Securing Your Dream Ride: The Ultimate Guide to the Minimum Car Loan You Deserve

Securing Your Dream Ride: The Ultimate Guide to the Minimum Car Loan You Deserve Carloan.Guidemechanic.com

The open road, the freedom of movement, the convenience of your own vehicle – for many, owning a car is a fundamental part of life. Yet, the path to car ownership often comes with a significant financial decision: securing a car loan. For some, the goal isn’t just any loan, but the minimum car loan – one that is not only accessible but also affordable and strategically optimized for their unique financial situation.

As an expert blogger and professional SEO content writer specializing in personal finance, I understand the nuances of car financing. Based on my experience, navigating the world of auto loans can feel overwhelming, but it doesn’t have to be. This comprehensive guide is designed to empower you with the knowledge to find not just the smallest loan amount, but the most advantageous minimum car loan possible, ensuring you drive away with confidence and financial peace of mind.

Securing Your Dream Ride: The Ultimate Guide to the Minimum Car Loan You Deserve

What Does "Minimum Car Loan" Truly Mean?

When we talk about a "minimum car loan," it’s important to clarify what that encompasses. It’s not just about the lowest possible principal amount. Instead, it’s a holistic approach to securing the most accessible and affordable financing package tailored to your needs. This can involve several interpretations:

- Minimum Loan Amount: This refers to borrowing the least amount of money necessary to acquire a vehicle. Perhaps you have significant savings and only need a small supplement.

- Minimum Down Payment: For many, the hurdle is the initial lump sum. A "minimum car loan" in this context means finding financing with the lowest possible upfront payment, sometimes even zero down.

- Minimum Monthly Payment: This focuses on affordability in your regular budget. It means structuring a loan to have the smallest possible recurring obligation, often achieved through longer loan terms or a lower principal.

- Minimum Credit Score Requirement: This is crucial for individuals with less-than-perfect credit. It’s about finding lenders willing to approve a loan despite a lower credit score, albeit often with different terms.

- Minimum Interest Rate: Ultimately, the goal is to pay as little as possible for the privilege of borrowing. A "minimum car loan" also means securing the lowest possible annual percentage rate (APR) to reduce the total cost of the loan.

Our mission today is to explore each of these facets in depth, providing you with actionable strategies to achieve your ideal minimum car loan.

Key Factors Influencing Your "Minimum Car Loan" Eligibility and Terms

Before diving into strategies, it’s essential to understand the core elements that lenders evaluate. These factors directly impact whether you’re approved, what interest rate you receive, and ultimately, the overall affordability of your car loan.

Your Credit Score: The Financial Report Card

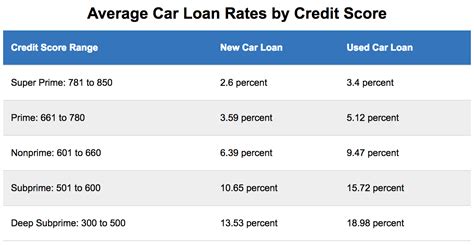

Your credit score is arguably the most significant factor in determining your loan eligibility and interest rate. Lenders use this three-digit number to gauge your creditworthiness – your likelihood of repaying borrowed money. A higher score indicates lower risk, translating to better loan terms, including a lower interest rate.

Based on my experience, scores generally range from 300 to 850. A score above 700 is typically considered good, while excellent credit often surpasses 750. If your score is in the lower ranges, say below 600, you might still qualify for a minimum car loan, but expect higher interest rates to compensate lenders for the increased risk. Understanding your score is the first step in preparing for a car loan application.

Debt-to-Income Ratio (DTI): Your Financial Balance

Your Debt-to-Income (DTI) ratio is a percentage that compares your total monthly debt payments to your gross monthly income. Lenders use DTI to assess your ability to manage additional monthly payments. A lower DTI indicates you have more disposable income to cover new debt, making you a more attractive borrower.

Pro tips from us: Most lenders prefer a DTI ratio of 36% or less, though some might go up to 43% for car loans. If your DTI is high, it signals to lenders that you might be overextended, making it harder to secure a favorable minimum car loan. Reducing existing debt before applying can significantly improve your chances.

Income Stability: A Predictable Foundation

Lenders want to be confident that you have a consistent and reliable source of income to make your monthly car loan payments. This means they will look at your employment history, salary, and how long you’ve been at your current job. Generally, a stable employment history (at least two years with the same employer or in the same field) is preferred.

Proof of income, such as pay stubs, tax returns, or bank statements, will be required. For self-employed individuals, a longer history of consistent income and detailed financial records become even more critical to demonstrate stability.

Loan-to-Value (LTV) Ratio: The Car’s Worth vs. Your Loan

The Loan-to-Value (LTV) ratio compares the amount you want to borrow against the car’s market value. If you’re borrowing more than the car is worth, your LTV is high, which represents a greater risk for the lender. This often happens if you roll negative equity from a previous car into a new loan or if you choose a very small down payment.

A lower LTV, achieved through a larger down payment, signals less risk to the lender. It also means you’re less likely to be "upside down" on your loan (owing more than the car is worth) early in the financing term. This directly impacts your ability to secure a favorable minimum car loan.

Vehicle Type and Age: The Asset’s Influence

The type and age of the vehicle you intend to purchase also play a role. Newer cars, especially those with good resale value, are generally seen as less risky collateral by lenders. This is because they depreciate slower initially and are easier to sell if the borrower defaults.

Used cars can also qualify for excellent rates, but very old or high-mileage vehicles might have shorter loan terms and potentially higher interest rates due to increased risk of mechanical issues and faster depreciation. Lenders want to ensure their collateral retains sufficient value throughout the loan term.

Strategies to Secure the Best "Minimum Car Loan" for You

Now that you understand the influencing factors, let’s explore practical strategies to position yourself for the most advantageous minimum car loan. These are the pro tips that can make a real difference in your car buying journey.

1. Boost Your Credit Score: The Foundation of Favorable Terms

Improving your credit score is perhaps the most impactful step you can take. Even small increases can lead to significantly better interest rates, saving you hundreds or thousands of dollars over the life of the loan.

- Pay Bills On Time, Every Time: Payment history is the biggest component of your credit score. Set up reminders or automatic payments.

- Reduce Existing Debt: Lowering your credit utilization (the amount of credit you’re using compared to your available credit) can quickly boost your score.

- Avoid New Credit Applications: Each new application can cause a small, temporary dip in your score.

- Check Your Credit Report Regularly: Use annualcreditreport.com to get free copies of your reports from Experian, TransUnion, and Equifax. Dispute any errors promptly.

2. Save for a Down Payment: Your Financial Power Play

A larger down payment is a golden ticket to a better minimum car loan. It reduces the amount you need to borrow, lowers your monthly payments, and signals financial responsibility to lenders.

- Lower LTV: A bigger down payment means a lower Loan-to-Value ratio, making you a less risky borrower.

- Reduced Interest Paid: You’re borrowing less, so you’ll pay interest on a smaller principal, reducing the total cost of the loan.

- Avoid Being Upside Down: A substantial down payment helps ensure you don’t owe more than the car is worth, especially in the early years of ownership.

- Potential for Lower Rates: Some lenders offer better rates for borrowers who put down a significant percentage.

Even 10-20% of the car’s purchase price can make a substantial difference.

3. Shop Around for Lenders: Don’t Settle for the First Offer

This is a common mistake to avoid: taking the first loan offer, especially from the dealership. Dealerships are convenient, but they may not always offer the most competitive rates.

- Banks: Your local bank or credit union might offer competitive rates, especially if you have an existing relationship.

- Credit Unions: Often known for lower interest rates and more flexible terms, credit unions are excellent options.

- Online Lenders: Companies like LightStream, Capital One Auto Finance, or Carvana offer streamlined application processes and competitive rates.

- Pre-Approval is Key: Get pre-approved by several lenders before you even step foot in a dealership. This gives you a clear understanding of the best rate you qualify for and empowers you to negotiate confidently.

4. Consider a Shorter Loan Term (If Affordable): Save on Interest

While a longer loan term (e.g., 72 or 84 months) will result in a lower monthly payment, it also means you pay significantly more in interest over the life of the loan.

- Total Cost Savings: A 48- or 60-month loan term, while having higher monthly payments, will drastically reduce the total amount of interest you pay.

- Faster Equity Build-Up: You’ll own your car outright sooner and build equity more quickly.

- Assess Your Budget: Carefully calculate if you can comfortably afford the higher monthly payments of a shorter term. This is a crucial step in finding the true minimum car loan for your financial health.

5. Negotiate the Car Price: Reduce the Principal Before You Borrow

Remember, the car loan amount is directly tied to the price of the car. The lower the purchase price, the less you need to borrow, and the smaller your minimum car loan will be.

- Research Market Value: Use sites like Kelley Blue Book or Edmunds to understand the fair market value of the car you’re interested in.

- Don’t Be Afraid to Haggle: Dealerships expect negotiation. Be firm but polite.

- Separate Negotiations: Try to negotiate the car price before discussing financing. This prevents the dealership from moving numbers around between the car price and the loan terms.

6. Beware of Add-ons: They Inflate Your Loan

Dealerships often offer various add-ons like extended warranties, paint protection, fabric guards, or gap insurance. While some might be beneficial, many are high-profit items for the dealership and can significantly inflate your loan amount.

- Question Everything: Ask what each add-on costs and if it’s truly necessary.

- Do Your Research: You can often purchase extended warranties or gap insurance from third-party providers at a lower cost.

- Stick to Your Budget: Only agree to add-ons that genuinely provide value and fit within your pre-determined budget.

7. Get Pre-Approved: Your Negotiating Power

As mentioned earlier, getting pre-approved for a loan before you visit a dealership is a game-changer. It gives you a strong negotiating position.

- Know Your Rate: You walk into the dealership knowing the best interest rate you qualify for. If the dealership can’t beat it, you already have financing secured.

- Focus on Car Price: With financing handled, you can concentrate solely on negotiating the car’s purchase price, rather than getting distracted by loan terms.

- Time-Saving: The pre-approval process is often quick and can be done online, saving you time at the dealership.

8. Consider a Co-signer: When You Need a Boost

If you have a lower credit score or limited credit history, a co-signer with excellent credit can significantly improve your chances of approval and help you secure a lower interest rate for your minimum car loan.

- Shared Responsibility: Be aware that a co-signer is equally responsible for the loan. If you miss payments, it impacts their credit, too.

- Trust is Key: Only ask someone you trust implicitly and who understands the commitment.

- Not a Permanent Solution: While helpful for initial approval, your goal should be to build your own credit so you won’t need a co-signer in the future.

9. Refinancing: A Future Option for Lower Payments/Rates

Even if you don’t secure the absolute best minimum car loan initially, refinancing is always an option down the line. If your credit score improves or interest rates drop, you could refinance your existing loan for better terms.

- Lower Interest Rate: If your credit has improved, you might qualify for a significantly lower APR.

- Reduced Monthly Payments: A new loan with a lower rate or a longer term (if you need to reduce monthly outflow) can ease budget strain.

- Shorter Loan Term: Conversely, if you want to pay off the car faster, you can refinance to a shorter term.

"Minimum Car Loan" with Challenging Credit: Hope is Not Lost

Based on my experience, one of the biggest misconceptions is that a low credit score means you can’t get a car loan. While it might be more challenging, and the terms won’t be as favorable, it’s certainly possible to secure a minimum car loan even with challenging credit.

Understanding Subprime Loans

Lenders specializing in subprime auto loans cater to individuals with lower credit scores (typically below 620). These loans come with higher interest rates to offset the increased risk.

- Higher APRs: Expect to pay significantly more in interest compared to prime borrowers.

- Stricter Requirements: Lenders might require a larger down payment, a co-signer, or proof of a very stable income.

- Focus on the Future: While the rate might be high, making consistent, on-time payments on a subprime loan can be a powerful way to rebuild your credit.

Secured Loans: Using the Car as Collateral

Almost all car loans are secured loans, meaning the vehicle itself serves as collateral. If you default on the loan, the lender can repossess the car. This inherent security helps lenders approve loans even for higher-risk borrowers.

Building Credit with a Car Loan

A car loan, when managed responsibly, can be an excellent tool for building or rebuilding credit. Consistent, on-time payments demonstrate your reliability to credit bureaus, gradually improving your score.

- Start Small: If possible, consider a more affordable used car to keep the loan amount manageable.

- Make Extra Payments: Even small extra payments can help reduce the principal faster and show good payment behavior.

Pro Tip: For challenging credit, focus on showing income stability, having a reasonable down payment, and keeping your debt-to-income ratio as low as possible. Lenders will look for any positive indicators to offset the credit risk.

Common Mistakes to Avoid When Seeking a "Minimum Car Loan"

As an expert blogger, I’ve observed several pitfalls that often derail people’s efforts to secure the best car loan. Avoiding these can save you a lot of headache and money.

- Not Checking Your Credit Report: Going into a loan application blind is a huge mistake. Always know your score and review your reports for errors.

- Focusing Solely on the Monthly Payment: Dealerships love this. They can extend the loan term or add fees to lower the monthly payment, but it drastically increases the total cost of the loan. Always look at the total amount you’ll pay.

- Not Shopping Around for Lenders: As emphasized, relying on the dealership’s financing without comparing other offers is almost guaranteed to cost you more.

- Ignoring the Total Cost of the Loan: Factor in interest, fees, and any add-ons. The lowest monthly payment isn’t always the cheapest overall.

- Falling for Dealership "Tricks": Be wary of "four-square" negotiations, high-pressure sales tactics, or being rushed through paperwork. Take your time and read everything carefully.

- Not Understanding the Terms: If you don’t understand a term or condition, ask for clarification. Never sign something you don’t fully comprehend.

The Application Process: What to Expect

Once you’ve done your research and prepared your finances, the actual application for a minimum car loan is relatively straightforward.

- Gather Documents: You’ll typically need proof of identity (driver’s license), proof of income (pay stubs, tax returns), proof of residence (utility bill), and sometimes bank statements.

- Fill Out Application: This can be done online, in person at a bank, or at the dealership. It will ask for personal, employment, and financial information.

- Credit Check: The lender will perform a hard inquiry on your credit report. Multiple inquiries for the same type of loan within a short period (usually 14-45 days, depending on the scoring model) are generally counted as a single inquiry, so shopping around won’t hurt your score excessively.

- Review Offer: If approved, the lender will present you with loan terms, including the principal amount, interest rate, term length, and monthly payment.

- Sign & Drive: Once you agree to the terms, you’ll sign the loan documents and can finalize your car purchase.

Pro Tips from Our Team: Navigating Your Car Loan Journey

Based on my years of experience helping individuals navigate complex financial decisions, here are some final pieces of advice for securing your minimum car loan:

- Always Prioritize Your Budget: Before you even look at cars, determine what you can truly afford for a monthly payment, insurance, fuel, and maintenance. Don’t let emotion override your financial reality.

- Think Long-Term: A car loan isn’t just about the next few months. Consider how it fits into your long-term financial goals. Will it hinder other savings or investment plans?

- Don’t Be Afraid to Walk Away: If a deal doesn’t feel right, or you’re being pressured, it’s always okay to walk away. There will always be another car and another loan.

- Consider a Certified Pre-Owned (CPO) Vehicle: CPO cars offer a sweet spot between new and used. They’re often newer models, have undergone rigorous inspections, and come with manufacturer-backed warranties, making them excellent candidates for favorable loan terms.

- Read the Fine Print: Every single word in your loan agreement matters. Understand all fees, prepayment penalties (rare for auto loans but possible), and default clauses.

Conclusion: Your Path to an Optimized Minimum Car Loan

Securing a minimum car loan isn’t about finding the cheapest option; it’s about finding the smartest option that aligns with your financial capacity and goals. By understanding the factors that influence your loan, strategically preparing your finances, and diligently shopping around, you can significantly improve your chances of getting a car loan with the most favorable terms.

From boosting your credit score to understanding the power of a down payment and avoiding common mistakes, every step you take contributes to a more affordable and accessible car ownership experience. Remember, knowledge is power in the world of finance. Equip yourself with the insights from this guide, and embark on your car-buying journey with confidence. Your ideal minimum car loan is within reach – go get it!