Should I Take Out a Loan for a Car? Navigating Your Auto Financing Options

Should I Take Out a Loan for a Car? Navigating Your Auto Financing Options Carloan.Guidemechanic.com

Buying a car is a significant milestone for many, offering unparalleled freedom and convenience. Yet, the path to vehicle ownership often leads to a crossroads: should you pay cash, or should you take out a loan for a car? This isn’t just a simple financial transaction; it’s a decision that impacts your budget, your credit, and your future financial flexibility for years to come.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals grapple with this exact question. The answer isn’t a one-size-fits-all solution. It depends entirely on your personal financial situation, your lifestyle needs, and your long-term goals. In this comprehensive guide, we’ll dive deep into the world of auto financing, equipping you with the knowledge to make the most informed decision possible.

Should I Take Out a Loan for a Car? Navigating Your Auto Financing Options

The Big Question: Is a Car Loan Right for You?

At its core, taking out a car loan means borrowing money from a lender to purchase a vehicle, agreeing to repay the borrowed amount, plus interest, over a set period. For many, it’s the most practical way to acquire a car, especially when a significant upfront cash payment isn’t feasible. However, it’s crucial to weigh the advantages against the potential drawbacks before committing.

Based on my experience in personal finance, understanding the full scope of a car loan goes beyond just the monthly payment. It involves evaluating the total cost of ownership, including interest, insurance, maintenance, and fuel. Let’s break down the pros and cons to give you a clearer picture.

The Advantages of Taking Out a Car Loan

For many prospective car owners, a loan offers several compelling benefits that make vehicle ownership attainable and even financially strategic.

1. Accessibility to a Vehicle

Perhaps the most immediate benefit of an auto loan is that it makes purchasing a car accessible to a wider range of people. Most individuals don’t have tens of thousands of dollars sitting in their bank account, ready to be spent on a car. A loan bridges this gap, allowing you to acquire a reliable vehicle without depleting your savings.

This accessibility is particularly important for those who need a car for work, family responsibilities, or simply to improve their quality of life. Without a loan, many would be limited to older, potentially less reliable vehicles, or no vehicle at all.

2. Opportunity to Build or Improve Credit History

Responsible management of a car loan can be a powerful tool for building or improving your credit score. When you consistently make on-time payments, you demonstrate financial responsibility to credit bureaus. This positive payment history is a significant factor in your credit score calculation.

A good credit score, in turn, can open doors to better interest rates on future loans, whether it’s for a mortgage, another car, or even personal loans. It’s a stepping stone towards a stronger financial future, proving your reliability as a borrower.

3. Preserving Your Cash for Other Investments or Emergencies

Committing all your available cash to a car purchase can leave you financially vulnerable. By taking out a loan, you can preserve your liquid assets for other important uses. This might include maintaining an emergency fund, making a down payment on a home, or investing in opportunities that offer a higher return than the interest paid on your car loan.

Having an emergency fund is crucial for financial security, protecting you from unexpected expenses like medical bills or job loss. A car loan allows you to keep this safety net intact, providing peace of mind.

4. Driving a Newer, More Reliable Vehicle

Financing often allows you to afford a newer, more reliable vehicle than you could purchase outright with cash. Newer cars typically come with better safety features, advanced technology, and often, a manufacturer’s warranty. This warranty can save you money on unexpected repairs during the initial years of ownership.

While depreciation is a factor, the enhanced reliability and lower immediate maintenance costs of a newer vehicle can be a significant advantage. This can reduce stress and offer a more comfortable, safer driving experience.

The Disadvantages of Taking Out a Car Loan

Despite the benefits, taking out a car loan also comes with notable drawbacks that should be carefully considered. Ignoring these can lead to financial strain down the road.

1. Interest Costs Increase the Total Price

The most apparent downside of a car loan is the interest you’ll pay over the life of the loan. This interest is essentially the cost of borrowing money, and it adds significantly to the overall price of the vehicle. A car that costs $25,000 might end up costing you $28,000 or more after interest, depending on your interest rate and loan term.

It’s crucial to understand that the advertised price of the car is not the final price when financing. Always factor in the total amount you will pay, including all interest and fees.

2. Depreciation: A Rapid Loss of Value

Cars are notoriously depreciating assets, meaning their value decreases significantly over time, especially in the first few years. A new car can lose 20-30% of its value in the first year alone. When you finance a car, you’re paying interest on an asset that is constantly losing value.

This rapid depreciation can lead to a situation known as "negative equity" or being "upside down" on your loan. This means you owe more on the car than it’s currently worth, which can be problematic if you need to sell or trade in the vehicle before the loan is paid off.

3. Long-Term Debt Commitment

A car loan represents a long-term financial commitment, often spanning three to seven years. This means you’ll have a fixed monthly payment that needs to be factored into your budget for an extended period. This commitment can limit your financial flexibility, making it harder to save for other goals or respond to unexpected financial challenges.

Before taking on this debt, consider how it will impact your ability to save for a down payment on a house, fund your retirement, or simply enjoy discretionary spending. It’s a significant slice of your monthly income.

4. Risk of Negative Equity

As mentioned, negative equity occurs when the outstanding balance on your car loan is higher than the car’s current market value. This is a common issue, particularly with new cars that depreciate quickly. If your car is totaled in an accident or stolen, your insurance payout might not cover the full loan amount, leaving you to pay the difference out of pocket.

This risk highlights the importance of gap insurance, which covers the difference between what you owe and what your car is worth if it’s totaled or stolen. However, gap insurance is an additional cost.

5. Impact on Future Financial Flexibility

Having a car loan payment each month can constrain your ability to make other financial decisions. It might prevent you from taking a lower-paying job you’re passionate about, moving to a new city, or taking a sabbatical. Your monthly budget becomes less flexible, as a significant portion is already allocated to debt repayment.

Consider how this regular payment might affect your overall financial well-being and freedom. It’s not just about affording the payment today, but also about future financial opportunities.

Key Factors to Consider Before Applying for a Car Loan

Before you even start looking at car models, it’s essential to perform a thorough financial self-assessment. This preparation will empower you to secure the best possible loan terms and ensure your car purchase is sustainable.

1. Your Financial Health

Your personal financial standing is the bedrock upon which any loan decision should be made.

Your Credit Score: The Gateway to Better Rates

Your credit score is arguably the single most important factor determining the interest rate you’ll be offered on a car loan. Lenders use your score to assess your creditworthiness and the risk they’re taking by lending to you. A higher credit score (generally above 700) typically qualifies you for lower interest rates, saving you hundreds or even thousands of dollars over the life of the loan.

Pro tip from us: Check your credit score and report well before you apply for a loan. This allows you time to correct any errors and understand your financial standing. If your score is low, consider taking steps to improve it, such as paying down existing debts or making all payments on time, before applying. For a deeper dive, you might find our guide on Understanding Your Credit Score: A Comprehensive Guide helpful.

Budgeting and Affordability: Beyond the Monthly Payment

Many people focus solely on the monthly car payment, but a truly affordable car encompasses much more. You must consider the total cost of ownership, which includes:

- Monthly Loan Payment: Principal and interest.

- Car Insurance: Rates vary widely based on the car, your driving history, and location.

- Fuel Costs: Depending on mileage and car’s efficiency.

- Maintenance and Repairs: Oil changes, tires, unexpected breakdowns.

- Registration and Taxes: Annual fees.

Common mistakes to avoid are underestimating these additional costs. A seemingly affordable monthly payment can quickly become a financial burden when these other expenses are factored in. Create a detailed budget to ensure you can comfortably manage all these costs without stretching your finances too thin.

Down Payment: Your Head Start

Making a substantial down payment on a car loan offers several significant advantages. Firstly, it reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest paid over the loan term. Secondly, a larger down payment helps mitigate the risk of negative equity, as you start with more equity in the vehicle.

Lenders also view larger down payments favorably, as it demonstrates your commitment and reduces their risk. This can sometimes lead to better loan terms. Aim for at least 10-20% of the car’s purchase price as a down payment, if possible.

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio is a crucial metric lenders use to assess your ability to manage monthly payments and repay debts. It’s calculated by dividing your total monthly debt payments by your gross monthly income. A lower DTI indicates you have more disposable income available, making you a less risky borrower.

Most lenders prefer a DTI of 36% or less, though some might go higher. Understanding your DTI helps you gauge how much additional debt you can realistically take on without overextending yourself.

2. The Car Itself

The type of car you choose profoundly impacts your loan terms and overall financial commitment.

New vs. Used: The Depreciation Dilemma

Deciding between a new or used car is a pivotal choice. New cars offer the latest technology, better fuel efficiency, and a full warranty, but they also depreciate the fastest. This rapid depreciation means you’re paying more for an asset that quickly loses value, increasing the risk of negative equity.

Used cars, while potentially lacking some features or having a shorter warranty, have already undergone their steepest depreciation. This means you often get more car for your money, and the loan amount (and thus interest) is typically lower. However, older used cars might incur higher maintenance costs.

Reliability and Maintenance Costs

Beyond the purchase price, consider the long-term reliability and projected maintenance costs of the specific car model you’re interested in. Some brands and models are known for their reliability and lower repair costs, while others can be notorious money pits. Research consumer reports and reliability ratings.

Higher maintenance costs can negate the savings from a lower purchase price or interest rate. Factor these potential expenses into your overall budget.

3. Understanding Loan Terms

The terms of your car loan are just as important as the car’s price.

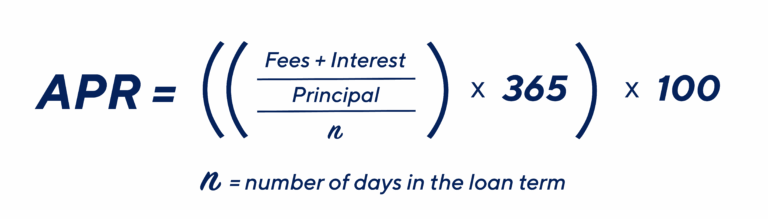

Interest Rate (APR): The True Cost of Borrowing

The Annual Percentage Rate (APR) is the total cost of borrowing money, expressed as a yearly percentage. It includes the interest rate plus any fees charged by the lender. A lower APR means lower monthly payments and less money paid over the life of the loan. This is where your credit score plays a significant role.

Always compare APRs, not just interest rates, when shopping for loans. Even a seemingly small difference in APR can translate to hundreds or thousands of dollars saved over the loan term.

Loan Term Length: Short-Term Pain vs. Long-Term Gain

The loan term refers to the length of time you have to repay the loan, typically ranging from 36 to 84 months. A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term results in lower monthly payments, making the car seem more affordable, but you’ll pay significantly more in interest over the life of the loan.

Based on my experience: While longer terms offer lower monthly payments, they often lead to negative equity for a longer period and a much higher total cost. Opt for the shortest loan term you can comfortably afford to minimize interest expenses.

Fees and Charges: Read the Fine Print

Car loans often come with various fees, such as origination fees, documentation fees, and pre-payment penalties. These can add to the overall cost of your loan. Always ask for a full breakdown of all fees associated with the loan.

Be particularly wary of pre-payment penalties, which charge you for paying off your loan early. Ideally, choose a loan without such penalties, allowing you the flexibility to accelerate payments if your financial situation improves.

4. Alternatives to Car Loans

It’s always wise to explore all your options before committing to a loan.

Paying with Cash: The Ideal Scenario

If you have enough cash saved to purchase a car outright without jeopardizing your emergency fund or other critical financial goals, this is often the most financially advantageous option. Paying with cash eliminates interest payments entirely, saving you a substantial amount of money. It also means you own the car free and clear from day one, with no monthly payments or debt burden.

This option offers complete financial freedom and simplicity. However, ensure you’re not depleting your emergency savings to do so.

Leasing a Car: A Different Form of Ownership

Leasing is essentially long-term renting. You make monthly payments for the use of a vehicle for a set period (typically 2-4 years) and mileage limit. At the end of the lease, you return the car or have the option to buy it. Leasing usually results in lower monthly payments than financing, and you always drive a new car under warranty.

However, you don’t own the asset, have mileage restrictions, and may face wear-and-tear charges. It’s suitable for those who like to drive new cars frequently and have predictable driving habits.

Public Transportation or Ridesharing: A Viable Option?

For some, especially those living in urban areas with robust public transport networks, owning a car might not be a necessity. Relying on public transportation, cycling, or ridesharing services like Uber or Lyft can be significantly cheaper than car ownership, especially when you factor in all the associated costs (payments, insurance, fuel, maintenance).

Consider your daily commute, lifestyle, and local infrastructure to determine if these alternatives are viable for you.

Buying a Much Cheaper Car Outright: The Frugal Approach

If a new or even a late-model used car is out of your budget, consider buying a much cheaper, older, but reliable used car with cash. While it might not have all the bells and whistles, it provides transportation without the burden of monthly payments and interest. This approach allows you to save money that would otherwise go towards a loan, potentially enabling you to save for a better car down the line.

This option emphasizes practicality and financial prudence over luxury.

The Application Process: What to Expect

Once you’ve decided that a car loan is the right path for you, understanding the application process will help you navigate it smoothly and confidently.

Gathering Your Documents

Before approaching lenders, ensure you have all necessary documents ready. This typically includes:

- Proof of identity (Driver’s license, passport)

- Proof of income (Pay stubs, tax returns, employment verification)

- Proof of residency (Utility bills, lease agreement)

- Bank statements

- Social Security Number

Having these documents organized and accessible will streamline the application process and prevent delays.

Shopping for Lenders: Don’t Settle for the First Offer

This is a critical step that many car buyers overlook. Don’t just accept the financing offered by the dealership. Shop around for the best interest rates and terms from various lenders, including:

- Banks: Traditional financial institutions often offer competitive rates.

- Credit Unions: Member-owned, non-profit institutions known for generally lower interest rates and fees.

- Online Lenders: Many reputable online platforms specialize in auto loans and can offer quick approvals and competitive rates.

Pro tips from us: Apply for pre-approval from a few different lenders within a short timeframe (usually 14-45 days, depending on the credit scoring model). This counts as a single hard inquiry on your credit report, minimizing the impact on your score while allowing you to compare offers.

Pre-Approval vs. On-the-Spot Financing

Getting pre-approved for a loan before you visit the dealership puts you in a much stronger negotiating position. You’ll know exactly how much you can afford and what interest rate you qualify for, allowing you to focus on the car’s price. Dealers are often more willing to negotiate on the car’s price when they know you have your financing secured.

On-the-spot financing at a dealership can be convenient, but it doesn’t always offer the best rates. Dealerships work with a network of lenders and may mark up the interest rate to earn a profit. Use your pre-approved offer as leverage to ensure you’re getting a competitive rate from the dealership’s financing options.

Reading the Fine Print: No Surprises

Before signing any loan agreement, read every single line of the contract carefully. Ensure you understand:

- The exact interest rate (APR).

- The total loan amount.

- The monthly payment.

- The loan term.

- Any additional fees or charges.

- Pre-payment penalties, if any.

If anything is unclear, ask questions until you fully understand. Do not feel pressured to sign anything until you are completely comfortable with all the terms.

Pro Tips for a Smart Car Loan Decision (E-E-A-T)

Having guided countless individuals through complex financial decisions, I’ve compiled some essential tips to help you make the smartest possible car loan choice.

1. Shop Around for Rates, Not Just Cars

As mentioned, securing the best interest rate is paramount. Don’t let the excitement of finding the perfect car overshadow the importance of finding the perfect loan. The difference of just a few percentage points in your APR can save you hundreds or even thousands of dollars over the loan’s lifetime.

Always get multiple pre-approvals and use them as bargaining chips. This empowers you, the buyer, to dictate terms rather than simply accepting what’s offered.

2. Negotiate the Car Price First, Then the Loan

One common mistake to avoid is discussing financing before settling on the car’s purchase price. When you combine these two negotiations, it becomes difficult to determine if you’re getting a good deal on the car or the loan. Dealerships might manipulate one to make the other seem more attractive.

Negotiate the car’s out-the-door price as if you were paying cash. Once that’s finalized, then discuss your financing options, comparing them against your pre-approved offers.

3. Understand the Total Cost, Not Just Monthly Payments

We’ve touched on this, but it bears repeating: fixate on the total amount you will pay over the life of the loan, not just the attractive monthly payment. A lower monthly payment over a longer term often means a significantly higher total cost due to increased interest.

Use online car loan calculators to visualize the impact of different interest rates and loan terms on your total outlay. This transparency will help you make a more financially sound decision.

4. Avoid Unnecessary Add-Ons and Extended Warranties

Dealerships often push various add-ons, such as extended warranties, paint protection, fabric protection, and VIN etching. While some might seem appealing, they significantly increase the total amount financed and, consequently, the interest you pay.

Based on my experience: Most extended warranties offered at dealerships are overpriced and often have limitations. Research third-party warranties if you truly feel you need one, or simply set aside money in a savings account for potential repairs. Say "no" firmly to anything you don’t genuinely need or understand.

5. Consider Refinancing Your Loan

If your credit score improves significantly after taking out a car loan, or if interest rates drop, you might be able to refinance your existing loan. Refinancing means taking out a new loan to pay off your current one, ideally at a lower interest rate or with more favorable terms.

This can lead to lower monthly payments or a reduced total interest paid. Keep an eye on market rates and your credit score; refinancing can be a smart move to save money.

When NOT to Take Out a Car Loan

While a car loan can be a valuable tool, there are specific situations where taking one out is ill-advised and could lead to significant financial hardship.

1. When You Have a Poor Credit Score

If your credit score is low, you’ll likely only qualify for loans with very high interest rates. These rates can make the car purchase incredibly expensive, often leading to payments that are difficult to manage. It might be wiser to delay your purchase, focus on improving your credit score, and save up for a larger down payment.

Paying excessive interest is a waste of money that could be better used elsewhere.

2. When You Have Unstable Income

A car loan requires consistent, predictable monthly payments for several years. If your income is unstable, irregular, or you’re facing job insecurity, taking on a long-term debt commitment can be incredibly risky. Missed payments will damage your credit score and could lead to vehicle repossession.

Prioritize financial stability before taking on such a significant recurring expense.

3. When You Already Have High Debt

If your current debt load (credit cards, student loans, personal loans) is already high, adding a car loan could push you into an unsustainable financial position. Your debt-to-income ratio will skyrocket, making it difficult to manage all your obligations. This can create a cycle of debt that is hard to break.

Address your existing debt first. Once your DTI is at a healthier level, then reconsider a car loan. For help with managing existing debt, check out our article on Budgeting for a New Car: Beyond the Monthly Payment.

4. When You’re Buying a Depreciating Asset You Can’t Truly Afford

Sometimes, the desire for a specific car can cloud financial judgment. If you’re stretching your budget to the absolute limit for a car that will rapidly lose value, you’re setting yourself up for potential financial distress. This is particularly true if you’re taking out a very long loan term (e.g., 72 or 84 months) just to make the monthly payment "affordable."

It’s better to buy a more modest car that truly fits your budget, even if it means compromising on some features. Remember, a car is primarily a tool for transportation, not an investment.

Making the Right Decision for YOU

The decision to take out a car loan is deeply personal and depends on a complex interplay of your financial health, your needs, and your willingness to manage debt. There’s no universal right or wrong answer. What’s crucial is making an informed choice that aligns with your financial goals and capabilities.

We’ve explored the myriad factors, from the benefits of building credit to the pitfalls of depreciation and high interest. We’ve also armed you with practical tips, drawn from years of experience, to navigate the lending landscape. The most important takeaway is to do your homework, understand all the costs involved, and never rush into a decision.

Ultimately, whether you should take out a loan for a car boils down to a thorough assessment of your financial situation, a careful comparison of loan offers, and a clear understanding of the long-term commitment. By following the advice in this guide, you can confidently drive towards a smart and sustainable car ownership experience. Make a choice that empowers your financial future, not one that burdens it.