Rolling Old Car Loan Into New One: The Ultimate Guide to Understanding the Risks and Rewards

Rolling Old Car Loan Into New One: The Ultimate Guide to Understanding the Risks and Rewards Carloan.Guidemechanic.com

The dream of a new car is powerful – that fresh scent, the latest tech, the promise of reliable journeys. But for many, the path to a new vehicle isn’t always smooth, especially if you still owe money on your current car, or even worse, owe more than it’s worth. This common predicament often leads people to consider a complex financial maneuver: rolling an old car loan into a new one.

This strategy, while seemingly convenient, is fraught with potential pitfalls that can trap you in a cycle of debt. As an expert blogger and professional SEO content writer, I’ve seen firsthand how this decision can impact personal finances. This comprehensive guide will dissect every aspect of rolling over a car loan, offering in-depth insights, practical advice, and crucial warnings to help you make the most informed decision possible.

Rolling Old Car Loan Into New One: The Ultimate Guide to Understanding the Risks and Rewards

What Does "Rolling Over Your Car Loan" Actually Mean?

At its core, rolling an old car loan into a new one means taking the outstanding balance of your current car loan and adding it to the principal of your new car loan. This typically happens when you trade in your old car, but its trade-in value is less than what you still owe on it. This difference is known as "negative equity" or being "upside down" on your loan.

Imagine you owe $10,000 on your current car, but the dealership offers you only $7,000 for it as a trade-in. You have $3,000 in negative equity. If you decide to roll this over, that $3,000 will be tacked onto the price of your new car, increasing the total amount you need to finance.

Why Do People Consider Rolling Over a Car Loan?

The allure of a new vehicle often outweighs financial prudence for many. There are several common reasons why individuals might consider rolling over an existing car loan:

1. The Need for a New Vehicle

Life happens. Your current car might be breaking down frequently, repairs are mounting, or perhaps your family has grown, necessitating a larger, safer vehicle. Sometimes, the perceived urgency for reliable transportation can push people towards this option.

2. Desire for Lower Monthly Payments (The Illusion)

Some consumers believe that by extending the loan term for a new car, even with negative equity rolled in, they can achieve lower monthly payments. While this might be true on a superficial level, it often masks a much larger total cost over the life of the loan.

3. Escaping a High-Interest Rate on the Old Loan

If you’re stuck with a high-interest rate on your current loan, you might hope that a new loan, even a larger one, could come with a better rate. While possible, the increased principal due to negative equity often negates any interest rate savings.

4. Financial Hardship or Convenience

For some, rolling over a loan seems like the easiest way out of a difficult situation. They might not have the cash to cover the negative equity or prefer the simplicity of one combined loan, even if it’s financially detrimental. This convenience often comes at a steep price.

The Mechanics: How Rolling Negative Equity Works

Understanding the actual process is crucial to grasp the financial implications. When you decide to trade in a car with negative equity and roll it into a new loan, here’s a simplified breakdown:

First, your negative equity is calculated. This is the difference between your current loan balance and the trade-in value of your car. For example, if you owe $15,000 and your car is worth $12,000, you have $3,000 in negative equity.

Next, this negative equity is added to the purchase price of your new vehicle. So, if your new car costs $30,000, and you have $3,000 in negative equity, your new loan amount effectively starts at $33,000 before any taxes, fees, or additional down payments. This immediately puts you further upside down on your new car.

Pro tips from us: Always ask the dealership for a clear breakdown of the new car’s price, your trade-in value, your old loan payoff, and the exact amount of negative equity being added to your new loan. Do not sign anything until you fully understand each line item. Transparency is key to avoiding unpleasant surprises down the road.

The Risks and Downsides of Rolling Over Your Car Loan

While it offers a seemingly simple solution, rolling over a car loan comes with significant financial risks that can compound over time. Understanding these downsides is paramount before making such a decision.

1. Increased Debt

This is the most obvious and significant risk. You are essentially borrowing money to pay off old debt, adding it to a new, larger loan. This immediately puts you further behind on your new vehicle.

2. Higher Monthly Payments

Despite the hope for lower payments, rolling over negative equity often results in higher monthly payments, especially if you maintain a reasonable loan term. Even if the payment feels manageable, the underlying debt burden has increased significantly.

3. Longer Loan Term

To make the higher loan amount affordable, lenders often extend the loan term (e.g., from 60 months to 72 or even 84 months). This means you’ll be paying for your car for a much longer period, prolonging your debt.

4. More Interest Paid Overall

A larger principal combined with a longer loan term invariably leads to paying substantially more in interest over the life of the loan. Even a seemingly small increase in the loan amount can translate to thousands of extra dollars in interest.

5. Deeper Negative Equity Cycle

New cars depreciate rapidly, especially in the first few years. By rolling over negative equity, you start your new car ownership journey already upside down, often deeper than before. This makes it harder to sell or trade in the car in the future without facing the same problem, perpetuating a vicious cycle.

6. Rapid Depreciation Exacerbation

The initial depreciation of a new vehicle, combined with the rolled-over negative equity, means you could owe significantly more than your car is worth for a substantial portion of the loan term. This limits your flexibility if your financial situation changes.

Common mistakes to avoid are: Focusing solely on the monthly payment without considering the total amount financed, the interest rate, and the loan term. Always look at the big picture and understand the true cost of the loan.

When Might Rolling Over Be a "Necessary Evil"? (Rare Scenarios)

While generally not recommended, there are extremely rare and specific circumstances where rolling over a car loan might be the least bad option. These situations typically involve unavoidable financial or practical exigencies.

1. Your Current Car is Unreliable and Unsafe

If your existing vehicle is a constant drain on your finances due to frequent, expensive repairs and poses a safety risk, replacing it might be non-negotiable. In such cases, if you absolutely cannot cover the negative equity out-of-pocket, rolling it over might be the only way to secure reliable transportation.

2. Significant, Unavoidable Life Change

A sudden, major life event, such as a growing family requiring a larger, safer vehicle that your current car cannot accommodate, could necessitate an immediate change. If all other alternatives are exhausted, this might be a last resort.

3. Substantial Down Payment to Offset Negative Equity

If you can make a significant down payment on the new car, large enough to cover most, if not all, of your negative equity, then the impact of rolling over the remaining small balance is minimized. This effectively reduces the "rolled over" portion to a manageable sum.

4. Securing a Significantly Lower Interest Rate

In very specific scenarios, if your credit score has drastically improved, you might qualify for a new car loan with an interest rate substantially lower than your old one. However, the interest savings must be significant enough to outweigh the increased principal from the rolled-over debt.

Based on my experience: These scenarios are exceptions, not the rule. Most people who roll over their loans do so out of convenience or a lack of understanding, not genuine necessity. Always exhaust all other options first.

Alternatives to Rolling Over Your Car Loan

Before you even consider rolling over your old car loan, it’s crucial to explore more financially sound alternatives. These strategies aim to address your negative equity or your need for a new car without burdening you with additional debt.

1. Pay Down Negative Equity First

The ideal solution is to save up and pay the difference between your loan balance and your car’s value before trading it in. This allows you to start your new car loan with a clean slate, or even better, with positive equity from a down payment. This might mean driving your current car for a few more months or a year.

2. Sell Your Old Car Privately

Often, selling your car yourself can fetch a higher price than a dealer’s trade-in offer. This extra money could potentially cover some or all of your negative equity. While it requires more effort, the financial reward can be significant. (You might find our article on helpful here).

3. Refinance Your Current Loan

If your credit score has improved since you first took out your current loan, or if interest rates have dropped, you might be able to refinance your existing car loan. This could lower your monthly payments and reduce the total interest paid, making it easier to pay down the principal and eventually get out of negative equity. (For more details, check out our guide on ).

4. Drive Your Current Car Longer

The simplest solution is often the best. Continue driving your current car until you’ve paid off enough of the loan principal that you are no longer upside down. This allows you to build equity and save for a down payment on your next vehicle.

5. Consider a Less Expensive New Car

If you must get a new car, choose a more affordable model. By minimizing the new loan amount, you reduce the overall impact of any rolled-over negative equity and shorten your path to positive equity.

6. Save for a Down Payment

Regardless of whether you have negative equity, saving a substantial down payment for your next car is always a wise financial move. It reduces the amount you need to finance, lowers your monthly payments, and helps you avoid being upside down early in the loan term.

Pro tips from us: Be patient and prioritize your financial health over immediate gratification. Exploring these alternatives can save you thousands of dollars and prevent long-term debt struggles.

Key Factors to Consider Before You Decide

Making an informed decision about your car loan requires a thorough evaluation of several financial and practical factors. Don’t rush into anything without considering these points.

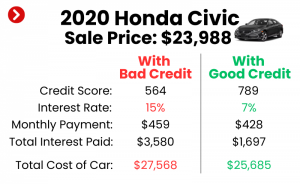

1. Your Credit Score

Your credit score will heavily influence the interest rate you qualify for on a new loan. A lower score means higher interest, which will exacerbate the cost of rolling over negative equity. Understand your score and take steps to improve it if possible.

2. Interest Rates

Even a seemingly small difference in interest rates can translate to thousands of dollars over the life of a loan, especially a larger one with rolled-over debt. Shop around for the best rate from multiple lenders, not just the dealership.

3. New Car’s Depreciation Rate

Some vehicles hold their value better than others. If you must roll over debt, choosing a car known for slower depreciation can help you build equity faster and reduce the time you spend upside down on the new loan.

4. Your Budget and Financial Stability

Can you truly afford the new, larger monthly payment without straining your budget? Consider your overall financial stability, including other debts, savings, and emergency funds. A new car should not jeopardize your financial security.

5. The Trade-in Value of Your Old Car

Research your car’s true market value using resources like Kelley Blue Book (KBB) or Edmunds. Don’t rely solely on the dealer’s initial offer. Knowing your car’s worth empowers you in negotiations and helps you accurately calculate your negative equity.

6. The Total Cost (Not Just Monthly Payment)

Always calculate the total cost of the new loan, including the rolled-over debt, interest, taxes, and fees. A lower monthly payment often comes with a longer loan term and a much higher overall cost. Focus on the total amount you will pay over the life of the loan.

Navigating the Dealership When You’re Upside Down

Dealerships are businesses, and their goal is to make a sale. When you have negative equity, they might present options that seem appealing but aren’t always in your best financial interest. Approach the negotiation process with caution and knowledge.

1. Be Transparent, But Informed

Don’t hide your negative equity, as it will come out eventually. However, go in knowing your exact loan payoff amount and your car’s approximate trade-in value. This prevents the dealer from lowballing your trade or inflating your negative equity.

2. Do Your Homework

Research the new car’s fair market price before you even step foot in the dealership. Tools like TrueCar or Edmunds can provide excellent pricing guides. This allows you to negotiate the car’s price independently of your trade-in.

3. Negotiate Separately

Try to negotiate the price of the new car, the value of your trade-in, and the financing terms as separate transactions. Combining them allows dealers to "shuffle" numbers, giving you a good deal on one aspect while overcharging on another.

4. Avoid the "Payment Shuffle"

Dealerships often try to focus the conversation on monthly payments. While important, it’s a tactic to distract from the total loan amount and interest. Stick to negotiating the total price of the car and the amount you’re financing.

5. Read the Fine Print

Before signing anything, meticulously review the entire contract. Ensure that the new car price, trade-in value, negative equity amount, interest rate, and loan term match what was discussed and agreed upon. Look out for hidden fees or unnecessary add-ons.

Impact on Your Credit Score

Any significant financial transaction, especially taking on new debt, can affect your credit score. Rolling over a car loan has several potential impacts:

1. Hard Inquiry

Applying for a new car loan results in a "hard inquiry" on your credit report, which can temporarily ding your score by a few points. Multiple applications within a short period can have a cumulative effect.

2. Increased Debt-to-Income Ratio

A larger new car loan means you’re taking on more debt relative to your income. Lenders use the debt-to-income (DTI) ratio to assess your ability to manage debt, and a higher DTI can make it harder to secure other loans in the future.

3. Potential for Late Payments

If the new, larger loan results in a monthly payment that stretches your budget too thin, you increase your risk of missing payments. Late payments are highly detrimental to your credit score and can have long-lasting negative effects.

4. Loan-to-Value (LTV) Ratio

Starting a new loan with a high LTV (because of negative equity) means you owe significantly more than the car is worth. While not directly a credit score factor, it can be viewed as a risk by future lenders.

Common mistakes to avoid are: Not understanding how a larger debt burden can impact your future borrowing capacity and credit health. Always assess the long-term credit implications before committing to a new loan.

Pro Tips for Minimizing the Damage (If You Must Roll Over)

If, after considering all alternatives, you determine that rolling over your old car loan is your only viable option, there are steps you can take to mitigate the financial damage. These tips are crucial for preventing an even deeper debt trap.

1. Make the Largest Down Payment Possible

This is the single most effective way to reduce the impact of rolled-over negative equity. Any amount you can put down will directly reduce the principal of your new loan, helping you get to positive equity faster. Even a few hundred dollars can make a difference.

2. Choose a New Car That Holds Its Value Well

Research vehicles with a strong resale value and low depreciation rates. While you’re starting upside down, selecting a car that depreciates slowly will help you close the gap between what you owe and what the car is worth more quickly.

3. Opt for the Shortest Loan Term You Can Comfortably Afford

Resist the urge to extend the loan term just to lower your monthly payment. A shorter term means less interest paid overall and a faster path to ownership. While the monthly payment might be higher, the total cost will be significantly less.

4. Seek the Absolute Best Interest Rate

Shop around aggressively for the lowest possible interest rate. Get pre-approved by banks, credit unions, and online lenders before going to the dealership. A lower rate on a larger loan can save you thousands.

5. Consider GAP Insurance (But Understand Its Limitations)

Guaranteed Asset Protection (GAP) insurance covers the difference between what you owe on your car loan and its actual cash value if the car is totaled or stolen. If you’re starting with negative equity, you’ll be upside down for a long time, making GAP insurance a wise, though temporary, consideration. However, understand it’s a one-time payout for a total loss, not a solution to your ongoing negative equity.

Based on my experience: These steps are non-negotiable if you find yourself in a position where rolling over debt is necessary. They are your best defense against spiraling into deeper financial trouble.

Conclusion: Make Informed Decisions About Your Car Loan

Rolling an old car loan into a new one is a financial maneuver that should generally be approached with extreme caution and, ideally, avoided. While it offers a seemingly easy path to a new vehicle, it often leads to a cycle of increased debt, higher interest payments, and prolonged financial burden. The allure of a new car should never overshadow the importance of sound financial planning.

Always remember that the goal is not just to acquire a new car, but to do so in a way that strengthens, rather than weakens, your financial position. Thoroughly understand your negative equity, explore all alternatives, and if you absolutely must proceed, take every possible step to minimize the financial damage. Your future self will thank you for making an informed, responsible decision.

By prioritizing financial literacy and making strategic choices, you can navigate the complexities of car financing and achieve your automotive goals without falling into a debt trap. Drive wisely, and your wallet will follow.

Internal Links:

External Link:

- For a deeper dive into understanding negative equity, you can refer to resources like Investopedia’s explanation of Negative Equity.