Securing a $20,000 Car Loan for 5 Years: Your Expert Guide to Smart Financing

Securing a $20,000 Car Loan for 5 Years: Your Expert Guide to Smart Financing Carloan.Guidemechanic.com

Are you dreaming of a new set of wheels but need to finance a significant portion of the cost? A $20,000 car loan spread over five years is a very common and manageable option for many buyers. However, navigating the world of auto loans can feel like a complex journey. From understanding interest rates to improving your credit score, there’s a lot to consider.

As an expert blogger and professional SEO content writer, my mission is to demystify this process for you. This comprehensive guide will equip you with all the knowledge you need to secure a $20,000 car loan for 5 years with confidence, ensuring you get the best possible terms and avoid common pitfalls. We’ll delve deep into every aspect, providing actionable advice that offers real value.

Securing a $20,000 Car Loan for 5 Years: Your Expert Guide to Smart Financing

Understanding the $20,000 Car Loan Over a 5-Year Term

When you take out a $20,000 car loan for 60 months (5 years), you’re essentially borrowing a principal amount that you’ll repay, plus interest, over that specified period. This loan term is incredibly popular because it often strikes a good balance between manageable monthly payments and a reasonable total cost of interest.

Let’s break down what this means for your finances. The principal is the $20,000 you’re borrowing. The interest is the cost of borrowing that money, expressed as an Annual Percentage Rate (APR). Over five years, these two components combine to form your total repayment.

What Your Monthly Payments Might Look Like

The exact monthly payment for a $20,000 car loan over 5 years depends heavily on the interest rate you secure. Even a small difference in APR can significantly impact your budget. Based on my experience, here’s a general idea of what you might expect:

- At 4% APR: Your monthly payment would be approximately $368.

- At 6% APR: Your monthly payment would be around $387.

- At 8% APR: Your monthly payment would be about $406.

- At 10% APR: Your monthly payment would be closer to $425.

These figures are illustrative and don’t include potential fees or taxes, but they highlight the importance of securing a low interest rate. Over 60 months, that difference can add up to hundreds or even thousands of dollars in total interest paid.

The Pros and Cons of a 5-Year Term

Choosing a 5-year loan term has distinct advantages and disadvantages that you should weigh carefully before committing. It’s crucial to assess if this duration aligns with your financial goals and your driving habits.

Pros of a 5-Year Car Loan:

- Manageable Monthly Payments: Compared to shorter terms (e.g., 3 years), a 5-year loan significantly lowers your monthly financial burden. This can free up cash flow for other expenses or savings.

- Accessibility for Higher-Priced Vehicles: A longer term makes financing a $20,000 vehicle more accessible by keeping payments affordable, especially for those with moderate budgets.

- Potential for Lower Interest Rates (Historically): While not always the case, shorter terms sometimes carry slightly higher rates, making 5-year loans competitive.

Cons of a 5-Year Car Loan:

- Higher Total Interest Paid: The longer you borrow money, the more interest accrues over the life of the loan. While monthly payments are lower, the overall cost of the car will be higher than with a shorter loan.

- Increased Risk of Negative Equity: Cars depreciate rapidly, especially in the first few years. With a 5-year loan, you might owe more on the car than it’s worth for a longer period, making it harder to sell or trade in without financial loss.

- Extended Debt Obligation: You’ll be making payments for five full years, which can feel like a long time. This commitment ties up a portion of your income for an extended period.

Understanding these trade-offs is the first step towards making an informed decision. For many, the lower monthly payments of a 5-year term outweigh the higher total interest, especially if it means driving a safer, more reliable vehicle.

Key Factors Influencing Your Loan Approval & Rate

Securing a $20,000 car loan for 5 years isn’t just about finding a lender; it’s about presenting yourself as a reliable borrower. Several critical factors will determine not only if your loan is approved but also the interest rate you’ll be offered. Lenders assess risk, and these elements are their primary indicators.

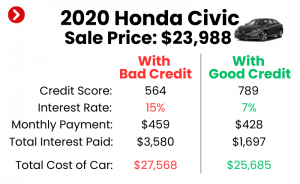

1. Your Credit Score: The Ultimate Determinant

Your credit score is arguably the most influential factor in securing any loan, and a car loan is no exception. This three-digit number, typically ranging from 300 to 850, reflects your creditworthiness based on your payment history, amounts owed, length of credit history, new credit, and credit mix.

- Excellent Credit (780-850): Borrowers in this tier are considered low-risk and will typically qualify for the lowest interest rates available. Lenders are eager to approve these applications.

- Good Credit (670-779): Most consumers fall into this category. You’ll likely get competitive rates, though perhaps not the absolute lowest. Approval is generally straightforward.

- Fair Credit (580-669): You might still be approved, but expect higher interest rates to compensate lenders for the increased risk. Options might be more limited.

- Poor Credit (300-579): Securing a $20,000 loan can be challenging with poor credit. If approved, the interest rates will be significantly higher, making the loan much more expensive.

Before even looking at cars, pull your credit report from all three major bureaus (Experian, Equifax, TransUnion) and check your scores. This gives you a clear picture of where you stand and allows you to dispute any errors.

2. Income and Employment Stability

Lenders want to be confident that you have the consistent financial capacity to repay the loan. Your income and employment history play a crucial role in this assessment. They will look for:

- Sufficient Income: Your gross monthly income needs to be high enough to comfortably cover the car payment, along with your other existing debts and living expenses.

- Stable Employment: A history of steady employment, ideally with the same employer for at least a year or two, indicates reliability. Frequent job changes can be a red flag.

- Verifiable Income: Be prepared to provide pay stubs, W-2s, or tax returns to verify your income. Self-employed individuals may need more extensive documentation.

Pro tips from us: Even if you have a great credit score, a lender might deny your application if they believe your income isn’t sufficient to handle the additional debt. Always be realistic about what you can truly afford.

3. Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. It’s a critical metric for lenders as it shows how much of your income is already committed to debt.

- Calculation: (Total Monthly Debt Payments / Gross Monthly Income) x 100.

- Ideal DTI: Most lenders prefer a DTI ratio of 36% or lower, though some may go up to 43% or even 50% for car loans, especially if you have excellent credit.

A high DTI ratio indicates that you might be stretched thin financially, making it riskier for a lender to approve another significant debt like a $20,000 car loan. Reducing existing debt before applying can significantly improve your chances.

4. Down Payment: Your Financial Cushion

Making a down payment on a car loan is one of the smartest financial moves you can make. It demonstrates your commitment to the purchase and immediately reduces the amount you need to borrow.

- Reduced Principal: A larger down payment means you borrow less, which translates to lower monthly payments and less interest paid over the life of the loan.

- Improved Loan-to-Value (LTV): Lenders look at the Loan-to-Value (LTV) ratio, which compares the loan amount to the car’s actual value. A lower LTV (meaning you’ve borrowed less relative to the car’s value) makes you a less risky borrower.

- Offsetting Depreciation: A down payment helps to counteract the rapid depreciation of a new car, reducing the risk of being "upside down" (owing more than the car is worth).

- Better Rates: Lenders are often willing to offer more favorable interest rates to borrowers who make a substantial down payment. Aim for at least 10-20% if possible.

5. Loan-to-Value (LTV) Ratio

The LTV ratio is a measure that lenders use to assess the risk of a loan. It compares the amount of the loan to the market value of the vehicle you are purchasing.

- How it works: If you’re borrowing $20,000 for a car valued at $22,000, your LTV is approximately 91% ($20,000 / $22,000). If you make a $2,000 down payment, borrowing $18,000 for the same car, your LTV drops to about 81% ($18,000 / $22,000).

- Lender Preference: Lenders prefer lower LTVs because it means they have more collateral should you default on the loan. A very high LTV, especially over 100% (which can happen if you roll negative equity from a trade-in into the new loan), signals higher risk and can lead to higher interest rates or even denial.

6. Vehicle Age and Type

The characteristics of the vehicle itself can also influence your loan approval and rate. Lenders consider the car as collateral for the loan.

- Newer vs. Older Cars: Newer cars typically get better loan terms because they are more reliable, hold their value better initially, and are less likely to require expensive repairs that could strain your budget.

- Vehicle Reliability: Lenders are more comfortable financing vehicles with a reputation for reliability and good resale value, as this reduces their risk if they have to repossess and sell the car.

- Mileage: High mileage on a used car can also be a factor, as it suggests more wear and tear and a shorter remaining lifespan for the vehicle.

Common mistakes to avoid are falling in love with a car before understanding how its characteristics might impact your financing options. Always research the car’s market value and reliability before applying for a loan.

The Application Process: A Step-by-Step Guide

Once you understand the factors that influence your loan, the next step is to navigate the application process itself. Being prepared and methodical can save you time, stress, and money.

1. Preparation is Key: Gather Your Documents

Before you even fill out an application, get your financial ducks in a row. This proactive approach shows lenders you are serious and organized.

- Check Your Credit Report: As mentioned, this is paramount. Use AnnualCreditReport.com for free reports. Review them for accuracy and dispute any errors.

- Gather Proof of Income: Recent pay stubs (last 2-3 months), W-2 forms (last 2 years), or tax returns (if self-employed).

- Proof of Residency: Utility bills, lease agreements, or mortgage statements.

- Identification: Driver’s license or state ID.

- Insurance Information: While not always required at the initial application, you’ll need proof of insurance before driving off with the car.

- Trade-in Information (if applicable): Title, registration, and any loan payoff amount.

Having these documents ready will streamline the application process and prevent delays.

2. Shop Around for Lenders: Don’t Settle for the First Offer

This is one of the most crucial steps. Many people make the mistake of only applying for financing at the dealership. While convenient, this often means missing out on better rates.

- Banks: Traditional banks are a reliable source for auto loans. Check with your current bank first, as they might offer loyalty discounts.

- Credit Unions: Often known for offering highly competitive interest rates and personalized service, especially to their members.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, and others offer quick online applications and competitive rates. They provide convenience and often a broad range of options.

- Dealerships: While they can offer convenience, be aware that their financing might include markups. It’s best to have an external pre-approval in hand before discussing dealership financing.

Pro tips from us: Apply for pre-approval with 2-3 different lenders within a short window (typically 14-45 days, depending on the credit scoring model). Multiple inquiries for the same type of loan within this timeframe are usually counted as a single hard inquiry on your credit report, minimizing the impact.

3. Pre-Approval: Understanding Its Benefits

Pre-approval is a conditional offer from a lender that states how much they are willing to lend you, at what interest rate, and for what term, based on a preliminary review of your credit and income.

- Set Your Budget: Pre-approval tells you exactly how much you can afford, empowering you to shop for cars within your budget. For a $20,000 car loan, this confirms your borrowing power.

- Negotiating Power: Walking into a dealership with a pre-approval letter is like having cash in hand. It allows you to negotiate the car’s price separately from the financing, often leading to a better deal.

- Faster Purchase: Once you find the right car, the actual financing process will be much quicker, as much of the paperwork has already been handled.

A common mistake to avoid is skipping pre-approval. It puts you at a significant disadvantage during negotiations and can lead to impulsive decisions.

4. The Formal Application: What to Expect

Once you’ve found your car and chosen your preferred lender (whether it’s your pre-approved lender or a better offer from the dealership), you’ll complete the formal application.

- Detailed Information: You’ll provide more specific information about the vehicle (VIN, mileage, year, make, model) and likely re-verify your income and identity.

- Review and Sign: Carefully read all loan documents. Pay close attention to the APR, the total amount financed, the total interest paid, and any fees.

- Contingencies: Sometimes, pre-approvals have contingencies, such as the vehicle needing to meet certain criteria (e.g., age, mileage limits). Ensure your chosen car fits these.

5. Understanding the Loan Offer: APR, Fees, and Terms

Don’t just look at the monthly payment. Dive into the details of the loan offer.

- Annual Percentage Rate (APR): This is the true cost of borrowing, including interest and certain fees. It’s the best measure to compare different loan offers.

- Loan Term: Confirm it’s the 60-month (5-year) term you’re seeking. Be wary of lenders trying to extend the term to lower monthly payments, as this increases total interest.

- Fees: Look for origination fees, documentation fees, or prepayment penalties. Ideally, a good car loan should have minimal to no fees.

- Total Cost of the Loan: This is the sum of the principal borrowed plus all the interest you’ll pay over the 5 years. This figure truly reveals the overall expense.

Based on my experience, many borrowers overlook the total cost of the loan, focusing solely on the monthly payment. This can lead to paying significantly more than necessary.

Strategies to Secure the Best Deal

Getting approved for a $20,000 car loan for 5 years is one thing; getting the best deal is another. Here are proven strategies to put you in the driver’s seat.

1. Boost Your Credit Score Before You Apply

Since your credit score is so pivotal, taking steps to improve it before applying can save you thousands in interest.

- Pay Bills on Time: This is the single most important factor. Set up automatic payments to avoid missing due dates.

- Reduce Existing Debt: Lowering your credit card balances, especially, can improve your credit utilization ratio (amounts owed vs. available credit), which positively impacts your score.

- Avoid New Credit Applications: Don’t open new credit cards or take out other loans just before applying for a car loan, as this can temporarily lower your score.

- Check for Errors: Regularly review your credit reports for inaccuracies that could be dragging down your score.

Even a 20-30 point increase in your score can move you into a better rate tier, making it worth the effort.

2. Save for a Larger Down Payment

As discussed, a significant down payment is your best friend when it comes to car financing.

- Aim for 10-20%: For a $20,000 car, a $2,000-$4,000 down payment can make a huge difference in your loan terms and total cost.

- Reduce Risk for Lender: A larger down payment signals financial stability and reduces the lender’s risk, often resulting in a lower interest rate.

- Combat Depreciation: It provides a buffer against the car’s initial depreciation, helping you avoid negative equity.

Every dollar you put down is a dollar you don’t have to borrow and pay interest on.

3. Negotiate the Car Price Separately from the Loan

This is a pro tip that many car buyers miss. Treat the car purchase as one transaction and the financing as another.

- Focus on the Out-the-Door Price: Before discussing financing, negotiate the lowest possible selling price for the vehicle. This is easier if you have external pre-approval.

- Avoid "Payment Shopping": Don’t tell the dealer what monthly payment you want. They might achieve that by extending the loan term or increasing the interest rate, costing you more in the long run.

- Be Prepared to Walk Away: Having done your research and secured pre-approval gives you powerful leverage. If the deal isn’t right, don’t be afraid to leave.

4. Consider a Co-signer (If Necessary)

If your credit score is fair or poor, or if you have limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a better interest rate.

- Shared Responsibility: A co-signer agrees to be legally responsible for the loan if you fail to make payments. This reduces the lender’s risk.

- Impact on Co-signer’s Credit: Be aware that the loan will appear on both your and your co-signer’s credit reports. Missed payments will negatively affect both.

- Choose Wisely: Only consider a co-signer who fully understands the responsibility and whom you trust implicitly. It’s a significant favor.

5. Avoid Dealership Financing Pitfalls

While convenient, dealership financing can sometimes lead to less favorable terms if you’re not careful.

- The "Four-Square" Method: Dealers sometimes use this sales tactic to juggle price, trade-in value, down payment, and monthly payment, making it hard to see the true deal. Focus on one variable at a time.

- Add-ons and Extras: Be wary of high-pressure sales for extended warranties, paint protection, or other add-ons. These significantly inflate the loan amount and often aren’t worth the cost.

- "Spot Delivery" Scams: Never drive a car off the lot with a "conditional" approval. Ensure all financing is finalized before taking possession of the vehicle.

Always compare the dealership’s financing offer to your pre-approval from independent lenders. If the dealership can beat it, great! If not, stick with your external financing.

Managing Your $20,000 Car Loan Responsibly

Getting the loan is just the beginning. Responsible management over the next five years is crucial to avoid financial stress and build a positive credit history.

1. Budgeting for Monthly Payments

Integrate your car loan payment into your monthly budget from day one. This means understanding exactly how it fits into your income and expenses.

- Create a Detailed Budget: Track all your income and outflows. Ensure the car payment doesn’t strain your budget or force you to cut back on essential needs or savings.

- Automate Payments: Set up automatic payments from your checking account to avoid missing due dates. This protects your credit score and prevents late fees.

- Factor in Other Car Costs: Remember that a car loan is only one part of car ownership. Budget for insurance, fuel, maintenance, and potential repairs.

2. Understanding Amortization

Amortization refers to how your loan payments are applied over time, gradually paying down both the principal and interest.

- Interest-Heavy at First: In the early months of a 5-year loan, a larger portion of your payment goes towards interest. As the loan matures, more of each payment goes towards reducing the principal balance.

- Online Calculators: Use online auto loan amortization calculators

to see how your payments break down over the 60 months. This visualization can be very motivating.

Knowing this helps you understand the impact of extra payments.

3. Early Payoff Strategies: Is It Right for You?

If your financial situation improves, you might consider paying off your $20,000 loan early.

- Save on Interest: Paying off the loan sooner means you’ll pay less total interest, as interest accrues on the outstanding principal balance.

- Check for Prepayment Penalties: Most car loans do not have prepayment penalties, but always double-check your loan agreement to be sure.

- Make Extra Payments: Even small extra payments, like rounding up your monthly payment or making an extra payment annually, can significantly shorten your loan term and save interest.

- Bi-weekly Payments: Some borrowers opt for bi-weekly payments (half your monthly payment every two weeks). Since there are 26 bi-weekly periods in a year, this effectively results in one extra full monthly payment annually, accelerating payoff.

While saving interest is great, ensure paying off your car loan early doesn’t compromise other financial priorities, like building an emergency fund or contributing to retirement savings.

4. Refinancing Options: When and Why You Might Consider It

After a year or two, your financial situation or market interest rates might change, making refinancing an attractive option.

- Improved Credit Score: If your credit score has significantly improved since you took out the original loan, you might qualify for a lower interest rate.

- Lower Market Rates: If prevailing auto loan interest rates have dropped, refinancing could save you money.

- Change in Financial Circumstances: You might want to lower your monthly payment (by extending the term, though this increases total interest) or shorten your term (to save interest).

- Removing a Co-signer: If your credit has improved, you might be able to refinance the loan solely in your name, releasing your co-signer from their obligation.

Refinancing involves applying for a new loan to pay off your existing one. It’s worth exploring if you believe you can secure a significantly better APR.

Common Mistakes to Avoid

Even with the best intentions, car buyers often stumble into common pitfalls. Being aware of these can save you a lot of headache and money.

1. Not Checking Your Credit Score

This is a fundamental error. Going into the loan application process blind regarding your credit score is like playing darts in the dark. You won’t know if the rates you’re offered are fair, and you won’t have time to correct errors.

2. Only Applying to One Lender

Relying solely on the first offer you receive, whether from your bank or a dealership, is a sure way to leave money on the table. Shopping around is crucial for comparison. Lenders compete for your business, so let them!

3. Focusing Solely on the Monthly Payment

While important, focusing only on the monthly payment can lead to extending the loan term unnecessarily, resulting in a much higher total cost of the loan due to accumulated interest. Always consider the total interest paid.

4. Ignoring the Total Cost of the Loan

The "total cost of the loan" includes the principal plus all interest and fees. This figure is the true measure of what you’re paying for the privilege of borrowing. A lower monthly payment might mask a much higher total cost.

5. Stretching the Loan Term Too Long

While a 5-year loan is a good balance, extending a $20,000 loan to 6 or 7 years solely to get a lower monthly payment is often a mistake. This significantly increases the total interest paid and puts you at a higher risk of negative equity for a longer period.

6. Not Factoring in All Ownership Costs

Beyond the loan payment, cars come with significant expenses: insurance, fuel, maintenance, and potential repairs. A common mistake is not budgeting for these, leading to financial strain even if the loan payment is manageable.

Pro Tips from an Expert Blogger

Drawing from years of experience in personal finance and consumer advice, here are some final expert tips to ensure your $20,000 car loan for 5 years is a success.

The "20/3/8" Rule for Car Buying

This simple guideline can help you make a financially sound car purchase:

- 20% Down Payment: Aim to put down at least 20% of the car’s purchase price to reduce your loan amount, lower your monthly payments, and minimize negative equity risk.

- 3-Year Loan Term (or 5 years max): While we’re discussing 5-year loans, a 3-year term is generally ideal for minimizing interest. For a $20,000 loan, 5 years is a reasonable maximum to avoid excessive interest and long-term debt.

- 8% of Monthly Gross Income: Your total car expenses (loan payment, insurance, fuel, maintenance) should not exceed 8% of your gross monthly income. This ensures your car is an asset, not a financial burden.

Adhering to this rule, even if it means adjusting your expectations for the car, will set you up for long-term financial health.

Always Read the Fine Print

It sounds obvious, but in the excitement of buying a new car, many people rush through loan documents. Take your time. Read every line of the loan agreement, especially sections on interest rates, fees, prepayment penalties, and default clauses. If you don’t understand something, ask for clarification. Don’t sign until you’re completely comfortable.

Factor in Ownership Costs Beyond the Payment

A car is more than just a monthly loan payment. As mentioned, remember to budget for:

- Car Insurance: Get quotes before you buy, as rates vary wildly based on the vehicle, your driving record, and location.

- Fuel: Estimate your weekly or monthly fuel costs based on your commute and the car’s fuel efficiency.

- Maintenance: Set aside a small amount each month for routine maintenance (oil changes, tire rotations) and unexpected repairs. A good rule of thumb is 1-1.5% of the car’s purchase price annually.

Overlooking these can quickly turn an affordable monthly loan payment into an unaffordable overall car ownership cost.

Conclusion: Drive Away with Confidence

Securing a $20,000 car loan for 5 years can be a smart and manageable way to finance your next vehicle, provided you approach it with knowledge and preparation. By understanding the factors that influence your loan, diligently shopping for the best rates, and managing your loan responsibly, you can drive away with confidence, knowing you’ve made a sound financial decision.

Remember, the goal isn’t just to get approved; it’s to get the best possible terms that align with your financial well-being. Arm yourself with information, be patient, and don’t be afraid to negotiate. Your future self (and your wallet) will thank you. Start your journey wisely, and enjoy the open road!