Small Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

Small Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence Carloan.Guidemechanic.com

Finding the right financing for a vehicle can often feel like navigating a complex maze, especially when you’re looking for a specific amount. Whether you need a modest sum to purchase a reliable used car, cover an essential repair, or simply upgrade your current ride without breaking the bank, the quest for "small car loans near me" is a common and important one. This comprehensive guide is designed to demystify the process, offering you an in-depth look at how to secure an affordable, manageable car loan that fits your budget and gets you on the road.

We understand that a car is more than just a mode of transport; it’s a lifeline to work, family, and opportunities. That’s why securing the right small car loan is so vital. We’ll explore everything from understanding what these loans entail to finding the best local lenders, navigating credit challenges, and avoiding common pitfalls. Our goal is to equip you with the knowledge and confidence to make an informed decision, ensuring you drive away with not just a car, but also peace of mind.

Small Car Loans Near Me: Your Ultimate Guide to Driving Away with Confidence

What Exactly is a Small Car Loan? Defining the Scope

Before diving into the "near me" aspect, it’s crucial to understand what constitutes a "small car loan." Unlike traditional auto loans that might finance brand-new, high-value vehicles, a small car loan typically refers to financing for a lesser amount, often ranging from a few thousand dollars up to perhaps $10,000 or $15,000. This isn’t a rigid definition, as what one lender considers "small" another might see as moderate.

These loans are generally tailored for specific scenarios. They might be used for purchasing an older, but reliable, used car, or for covering the remaining balance after a significant down payment. Sometimes, they’re sought after to finance a classic car project, a secondary family vehicle, or even to consolidate existing car-related debt. The key differentiator is the lower principal amount, which often translates to more manageable monthly payments and shorter loan terms, making them an attractive option for budget-conscious buyers.

Why You Might Need a Small Car Loan: Common Scenarios

There are numerous reasons why individuals seek out small car loans. Understanding these common scenarios can help you determine if this financing option is right for your unique situation. Often, it’s about practical needs rather than luxury purchases.

Perhaps you’re a first-time car buyer, and a modest, pre-owned vehicle fits your budget perfectly. You might need a reliable car for commuting to a new job, or maybe your current vehicle just broke down unexpectedly and repairs are too costly, necessitating a quick replacement. In these instances, a small car loan offers a practical solution without the burden of a large, long-term financial commitment.

Another common scenario involves families looking for a second car. This might be for a new driver in the household, or simply to manage daily logistics more efficiently. Instead of investing in another expensive vehicle, a small car loan can make a budget-friendly used car accessible. These loans also appeal to those who prefer to keep their debt levels low, choosing to finance only a portion of a car’s value or to target an older model that still serves its purpose effectively.

The "Near Me" Advantage: Why Local Lenders Matter

When searching for "small car loans near me," you’re tapping into a significant advantage: the power of local connection. While national online lenders offer convenience, local banks and credit unions often provide a more personalized experience, which can be invaluable when dealing with financial decisions.

Local institutions frequently have a deeper understanding of the economic conditions and specific needs of their community. This local insight can sometimes translate into more flexible lending criteria or tailored loan products that larger, more impersonal lenders might not offer. They might be more willing to consider your individual circumstances beyond just a credit score, especially if you have an established banking relationship with them.

Based on my experience, forging a relationship with a local lender can simplify future financial needs. When you walk into a branch, you’re often speaking with someone who lives and works in your community. This personal touch can make the application process feel less intimidating and more collaborative. Furthermore, local lenders often pride themselves on quick decision-making, as they don’t have layers of corporate bureaucracy to navigate, potentially getting you approved and on the road faster.

Types of Lenders Offering Small Car Loans

The landscape of auto financing is diverse, with several types of institutions offering small car loans. Each has its own advantages and disadvantages, and understanding them will help you choose the best fit for your needs.

Banks (National, Regional, Local)

Banks are a traditional source for car loans. Larger national banks offer extensive online resources and branches, providing convenience and competitive rates for well-qualified borrowers. Regional and local banks, however, often offer that personalized service mentioned earlier. They might be more flexible with loan terms or offer specialized programs for local residents.

- Pros: Established reputation, competitive rates for good credit, various loan products.

- Cons: Can be slower processing, stricter credit requirements, less flexibility for unique situations.

Credit Unions

Credit unions are non-profit financial cooperatives owned by their members. They are renowned for offering some of the most competitive interest rates on auto loans, including small car loans. Their member-centric approach means they often prioritize lower fees and better terms for their community.

- Pros: Generally lower interest rates, personalized service, often more flexible for members with less-than-perfect credit.

- Cons: Requires membership (often easy to join), limited branch locations compared to large banks.

Dealership Financing

Many car dealerships offer in-house financing or work with a network of lenders. This can be a convenient "one-stop shop" solution, especially if you’re purchasing a used car directly from them. They might also have special promotions or incentives.

- Pros: Convenience, potential for special offers, can work with various credit profiles.

- Cons: Rates might be higher than direct lenders, limited options, can feel pressured to accept their terms.

Online Lenders

The digital age has brought a surge of online lenders specializing in auto loans. These platforms offer speed and convenience, allowing you to apply and get pre-approved from the comfort of your home. They often cater to a wide range of credit scores.

- Pros: Fast application and approval process, convenient, can compare multiple offers quickly.

- Cons: Less personal interaction, might miss out on local deals, requires careful vetting of the lender’s reputation.

Eligibility Requirements for Small Car Loans

While the loan amount might be small, lenders still have specific criteria you need to meet. Understanding these requirements is key to a successful application for "small car loans near me."

- Credit Score: Your credit score is a primary factor. While a perfect score isn’t always necessary for a small car loan, a higher score generally translates to better interest rates. Lenders categorize scores into excellent, good, fair, and poor. Even if you have a lower score, options exist, though the terms might be less favorable.

- Income and Employment: Lenders want assurance that you can repay the loan. This means demonstrating a stable income and consistent employment. They’ll typically ask for pay stubs, tax returns, or bank statements to verify your financial stability.

- Debt-to-Income (DTI) Ratio: This ratio compares your total monthly debt payments to your gross monthly income. A lower DTI indicates you have more disposable income to cover new loan payments, making you a less risky borrower.

- Down Payment: While not always mandatory for small car loans, a down payment can significantly improve your chances of approval and secure a better interest rate. It shows the lender your commitment and reduces their risk.

- Vehicle Age and Mileage: For small car loans, especially those for used vehicles, the age and mileage of the car can influence the loan terms. Older cars with high mileage might have shorter loan terms or slightly higher rates due to perceived higher risk of mechanical issues.

Navigating Small Car Loans with Less-Than-Perfect Credit

Don’t despair if your credit score isn’t stellar. Many individuals search for "bad credit car loans near me," and thankfully, options do exist. It’s about knowing the strategies to improve your chances and finding the right lenders.

One common strategy is to seek a co-signer with good credit. A co-signer essentially guarantees the loan, mitigating the lender’s risk and often leading to approval and better terms. Just remember, your co-signer is equally responsible for the debt. Another effective approach is to offer a larger down payment. This reduces the amount you need to borrow and demonstrates your financial commitment, making you a more attractive borrower.

Pro tips from us: Explore lenders specifically catering to subprime borrowers. Some local credit unions or smaller finance companies specialize in working with individuals building or rebuilding their credit. While interest rates might be higher, making timely payments on a small car loan can be an excellent way to improve your credit score over time, opening doors to better financial products in the future. Be prepared to explain any past credit issues transparently, as some lenders appreciate honesty and context.

The Application Process: A Step-by-Step Guide

Securing a small car loan doesn’t have to be daunting. Following a structured application process can streamline your experience and increase your chances of approval.

- Check Your Credit Score: Before anything else, obtain a copy of your credit report and score. This allows you to understand your financial standing and correct any errors. Knowing your score helps you set realistic expectations for interest rates and loan terms.

- Determine Your Budget: Carefully assess how much you can truly afford for a monthly car payment, factoring in insurance, fuel, and maintenance. Don’t just focus on the loan amount; consider the total cost of ownership.

- Gather Necessary Documents: Lenders will require documentation such as government-issued ID, proof of income (pay stubs, tax returns), proof of residency (utility bills), and potentially bank statements. Having these ready will expedite the process.

- Get Pre-Qualified/Pre-Approved: This is a crucial step. Many lenders offer pre-qualification, which involves a soft credit check and gives you an idea of potential loan amounts and rates without impacting your score. Pre-approval involves a harder credit check but gives you a firm offer, allowing you to shop for a car with confidence, knowing exactly how much you can spend.

- Shop Around for the Best Offers: Don’t settle for the first offer you receive. Contact multiple lenders—banks, credit unions, and online providers—to compare interest rates, loan terms, and fees. This is where the "near me" search really pays off, as local lenders can sometimes beat national rates.

- Submit Your Application: Once you’ve chosen a lender and a vehicle, complete the full application. Be thorough and honest with all information provided.

- Review and Sign: Before signing any loan agreement, read every line carefully. Ensure you understand the interest rate (APR), total loan amount, monthly payment, and any associated fees. Don’t hesitate to ask questions if anything is unclear.

Key Factors to Consider Before Applying

Making an informed decision about your small car loan requires a close look at several critical factors. These go beyond just the monthly payment.

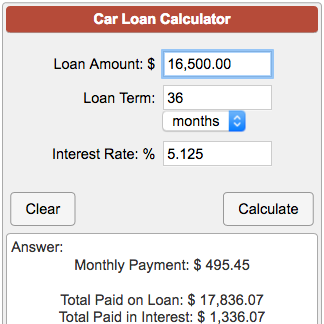

- Interest Rates (APR): The Annual Percentage Rate (APR) is perhaps the most important figure. It includes not only the interest rate but also any fees, giving you the true annual cost of borrowing. Even a small difference in APR can save you hundreds of dollars over the life of the loan. Always compare APRs, not just interest rates.

- Loan Term: This is the length of time you have to repay the loan. Shorter terms typically mean higher monthly payments but less interest paid overall. Longer terms reduce monthly payments but increase the total interest paid and the risk of owing more than the car is worth (being upside down). For a small car loan, aiming for a shorter term is often advisable to minimize interest costs.

- Fees and Charges: Be aware of any origination fees, application fees, late payment fees, or prepayment penalties. While small car loans might have fewer fees than larger loans, they can still add up. Proactively ask lenders for a full disclosure of all potential charges.

- Total Cost of the Loan: Always calculate the total amount you will pay back, including the principal and all interest and fees. Sometimes, a seemingly low monthly payment can hide a much higher total cost due to a long loan term or high APR. Understanding this figure helps you make a truly cost-effective decision. For more detailed insights, you might want to check out our article on .

Pro Tips for Securing the Best Small Car Loan Near You

Based on my experience in the financial sector, a strategic approach can significantly improve your chances of securing favorable terms for "small car loans near me."

- Shop Around Aggressively: This cannot be stressed enough. Don’t just take the first offer. Contact at least three to five different lenders, including local credit unions, banks, and reputable online platforms. Use their initial offers as leverage to negotiate better terms.

- Improve Your Credit Score First: If you’re not in a rush, dedicating a few months to improving your credit score can save you a substantial amount in interest. Pay down existing debts, make all payments on time, and dispute any errors on your credit report. For tips on boosting your score, read our guide on .

- Negotiate, Negotiate, Negotiate: Everything is negotiable, from the interest rate to potential fees. If one lender offers a lower APR, see if another can match or beat it. Be confident and clear about what you’re looking for.

- Be Realistic About What You Can Afford: It’s tempting to stretch your budget for a slightly better car, but overextending yourself can lead to financial strain. Stick to a budget you’re comfortable with, even if it means a slightly older or less feature-rich vehicle.

- Read the Fine Print: Before signing, thoroughly review the entire loan agreement. Pay close attention to clauses regarding late payments, default, and any early payoff penalties. Common mistakes to avoid are signing without fully understanding every term.

Common Mistakes to Avoid When Seeking a Small Car Loan

While the idea of a small loan might seem less intimidating, certain missteps can still lead to financial headaches. Being aware of these common pitfalls can save you time, money, and stress.

- Not Checking Your Credit Report: A surprising number of people apply for loans without knowing their credit standing. This can lead to unexpected rejections or being offered much higher interest rates than anticipated. Always check your report for accuracy.

- Only Applying to One Lender: Limiting your options means you’re missing out on potentially better deals. Lenders have different criteria and rates; comparing multiple offers is essential for securing the best terms.

- Focusing Only on Monthly Payments: While crucial, the monthly payment is just one piece of the puzzle. Overly long loan terms can make monthly payments seem affordable but result in paying significantly more in total interest. Always look at the total cost of the loan and the APR.

- Ignoring the APR: Some lenders might quote a low "interest rate" but then add various fees that push the true annual cost much higher. The APR gives you the most accurate picture of the total cost of borrowing.

- Being Dishonest on Your Application: Providing false information can lead to immediate loan rejection, or worse, legal repercussions. Always be truthful and transparent with your financial details.

- Not Budgeting for Other Car Expenses: Beyond the loan payment, remember to budget for insurance, fuel, maintenance, and potential repairs. A small car loan can be affordable, but the overall cost of car ownership still needs to be considered.

Based on My Experience: Real-World Insights

Having guided countless individuals through the car financing process, I’ve seen firsthand how important a local approach can be, especially for smaller loan amounts. Often, people overlook their local credit union, thinking they only cater to large loans. This is a common misconception. Many credit unions are eager to help members with smaller financial needs, viewing it as an opportunity to build a lasting relationship.

I recall a client who needed a $7,000 loan for a reliable used car after their old one unexpectedly broke down. They initially applied online and were met with high-interest offers due to a minor credit hiccup from a few years prior. After advising them to visit their local credit union where they had a checking account, they were not only approved but received an interest rate significantly lower than the online offers. The personal conversation with the loan officer allowed them to explain their situation, something a faceless online application couldn’t accommodate. This highlights the "near me" advantage – human connection and understanding can sometimes outweigh rigid algorithms.

Another valuable insight is the power of a strong down payment, even for a small loan. It significantly reduces the principal, making the loan less risky for the lender and almost always resulting in better terms for you. Even an extra few hundred dollars saved for a down payment can make a noticeable difference in your interest rate or monthly payment.

Beyond the Loan: What Happens After Approval?

Once your small car loan is approved and you’ve found your perfect vehicle, there are a few more steps to ensure a smooth transition to car ownership.

- Finalizing the Purchase: Work with your chosen dealership or private seller to complete the purchase. Your lender will typically disburse the funds directly to the seller.

- Vehicle Registration and Titling: You’ll need to register your car with your state’s Department of Motor Vehicles (DMV) and ensure the title is properly transferred. The lender will usually hold the title as collateral until the loan is fully repaid.

- Insurance: Auto insurance is a legal requirement in most places. Secure comprehensive insurance coverage before driving your new car off the lot. Lenders often require certain levels of coverage to protect their investment.

- Making Timely Payments: This is crucial for building good credit and avoiding late fees. Set up automatic payments or mark your calendar to ensure you never miss a due date. Consistently making on-time payments on your small car loan can significantly improve your credit score over time, paving the way for better financial opportunities in the future.

Future-Proofing Your Car Loan Journey

Even after you’ve secured your small car loan and are happily driving your vehicle, it’s wise to think ahead.

- Building Credit: Use your small car loan as a tool to build a strong credit history. Consistent, on-time payments will positively impact your credit score, making future loans (whether for another car, a home, or personal needs) more accessible and affordable.

- Refinancing Options: If your credit score improves significantly after a year or two of on-time payments, or if interest rates drop, you might consider refinancing your small car loan. Refinancing could potentially lower your interest rate, reduce your monthly payment, or shorten your loan term, saving you money in the long run.

- Prepaying Your Loan: If your financial situation improves, consider making extra payments or paying off your loan early. This saves you money on interest and frees up your monthly budget. Just ensure your loan agreement doesn’t have prepayment penalties.

Conclusion: Driving Towards Your Small Car Loan

Securing "small car loans near me" is an achievable goal that can open up a world of convenience and opportunity. By understanding the types of loans available, knowing your financial standing, meticulously preparing your application, and comparing offers from local lenders, you can find a financing solution that perfectly fits your budget and needs. Remember, a small car loan is not just about the vehicle itself, but about smart financial planning and building a positive credit future.

Don’t let the search for affordable car financing overwhelm you. Take the time to explore your local options, leverage the power of personalized service, and approach the process with confidence. With the insights and strategies provided in this guide, you are well-equipped to make an informed decision and drive away with confidence, knowing you’ve made a smart financial choice. Start your search for those ideal small car loans near you today – your next reliable ride awaits!

External Resource: For more general advice on car buying and financing, visit the Consumer Financial Protection Bureau (CFPB) website: https://www.consumerfinance.gov/consumer-tools/auto-loans/