explanation: While lenders will pull your credit report themselves, it’s always a good practice to review your own credit report beforehand. You can obtain a free copy annually from each of the three major credit bureaus (Experian, Equifax, TransUnion) via AnnualCreditReport.com. This allows you to identify and dispute any errors that could negatively impact your score before a lender sees them.

Navigating the Application Process: Step-by-Step for Success

Applying for a car loan can feel daunting, but by following a structured approach, you can significantly increase your chances of approval and secure favorable terms.

Step 1: Know Your Credit Score (and History)

Before you even think about looking at cars, pull your credit reports and scores. Understand what’s on your report, check for any inaccuracies, and get a realistic picture of your credit standing. This knowledge empowers you to approach lenders confidently and helps you anticipate the types of offers you might receive.

Step 2: Organize Your Financial Documents

As detailed above, gathering all your income verification documents, tax returns, and bank statements before you apply is crucial. Having everything ready demonstrates your seriousness and efficiency to the lender. It prevents delays and ensures you can provide prompt answers to any questions they might have.

Step 3: Get Pre-Approved (A Game Changer)

Getting pre-approved for a car loan is one of the most powerful steps you can take as a self-employed individual. Pre-approval means a lender has reviewed your financial information and tentatively agreed to lend you a specific amount at a particular interest rate, before you even choose a car.

Benefits of Pre-Approval:

- Budget Clarity: You know exactly how much you can afford, preventing you from falling in love with a car outside your price range.

- Negotiating Power: You walk into the dealership as a cash buyer, which gives you leverage to negotiate a better vehicle price. You’re focused on the car’s price, not the monthly payment.

- Streamlined Process: It significantly speeds up the buying process at the dealership.

- Confidence: It reduces stress and uncertainty during the car buying experience.

Step 4: Explore Lender Options

Don’t limit yourself to just the dealership’s financing office. Shop around for the best loan terms.

- Traditional Banks: Your existing bank or credit union might be a good first stop, as they already have a relationship with you and access to your financial history.

- Credit Unions: Often known for competitive rates and personalized service.

- Online Lenders: Many online platforms specialize in car loans and can offer quick approvals and competitive rates, sometimes even catering to specific borrower profiles.

- Dealership Finance: While convenient, their rates might not always be the most competitive. Use your pre-approval offer to benchmark their rates.

Step 5: Compare Offers and Negotiate

Once you have multiple loan offers (ideally from pre-approvals), compare them carefully. Look beyond just the monthly payment. Focus on:

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and fees.

- Loan Term: A shorter term means higher monthly payments but less total interest paid. A longer term means lower monthly payments but more interest over time.

- Total Cost of the Loan: Calculate the total amount you’ll pay back (principal + interest).

Don’t be afraid to use competing offers to negotiate for a better rate or terms. Your good credit gives you this advantage.

Pro Tips for Self-Employed Car Loan Success

Even with good credit, a little extra effort can go a long way in securing the best possible car loan.

- Maintain Meticulous Records: This cannot be stressed enough. Keep all your financial documents organized, whether digitally or physically. This includes tax returns, bank statements, invoices, and business receipts. When a lender asks for something, you want to be able to provide it immediately.

- Keep Personal and Business Finances Separate: This is a golden rule for self-employed individuals. Mixing funds makes it incredibly difficult to accurately assess your personal income and expenses, which is what lenders primarily care about for a personal car loan. Use separate bank accounts and credit cards for business transactions.

- Consider a Co-Signer (Even with Good Credit): While your good credit is a huge asset, if your DTI is a bit high or your business is relatively new, a co-signer with excellent credit and stable income can further strengthen your application. This adds another layer of security for the lender.

- Build a Strong Relationship with a Bank/Credit Union: Loyalty can sometimes pay off. If you have a long-standing relationship with a financial institution, they might be more inclined to work with you due to your established history as a customer.

- Don’t Apply for Too Many Loans at Once: Each loan application results in a "hard inquiry" on your credit report, which can temporarily ding your credit score. Bunch your applications within a short window (typically 14-45 days) so they count as a single inquiry for scoring purposes.

- Understand the Vehicle’s Value: Research the fair market value of the car you intend to purchase. Lenders are less likely to approve loans that significantly exceed the vehicle’s actual worth. This also helps you avoid overpaying.

Common Mistakes Self-Employed Individuals Make (and How to Avoid Them)

Being self-employed brings unique challenges, and it’s easy to stumble if you’re not prepared.

- Lack of Documentation: The most frequent mistake. Many self-employed individuals underestimate the amount of paperwork lenders require. Avoid this by: Starting to gather your documents weeks, if not months, before you plan to apply.

- Inflating Income or Misrepresenting Financials: Never provide inaccurate information on your application. Lenders have sophisticated ways of verifying income, and misrepresentation can lead to outright denial or even legal trouble. Avoid this by: Always being truthful and providing verifiable documentation.

- Not Getting Pre-Approved: Relying solely on dealership financing often means you miss out on potentially better rates and lose significant negotiation power. Avoid this by: Applying for pre-approval from at least two external lenders before stepping foot on a car lot.

- Ignoring Debt-to-Income (DTI) Ratio: Focusing only on your credit score and neglecting your overall debt burden. A high DTI can be a deal-breaker, even with good credit. Avoid this by: Calculating your DTI yourself and actively working to reduce existing debts before applying for a new loan.

- Applying with a New Business: If your business is less than two years old, many lenders will view it as too risky, regardless of your personal credit. They prefer to see a longer track record of profitability. Avoid this by: Waiting until your business has at least two years of solid financial history, or preparing to explain your business model and future projections very thoroughly.

The Benefits of Good Credit for Self-Employed Car Loans

Let’s reiterate why your good credit is such a powerful asset in this journey.

- Lower Interest Rates: This is arguably the biggest advantage. A lower APR means you’ll pay less interest over the life of the loan, saving you potentially thousands of dollars.

- Better Loan Terms: Lenders are more willing to offer flexible terms, such as longer repayment periods (if desired) or more favorable payment structures, to borrowers with strong credit.

- Higher Approval Odds: Good credit significantly increases your chances of being approved for a loan, even when your self-employment income might raise some questions. It demonstrates your reliability.

- More Options and Flexibility: With good credit, you’ll have a wider array of lenders and loan products to choose from, allowing you to pick the option that best fits your financial situation.

- Faster Approval Process: Lenders can process applications from high-credit borrowers more quickly because less risk assessment is needed.

Conclusion: Drive Your Ambition Forward

Securing a car loan as a self-employed individual with good credit is not just possible; it’s a realistic and often straightforward process when approached correctly. Your good credit score is your most valuable asset, opening doors to competitive rates and favorable terms. By understanding what lenders look for, meticulously organizing your financial documents, and proactively seeking pre-approval, you can navigate the application process with confidence and ease.

Don’t let the unique nature of self-employment deter you from getting the vehicle you need and deserve. Prepare thoroughly, present your financial story clearly, and leverage your excellent credit standing. The open road awaits – go get that car! Start gathering your documents today and take the first step towards driving your ambition.