Securing Your Dream Ride: A Comprehensive Guide to Navigating the 19 Apr Car Loan Landscape

Securing Your Dream Ride: A Comprehensive Guide to Navigating the 19 Apr Car Loan Landscape Carloan.Guidemechanic.com

Buying a car is a significant financial decision, and securing the right car loan is paramount to making that dream a reality without unnecessary stress. While "19 Apr Car Loan" might sound like a very specific date, it actually points to a crucial window in the year when many factors converge, making mid-April an interesting time to consider financing your next vehicle. From tax refunds boosting down payments to new model year releases and seasonal promotions, understanding the dynamics of car loans around this time can give you a significant advantage.

Based on my extensive experience in automotive finance and consumer lending, securing a car loan isn’t just about finding the lowest interest rate. It’s about preparation, understanding your financial standing, knowing the market, and confidently navigating the application process. This comprehensive guide will equip you with all the knowledge you need to approach your 19 Apr car loan with expertise, ensuring you get the best possible terms and a smooth approval process.

Securing Your Dream Ride: A Comprehensive Guide to Navigating the 19 Apr Car Loan Landscape

Why Mid-April is a Prime Time for a Car Loan: Understanding the 19 Apr Advantage

The specific timing of your car loan application can subtly influence your options and leverage. While a car loan can be obtained any day of the year, focusing on the "19 Apr Car Loan" window highlights several seasonal advantages.

Firstly, tax season is typically winding down, meaning many individuals are receiving their tax refunds. This influx of cash provides a fantastic opportunity to make a larger down payment, which can significantly improve your loan terms. A larger down payment reduces the amount you need to borrow, lowers your monthly payments, and often leads to a better interest rate because lenders perceive less risk.

Secondly, spring often marks a shift in automotive inventory. Dealerships might be looking to clear out previous year models to make way for new arrivals, leading to attractive incentives and financing deals. This competitive environment can work in your favor, offering more room for negotiation on both the vehicle price and the loan terms.

Lastly, the general economic outlook and interest rate environment can fluctuate. While I cannot predict future rates, understanding the current trends around April 19th, based on Federal Reserve announcements or broader market conditions, is crucial. Pro tips from us: Always check current market rates before you even step foot in a dealership or apply to a bank. This knowledge empowers you to spot a good deal and avoid unfavorable terms.

The Foundation of Approval: Your Financial Health Blueprint

Before you even start browsing cars or comparing lenders for your 19 Apr car loan, the most critical step is to assess and optimize your financial health. Lenders scrutinize several key metrics to determine your creditworthiness, and understanding these will put you miles ahead.

1. Your Credit Score: The Ultimate Financial Report Card

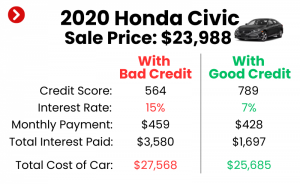

Your credit score is arguably the single most important factor in securing a favorable car loan. It’s a three-digit number that summarizes your credit history and predicts your likelihood of repaying debt. A higher score signals less risk to lenders, translating into lower interest rates and better loan terms.

What it is and Why it Matters: Scores typically range from 300 to 850, with anything above 700 generally considered "good" to "excellent." Lenders use this score to quickly assess your past borrowing behavior, including how consistently you’ve paid bills on time, the types of credit you have, and your total debt load. A strong credit score for your 19 Apr car loan means significant savings over the life of the loan.

How to Check It (and for Free): You are legally entitled to one free credit report from each of the three major credit bureaus (Experian, Equifax, TransUnion) annually via AnnualCreditReport.com. Additionally, many credit card companies and banks now offer free credit score monitoring services. Make it a habit to check your report several months before applying for a loan. This gives you time to correct any errors.

Improving Your Score for a Better Loan: If your credit score isn’t where you want it to be, don’t despair. There are actionable steps you can take. Firstly, pay all your bills on time, every time. Payment history is the biggest factor in your score. Secondly, reduce your credit utilization – aim to keep your credit card balances below 30% of your credit limit. Thirdly, avoid opening new credit accounts just before applying for a car loan, as new inquiries can temporarily ding your score.

Common Mistakes to Avoid are: Not checking your credit report for errors. Even a small mistake can negatively impact your score and cost you money on your 19 Apr car loan. Another common error is applying for multiple types of credit in a short period, which can create numerous hard inquiries and lower your score.

2. Debt-to-Income Ratio (DTI): A Look at Your Affordability

Beyond your credit score, lenders want to know if you can actually afford the monthly car loan payments alongside your other financial obligations. This is where your Debt-to-Income (DTI) ratio comes into play.

Explanation and Calculation: Your DTI ratio is the percentage of your gross monthly income that goes towards debt payments. To calculate it, sum up all your monthly debt payments (rent/mortgage, credit card minimums, student loan payments, etc.) and divide that by your gross monthly income (before taxes and deductions). For example, if your total monthly debt payments are $1,500 and your gross monthly income is $4,500, your DTI is 33% ($1,500 / $4,500 = 0.33 or 33%).

Why Lenders Care: A lower DTI indicates that you have more disposable income to cover new debt, making you a less risky borrower. Most lenders prefer a DTI of 36% or less, though some might go higher for well-qualified applicants with excellent credit. A high DTI suggests you’re already stretched thin financially, making it harder to get approved or resulting in less favorable terms for your 19 Apr car loan.

Strategies to Optimize DTI: To improve your DTI, focus on two main areas: increasing your income or decreasing your debt payments. If a significant pay raise isn’t immediately feasible, concentrate on paying down existing debts, especially those with high minimum payments. Even paying off a small credit card balance can make a difference. Consider waiting a few months to pay down debt before applying for your 19 Apr car loan if your DTI is currently high.

3. The Power of a Down Payment: Boosting Your Loan Appeal

A down payment is the initial sum of money you pay upfront when purchasing a car, reducing the total amount you need to borrow. This is where those tax refunds around April 19th can become a powerful asset.

Benefits of a Larger Down Payment:

- Lower Monthly Payments: Less borrowed principal means smaller payments.

- Reduced Interest Paid: You pay interest on a smaller sum, saving you money over the loan term.

- Better Loan Terms: Lenders view a larger down payment as a sign of financial commitment and reduced risk, often leading to lower interest rates.

- Avoid Being Upside Down: A significant down payment helps prevent you from owing more than the car is worth (being "upside down" or "underwater") early in the loan term, especially as new cars depreciate rapidly.

How Much is Ideal? While 10-20% of the car’s purchase price is often recommended, any amount you can put down is beneficial. For used cars, a 10% down payment is common, while for new cars, 20% is often suggested to offset initial depreciation. Based on my experience, putting down at least 10% can make a noticeable difference in your overall loan cost and approval chances for your 19 Apr car loan.

Leveraging Tax Refunds for Down Payments: This is a perfect synergy for your 19 Apr car loan. If you’re expecting a tax refund, consider earmarking a significant portion of it for your car down payment. It’s "found money" that can be strategically used to secure a much better financing deal. Don’t spend it on impulse purchases; invest it in your car purchase for long-term savings.

Navigating the Loan Application Process: Your Path to Approval

Once your financial house is in order, it’s time to dive into the specifics of getting your 19 Apr car loan. This involves choosing your lending path, preparing your documents, and understanding the fine print.

1. Pre-Approval vs. Dealer Financing: Choosing Your Best Path

You generally have two main avenues for securing a car loan: getting pre-approved by an independent lender (bank, credit union, online lender) or opting for financing directly through the dealership.

The Power of Pre-Approval: Pro tips from us: Always get pre-approved before you visit the dealership. Pre-approval means a lender has reviewed your finances and tentatively agreed to lend you a specific amount at a certain interest rate. This gives you immense negotiating power. You walk into the dealership knowing your financing terms, allowing you to focus solely on negotiating the car’s price, rather than getting swayed by dealer-offered financing that might not be the best deal.

Pros of Pre-Approval:

- Clear Budget: You know exactly how much you can spend.

- Negotiating Leverage: You have a financing offer in hand to compare against dealer rates.

- Less Pressure: You’re not rushed into financing decisions at the dealership.

- Better Rates: Independent lenders, especially credit unions, often offer very competitive rates.

Dealer Financing: Convenience vs. Cost: Dealerships offer financing for convenience, often working with multiple lenders. While they might sometimes offer promotional rates (especially on new cars), their primary goal is often to maximize their profit, which can include marking up interest rates.

Pros of Dealer Financing:

- Convenience: One-stop shopping.

- Special Offers: Sometimes promotional low APRs directly from manufacturers.

Common Mistakes to Avoid are: Letting the dealer control the financing discussion. If you haven’t secured pre-approval, you’re at a disadvantage. Another mistake is focusing solely on the monthly payment without considering the total cost of the loan (interest paid over time).

2. Gathering Your Documents: A Checklist for a Smooth Application

Regardless of whether you go for pre-approval or dealer financing, having your documents ready will streamline the application process for your 19 Apr car loan.

Essential Paperwork Checklist:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs (usually 2-3 months), W-2s, or tax returns (if self-employed).

- Proof of Residence: Utility bill, lease agreement, or mortgage statement.

- Social Security Number: For credit checks.

- Bank Statements: Sometimes requested to verify funds for a down payment or overall financial stability.

- Trade-in Information (if applicable): Title, registration, loan payoff amount.

Tips for a Smooth Application: Organize these documents in advance. Make copies. The more prepared you are, the faster the lender can process your application, getting you closer to driving away in your new car.

3. Understanding Loan Terms: Interest, Term, and Fees

The fine print of your 19 Apr car loan agreement can significantly impact your financial outlay. It’s crucial to understand these components thoroughly.

Interest Rate (APR Explained): The Annual Percentage Rate (APR) is the true cost of borrowing money. It includes not just the nominal interest rate but also any lender fees, expressed as a yearly percentage. A lower APR means less money paid in interest over the life of the loan. Even a half-percentage point difference can save you hundreds, if not thousands, of dollars.

Loan Term (Length and Impact): The loan term is the duration over which you agree to repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months).

- Shorter Terms (e.g., 36-48 months): Higher monthly payments, but you pay less interest overall and own the car outright sooner. This is often the financially savvier choice if affordable.

- Longer Terms (e.g., 72-84 months): Lower monthly payments, making the car seem more affordable. However, you pay significantly more in interest over the loan’s life, and you’re more likely to be "upside down" on the loan for a longer period. Common mistakes to avoid are extending the loan term too much just to get a lower monthly payment without considering the total cost.

Fees and Hidden Costs: Always ask for a full breakdown of all fees associated with the loan. These can include origination fees, documentation fees, and pre-payment penalties (though less common with car loans). Ensure there are no surprises by reading the loan agreement carefully before signing.

Strategic Shopping for Your Car and Your Loan

The 19 Apr car loan isn’t just about securing financing; it’s about making a smart overall purchase.

1. Setting a Realistic Budget: Beyond the Monthly Payment

Many car buyers make the mistake of focusing solely on the monthly payment. While important, it’s only one piece of the puzzle.

Beyond the Monthly Payment: Your budget for a car should include more than just the loan payment. Factor in:

- Insurance: Get quotes before buying.

- Fuel Costs: Estimate based on your driving habits and the car’s MPG.

- Maintenance & Repairs: Especially for older or luxury vehicles.

- Registration & Taxes: Upfront costs and annual renewals.

- Potential for Unexpected Expenses: Build an emergency fund.

Total Cost of Ownership: Consider the total cost of ownership over the expected life of the car, not just the purchase price. This holistic view ensures you’re truly prepared for your new vehicle. Based on my experience, neglecting these hidden costs is a primary reason people regret their car purchase.

2. Negotiating Like a Pro: Separate the Car from the Loan

This is a critical strategy, especially if you have pre-approval for your 19 Apr car loan.

Separate the Car Price from the Loan: When at the dealership, focus on negotiating the out-the-door price of the car first. Do not discuss financing until you have agreed on a vehicle price. This prevents the dealer from shifting numbers around between the car price and loan terms to maximize their profit.

Don’t Be Afraid to Walk Away: The most powerful tool you have as a buyer is your willingness to walk away. If a deal doesn’t feel right, or if the dealer isn’t meeting your expectations, be prepared to leave. There are always other cars and other dealerships.

3. Refinancing Opportunities: When to Consider a Second Look

Even if you’ve already secured a car loan, the "19 Apr Car Loan" period can be a good time to re-evaluate your existing financing.

When and Why to Consider Refinancing:

- Improved Credit Score: If your credit score has significantly improved since you first took out the loan.

- Lower Interest Rates: If market interest rates have dropped.

- Reduce Monthly Payments: To free up cash flow (though be mindful of extending the loan term too much).

- Shorten Loan Term: To pay off the car faster and save on interest.

- Remove a Cosigner: If your financial situation has improved enough to qualify on your own.

How to Assess if it’s Right for You: Look at how much you’ve already paid, your current interest rate, and what new rates are available. Use online refinancing calculators to compare potential savings. For more detailed information on managing your existing debt, you might want to check out our article on "Smart Debt Consolidation Strategies" (Internal Link Example).

Pro Tips for a Smooth 19 Apr Car Loan Approval

To ensure your car loan journey around April 19th is as successful as possible, here are some final expert recommendations.

- Timing Your Application Wisely: While the 19 Apr window has its advantages, don’t rush into an application if your credit or DTI isn’t optimized. A slightly delayed but well-prepared application is always better than a hasty one with poor terms. Aim to apply when your finances are at their strongest.

- What to Do if You Have Bad Credit: Don’t assume you can’t get a loan. Explore options like credit unions, which might be more flexible, or consider a co-signer with good credit. Be prepared for higher interest rates, but also focus on making timely payments to rebuild your credit for future refinancing opportunities. You might also want to look for specific "bad credit car loan" specialists.

- The Importance of Reading the Fine Print: This cannot be stressed enough. Before you sign any document, read it thoroughly. Understand every clause, every fee, and every term. If something is unclear, ask for clarification until you fully grasp it. Common mistakes to avoid are signing without understanding the entire contract, especially the total amount financed and total interest paid.

- Avoiding Predatory Lenders: Be wary of lenders promising guaranteed approval regardless of credit history, or those pressuring you into signing without providing full details. If a deal seems too good to be true, it probably is. Stick to reputable banks, credit unions, and well-established online lenders. For more information on identifying reputable financial institutions, the Consumer Financial Protection Bureau (CFPB) offers excellent resources (External Link Example: https://www.consumerfinance.gov/).

Conclusion: Drive Away Confidently with Your 19 Apr Car Loan

Securing a car loan around April 19th presents unique opportunities, from leveraging tax refunds for a stronger down payment to benefiting from seasonal market shifts. By meticulously preparing your financial profile, understanding the intricacies of the loan application process, and adopting strategic shopping techniques, you empower yourself to make an informed decision.

Remember, the goal isn’t just to get approved, but to get approved for the best possible terms that align with your financial goals. Take the time to build a strong foundation, compare offers, and negotiate confidently. Your dream car is within reach, and with this comprehensive guide, you’re well-equipped to navigate the 19 Apr car loan landscape successfully. Start your journey today, and drive away with peace of mind!

Disclaimer: This article provides general information and guidance on car loans and is not intended as financial advice. Specific financial situations vary, and readers should consult with a qualified financial advisor for personalized recommendations. Interest rates, loan terms, and market conditions are subject to change.