Securing Your Dream Ride: Navigating a Car Loan with a 743 Credit Score

Securing Your Dream Ride: Navigating a Car Loan with a 743 Credit Score Carloan.Guidemechanic.com

Embarking on the journey to purchase a new car is an exciting prospect. For many, it represents a significant life event, offering newfound freedom and convenience. When you approach this process with a strong credit score, like a robust 743, you’re already in an excellent position to secure favorable financing.

A 743 credit score places you firmly in the "Very Good" category, bordering on "Excellent." This isn’t just a number; it’s a powerful indicator to lenders that you are a reliable borrower with a proven track record of managing debt responsibly. It signals lower risk, which translates directly into better loan terms for you. In this comprehensive guide, we will explore exactly what a 743 credit score means for your car loan application, how to leverage it for the best possible deal, and the steps to confidently drive away in your new vehicle.

Securing Your Dream Ride: Navigating a Car Loan with a 743 Credit Score

Understanding Your 743 Credit Score: A Golden Ticket to Better Rates

Your credit score is a three-digit number that summarizes your creditworthiness. While scores range from 300 to 850, a 743 places you significantly above the national average. This score demonstrates a consistent history of on-time payments, responsible credit utilization, and a stable financial profile.

Lenders use this score to assess the likelihood of you repaying your loan. A higher score means lower risk for them, and they reward this reduced risk with more attractive interest rates and flexible terms. For a car loan, this translates into substantial savings over the life of the loan.

What "Very Good" Really Means for Lenders

When a lender sees a 743 credit score, they immediately categorize you as a prime borrower. This puts you in a highly competitive bracket, where financial institutions are eager to win your business. They perceive you as someone who consistently meets their financial obligations.

This perception is crucial because it directly influences the loan offers you receive. You’re not just likely to be approved; you’re likely to be approved for the best rates available to consumers. This allows you to focus more on finding the right car and less on worrying about whether you’ll qualify for financing.

The Unmistakable Advantages of a 743 Credit Score for Car Loans

Having a 743 credit score provides a significant edge in the car financing landscape. It opens doors to opportunities that borrowers with lower scores simply don’t have. Understanding these benefits can empower you to negotiate effectively and secure the most advantageous deal.

1. Access to the Lowest Interest Rates

This is arguably the most significant advantage of a high credit score. Lenders reserve their absolute best interest rates for borrowers who present the lowest risk. A 743 credit score signals this low risk unequivocally.

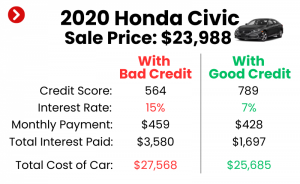

Based on my experience, a borrower with a 743 score could potentially qualify for interest rates as low as 3-5% APR (Annual Percentage Rate) or even lower, depending on market conditions and the loan term. In contrast, someone with a fair credit score might face rates of 8-15% or more. Over a five or six-year car loan, this difference can amount to thousands of dollars in savings, significantly reducing your total cost of ownership.

2. More Favorable Loan Terms and Conditions

Beyond just the interest rate, a strong credit score gives you leverage to secure better overall loan terms. Lenders may be more flexible with down payment requirements, offering options for lower or even no down payment. They might also extend longer loan terms without drastically increasing your interest rate, which can help lower your monthly payments if that’s a priority for your budget.

However, a pro tip from us is to be cautious with excessively long loan terms. While they lower monthly payments, they can lead to paying more interest over time and potentially put you in an "upside-down" position where you owe more than the car is worth. Aim for the shortest term you can comfortably afford.

3. A Wider Range of Lender Options

With a 743 credit score, you’re not limited to just a few financing sources. Banks, credit unions, online lenders, and even dealership financing departments will all be eager to offer you a loan. This competition among lenders works in your favor.

You can shop around confidently, knowing that you’re a desirable customer. This ability to compare multiple offers is crucial for finding the absolute best deal. Don’t settle for the first offer you receive; leverage your excellent credit to explore all your options.

4. Simplified and Faster Approval Process

Lenders can process applications from high-scoring individuals more quickly because the risk assessment is straightforward. You’ll likely experience a smoother, less scrutinized approval process compared to someone with a lower score. This can mean getting approved within minutes or hours, rather than days.

A quicker approval means you can move forward with your car purchase without unnecessary delays. This efficiency is a real benefit, especially if you’re in a hurry to get a new vehicle.

Beyond the Score: Other Factors Lenders Consider

While your 743 credit score is a tremendous asset, it’s not the only factor lenders review. To paint a complete picture of your financial health, they also look at several other key elements. Understanding these can help you present the strongest possible application.

1. Debt-to-Income (DTI) Ratio

Your Debt-to-Income (DTI) ratio is a crucial metric that lenders use to assess your ability to take on new debt. It compares your total monthly debt payments to your gross monthly income. For example, if your total monthly debt (credit card minimums, mortgage/rent, student loans) is $1,500 and your gross monthly income is $5,000, your DTI is 30%.

Lenders generally prefer a DTI of 36% or lower, though some may go up to 43% or even higher depending on the loan type and other factors. Even with a great credit score, a high DTI could signal that you’re stretched too thin, potentially impacting your approval or the terms offered.

2. Income and Employment Stability

Lenders want to see a consistent and reliable source of income. They’ll typically ask for proof of employment, such as pay stubs, W-2 forms, or tax returns. Stable employment over a period of several years is a strong positive indicator.

Someone with a long tenure at their current job is often viewed more favorably than someone who frequently changes employers, even if their income is similar. This stability reassures lenders of your ongoing ability to make loan payments.

3. Down Payment Amount

While a 743 credit score might allow for a zero-down payment loan, making a significant down payment can still be highly beneficial. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the life of the loan.

Furthermore, a substantial down payment reduces the lender’s risk, as you have more "skin in the game." This can sometimes result in an even better interest rate or more flexible terms. It also helps prevent you from being "upside down" on your loan, where the car’s value depreciates faster than you pay off the loan.

4. Loan-to-Value (LTV) Ratio

The Loan-to-Value (LTV) ratio compares the amount you want to borrow to the car’s appraised value. For instance, if a car is valued at $20,000 and you want to borrow $18,000, your LTV is 90%. Lenders generally prefer lower LTVs, as it means they are less exposed if the car needs to be repossessed.

A high LTV, especially over 100%, can be a red flag. This often happens if you roll negative equity from a trade-in into a new loan. While your 743 score might allow for a higher LTV, aiming for a lower one demonstrates financial prudence and can lead to better loan terms.

Step-by-Step Guide to Securing Your Car Loan with a 743 Credit Score

Navigating the car loan process can feel daunting, but with a 743 credit score, you have a significant advantage. By following these structured steps, you can confidently secure the best possible financing for your new vehicle.

Step 1: Check Your Credit Report (and Score)

Even with a strong 743 score, it’s crucial to review your full credit report from all three major bureaus (Equifax, Experian, TransUnion). Mistakes can happen, and even a minor error could potentially impact your loan application. You are entitled to a free copy of your credit report from each bureau once every 12 months.

Pro tips from us: Look for any inaccuracies, such as incorrect personal information, accounts you don’t recognize, or late payments that were actually made on time. If you find any errors, dispute them immediately. Correcting even small discrepancies can sometimes nudge your score even higher or remove any potential red flags. To get your free credit reports, visit AnnualCreditReport.com .

Step 2: Determine Your Budget and Affordability

Before you even start looking at cars, understand what you can truly afford. This involves more than just the monthly loan payment. Factor in insurance, fuel, maintenance, and potential registration fees. Use online calculators to estimate how different loan amounts, interest rates, and terms affect your monthly payment.

Common mistakes to avoid are focusing solely on the monthly payment without considering the total cost of the loan or the overall impact on your budget. Based on my experience, many buyers stretch themselves too thin by not accounting for these additional costs. Create a realistic budget that leaves room for savings and other expenses.

Step 3: Get Pre-Approved for Your Car Loan

This is a critical step for anyone, especially with a strong credit score like 743. Pre-approval means a lender has already reviewed your financial information and tentatively agreed to lend you a specific amount at a certain interest rate. It’s essentially getting a "coupon" for financing before you even step foot in a dealership.

Benefits of Pre-Approval:

- Know Your Buying Power: You’ll know exactly how much you can spend, which helps narrow down your car search.

- Stronger Negotiation Position: You walk into the dealership as a cash buyer, negotiating on the car’s price, not the monthly payment. This removes the "mystery" of financing from the car buying process.

- Compare Offers: You can get pre-approvals from multiple lenders (banks, credit unions, online lenders) within a short period (typically 14-45 days) without significantly impacting your credit score, as multiple inquiries for the same type of loan are often treated as a single inquiry. This allows you to compare and choose the best rate.

Step 4: Shop for Your Vehicle

With your pre-approval in hand, you can now confidently shop for a car. Focus on finding the right vehicle that fits your needs and budget. Remember, your pre-approval is a maximum, not a target.

When you find a car you like, negotiate the purchase price first, completely separate from financing. Since you already have your own financing offer, you can tell the dealer you’re interested in the cash price. Only after you’ve agreed on the vehicle price should you mention financing, and even then, you can see if the dealership can beat your pre-approved rate.

Step 5: Finalize Your Loan and Close the Deal

Once you’ve settled on a car and negotiated the best price, review all the loan documents carefully. Ensure the interest rate, term, and any fees match what was discussed and agreed upon. Don’t be afraid to ask questions if anything is unclear.

Pro tips from us: Pay close attention to any additional products or services the dealership might try to add, such as extended warranties, paint protection, or GAP insurance. While some of these might be valuable, assess them critically and ensure they align with your needs and budget. You can often purchase these separately and sometimes at a lower cost.

Maximizing Your 743 Score for an Even Better Outcome

While a 743 is an excellent starting point, there are always ways to refine your financial profile and potentially secure an even more advantageous car loan. These strategies focus on presenting yourself as an impeccable borrower.

1. Reduce Existing Debt

Lowering your DTI ratio before applying for a car loan can significantly strengthen your application. Pay down credit card balances or any other revolving debt. This not only improves your DTI but also frees up more of your income for your new car payment.

Even a small reduction in your overall debt can demonstrate financial discipline to lenders. It shows you’re proactive about managing your finances and not overextending yourself.

2. Avoid New Credit Inquiries or Applications

In the months leading up to a car loan application, avoid applying for new credit cards, personal loans, or other forms of credit. Each hard inquiry can temporarily dip your credit score by a few points. While a 743 can absorb a few points, it’s best to maintain as high a score as possible.

This period of "credit abstinence" ensures your score is at its peak when lenders pull your report for the car loan. It signals stability and prevents unnecessary fluctuations.

3. Save for a Larger Down Payment

As discussed, a larger down payment is always a good idea. It reduces the loan amount, lowers your monthly payments, and decreases the overall interest you’ll pay. For a 743 score borrower, a substantial down payment might even unlock an ultra-low promotional rate that’s only available to the most qualified applicants.

Based on my experience, putting down 20% or more often leads to the most favorable terms and helps you avoid negative equity as the car depreciates. It’s a strategic move for long-term financial health.

Navigating Different Lender Types

Your 743 credit score gives you the luxury of choice when it comes to where you get your car loan. Each type of lender has its own advantages and disadvantages.

1. Banks

Traditional banks are a common source for auto loans. They often offer competitive rates, especially for high-credit borrowers, and have robust online platforms for applications and account management. If you already have an established relationship with a bank, they might offer you special rates.

However, bank approval processes can sometimes be a bit slower than online lenders. It’s worth checking with your current bank first, but always compare their offer with others.

2. Credit Unions

Credit unions are member-owned financial institutions known for often offering some of the lowest interest rates on car loans. Their non-profit status allows them to pass savings onto their members. Membership requirements are usually easy to meet (e.g., living in a specific area, working for certain employers).

Pro tips from us: Always check with local credit unions. Their rates are frequently among the best, and they often provide a more personalized customer service experience.

3. Online Lenders

Online lenders have become increasingly popular due to their speed and convenience. They allow you to apply and get pre-approved from the comfort of your home, often within minutes. Many online platforms specialize in comparing offers from multiple lenders, simplifying the shopping process.

For a 743 credit score, online lenders can be incredibly competitive, often vying for top-tier borrowers with attractive rates. Ensure any online lender you consider is reputable and has positive customer reviews.

4. Dealership Financing

Dealerships often act as intermediaries, working with a network of banks and finance companies to offer you a loan. They can sometimes secure promotional rates (especially for new cars) or provide convenience by handling all the paperwork in one place.

However, based on my experience, dealership financing can sometimes include markups on interest rates to generate profit. While it’s convenient, always compare their offer against your pre-approval to ensure you’re getting the best deal. Don’t let the convenience cost you more in the long run.

Common Mistakes to Avoid, Even with a High Credit Score

Even with a fantastic 743 credit score, there are pitfalls that can prevent you from getting the absolute best deal or even lead to future financial headaches. Being aware of these can save you time, money, and stress.

1. Not Shopping Around for Rates

This is perhaps the biggest mistake. Assuming the first offer you receive is the best one, simply because you have great credit, is a costly error. As mentioned, different lenders will offer different rates, even for the same credit score.

Always get at least 3-5 pre-approvals from various sources (banks, credit unions, online lenders) before finalizing your decision. This competition forces lenders to put their best foot forward.

2. Focusing Only on the Monthly Payment

While managing your budget is essential, fixating solely on the lowest possible monthly payment can lead to longer loan terms and significantly more interest paid over time. A longer term means you’ll pay interest for more years, increasing the total cost of the loan.

Instead, balance the monthly payment with the total cost of the loan. Aim for the shortest term you can comfortably afford to minimize interest charges.

3. Skipping the Pre-Approval Process

Walking into a dealership without a pre-approval is like going to a negotiation without knowing your own strength. You lose your leverage, and the dealership controls the financing narrative.

Always secure your own financing before stepping onto the lot. This empowers you to negotiate the car price separately and use your pre-approval as a benchmark against any dealership offers.

4. Not Reading the Fine Print

Loan documents can be dense, but it’s crucial to read every single line before signing. Look for hidden fees, early repayment penalties, or terms that differ from what was discussed.

Common mistakes to avoid are rushing through the signing process or feeling pressured to sign quickly. Take your time, ask questions, and ensure you fully understand every aspect of your loan agreement.

5. Letting Inquiries Impact Your Score Unnecessarily

While multiple inquiries for the same type of loan within a short window are usually grouped as one for scoring purposes, spreading them out over several months can negatively impact your score. It’s important to do your rate shopping efficiently.

Pro tips from us: Complete all your rate shopping for car loans within a 14-to-45-day window. This minimizes the impact on your credit score and allows you to compare offers effectively.

Final Thoughts: Drive Away Confidently with Your 743 Credit Score

A 743 credit score is a powerful tool in your car buying arsenal. It signifies financial responsibility and opens the door to the most competitive interest rates and favorable loan terms. By understanding its implications, leveraging pre-approval, and carefully navigating the loan process, you are perfectly positioned to secure an excellent deal on your next vehicle.

Remember, your strong credit score puts you in the driver’s seat of the financing negotiation. Do your homework, compare offers, and don’t be afraid to walk away if the terms aren’t right. With careful planning and smart execution, you’ll not only drive away in your dream car but also save a significant amount of money over the life of your loan. For further insights on optimizing your credit for major purchases, consider reading our article on .