Securing a Car Loan with a 558 Credit Score: Your Comprehensive Guide to Driving Away

Securing a Car Loan with a 558 Credit Score: Your Comprehensive Guide to Driving Away Carloan.Guidemechanic.com

Navigating the world of auto financing can feel daunting, especially when your credit score isn’t in the "excellent" or "good" range. If you’re looking to buy a car with a 558 credit score, you’re likely facing some unique challenges. But here’s the good news: getting a car loan with a 558 credit score is absolutely possible. It simply requires a strategic approach, a clear understanding of your options, and a commitment to smart financial planning.

As an expert blogger and SEO content writer with years of experience in personal finance, I’ve seen firsthand how challenging and rewarding this journey can be. My mission with this comprehensive guide is to equip you with all the knowledge and actionable steps you need to secure a car loan, even with a credit score that’s considered "poor." We’ll dive deep into understanding your score, exploring lender options, and building a strong application.

Securing a Car Loan with a 558 Credit Score: Your Comprehensive Guide to Driving Away

Understanding Your 558 Credit Score: What It Means for Auto Financing

Before we explore loan options, let’s understand what a 558 credit score signifies. Credit scores, particularly FICO scores, range from 300 to 850. A score of 558 falls squarely into the "Poor" category.

This classification indicates to lenders that you may have a history of missed payments, high credit utilization, or other financial behaviors that suggest a higher risk of default. It doesn’t mean you’re a lost cause; it simply means lenders will approach your application with more caution.

The Impact of a Low Credit Score

A 558 credit score significantly impacts the terms of any loan you might receive. You’ll likely encounter higher interest rates, stricter repayment terms, and potentially a requirement for a larger down payment. Lenders are taking on more risk, and they compensate for that risk through less favorable loan conditions for the borrower.

Based on my experience, many individuals with scores in this range feel discouraged. However, approaching this with a realistic mindset is crucial. While you might not qualify for the lowest advertised rates, a car loan can be a powerful tool for rebuilding your credit if managed responsibly.

Can You Get a Car Loan with a 558 Credit Score? The Direct Answer

Yes, you can absolutely get a car loan with a 558 credit score. While it’s more challenging than for someone with excellent credit, there are lenders and strategies specifically designed for individuals in your situation. It’s not a question of "if," but "how" and "under what terms."

Many lenders specialize in what’s known as "subprime auto loans." These loans are extended to borrowers with lower credit scores, typically below 660. These lenders understand that life happens, and they are willing to work with you, provided you can demonstrate the ability to repay the loan.

The Realities and Challenges of Subprime Auto Loans

While possible, securing a car loan with a 558 credit score comes with certain realities you need to be aware of. Understanding these challenges upfront will help you prepare and set realistic expectations.

Higher Interest Rates

This is perhaps the most significant reality. Lenders view a 558 credit score as a higher risk, and to mitigate that risk, they charge higher interest rates. This means you’ll pay significantly more over the life of the loan compared to someone with a good or excellent credit score.

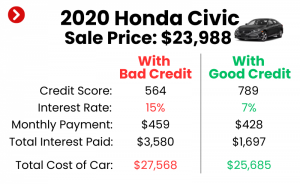

For example, while someone with a 720+ score might get an APR of 5-8%, you might be looking at rates anywhere from 15% to 25% or even higher, depending on various factors. It’s essential to factor this into your budget.

Stricter Loan Terms

Lenders might impose stricter terms to protect their investment. This could include shorter loan terms (to reduce the total interest paid and the risk period), or requiring a larger down payment. They might also limit the types of vehicles you can finance.

You might find that some lenders are hesitant to finance older vehicles or cars with very high mileage, as these present a higher risk of mechanical failure and depreciation.

Limited Lender Options

While subprime lenders exist, your pool of potential lenders will be smaller compared to someone with prime credit. Traditional banks and credit unions might be less likely to approve you directly without a co-signer or substantial down payment. This means you’ll need to know where to look.

Pro tips from us: Don’t get discouraged by initial rejections. The key is to target the right lenders from the start.

Strategic Steps to Boost Your Chances of Car Loan Approval

Getting approved for a car loan with a 558 credit score isn’t about luck; it’s about preparation and strategy. Here are the most effective steps you can take to significantly improve your chances.

1. Check Your Credit Report for Errors

Before you even think about applying for a loan, pull your full credit reports from all three major bureaus: Experian, Equifax, and TransUnion. You can do this for free once a year at AnnualCreditReport.com. Scrutinize every detail for inaccuracies.

Based on my experience, errors on credit reports are more common than people realize. A simple reporting mistake could be artificially lowering your score. If you find any errors, dispute them immediately with the credit bureau. This process can take time, so start early.

2. Save for a Significant Down Payment

This is arguably one of the most powerful tools you have with a low credit score. A substantial down payment reduces the amount you need to borrow, which in turn reduces the lender’s risk. It shows commitment and financial stability.

Aim for at least 10-20% of the car’s purchase price, if possible. Even 5% is better than nothing. A larger down payment can also help you secure a lower interest rate, as it demonstrates your ability to save and invest in the purchase.

3. Consider a Co-signer

Bringing a co-signer with good credit to your application can dramatically improve your approval odds and potentially secure you a much better interest rate. A co-signer essentially guarantees the loan, promising to make payments if you default.

Common mistakes to avoid are: Asking someone to co-sign without fully explaining the responsibility. Make sure your co-signer understands that their credit will also be affected if you miss payments. Choose someone you trust implicitly and who trusts you.

4. Prove Your Income and Stability

Lenders want to see a consistent income stream that can comfortably cover your car payments, insurance, and other living expenses. Gather documentation such as pay stubs, bank statements, and employment verification letters.

The more stable and reliable your income appears, the more confident a lender will be in your ability to repay the loan. If you have a long history with your current employer, highlight that stability.

5. Be Realistic About Your Vehicle Choice

With a 558 credit score, luxury or brand-new vehicles are likely out of reach – at least for now. Focus on an affordable, reliable used car that meets your essential needs. A lower purchase price means a smaller loan amount, which is easier to get approved for and has lower monthly payments.

Pro tips from us: Look for cars that are a few years old but still have a good reputation for reliability and lower insurance costs. This reduces both your loan burden and your overall cost of ownership.

6. Get Pre-approved (But Don’t Get Multiple Hard Inquiries)

Pre-approval is a fantastic way to understand what you can afford before stepping foot in a dealership. Many online lenders and financial institutions offer pre-approval with a "soft inquiry," which doesn’t harm your credit score.

This process gives you an estimate of the loan amount, interest rate, and terms you qualify for. It empowers you to negotiate confidently at the dealership, as you already know your financing baseline. However, limit hard inquiries when applying for final approval to a short window (typically 14-45 days) so they count as one for scoring purposes.

7. Explore Different Lender Types

Not all lenders are created equal, especially for subprime borrowers. Here’s where to focus your search:

- Online Subprime Lenders: Companies like Capital One Auto Finance, Carvana, and specialized bad credit auto lenders often have more flexible criteria than traditional banks. They are accustomed to working with lower credit scores.

- Credit Unions: While sometimes stricter, credit unions are member-focused and might be more willing to work with you, especially if you have an existing relationship. Their interest rates can also be competitive.

- Dealership Financing (Buy Here Pay Here – BHPY): These dealerships offer in-house financing, often without a traditional credit check. While convenient, they typically come with very high interest rates and less consumer protection. Use them as a last resort and proceed with extreme caution. Always read the fine print.

8. Negotiate Your Terms

Even with a low credit score, negotiation is still possible. Don’t just accept the first offer. Focus on the total cost of the loan, not just the monthly payment. A longer loan term might reduce your monthly payment but significantly increase the total interest paid.

Based on my experience, many people get fixated on the monthly payment. Always ask about the APR, total interest, and any fees. Try to negotiate down the interest rate, even by a percentage point, as it can save you hundreds or thousands over the loan term.

The Car Loan Application Process: A Step-by-Step Walkthrough

Once you’ve done your preparation, the application process itself becomes much smoother.

- Budget Creation: Before you apply, create a realistic budget. Factor in not just the car payment, but also insurance (which will be higher with a newer car and lower credit score), fuel, maintenance, and registration. Can you truly afford this?

- Gather Documents: Have all necessary documents ready: proof of income (pay stubs, tax returns), proof of residence (utility bills), driver’s license, insurance quotes, and down payment funds.

- Seek Pre-approval: As mentioned, get pre-approved by a few lenders to compare offers. This gives you leverage and clarity.

- Shop for a Car: With your pre-approval in hand, you know your budget. Shop for a car that fits your needs and financial constraints. Don’t be swayed by high-pressure sales tactics.

- Finalize the Loan: Once you’ve chosen a car, the dealer or your chosen lender will finalize the loan. Review all documents carefully, asking questions about anything you don’t understand. Don’t rush this step.

What to Expect: Terms & Conditions for a 558 Credit Score Car Loan

When you’re approved for a car loan with a 558 credit score, anticipate certain terms and conditions that differentiate it from prime loans.

- Higher Annual Percentage Rate (APR): This is the cost of borrowing expressed as a yearly rate. Expect an APR significantly above the national average, often in the double digits.

- Shorter Loan Terms: Lenders might offer shorter repayment periods (e.g., 36 or 48 months instead of 60 or 72 months) to reduce their risk exposure. This means higher monthly payments but less total interest.

- Required Down Payment: It’s highly likely you’ll need a down payment. The larger it is, the better your chances and terms.

- Potentially Fewer Perks: You might not get access to special financing offers, low-APR promotions, or dealer incentives typically reserved for borrowers with higher credit scores.

- Potential for Collateral Requirements: While the car itself usually serves as collateral, be aware of any additional requirements or restrictions on the vehicle.

for a deeper dive into understanding APR, loan terms, and more.

Post-Loan Approval: Leveraging Your Car Loan to Improve Your Credit

Getting the loan is just the first step. This car loan can become a powerful tool for credit rebuilding if managed correctly.

Make every single payment on time, every single month. Payment history is the most significant factor in your credit score. Consistent, timely payments will demonstrate your reliability to credit bureaus.

As you make on-time payments, your credit score will gradually improve. After 6-12 months of perfect payments, you might even consider refinancing your car loan for a lower interest rate, saving you money in the long run.

Common Mistakes to Avoid When Getting a Car Loan with Bad Credit

Navigating subprime auto loans can be tricky. Here are some common pitfalls to steer clear of:

- Not Checking Your Credit Report: Assuming your score is what you think it is, or failing to correct errors, can severely hinder your application.

- Applying Everywhere: Each hard inquiry can temporarily ding your score. Group your applications within a short window (14-45 days) so they count as one for scoring models.

- Focusing Only on Monthly Payment: A low monthly payment might mean a very long loan term and excessive interest. Always look at the total cost of the loan.

- Skipping the Down Payment: This is a missed opportunity to reduce risk for the lender and improve your terms.

- Buying More Car Than You Can Afford: Overextending yourself financially can lead to missed payments, repossession, and further damage to your credit.

- Not Understanding the Terms: Signing documents without fully comprehending the interest rate, fees, and repayment schedule is a recipe for regret.

- Ignoring Insurance Costs: Car insurance can be expensive, especially with a newer car and a lower credit score. Factor it into your budget.

Pro Tips from Us: Expert Advice for Success

- Be Patient: Improving your credit score takes time, and finding the right loan might not happen overnight. Patience is key.

- Demonstrate Stability: Lenders love stability. Highlight your long-term employment, stable residence, and consistent income.

- Consider a Smaller Loan First: If a car loan feels too risky, consider a smaller credit-builder loan or a secured credit card to start improving your payment history.

- Set Up Automatic Payments: This is a foolproof way to ensure you never miss a payment and avoid late fees, helping your credit score immensely.

- Read Reviews of Lenders: Before committing, research lenders online. Look for reviews regarding their customer service, transparency, and fairness, especially for subprime loans.

- Understand Your FICO Score: to better understand how to improve it.

- Don’t Settle: While your options might be limited, don’t jump at the first offer. Compare at least 2-3 pre-approvals before making a decision.

for more targeted strategies on improving your financial standing.

Final Thoughts: Driving Towards a Better Financial Future

Securing a car loan with a 558 credit score is a significant step towards achieving your transportation needs and, more importantly, an opportunity to build a stronger financial future. While the road may have a few more bumps, with diligent preparation, realistic expectations, and smart decision-making, you can absolutely drive away with a car and a plan for improved credit.

Remember, this isn’t just about getting a car; it’s about demonstrating financial responsibility and opening doors to better financial opportunities down the line. Start by understanding your credit, saving for a down payment, and exploring all your lender options. With this comprehensive guide, you are well-equipped to navigate the process successfully. Good luck on your journey!