Safeguarding Your Legacy: The Ultimate Guide to Car Loan Death Insurance

Safeguarding Your Legacy: The Ultimate Guide to Car Loan Death Insurance Carloan.Guidemechanic.com

The joy of driving a new car is undeniable, a symbol of freedom and convenience. Yet, in life’s unpredictable journey, we often overlook crucial financial safeguards that protect our loved ones from unforeseen burdens. One such safeguard, often misunderstood or entirely unknown, is Car Loan Death Insurance.

Imagine a scenario: you’ve just financed your dream car, making regular payments. Then, an unexpected tragedy strikes, and you’re no longer here. What happens to that car loan? Does your family inherit the debt along with their grief? This is precisely where car loan death insurance steps in, offering a vital safety net.

Safeguarding Your Legacy: The Ultimate Guide to Car Loan Death Insurance

This comprehensive guide will demystify car loan death insurance, exploring its purpose, how it works, its benefits, potential drawbacks, and whether it’s the right choice for your financial plan. Our goal is to equip you with the knowledge to make an informed decision, ensuring peace of mind for you and your loved ones.

Understanding Car Loan Death Insurance: What Exactly Is It?

At its core, car loan death insurance is a specialized form of insurance designed to cover the outstanding balance of your vehicle loan in the event of your passing. It’s often referred to as "credit life insurance" when associated with a loan. Unlike traditional life insurance, which pays a lump sum to your beneficiaries, car loan death insurance typically pays the lender directly.

The primary purpose of this insurance is to prevent your outstanding car loan debt from becoming a financial burden on your estate or your co-signer. It ensures that your family won’t have to choose between selling the car, taking on the payments themselves, or facing potential credit score damage. It’s a targeted solution for a specific debt.

Think of it as a protective shield around your car loan. Should the unthinkable happen, this shield activates, settling the debt and allowing your family to retain ownership of the vehicle without the financial stress. This protection can be incredibly valuable during an already difficult emotional time.

Why Consider Car Loan Death Insurance? The Real Stakes

The decision to take on a car loan is a significant financial commitment. While we all hope to see our loans through to completion, life has a way of throwing curveballs. Understanding the potential ramifications of an unpaid car loan after death highlights the importance of this specific coverage.

Based on my experience, many people overlook the potential financial ripple effects that an outstanding car loan can cause after a borrower’s death. It’s not just about the car itself; it’s about protecting your entire financial legacy.

Protecting Your Co-Signer or Joint Owner

If you have a co-signer on your car loan, they become 100% responsible for the remaining debt if you pass away. This can be a devastating blow, forcing them to make payments they hadn’t anticipated or, worse, damaging their credit score if they can’t. Car loan death insurance directly mitigates this risk.

For joint owners, the situation is similar. While they might still have access to the vehicle, they would also inherit the full financial obligation. This insurance ensures they won’t face the double tragedy of losing a loved one and then struggling to pay for a car they might not be able to afford alone.

Safeguarding Your Estate and Beneficiaries

Without car loan death insurance, the outstanding debt becomes a liability of your estate. This means that funds or assets intended for your beneficiaries might need to be used to pay off the car loan, reducing the inheritance they receive. In some cases, the estate might even be forced to sell the vehicle.

By settling the car loan, this insurance preserves your estate for your loved ones. It ensures that your other assets and any life insurance payouts can be distributed as you intended, without being siphoned off to cover vehicle debt. This offers significant peace of mind.

Preventing Repossession and Credit Score Damage

If your family or estate cannot keep up with car loan payments, the vehicle could be repossessed. This process is not only emotionally painful but can also negatively impact the credit scores of any co-signers or even the deceased’s estate, depending on the circumstances.

Car loan death insurance prevents this scenario entirely. The prompt payment of the loan by the insurer means the car remains with your family, free and clear, without any risk of repossession or detrimental credit reporting. It’s a clean and clear resolution to a complex problem.

How Does Car Loan Death Insurance Actually Work? A Step-by-Step Guide

The mechanism behind car loan death insurance is relatively straightforward, designed for efficiency during a difficult period. Understanding this process can help you appreciate its value.

Application and Premium Payments

When you apply for a car loan, your lender or dealership might offer car loan death insurance as an add-on. You’ll typically fill out an application, which may include some basic health questions, though often the underwriting is less stringent than for traditional life insurance.

The premiums for this insurance can be structured in a couple of ways. Sometimes, a single premium is calculated for the entire loan term and rolled directly into your total loan amount. More commonly, you might pay monthly premiums that are either added to your car payment or billed separately.

The Claim Process Upon Death

Should the insured borrower pass away, a beneficiary (often the surviving family member or executor of the estate) or the lender would initiate a claim with the insurance provider. This typically involves submitting a death certificate and proof of the outstanding loan balance.

The insurance company then reviews the claim to ensure all policy conditions are met. This is usually a swift process, especially for clear-cut cases, as the purpose is to quickly settle the debt.

Payout Mechanism

Upon approval, the insurance company does not pay a lump sum to your family. Instead, it pays the remaining balance of the car loan directly to the lender. This ensures that the specific debt is extinguished, aligning with the policy’s design.

Once the lender receives the payment, the car loan is considered paid in full. This frees your family from the financial obligation and allows them to retain ownership of the vehicle without any further payments. It’s a seamless transition designed to alleviate financial stress.

Types of Car Loan Death Insurance (and What to Look For)

While the core concept remains consistent, car loan death insurance can manifest in slightly different forms, each with its own nuances. Understanding these variations is key to choosing the right coverage.

Credit Life Insurance

This is the most common form of car loan death insurance. Credit life insurance is designed specifically to pay off a particular debt if the borrower dies. The coverage amount typically decreases as you pay down your loan, matching the outstanding balance. This ensures you’re only paying for the coverage you need.

It’s often offered directly by lenders or through dealerships as part of the financing package. While convenient, it’s crucial to evaluate its terms and cost carefully, as sometimes these bundled options can be more expensive than standalone alternatives.

Specific Car Loan Protection Plans

Some dealerships or financial institutions might offer their own branded "loan protection plans" that function similarly to credit life insurance. These plans are tailored to their specific loan products and may include additional benefits, such as disability coverage, which pays your car payments if you become unable to work due.

Always scrutinize the details of these plans. Ensure you understand what specific events trigger a payout, what the exclusions are, and how the premium is calculated. Don’t assume all "protection plans" are identical in their offerings.

Key Features to Compare

When considering any form of car loan death insurance, several features warrant close attention:

- Coverage Amount: Does it cover the full outstanding loan balance, or is there a cap? Most credit life policies match the declining balance.

- Term of Coverage: Does the policy cover the entire loan term, or is it for a shorter period? Ideally, it should match your loan duration.

- Exclusions: What circumstances would prevent a payout? Common exclusions might include suicide within a certain period, or deaths related to pre-existing conditions not disclosed during application.

- Premium Structure: Is it a single upfront premium, or monthly payments? Understand how this impacts your overall loan cost.

Is Car Loan Death Insurance Worth the Investment? Weighing the Pros and Cons

Deciding whether to purchase car loan death insurance involves a careful evaluation of its benefits against its costs and your existing financial situation. There are compelling reasons to consider it, as well as scenarios where it might not be the most efficient use of your funds.

The Pros: Peace of Mind and Financial Protection

- Ultimate Peace of Mind: Knowing that your family won’t inherit a car loan debt during their time of grief is invaluable. This peace of mind extends to you, allowing you to focus on enjoying your vehicle.

- Financial Protection for Loved Ones: It directly protects your co-signer, joint owner, or beneficiaries from having to take on the financial burden of the car loan. This is especially crucial for those who might struggle with the additional payments.

- Avoids Estate Complications: By settling the debt, it simplifies your estate settlement process, ensuring your other assets are distributed as intended without being used to cover vehicle debt.

- Prevents Repossession: Your family gets to keep the car, which might be essential for their daily transportation, without the risk of it being taken back by the lender.

The Cons: Cost and Potential Overlap

- Additional Cost: Like any insurance, it comes with a premium. This adds to the overall cost of your car loan, and sometimes these premiums can be higher than alternative forms of coverage.

- Limited Scope: Car loan death insurance only covers the specific car loan. It doesn’t provide broader financial protection for other debts or living expenses, unlike a general life insurance policy.

- Potential Overlap with Existing Life Insurance: If you have a robust term life insurance policy with sufficient coverage, your beneficiaries might already be able to pay off the car loan using those funds. In such cases, car loan death insurance might be redundant.

- Exclusions and Limitations: Policies can have specific exclusions, such as pre-existing conditions or certain types of death, which could prevent a payout. Pro tips from us: Always scrutinize the fine print and ask for a complete list of exclusions before committing.

Ultimately, the "worth" of car loan death insurance depends on your individual circumstances, including your financial health, existing insurance coverage, and the potential impact on your loved ones.

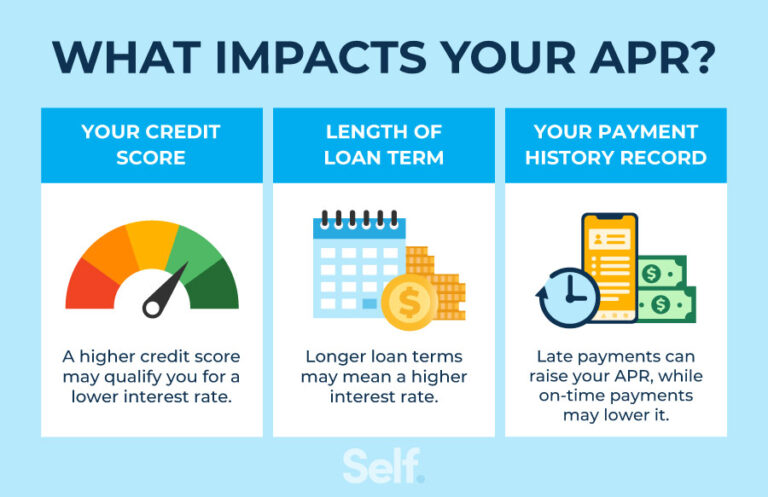

The Cost Factor: How Much Does Car Loan Death Insurance Typically Cost?

The cost of car loan death insurance isn’t uniform; it varies based on several factors. Understanding these elements will help you gauge whether the premium you’re quoted is reasonable.

Factors Influencing Cost

- Loan Amount and Term: Generally, the larger your loan amount and the longer your loan term, the higher the overall cost of the insurance. The coverage is tied directly to the debt.

- Borrower’s Age and Health: While less intensive than traditional life insurance, some credit life policies may consider your age and health status. Older individuals or those with certain health conditions might face higher premiums.

- Insurer and Lender: Different insurance providers and lenders will have varying pricing structures. Shopping around and comparing quotes is always advisable.

- Premium Structure: As mentioned, whether it’s a single premium rolled into the loan or monthly payments will affect how you perceive and pay for the cost. A single premium often means you’re paying interest on the insurance itself over the loan’s life.

Tips for Comparing Quotes

When evaluating quotes for car loan death insurance, ask for a clear breakdown of the total cost. Don’t just look at the monthly payment; understand the total premium over the life of the loan. Compare this figure against the peace of mind it offers and alternative solutions.

It’s also wise to inquire about the cancellation policy. Can you cancel the insurance at any time, and if so, is there a refund for any unearned premium? This can be important if your financial situation changes or you decide to refinance.

Common Mistakes to Avoid When Considering Car Loan Death Insurance

Navigating the world of insurance can be tricky, and car loan death insurance is no exception. Being aware of common pitfalls can save you money and ensure you get the right coverage.

Common mistakes to avoid are rushing into a decision without fully understanding the product or assuming it’s a "one-size-fits-all" solution.

Assuming Existing Life Insurance Covers It Sufficiently

Many people mistakenly believe that their existing term or whole life insurance policy automatically negates the need for car loan death insurance. While a general life insurance policy can provide funds to pay off a car loan, it’s crucial to assess if the coverage is truly sufficient.

If your life insurance payout is primarily intended for income replacement, education funds, or other major debts, allocating a portion to a car loan might stretch its limits. Car loan death insurance offers dedicated, targeted protection for this specific debt, ensuring it doesn’t compete with other critical financial needs.

Not Reading the Policy Thoroughly

The fine print matters. It outlines exactly what is covered, what isn’t, and under what conditions a payout will be made. Not reading the policy thoroughly means you might be unaware of exclusions, limitations, or the precise claims process.

Take the time to understand terms like "pre-existing conditions clause," "suicide clause," and the definitions of "total and permanent disability" if disability coverage is included. A clear understanding prevents unpleasant surprises later.

Buying Without Comparing Options

It’s easy to accept the insurance offered by your car dealership or lender out of convenience. However, this might not always be the most cost-effective or comprehensive option. Different providers may offer similar coverage at varying price points or with slightly different terms.

Always ask for a separate quote for the car loan death insurance and compare it with alternatives, including potentially increasing your general life insurance coverage. Don’t be pressured into an immediate decision.

Not Understanding Exclusions

Every insurance policy has exclusions – specific circumstances under which the policy will not pay out. Forgetting to clarify these can lead to significant disappointment. For instance, some policies might exclude deaths related to specific high-risk activities or if the death occurs within a very short period after policy inception due to a pre-existing, undisclosed condition.

Always ask for a clear list of exclusions and ensure you understand them before signing any agreement.

Alternatives to Car Loan Death Insurance

While car loan death insurance offers targeted protection, it’s not the only way to safeguard your family from car loan debt. Exploring alternatives can help you determine the most appropriate strategy for your financial situation.

Term Life Insurance: A Broader Safety Net

A well-structured term life insurance policy can often serve as a more flexible and, in many cases, more cost-effective alternative. Term life insurance provides a lump sum payout to your beneficiaries if you die within a specified term.

Your beneficiaries can then use these funds to cover various expenses, including paying off the car loan, other debts, mortgage payments, living expenses, and education costs. It offers broader protection and is often more affordable per dollar of coverage compared to credit life insurance. (Hypothetical internal link)

Savings and Emergency Fund: Self-Insurance

Building a robust emergency fund or maintaining sufficient savings can act as a form of "self-insurance." If you pass away, these funds could be accessed by your estate or family to pay off the car loan.

This approach requires discipline and sufficient liquid assets. While it offers complete control, it may not be feasible for everyone, especially those just starting their financial journey or managing other significant debts.

Will and Estate Planning: Designating Assets

Proper estate planning, including a clear will, can designate specific assets or funds to cover outstanding debts like a car loan. You can instruct your executor to use a portion of your estate or proceeds from a specific account to settle the debt.

This method requires careful planning and ensuring your estate has sufficient liquid assets. It’s a crucial step for comprehensive financial planning, regardless of your car loan situation.

Joint Ownership and Co-signer Considerations

If you have a co-signer or joint owner, understand that they are fully responsible for the loan. While this means the debt won’t fall solely on your estate, it places a direct burden on another individual. Discussing these contingencies with them and considering their financial capacity is essential.

Sometimes, the best "alternative" is to ensure your co-signer is fully aware of their responsibilities and that they have the means or their own insurance to cover the debt if needed.

Making an Informed Decision: What to Ask Your Lender and Insurer

Choosing the right path for car loan death insurance requires diligence and asking the right questions. Don’s hesitate to seek clarification from both your lender and the insurance provider.

Here’s a checklist of questions to guide your conversations:

- What exactly does this policy cover? Get a clear understanding of the specific events that trigger a payout (e.g., natural death, accidental death, terminal illness).

- What are the exclusions? Ask for a detailed list of circumstances where the policy would not pay out. This is critical.

- How are the premiums calculated, and what is the total cost over the loan term? Understand if it’s a single premium rolled into the loan or monthly payments, and the total financial commitment.

- Does the coverage amount decline with my loan balance? Most credit life policies do, which is generally a fair structure.

- What is the claims process, and what documentation is required? Knowing this beforehand can simplify a difficult situation for your family.

- Can I cancel the policy, and if so, is there a refund for unearned premiums? This provides flexibility if your circumstances change.

- How does this policy compare to a standard term life insurance policy in terms of cost and coverage? This question helps you compare apples to apples.

- Is this policy transferable if I refinance my car loan? Some policies might not be, requiring you to purchase new coverage.

Pro Tip: Don’t be afraid to take notes during these conversations and request all information in writing. A clear paper trail is always beneficial.

Real-Life Scenarios: When Car Loan Death Insurance Shines (and When it Might Not)

To truly grasp the utility of car loan death insurance, let’s consider a few real-world examples. These scenarios highlight when this specific coverage can be a game-changer and when other solutions might be more fitting.

Scenario 1: The Single Parent with Young Children

Maria, a single mother, finances a reliable minivan for her two young children. Her budget is tight, and while she has a small term life insurance policy, it’s primarily earmarked for her children’s education and basic living expenses. She has no co-signer.

Here, car loan death insurance shines. If Maria were to pass away, her small life insurance policy would be stretched thin. The car loan death insurance would ensure the minivan, essential for her children’s transportation, is paid off immediately. This removes a significant financial burden from her estate and allows her children to keep the vehicle without any added stress.

Scenario 2: The Elderly Individual with a Co-signer

Robert, 70, co-signs a car loan for his adult daughter, Sarah, who has a modest income. Robert has a substantial life insurance policy, but Sarah’s financial situation is less robust.

Car loan death insurance could be highly beneficial here, especially if Robert is the primary borrower. If Robert were to pass away, Sarah would become solely responsible for the loan. While Robert’s life insurance could cover it, the car loan death insurance guarantees that specific debt is cleared, protecting Sarah from financial strain and ensuring she doesn’t face an unexpected bill during a time of mourning.

Scenario 3: The Young, Healthy Professional with Substantial Life Insurance

David, 30, is a healthy professional with a high-paying job. He has a robust term life insurance policy that far exceeds his total debts, including his car loan. His policy is designed to cover his mortgage, all outstanding debts, and provide significant income replacement for his spouse.

In this case, car loan death insurance might be redundant. David’s existing life insurance policy provides ample coverage to pay off the car loan and much more. The additional cost of car loan death insurance would likely be an unnecessary expense, as his beneficiaries could easily use a portion of his general life insurance payout to clear the vehicle debt. (Hypothetical internal link)

Conclusion: Driving Towards Financial Security

Car loan death insurance is more than just another add-on; it’s a thoughtful layer of financial protection designed to safeguard your loved ones from an unexpected burden. It ensures that the excitement of a new vehicle doesn’t turn into a financial headache for your family should the unthinkable occur.

By understanding what it is, how it works, and its potential benefits and drawbacks, you can make an informed decision that aligns with your personal circumstances and financial goals. Whether you opt for this specific coverage or choose to bolster your general life insurance, the key is proactive planning.

Don’t leave your family vulnerable to the complexities of outstanding debt. Take the time to evaluate your options, ask thorough questions, and secure the peace of mind that comes with knowing your legacy is protected. For more comprehensive financial planning advice, consider consulting a reputable financial advisor or exploring resources like the Consumer Financial Protection Bureau to understand your rights and options.

Drive confidently, knowing you’ve taken steps to protect your future and the financial well-being of those you care about most.