Securing Your Ideal Car Loan Right Now: An Expert’s Comprehensive Guide to Navigating Today’s Market

Securing Your Ideal Car Loan Right Now: An Expert’s Comprehensive Guide to Navigating Today’s Market Carloan.Guidemechanic.com

Are you currently in the market for a new set of wheels or looking to refinance your existing auto loan? Understanding the intricacies of securing a car loan right now is more crucial than ever. The automotive and financial landscapes are constantly evolving, presenting both opportunities and challenges for borrowers. This isn’t just about finding the lowest interest rate; it’s about making an informed decision that aligns with your financial health and long-term goals.

As an expert blogger and professional SEO content writer who has meticulously tracked the automotive financing sector for years, I’m here to provide you with a definitive guide. Our goal is to equip you with the knowledge and strategies needed to confidently navigate the current market and secure the best possible car loan right now. This comprehensive article will delve deep into every facet, ensuring you’re empowered to make smart choices.

Securing Your Ideal Car Loan Right Now: An Expert’s Comprehensive Guide to Navigating Today’s Market

Understanding Today’s Car Loan Landscape: What’s Happening "Right Now"?

The current economic climate significantly influences the availability and cost of auto financing. Interest rates, lender policies, and even vehicle inventory all play a role in shaping your loan options. Ignoring these factors can lead to missed opportunities or, worse, a less favorable loan agreement.

Interest rates are perhaps the most immediate concern for anyone seeking a car loan right now. They fluctuate based on the broader economic environment, central bank policies, and inflation. While we’ve seen periods of historically low rates, the market can shift rapidly. It’s essential to check current average rates from multiple sources to establish a benchmark for comparison. This will help you identify a truly competitive offer.

Beyond rates, lender appetites vary. Some lenders might be tightening their credit criteria, making approval slightly harder, especially for those with lower credit scores. Others might be aggressively competing for business, offering incentives or more flexible terms. Being aware of these dynamics puts you in a stronger negotiating position.

Are You Truly Ready for a Car Loan Right Now? A Critical Self-Assessment

Before you even begin shopping for a vehicle or a loan, it’s vital to conduct an honest self-assessment of your financial readiness. Rushing into a loan without proper preparation is a common pitfall that can lead to long-term financial strain. Based on my experience, this preliminary step is often overlooked but incredibly impactful.

First, evaluate your budget. How much can you realistically afford for a monthly car payment, factoring in insurance, fuel, maintenance, and potential depreciation? A good rule of thumb is that your total vehicle expenses (loan payment, insurance, gas) shouldn’t exceed 15-20% of your net monthly income. Don’t forget to consider unexpected repairs, which can quickly add up.

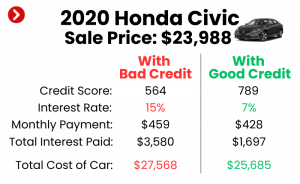

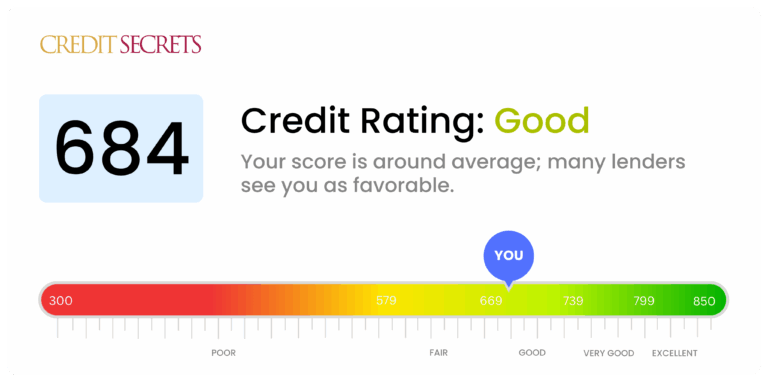

Next, examine your credit score. This three-digit number is arguably the most critical factor in determining the interest rate you’ll be offered. Lenders use it to assess your creditworthiness. A higher score typically translates to lower interest rates and better terms. If your score isn’t where you’d like it to be, taking steps to improve it before applying for a car loan right now can save you thousands over the life of the loan.

Finally, consider your down payment and trade-in. A substantial down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid. If you have an existing vehicle to trade in, its value can effectively act as a down payment, further sweetening your deal.

The Application Process: Your Step-by-Step Guide to Securing a Car Loan

Navigating the car loan application process can feel daunting, but by breaking it down into manageable steps, you can approach it with confidence. This systematic approach increases your chances of approval and helps you secure the most favorable terms for your car loan right now.

1. Gather Your Documents:

Preparation is key. Lenders will require several documents to verify your identity, income, and financial stability. Common requirements include:

- Government-issued ID (driver’s license).

- Proof of income (pay stubs, tax returns, bank statements).

- Proof of residence (utility bill, lease agreement).

- Social Security number.

- Vehicle information (if you’ve already chosen one).

Having these documents organized and readily available will streamline the application process and prevent unnecessary delays.

2. Check Your Credit Score and Report:

As mentioned, your credit score is paramount. Obtain a copy of your credit report from all three major bureaus (Experian, Equifax, TransUnion) and review them for inaccuracies. Disputing errors can quickly boost your score. Knowing your score beforehand also gives you a realistic expectation of the rates you qualify for.

3. Get Pre-Approved Before You Shop:

This is a pro tip from us that can dramatically change your car-buying experience. Seeking pre-approval from multiple lenders (banks, credit unions, online lenders) before visiting a dealership offers several advantages. It gives you a clear understanding of how much you can borrow and at what interest rate, effectively setting your budget. This empowers you to negotiate the car’s price based on cash, rather than being swayed by monthly payment figures from the dealer.

4. Compare Loan Offers:

Don’t settle for the first offer you receive. Use your pre-approval offers as leverage to compare terms. Look beyond just the interest rate; consider the loan term (number of months), any fees, and prepayment penalties. A slightly higher interest rate over a shorter term might result in less overall interest paid than a lower rate over a much longer term.

5. Understand the Fine Print and Negotiate:

Once you have an offer you like, read every line of the loan agreement. Ask questions about anything you don’t understand. Can you make extra payments without penalty? What happens if you miss a payment? Based on my experience, many borrowers overlook this crucial step, only to discover unfavorable terms later. Don’t hesitate to negotiate. Even a quarter-point reduction in the interest rate can save you hundreds over the life of the loan.

Exploring Types of Car Loans "Right Now": New, Used, and Refinancing

The term "car loan right now" isn’t a one-size-fits-all concept. Your specific needs and the type of vehicle you’re interested in will dictate the kind of loan you pursue. Let’s break down the common options available today.

New Car Loans:

These are typically offered for vehicles purchased directly from a dealership that have never been previously titled. New car loans often come with the lowest interest rates due to the vehicle’s higher value and lower depreciation risk for the lender. Manufacturers sometimes offer special financing deals, like 0% APR for qualified buyers, to move new inventory. However, new cars depreciate rapidly, meaning you might owe more than the car is worth in the early years of the loan.

Used Car Loans:

For those opting for pre-owned vehicles, used car loans are the answer. While interest rates for used cars are generally higher than for new cars, the overall cost of the vehicle is significantly lower. Lenders often have stricter criteria for used car loans, sometimes limiting the age or mileage of the vehicle they’re willing to finance. It’s crucial to get a pre-purchase inspection for any used car to avoid hidden issues that could lead to costly repairs down the line.

Refinancing Your Existing Car Loan:

Many people overlook the opportunity to refinance their current auto loan. If interest rates have dropped since you originally financed your car, or if your credit score has significantly improved, refinancing can be a smart move. This involves taking out a new loan to pay off your existing one, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payment, lower the total interest paid, or shorten your loan term. It’s an excellent strategy to consider if you’re looking to optimize your car loan right now.

Leasing vs. Buying (Brief Context):

While not strictly a loan, leasing is another popular option for acquiring a vehicle. Leasing typically involves lower monthly payments and allows you to drive a new car every few years. However, you don’t own the vehicle, and there are mileage limits and potential wear-and-tear charges. Buying, on the other hand, means you own the car outright once the loan is paid off, offering long-term equity. Your decision depends on your financial situation and driving habits.

Navigating Challenges: Bad Credit Car Loans "Right Now"

Having a less-than-perfect credit score doesn’t mean you can’t get a car loan right now. While it might be more challenging and result in higher interest rates, options are available. The key is to approach these situations strategically and avoid predatory lenders.

Strategies for Securing a Bad Credit Car Loan:

- Larger Down Payment: This reduces the lender’s risk and shows your commitment, making them more willing to approve your loan.

- Co-signer: A trusted individual with good credit can co-sign your loan, making you more attractive to lenders. Be aware that the co-signer is equally responsible for the debt.

- Secured Loan: Some lenders offer secured auto loans, where the car itself acts as collateral. While these might have lower rates, failing to make payments can result in repossession.

- Credit Unions: Often more flexible than traditional banks, credit unions may be more willing to work with members who have lower credit scores, sometimes offering better rates.

- Specialty Lenders: There are lenders who specialize in bad credit auto loans. While convenient, their interest rates can be significantly higher, so compare offers carefully.

Common Mistakes to Avoid:

Based on my experience, a common mistake is only applying to one dealership’s financing department. This limits your options and can lead to accepting a high-interest loan out of desperation. Another error is not understanding the total cost of the loan, focusing solely on the monthly payment. Always ask for the total interest you’ll pay over the loan’s term.

Pro tips from us: Be wary of "buy here, pay here" dealerships that offer easy approval but often come with extremely high interest rates and unfavorable terms. Always seek transparent terms and compare at least three different offers before committing. Improving your credit score, even slightly, before applying can significantly impact your loan terms.

Pro Tips for Securing the Best Car Loan "Right Now"

To truly optimize your chances of getting an excellent car loan right now, adopt these expert strategies. These insights come from years of analyzing market trends and helping individuals navigate complex financial decisions.

-

Boost Your Credit Score (Even a Little):

Before you even think about applying, take steps to improve your credit. Pay down existing debts, especially high-interest credit card balances. Make sure all your bill payments are on time. Even a 20-point increase in your score can move you into a better rate tier, saving you hundreds or even thousands. -

Shop Around Aggressively for Lenders:

Do not limit yourself to the dealership’s financing office. While convenient, it might not offer the most competitive rates. Apply for pre-approval with at least three different lenders: your personal bank, a local credit union, and a reputable online lender. This competitive environment forces lenders to offer their best terms. -

Understand the Full Cost, Not Just the Monthly Payment:

A common tactic is to focus on a "manageable" monthly payment. However, a low monthly payment often comes with a longer loan term and a much higher total interest paid. Always ask for the total cost of the loan over its entire duration. A shorter term with a slightly higher monthly payment can be more financially sound in the long run. -

Be Prepared for Negotiation:

Everything is negotiable, from the car’s price to the loan’s interest rate. If you have a pre-approval in hand, use it as leverage. Don’t be afraid to walk away if the terms aren’t favorable. Your patience can pay off. -

Consider a Shorter Loan Term:

While a longer loan term means lower monthly payments, it also means you pay more in interest over time and stay "upside down" (owing more than the car is worth) for longer. If your budget allows, opt for the shortest term you can comfortably afford. -

Avoid Unnecessary Add-ons:

Dealerships often try to sell extended warranties, GAP insurance (which can be beneficial but should be priced competitively), and other add-ons. Carefully evaluate if you truly need these, as they significantly increase the total amount financed and, consequently, your interest payments.

The Future of Car Loans: What to Watch Out For

The landscape of automotive financing is always shifting, and understanding potential future trends can help you make even smarter decisions about a car loan right now.

The rise of electric vehicles (EVs) is a significant factor. As more consumers transition to EVs, lenders are adapting their loan products. Some might offer preferential rates for eco-friendly vehicles, while others might adjust their depreciation models, which could impact residual values and, consequently, loan terms.

Digital lending platforms are also gaining traction. Online lenders offer speed and convenience, often with competitive rates due to lower overheads. This trend will likely continue, making it even easier to compare and secure a loan from the comfort of your home. Keeping an eye on these innovations ensures you’re always leveraging the most efficient ways to finance your vehicle.

For more detailed insights into managing your finances and making informed vehicle purchasing decisions, you might find our article on extremely helpful. Understanding your overall financial picture is paramount.

Conclusion: Empowering Your Car Loan Decision "Right Now"

Securing the best car loan right now is a nuanced process that requires careful planning, diligent research, and strategic execution. It’s more than just finding a vehicle; it’s about making a sound financial decision that contributes positively to your long-term economic well-being. By understanding the current market, assessing your readiness, navigating the application process, exploring various loan types, and leveraging expert tips, you can confidently secure financing that meets your needs.

Remember, the goal isn’t just to get approved, but to get approved on your terms. Take the time to prepare, compare offers from multiple lenders, and read every line of the agreement. Your informed approach will undoubtedly lead to a more favorable outcome. For up-to-date economic insights that might influence interest rates, we recommend consulting reliable sources like the Federal Reserve’s official website: https://www.federalreserve.gov/.

Armed with this comprehensive guide, you are now well-equipped to make intelligent decisions regarding your car loan right now. Drive away with confidence, knowing you’ve secured the best deal possible. And if you’re ever considering refinancing or adjusting your current loan, remember that continuous financial health check-ups are always a good idea. Consider reviewing our guide on for future reference.