Should You Apply For A Car Loan Before Visiting a Dealership? The Ultimate Pre-Approval Guide

Should You Apply For A Car Loan Before Visiting a Dealership? The Ultimate Pre-Approval Guide Carloan.Guidemechanic.com

The scent of a new car, the thrill of cruising in a different ride – buying a vehicle is an exciting milestone. Yet, for many, the joy quickly turns into apprehension when it comes to financing. The question often arises: "Should I apply for a car loan before I even step foot into a dealership?" This isn’t just a minor detail; it’s a pivotal decision that can profoundly impact your entire car-buying experience, from the price you pay to the stress you endure.

Navigating the world of auto financing can feel like a labyrinth, with dealerships, banks, and credit unions all vying for your business. Many prospective buyers make the common mistake of walking onto a car lot without a clear financial strategy, leaving themselves vulnerable to high-pressure sales tactics and potentially unfavorable loan terms. This comprehensive guide is designed to empower you with the knowledge and confidence to make the best financial choices, ensuring you drive away happy and financially secure. We’ll dive deep into the ‘why’ and ‘how’ of preparing your finances before you start car shopping, transforming you from a reactive buyer into a proactive, informed negotiator.

Should You Apply For A Car Loan Before Visiting a Dealership? The Ultimate Pre-Approval Guide

The Core Question: Should You Apply for a Car Loan Before Visiting the Dealership?

The short answer is a resounding yes. Applying for and securing a car loan pre-approval before you set foot in a dealership is one of the smartest moves you can make. It fundamentally shifts the power dynamic from the seller to you, the buyer. This single action can save you thousands of dollars, countless hours, and a significant amount of stress.

Why Pre-Approval is Your Secret Weapon

Pre-approval is not a commitment to a specific loan or lender; rather, it’s an offer from a financial institution (like a bank or credit union) stating that they are willing to lend you a certain amount of money at a specific interest rate, based on your creditworthiness. Think of it as having cash in your pocket, even if it’s just a promise of cash.

Based on my experience, walking into a dealership with a pre-approval letter transforms your entire car-buying journey. You’re no longer a shopper hoping to be approved; you’re a qualified buyer with a defined budget. This clarity allows you to focus solely on negotiating the vehicle’s price, rather than being distracted by the complexities of financing.

The benefits extend far beyond just knowing your budget. A pre-approval provides you with a benchmark interest rate, which is incredibly powerful. When the dealership offers their financing, you already know if their terms are competitive or if they’re trying to upsell you on a higher rate. It empowers you to either accept a better offer from the dealer or confidently stick with your pre-approved loan.

Dealer Financing vs. Independent Lender: A Crucial Distinction

When you arrive at a dealership without pre-approval, you’re essentially putting all your eggs in one basket. The dealer will likely offer to arrange financing for you through their network of lenders. While this can sometimes yield a good rate, it often comes with a significant markup that benefits the dealership, not you. They are, after all, in the business of selling cars and financing.

The crucial distinction lies in whose best interest is being served. An independent lender (your bank, credit union, or an online lender) works directly with you. Their goal is to offer you the best rate they can based on your financial profile. A dealership, however, is motivated by profit from both the car sale and the financing package. Your pre-approval acts as a formidable counter-offer, ensuring you don’t get taken advantage of. It provides a non-negotiable floor for your interest rate.

Essential Steps Before Even Thinking About an Application

Before you even consider filling out a loan application, whether for pre-approval or a direct loan, there are several foundational steps you absolutely must take. Skipping these can lead to applying for a car loan before you’re truly ready, resulting in higher interest rates or even outright rejection. Preparation here is not just an advantage; it’s a necessity.

Know Thyself (and Thy Wallet): Budgeting for Your Dream Ride

Buying a car involves much more than just the monthly loan payment. Many first-time buyers, and even some seasoned ones, overlook the true cost of vehicle ownership. This oversight can quickly lead to financial strain and buyer’s remorse.

Beyond the principal and interest of your car loan, you need to factor in insurance premiums, which can vary wildly based on the car’s make, model, and your driving history. Fuel costs are another ongoing expense, as is routine maintenance like oil changes, tire rotations, and unexpected repairs. Don’t forget registration fees, taxes, and potential parking costs. A good rule of thumb is the 20/4/10 rule: put down at least 20%, finance the car for no more than four years, and your total monthly car expenses (payment, insurance, fuel) should not exceed 10% of your gross monthly income. Pro tips from us: create a detailed spreadsheet to itemize all potential costs. This holistic view will give you a realistic picture of what you can truly afford, ensuring your dream car doesn’t become a financial nightmare.

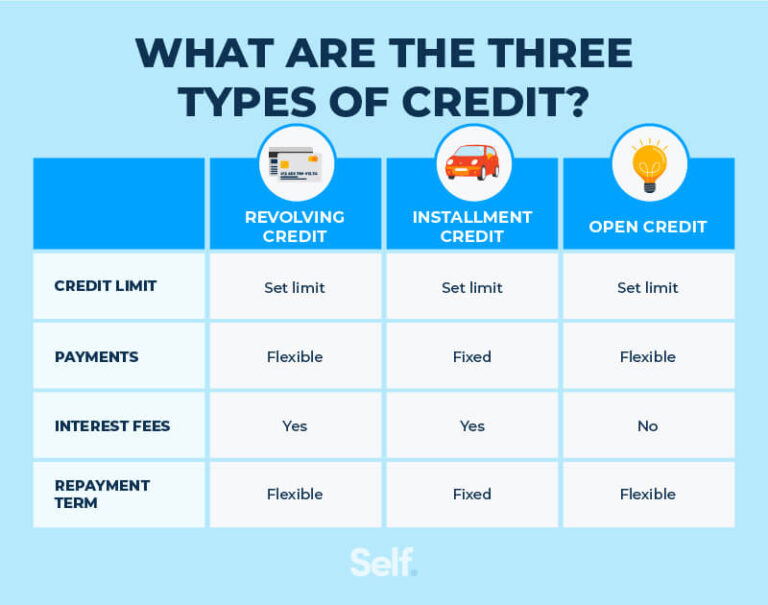

Your Credit Score: The Ultimate Game Changer

Your credit score is arguably the single most important factor determining the interest rate you’ll be offered on a car loan. Lenders use this three-digit number to assess your creditworthiness – essentially, how risky it is to lend you money. A higher score typically means a lower interest rate, which translates into significant savings over the life of the loan.

Before applying for a car loan before, it is imperative to check your credit score. You can obtain a free copy of your credit report from each of the three major credit bureaus (Experian, Equifax, and TransUnion) once every 12 months. Services like AnnualCreditReport.com allow you to do this. Be aware of the difference between a "soft pull" and a "hard pull" on your credit. Checking your own score is a soft pull and won’t affect it, whereas a loan application is a hard pull and can temporarily lower your score by a few points.

Common mistakes to avoid are not knowing your score until you’re already at the dealership, or worse, finding errors on your report that could be dragging your score down. If your score isn’t where you want it to be, take steps to improve it. Pay down existing debts, especially credit card balances, and ensure all your bills are paid on time. Dispute any inaccuracies on your credit report immediately. Even a small improvement in your score can lead to a substantially better interest rate, saving you hundreds or even thousands of dollars. For more detailed information on understanding and improving your credit, consider visiting trusted resources like Experian.com.

The Power of the Down Payment

While it might seem tempting to finance the entire cost of a car, making a substantial down payment offers numerous benefits that can significantly improve your financial standing. A larger down payment immediately reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Furthermore, a down payment provides you with instant equity in the vehicle. Cars depreciate rapidly the moment they leave the lot, and a significant down payment helps mitigate the risk of being "upside down" on your loan – owing more than the car is worth. Lenders also view borrowers with a larger down payment as less risky, which can sometimes lead to more favorable loan terms and interest rates. Aiming for at least 10-20% of the car’s purchase price as a down payment is generally recommended. If you’re buying a brand new car, the closer to 20% you get, the better. Start saving early and consider earmarking specific funds for this purpose.

What About Your Trade-In? Don’t Get Shortchanged

If you plan to trade in your current vehicle, researching its value before applying for a car loan before you head to the dealership is crucial. Many buyers lose out on potential savings by letting the dealership dictate the trade-in value. Just as you wouldn’t buy a car without knowing its market price, you shouldn’t sell your old one blind.

Utilize online valuation tools like Kelley Blue Book (KBB.com) or Edmunds.com to get an accurate estimate of your car’s trade-in value based on its condition, mileage, and features. Be honest about its condition to get the most realistic figure. Remember that the trade-in value is different from the private sale value; dealerships need to make a profit when they resell your car. Pro tips from us: separate the trade-in negotiation from the new car’s price negotiation. Always negotiate the price of the new vehicle first, and then discuss your trade-in. This prevents the dealer from blurring the lines and making it difficult to discern if you’re getting a good deal on either. For more insights on this, you might find our article, "Maximizing Your Trade-In Value: A Step-by-Step Guide," particularly helpful.

Navigating the Pre-Approval Process

Once you’ve diligently completed your preliminary homework, you’re ready to embark on the pre-approval process. This is where your preparation truly pays off, as you approach lenders from a position of strength and clarity. Knowing how and where to apply for a car loan before can make all the difference.

Where to Get Pre-Approved: Banks, Credit Unions, and Online Lenders

You have several excellent options when seeking pre-approval, each with its own set of advantages.

- Traditional Banks: Large national and local banks are a common choice. They offer convenience, especially if you already have an account with them, and can sometimes provide competitive rates. Their application processes are typically straightforward.

- Credit Unions: Often lauded for their customer-centric approach, credit unions are non-profit organizations that frequently offer some of the best interest rates due to their structure. Membership is usually required but is often easy to obtain. If you’re looking for favorable terms, a credit union should be high on your list.

- Online Lenders: The digital age has brought forth numerous online-only lenders specializing in auto loans. Companies like Capital One Auto Finance, LightStream, and others offer quick online applications and can provide competitive rates from the comfort of your home. They are excellent for comparison shopping.

Pro tips from us: It’s wise to shop around and get quotes from at least three different lenders. Don’t worry about multiple credit inquiries hurting your score too much if done within a short period. Credit bureaus typically count multiple auto loan inquiries within a 14-45 day window as a single inquiry, recognizing that consumers shop for the best rates.

The Documents You’ll Need

To streamline the pre-approval process, have your documents ready. Lenders will typically ask for:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Recent pay stubs, W-2 forms, or tax returns (especially for self-employed individuals).

- Proof of Residence: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Basic Personal Information: Employment history, current debts, and assets.

Having these documents organized and accessible will significantly speed up your application and approval time.

Understanding Your Pre-Approval Offer

Once approved, you’ll receive an offer outlining the key terms of your potential loan. This includes:

- Interest Rate (APR): This is the cost of borrowing money, expressed as an annual percentage. A lower APR means less money paid over time.

- Loan Term: The duration of the loan, typically in months (e.g., 36, 48, 60, 72 months). Shorter terms mean higher monthly payments but less interest paid overall. Longer terms mean lower monthly payments but more interest.

- Maximum Loan Amount: The highest amount the lender is willing to lend you.

- Contingencies: Sometimes, pre-approvals have specific conditions, such as the vehicle needing to be below a certain age or mileage, or a specific down payment amount. Make sure you understand these clearly.

Carefully review all aspects of the offer. This is your benchmark for negotiations at the dealership.

Common Mistakes to Avoid During Pre-Approval

Even with the best intentions, it’s easy to make missteps during the pre-approval phase. Common mistakes to avoid are:

- Applying everywhere at once outside the shopping window: As mentioned, multiple inquiries within a specific timeframe for the same type of loan are usually grouped. However, applying for various types of credit (e.g., a car loan, a credit card, and a mortgage) simultaneously will impact your score more negatively.

- Not reading the fine print: Always understand the full terms and conditions of your pre-approval. Are there any hidden fees? What are the conditions for the rate?

- Ignoring the loan term: While a longer term can make monthly payments seem more affordable, it dramatically increases the total interest you pay over the life of the loan. Balance affordability with the overall cost. Aim for the shortest term you can comfortably manage.

The Strategic Advantage of Being Pre-Approved

Having your car loan pre-approval in hand before you walk into a dealership is not just about convenience; it’s a strategic move that fundamentally alters your buying experience. You transition from a hopeful buyer to a powerful negotiator.

Your Negotiating Superpower at the Dealership

With a pre-approval, you enter the dealership armed with a powerful piece of information: your maximum loan amount and, more importantly, your confirmed interest rate. This transforms the negotiation. Instead of discussing monthly payments, which dealers often manipulate by extending loan terms, you can focus squarely on the vehicle’s purchase price.

You can confidently say, "I’m approved for $X at Y% APR. Can you beat that, or at least match it?" This puts the ball squarely in the dealer’s court. They know you’re a serious buyer with outside financing options, which means they’ll work harder to earn your business. If the dealer can’t beat your pre-approved rate, you have the ultimate power to walk away and stick with your original lender. This leverage is invaluable.

Streamlined Car Buying Experience

One of the most immediate benefits of pre-approval is how much it simplifies and speeds up the car-buying process. Without pre-approval, you could spend hours in the finance office, waiting for the dealer to submit your application to various lenders and hear back. This is often a high-pressure environment designed to wear you down.

With pre-approval, you already have your financing sorted. The time you spend at the dealership can be dedicated to test driving, inspecting the vehicle, and negotiating the price. When it comes time to finalize the purchase, the finance process is significantly quicker and less stressful, as you’re primarily reviewing paperwork rather than waiting for approvals.

Avoiding Unnecessary Add-ons

Dealerships often rely on "extras" to boost their profit margins. These can include extended warranties, paint protection plans, fabric treatments, gap insurance, and various other add-ons that may or may not be necessary for your specific situation. When you’re focused on securing financing, it’s easy to get distracted and pressured into accepting these additional costs.

Being pre-approved allows you to remain focused and firm. You can clearly distinguish between the price of the car and any optional add-ons. You’re in a better position to decline items you don’t need or negotiate their prices down. Pro tips from us: always scrutinize every line item on the final purchase agreement. If you don’t understand it or don’t want it, question it and don’t be afraid to say no. For more detailed information on navigating these costs, our article, "Decoding Dealer Fees and Add-ons: What You Need to Know," offers valuable insights.

Conclusion

The question "Should I apply for a car loan before visiting a dealership?" has a clear answer: absolutely. Taking the time to secure pre-approval and thoroughly prepare your finances before you begin car shopping is not merely a recommendation; it’s a fundamental strategy for a successful, stress-free, and cost-effective car purchase. From understanding your budget and credit score to leveraging the power of a down payment and smart trade-in tactics, every step you take in advance empowers you.

By walking into a dealership with a pre-approved loan, you transform yourself from a hopeful shopper into a financially savvy buyer with significant negotiating power. You save time, reduce stress, and most importantly, you ensure that you get the best possible deal on your new vehicle. Don’t leave one of the largest purchases you’ll make to chance. Start your pre-approval journey today, and drive away with confidence, knowing you’ve made a smart financial decision. Your future self (and your wallet) will thank you.