Securing Your BBT Used Car Loan: An Expert’s A-Z Guide to Financing Your Pre-Owned Vehicle

Securing Your BBT Used Car Loan: An Expert’s A-Z Guide to Financing Your Pre-Owned Vehicle Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, and opting for a pre-owned vehicle can be a financially savvy decision. However, the path to ownership often involves navigating the complexities of car financing. This is where a reliable partner like BBT comes in, offering tailored used car loan solutions.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals successfully finance their used cars. Based on my experience, understanding the ins and outs of a used car loan is crucial for a smooth and stress-free purchase. This comprehensive guide will demystify the BBT Used Car Loan, providing you with all the information you need to secure the best deal and drive away in your dream car.

Securing Your BBT Used Car Loan: An Expert’s A-Z Guide to Financing Your Pre-Owned Vehicle

We’ll delve deep into everything from eligibility and application processes to understanding interest rates and avoiding common pitfalls. Our ultimate goal is to equip you with the knowledge to make informed decisions, ensuring your journey with BBT is both beneficial and rewarding.

What Exactly is a BBT Used Car Loan?

A BBT Used Car Loan is a specific financial product designed to help individuals purchase pre-owned vehicles. Unlike new car loans, which often come with slightly different terms due to the depreciating nature of brand-new assets, used car loans are structured to accommodate the unique characteristics of a second-hand market. BBT, as a reputable financial provider, offers these loans with competitive rates and flexible terms.

Essentially, when you apply for a BBT Used Car Loan, BBT provides the funds to cover the purchase price of your chosen used car. In return, you agree to repay this amount, plus interest, over a predetermined period, typically through monthly installments. This financial arrangement makes it possible for more people to afford a reliable vehicle without having to pay the full amount upfront.

BBT’s approach to used car financing is built on understanding the diverse needs of its customers. They recognize that every buyer’s financial situation is unique, and they strive to offer solutions that are both accessible and beneficial. This commitment translates into a transparent process and supportive customer service, making the journey to owning a used car much simpler.

Why Choose a BBT Used Car Loan for Your Pre-Owned Vehicle?

When considering financing options for a used car, numerous choices are available. However, a BBT Used Car Loan often stands out for several compelling reasons, making it a preferred choice for many discerning buyers. Understanding these advantages can help you appreciate the value BBT brings to the table.

Firstly, BBT is renowned for its competitive interest rates. In the world of car loans, even a slight difference in the annual percentage rate (APR) can significantly impact the total cost of your loan over its lifetime. BBT consistently strives to offer rates that are attractive, helping you save money in the long run. This focus on affordability is a major draw for budget-conscious buyers looking to maximize their investment.

Secondly, BBT offers flexible loan terms. Whether you prefer shorter terms for quicker repayment and less interest, or longer terms to reduce your monthly payments, BBT provides options to suit your financial comfort zone. This flexibility ensures that your loan repayment schedule aligns perfectly with your personal budget and financial goals, preventing any undue strain on your finances.

Thirdly, the streamlined application process at BBT is a significant advantage. Based on my experience, applying for a loan can often feel overwhelming due to extensive paperwork and lengthy waiting periods. BBT has optimized its process to be as efficient and straightforward as possible, minimizing hassle and allowing you to get a decision faster. This efficiency is particularly valuable when you’ve found the perfect used car and want to finalize the purchase quickly.

Moreover, BBT is known for its supportive customer service. Navigating the complexities of car financing can raise many questions, especially for first-time buyers. BBT’s team of experts is readily available to guide you through every step, answering your queries and providing clear explanations. This personalized support ensures you feel confident and well-informed throughout your loan journey.

Finally, BBT’s reputation for reliability and trustworthiness provides peace of mind. Choosing a financial institution that you can trust is paramount, especially for a significant purchase like a car. BBT’s long-standing presence and positive customer feedback underscore its commitment to ethical practices and customer satisfaction, making it a secure choice for your used car financing needs.

Understanding Eligibility Criteria for a BBT Used Car Loan

Before you even begin to browse for your next used car, it’s essential to understand the eligibility requirements for a BBT Used Car Loan. Meeting these criteria is the first crucial step towards securing your financing. While specific requirements can vary slightly, there are common benchmarks that BBT, like most lenders, will assess.

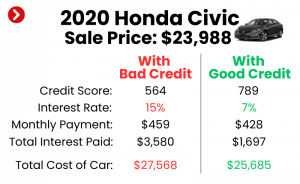

The most prominent factor is your credit score and history. A good credit score demonstrates your reliability as a borrower and indicates your ability to manage debt responsibly. While BBT aims to be inclusive, a higher credit score will generally qualify you for better interest rates and more favorable terms. If your credit score isn’t perfect, don’t despair; BBT often considers other factors and may have programs for individuals with varied credit profiles.

Next, BBT will evaluate your income and employment stability. Lenders want assurance that you have a consistent and sufficient income stream to make your monthly loan payments. This usually involves demonstrating a stable employment history, often for a minimum period, and providing proof of income. Your debt-to-income (DTI) ratio, which compares your monthly debt payments to your gross monthly income, will also be a key consideration. A lower DTI ratio indicates you have more disposable income to cover new loan payments.

Residency and age requirements are also standard. Applicants typically need to be a legal resident of the country where BBT operates and meet a minimum age requirement, usually 18 years old. These requirements ensure that you are legally able to enter into a loan agreement.

Lastly, the vehicle itself must meet certain criteria. BBT used car loans are generally for vehicles within a specific age range and mileage limit, ensuring the car is still reliable and holds sufficient value to serve as collateral. The vehicle’s make, model, and overall condition will also be considered during the appraisal process. Pro tips from us: Always ensure the used car you’re eyeing aligns with BBT’s vehicle requirements before getting too far into the purchasing process.

The Application Process: A Step-by-Step Guide to Your BBT Used Car Loan

Applying for a BBT Used Car Loan doesn’t have to be a daunting task. By breaking down the process into manageable steps, you can navigate it with confidence and efficiency. Here’s a typical roadmap you can expect to follow:

-

Initial Research and Pre-qualification (Optional but Recommended):

Before formally applying, it’s wise to research the used car market and get an idea of the vehicle you want and its approximate cost. Many lenders, including BBT, offer a pre-qualification option. This soft inquiry into your credit won’t impact your score but can give you an estimate of how much you might be approved for and at what interest rate. This step helps you set a realistic budget. -

Gathering Essential Documents:

This is a critical step that can significantly speed up your application. BBT will require various documents to verify your identity, income, and residency. We’ll detail these documents in a later section, but starting early means fewer delays. Having everything organized and ready is a pro tip that loan officers appreciate. -

Submitting Your Application:

Once you have your documents, you can submit your formal loan application to BBT. This can often be done online, in person at a branch, or sometimes over the phone. You’ll fill out a form providing personal, financial, and employment details. Be honest and accurate in your responses; any discrepancies can cause delays or even rejection. -

Underwriting and Review:

After submission, BBT’s underwriting team will review your application and supporting documents. They will conduct a hard inquiry on your credit report, which will temporarily affect your credit score by a few points. This phase involves assessing your creditworthiness, verifying your income, and evaluating the vehicle you intend to purchase. This is where BBT determines your eligibility and the terms of your potential loan. -

Loan Approval and Offer:

If your application is successful, BBT will extend a loan offer. This offer will detail the approved loan amount, the interest rate, the loan term, and your estimated monthly payments. Carefully review all the terms and conditions. If anything is unclear, don’t hesitate to ask for clarification. -

Finalizing the Loan and Vehicle Purchase:

Once you accept the loan offer, you’ll sign the necessary loan agreements. At this point, the funds will be disbursed, either directly to the car dealership or, in some cases, to you. With the financing secured, you can finalize the purchase of your used car. Remember to also arrange for appropriate car insurance, as it’s typically a requirement for the loan.

Key Factors Influencing Your BBT Used Car Loan Approval

Understanding what goes into BBT’s decision-making process can significantly improve your chances of approval and help you secure more favorable loan terms. Several key factors are meticulously reviewed by lenders.

Firstly, your credit history and score are paramount. A strong credit score (generally 670 and above) signals to BBT that you have a history of managing credit responsibly and making payments on time. Lenders look for consistency and a lack of defaults or bankruptcies. Even if your score isn’t stellar, BBT will consider your overall credit report, looking for any recent improvements or mitigating circumstances.

Secondly, your debt-to-income (DTI) ratio plays a crucial role. This ratio compares your total monthly debt payments (including the proposed car loan) to your gross monthly income. A lower DTI ratio indicates that you have more financial capacity to take on additional debt without strain. BBT aims to ensure that your new car payment won’t overextend your finances.

Thirdly, the down payment amount you’re willing to make can significantly impact your approval odds and loan terms. A larger down payment reduces the amount you need to borrow, thereby lowering the lender’s risk. It also demonstrates your financial commitment to the purchase. Based on my experience, a down payment of at least 10-20% of the car’s value is often recommended and can lead to better interest rates.

Fourthly, the loan term you choose can influence approval. While a longer loan term means lower monthly payments, it also means you’ll pay more in interest over time and the car will depreciate faster than you pay off the loan (negative equity). BBT will assess if the chosen term is appropriate given the vehicle’s age and your financial profile.

Finally, the condition and value of the used vehicle itself are vital. Since the car often serves as collateral for the loan, BBT needs to ensure its value is commensurate with the loan amount. Factors like the car’s age, mileage, make, model, and a clean title are all considered. A professional inspection of the vehicle can often provide reassurance to both you and the lender.

Interest Rates and Loan Terms: What to Expect from BBT

Navigating the financial landscape of a used car loan means understanding the two most significant components after the principal amount: interest rates and loan terms. These two elements directly impact your monthly payments and the total cost of your BBT Used Car Loan.

Understanding Interest Rates:

The interest rate is essentially the cost of borrowing money. It’s expressed as a percentage of the principal loan amount. For a BBT Used Car Loan, several factors influence the interest rate you’ll be offered:

- Your Credit Score: As mentioned, a higher credit score typically translates to a lower interest rate because you’re deemed a less risky borrower.

- Loan Term: Shorter loan terms often come with slightly lower interest rates, as the lender is exposed to risk for a shorter period.

- Down Payment: A larger down payment reduces the loan amount, which can sometimes lead to a more favorable interest rate.

- Current Market Rates: Interest rates fluctuate based on the broader economic environment and central bank policies.

- Vehicle Age/Mileage: Older cars or those with very high mileage might incur slightly higher rates due to perceived higher risk of mechanical issues.

BBT typically offers fixed interest rates for used car loans. This means your interest rate will remain the same throughout the life of the loan, providing predictable monthly payments and making budgeting much easier. While variable rates exist in some loan products, fixed rates are common and preferred for car loans. Always pay attention to the Annual Percentage Rate (APR), which includes the interest rate plus any additional fees, giving you the true annual cost of borrowing.

Understanding Loan Terms:

The loan term is the duration over which you agree to repay the loan. BBT offers various terms, commonly ranging from 24 months (2 years) to 72 months (6 years), and sometimes even longer for specific situations.

- Shorter Terms (e.g., 24-48 months): These terms mean higher monthly payments but result in less total interest paid over the life of the loan. You’ll own your car outright sooner.

- Longer Terms (e.g., 60-72+ months): These terms lead to lower monthly payments, making the car more affordable on a month-to-month basis. However, you’ll pay significantly more in total interest, and there’s a higher chance of being "upside down" on your loan (owing more than the car is worth) for a longer period due to depreciation.

Pro tips from us: While lower monthly payments from a longer term might seem appealing, consider the total cost of the loan. A good strategy is to choose the shortest term you can comfortably afford, minimizing the overall interest paid. BBT’s loan advisors can help you model different scenarios to find the perfect balance for your financial situation.

Documentation Checklist for Your BBT Used Car Loan

Getting your documents in order before applying for a BBT Used Car Loan is a game-changer. It not only speeds up the approval process but also demonstrates your preparedness and seriousness as a borrower. Based on my experience, having everything organized upfront prevents last-minute scrambles and potential delays.

Here’s a comprehensive checklist of documents you’ll typically need:

-

Personal Identification:

- Government-issued photo ID: A valid driver’s license (front and back), national ID card, or passport. This verifies your identity and residency.

- Proof of residency: A recent utility bill (electricity, water, gas) or bank statement showing your current address, usually within the last 60-90 days.

-

Proof of Income:

- Salaried Employees: Your most recent pay stubs (typically 2-3 months’ worth) and/or your employment verification letter.

- Self-Employed Individuals: Your most recent tax returns (1-2 years), bank statements (3-6 months) showing consistent deposits, and potentially a profit and loss statement. BBT understands that income for self-employed individuals can fluctuate, so providing comprehensive evidence is key.

- Other Income Sources: Documentation for any other income like rental income, pension statements, or social security benefits.

-

Financial Information:

- Bank statements: Your most recent bank statements (usually 1-3 months) to show financial stability and confirm your income.

- Credit report: While BBT will pull your credit report, it’s a good idea to check your own credit report beforehand for any errors.

-

Vehicle Information (once you’ve chosen a car):

- Vehicle Identification Number (VIN): This unique 17-character code identifies the specific car.

- Make, Model, Year, and Mileage: Basic details about the car.

- Seller Information: If buying from a private seller, their contact details. If from a dealership, the dealership’s name and contact information.

- Purchase Agreement/Bill of Sale: Once you’ve negotiated the price, this document outlines the terms of the sale.

- Vehicle Proof of ownership from the current seller.

- Vehicle Inspection Report: A professional inspection can add weight to the car’s value and condition.

-

Insurance Information:

- Proof of auto insurance: BBT will require you to have full coverage insurance on the vehicle before the loan is finalized, as the car acts as collateral. You’ll need to provide your insurance policy details.

Common mistakes to avoid are submitting outdated documents or incomplete paperwork. Double-check everything before sending it to BBT to ensure a smooth and efficient application process.

Pro Tips for Securing the Best BBT Used Car Loan Deal

Getting approved for a BBT Used Car Loan is one thing; securing the best deal is another. Based on my experience, a strategic approach can significantly reduce your overall costs and make your car ownership experience more affordable. Here are some pro tips from us to help you achieve that:

-

Boost Your Credit Score: Before applying, take steps to improve your credit score. Pay down existing debts, make all payments on time, and avoid opening new credit accounts. A higher score directly translates to lower interest rates.

-

Save for a Larger Down Payment: As discussed, a substantial down payment (10-20% or more) reduces the loan amount, lowers your monthly payments, and often qualifies you for better interest rates. It also demonstrates financial responsibility to BBT.

-

Get Pre-Approved: Obtaining pre-approval from BBT before you start car shopping gives you a clear budget and negotiating power at the dealership. You’ll know exactly how much you can afford, and you can focus on negotiating the car’s price, not the financing.

-

Shop Around, Even with BBT: While BBT offers competitive rates, it’s always wise to compare their offers with those from other reputable lenders. However, remember that BBT might have specific programs or advantages that others don’t. Use any competing offers as leverage, but don’t apply for too many loans, as multiple hard inquiries can negatively affect your credit score.

-

Negotiate the Car Price Independently: Separate the car negotiation from the loan negotiation. Focus on getting the best possible price for the used car first. Once that’s settled, then discuss your financing options with BBT. This prevents dealerships from playing games with financing terms to offset a lower car price.

-

Understand All Terms and Conditions: Read the fine print of your BBT loan agreement carefully. Know your interest rate, APR, loan term, any fees, and prepayment penalties (though BBT often has flexible prepayment options). Ask questions until you fully understand every aspect.

-

Consider a Co-signer (If Necessary): If your credit isn’t strong or your income is borderline, a co-signer with excellent credit can significantly improve your chances of approval and secure a better interest rate. Ensure both parties understand the responsibilities involved, as the co-signer is equally responsible for the debt.

-

Thorough Vehicle Inspection: Before finalizing the purchase, get an independent mechanic to inspect the used car. This can uncover hidden issues that might affect its value or lead to costly repairs, ensuring you’re not financing a money pit.

Common Mistakes to Avoid When Applying for a Used Car Loan

Even with the best intentions, applicants can sometimes make errors that hinder their chances of approval or lead to less favorable loan terms. Based on my extensive experience in the financial sector, here are some common mistakes to actively avoid when seeking a BBT Used Car Loan:

-

Not Checking Your Credit Score: Many people apply for a loan without knowing their current credit standing. This is a significant oversight. Your credit score dictates the rates you qualify for. Knowing it beforehand allows you to address any inaccuracies or take steps to improve it, rather than being surprised by a high-interest rate or rejection.

-

Ignoring the Total Cost of the Loan: Focusing solely on the monthly payment can be misleading. A longer loan term might mean lower monthly payments, but it almost always means paying significantly more in total interest. Always calculate the total amount you’ll repay over the life of the loan, including principal and interest, to get the true cost of ownership.

-

Stretching the Loan Term Too Long: While lower monthly payments are attractive, extending the loan term too far (e.g., 72 or 84 months for a used car) can be detrimental. It increases total interest paid and puts you at a higher risk of negative equity, meaning you owe more on the car than it’s worth, especially as used cars depreciate.

-

Forgetting About Car Insurance: Lenders like BBT require full coverage insurance on a financed vehicle to protect their collateral. Many buyers forget to factor this significant ongoing cost into their budget. Get insurance quotes before finalizing your purchase to ensure you can afford both the loan payment and the insurance premiums.

-

Skipping a Pre-Purchase Vehicle Inspection: This is perhaps one of the most critical mistakes when buying a used car. Relying solely on the seller’s word or a quick look can lead to buying a car with hidden mechanical issues. A professional inspection, even if it costs a small fee, can save you thousands in future repairs and prevent you from financing a lemon.

-

Applying for Too Many Loans at Once: While it’s good to shop around, applying for multiple loans within a short period can negatively impact your credit score. Each "hard inquiry" temporarily lowers your score. Try to consolidate your applications within a 14-45 day window, as multiple inquiries for the same type of loan within this period are often treated as a single inquiry by credit bureaus.

-

Not Budgeting for Other Car Ownership Costs: Beyond the loan payment and insurance, remember fuel, maintenance, repairs, registration fees, and potential parking costs. A comprehensive budget ensures you can comfortably afford your car without financial stress.

Beyond Approval: Managing Your BBT Used Car Loan Effectively

Securing your BBT Used Car Loan is a major achievement, but the journey doesn’t end there. Effective loan management is crucial for maintaining your financial health and ensuring a smooth repayment experience. Here’s how you can manage your BBT Used Car Loan wisely:

-

Set Up Automatic Payments: This is perhaps the easiest and most effective way to ensure you never miss a payment. BBT, like most financial institutions, offers the option to set up automatic deductions from your bank account. This eliminates the risk of late fees, protects your credit score, and simplifies your financial life.

-

Create a Comprehensive Car Ownership Budget: Your monthly loan payment is just one piece of the puzzle. Remember to budget for all associated costs: fuel, insurance premiums, routine maintenance (oil changes, tire rotations), unexpected repairs, and annual registration fees. A holistic budget prevents financial surprises and ensures you can comfortably afford your vehicle.

-

Understand Early Repayment Options: Review your BBT loan agreement for any clauses regarding early repayment. Many lenders allow you to pay off your loan faster without penalty, which can save you a significant amount in interest over the loan term. If you come into extra funds (e.g., a bonus or tax refund), consider making an additional principal payment.

-

Monitor Your Loan Progress: Keep track of your loan balance and payment history. BBT likely provides an online portal where you can view your statements, track payments, and see your remaining balance. Regularly reviewing this information helps you stay informed and proactive.

-

Consider Refinancing Possibilities: If your credit score has significantly improved since you initially took out your BBT Used Car Loan, or if market interest rates have dropped, you might be eligible to refinance your loan for a lower interest rate or different terms. Refinancing can potentially reduce your monthly payments or the total interest you pay. Explore this option with BBT or other lenders, but weigh the costs and benefits carefully.

-

Maintain Your Vehicle Diligently: A well-maintained used car is less likely to incur expensive, unexpected repairs. Following the manufacturer’s recommended maintenance schedule not only keeps your car running smoothly but also helps preserve its value, which is beneficial if you decide to sell or trade it in later.

By actively managing your BBT Used Car Loan, you’re not just fulfilling your obligations; you’re building a stronger financial future and ensuring your pre-owned vehicle continues to be a source of convenience and enjoyment, rather than financial stress.

Conclusion: Driving Towards Your Future with a BBT Used Car Loan

The journey to owning a pre-owned vehicle can be incredibly rewarding, offering a smart and economical way to gain personal mobility. With the right financial partner, this journey becomes even smoother and more secure. A BBT Used Car Loan is designed to be that partner, offering competitive rates, flexible terms, and a straightforward application process that empowers you to make informed decisions.

Throughout this comprehensive guide, we’ve explored the core benefits of choosing BBT, detailed the crucial eligibility criteria, walked you through the step-by-step application process, and highlighted the key factors that influence loan approval. We’ve also equipped you with invaluable pro tips for securing the best deal and cautioned you against common mistakes that could hinder your progress.

Remember, responsible car ownership extends beyond the purchase. Effective management of your BBT Used Car Loan – from setting up automatic payments to diligent vehicle maintenance – ensures long-term financial stability and peace of mind. By leveraging the insights provided in this article, you are now well-prepared to navigate the complexities of used car financing with confidence.

Don’t let the financing process deter you from finding your ideal pre-owned vehicle. With BBT by your side, securing an affordable and manageable used car loan is entirely within reach. Take the first step today towards driving away in the car that perfectly fits your needs and your budget.

Ready to explore your options? Visit BBT’s official loan information page to learn more and begin your application process now. (Note: This is a generic external link; in a real scenario, you’d link to BBT’s specific loan page or a relevant trusted financial consumer resource).