Stuck in Neutral? How a Personal Loan Can Get Your Car – And Your Life – Back on Track

Stuck in Neutral? How a Personal Loan Can Get Your Car – And Your Life – Back on Track Carloan.Guidemechanic.com

That dreaded moment: your car sputters, a warning light flashes, or worse, it just won’t start. For many of us, a vehicle isn’t just a convenience; it’s a lifeline. It gets us to work, takes our kids to school, and connects us to the world. But what happens when unexpected repairs hit, and your emergency fund isn’t quite ready for the hefty bill? This is a common predicament, and it’s where a well-chosen personal loan can become a crucial solution.

In this comprehensive guide, we’ll explore everything you need to know about using a personal loan to fix your car. We’ll delve into the benefits, potential drawbacks, the application process, and smart strategies to ensure you make the best financial decision. Our goal is to empower you with the knowledge to navigate this stressful situation confidently, getting you back on the road safely and without undue financial strain.

Stuck in Neutral? How a Personal Loan Can Get Your Car – And Your Life – Back on Track

The Unexpected Reality of Car Repairs: More Than Just a Nuisance

Cars, like any complex machinery, are prone to wear and tear. One day they’re running smoothly, the next you’re faced with a sudden breakdown. These aren’t just minor inconveniences; they can represent a significant financial hurdle.

Common repairs, such as transmission issues, engine problems, or even major brake overhauls, can easily run into hundreds or even thousands of dollars. These costs are often unpredictable, striking when you least expect them and, frustratingly, when your budget is already stretched thin. Based on my experience in personal finance, I’ve seen countless individuals caught off guard by these sudden expenses, leading to difficult choices between essential repairs and other financial obligations.

Understanding Personal Loans for Car Repairs: A Flexible Solution

So, what exactly is a personal loan, and why is it often a go-to option when you need to finance car repairs? Simply put, a personal loan is a type of installment loan provided by banks, credit unions, or online lenders. It’s typically unsecured, meaning you don’t have to put up collateral like your car or home to get the funds.

This flexibility is a major advantage. Unlike an auto loan, which is tied directly to the purchase of a vehicle, a personal loan gives you cash that you can use for almost any purpose – including those unforeseen car repairs. You receive a lump sum, which you then repay over a fixed period, usually with fixed monthly payments and a predetermined interest rate. This predictability makes budgeting much easier.

Pros and Cons of Using a Personal Loan to Fix Your Car

While a personal loan can be a lifesaver for unexpected car repairs, it’s essential to weigh its advantages against its potential drawbacks. A balanced perspective ensures you make an informed decision that aligns with your financial health.

The Advantages: Getting You Back on the Road

- Quick Access to Funds: When your car is out of commission, time is of the essence. Personal loans often offer a fast application and approval process, with funds disbursed within a few business days, sometimes even faster.

- Fixed Interest Rates and Payments: Unlike credit cards with variable rates, personal loans typically come with fixed interest rates. This means your monthly payment remains consistent throughout the loan term, making it easier to budget and manage your finances.

- No Collateral Required: Most personal loans are unsecured. You don’t have to pledge your car, home, or other assets as collateral, reducing your personal risk compared to options like title loans.

- Potentially Lower Interest Rates: Depending on your creditworthiness, personal loan interest rates can be significantly lower than those on credit cards, especially if you have excellent credit. This can save you a substantial amount of money over the life of the loan.

- Consolidation of Debt (Indirectly): If you’ve already put some repair costs on a high-interest credit card, a personal loan with a lower interest rate could effectively help you consolidate that debt into a more manageable payment.

The Disadvantages: Considerations Before You Commit

- Interest Accrues: While rates can be competitive, you will still pay interest on the borrowed amount. This adds to the overall cost of your car repair.

- Impact on Credit Score: Applying for a personal loan typically involves a hard inquiry on your credit report, which can temporarily ding your score. More importantly, missing payments will negatively impact your credit score significantly.

- Risk of Debt: Taking on any new debt requires careful consideration. If you overborrow or struggle to make payments, you could find yourself in a worse financial situation.

- Origination Fees: Some lenders charge an origination fee, which is a percentage of the loan amount deducted from your disbursed funds. Always factor this into the total cost.

Are You Eligible? Key Factors Lenders Consider

Before you dive into applications, it’s wise to understand what lenders look for. Knowing these criteria can help you prepare and even improve your chances of approval and securing a better rate. Pro tips from us: always assess your financial standing honestly before applying.

Lenders evaluate several factors to determine your creditworthiness and your ability to repay the loan.

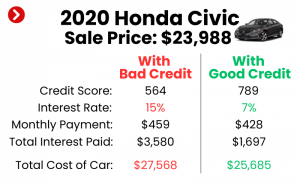

- Credit Score: This is perhaps the most significant factor. A higher credit score (generally 670 and above) indicates a lower risk to lenders, often leading to better interest rates and higher approval chances. If your credit score is lower, don’t despair; some lenders specialize in loans for fair or even poor credit, though at higher interest rates.

- Income and Employment Stability: Lenders want to see a consistent and sufficient income stream to ensure you can comfortably make your monthly payments. They’ll typically ask for proof of employment, such as pay stubs or tax returns.

- Debt-to-Income (DTI) Ratio: Your DTI ratio compares your total monthly debt payments to your gross monthly income. A lower DTI (ideally below 36%) signals that you have enough disposable income to handle new loan payments without being overextended.

- Credit History: Lenders will review your overall credit report to see how you’ve managed past debts. A history of on-time payments and responsible credit use will work in your favor. Conversely, bankruptcies, defaults, or a high number of recent credit inquiries can raise red flags.

- Existing Debts: The amount of outstanding debt you already carry will influence a lender’s decision. They want to ensure that adding another loan won’t push you into an unsustainable debt spiral.

Navigating the Application Process: A Step-by-Step Guide

Applying for a personal loan might seem daunting, but breaking it down into manageable steps makes the process straightforward. Based on my experience helping individuals secure financing, preparation is key.

- Assess Your Needs: First, get an accurate estimate for your car repairs. Don’t borrow more than you need, but also ensure you borrow enough to cover the full cost.

- Check Your Credit Score: Before applying, know your credit score. You can get free access to your credit report from services like AnnualCreditReport.com. This will give you an idea of what interest rates you might qualify for.

- Research Lenders: Don’t just go with the first offer. Compare options from traditional banks, credit unions, and online lenders. Online lenders often have faster processes and competitive rates, while credit unions might offer more personalized service and lower rates for members.

- Get Pre-qualified: Many lenders offer a pre-qualification process, which involves a soft credit pull (doesn’t impact your score). This gives you an idea of potential rates and terms without committing to a full application. It’s a great way to compare offers from multiple lenders.

- Gather Your Documents: Once you choose a lender, you’ll need documents like government-issued ID, proof of income (pay stubs, W-2s, tax returns), bank statements, and potentially proof of residence. Having these ready will expedite the application.

- Submit Your Application: Complete the full application form, providing accurate and truthful information. Any discrepancies could cause delays or rejection.

- Review the Loan Offer: If approved, carefully read the loan agreement, paying close attention to the interest rate (APR), loan term, monthly payment, and any fees.

- Receive Funds: Once you accept the terms, the funds are typically disbursed directly into your bank account within a few business days.

Comparing Loan Offers: What to Look For

When you’re faced with multiple loan offers, it’s crucial to compare them diligently to find the one that best suits your financial situation. Don’t just focus on the advertised interest rate; a deeper dive is necessary.

- Annual Percentage Rate (APR): This is the most critical figure. The APR includes both the interest rate and any fees (like origination fees), giving you the true annual cost of borrowing. Always compare APRs, not just interest rates.

- Loan Term: This is the length of time you have to repay the loan. Shorter terms usually mean higher monthly payments but less interest paid overall. Longer terms result in lower monthly payments but more interest over time. Choose a term that makes your monthly payment affordable.

- Monthly Payments: Ensure the monthly payment fits comfortably within your budget. A payment that stretches your finances too thin can lead to missed payments and a damaged credit score.

- Fees: Look out for origination fees, late payment fees, prepayment penalties (though rare with personal loans), and any other charges. Some lenders are more transparent than others.

- Total Cost of the Loan: Calculate the total amount you will repay over the life of the loan (principal + interest + fees). This gives you a clear picture of the true cost of borrowing.

Alternatives to Personal Loans for Car Repairs

While a personal loan is a strong contender, it’s not the only option. Exploring alternatives ensures you pick the most appropriate solution for your unique circumstances. Common mistakes to avoid are jumping into the first financing option without considering all possibilities.

- Emergency Savings: The ideal scenario is to have an emergency fund specifically for unexpected expenses like car repairs. If you have one, using your savings avoids debt and interest payments altogether. If you’re interested in building a robust emergency fund, check out our guide on .

- Credit Cards: If you have a credit card with a low balance and a low interest rate, or better yet, a 0% introductory APR offer, this could be a viable option for smaller repairs. However, beware of high interest rates after the promotional period and ensure you can pay off the balance quickly.

- Auto Repair Shop Financing: Some larger repair shops offer their own financing options, often through third-party providers. These can sometimes have attractive introductory rates but always scrutinize the terms and conditions, especially after any promotional periods expire.

- Home Equity Line of Credit (HELOC) or Loan: If you’re a homeowner with significant equity, a HELOC or home equity loan could offer lower interest rates. However, these are secured loans, meaning your home acts as collateral, and the application process is longer. This is generally overkill for most car repairs.

- Borrowing from Family or Friends: This can be a no-interest or low-interest option, but it comes with potential relational complexities. Ensure clear terms and repayment plans are established to avoid misunderstandings.

- Peer-to-Peer Lending: Platforms connect borrowers directly with individual investors. Rates can be competitive, and approval might be possible for those with less-than-perfect credit, but the process can sometimes be slower.

- Title Loans (Caution Advised): These loans use your car’s title as collateral. While they offer quick cash, they come with extremely high interest rates and fees. If you default, you risk losing your vehicle. Pro tips from us: We strongly advise against title loans unless you have absolutely no other option and are certain you can repay it promptly.

Smart Repayment Strategies for Your Car Repair Loan

Securing the loan is only half the battle; successfully repaying it is where true financial discipline comes in. A well-thought-out repayment plan can save you money and protect your credit score.

- Budget for Payments: Integrate your new loan payment into your monthly budget immediately. Treat it as a fixed expense, just like rent or utilities. Ensure you have enough disposable income to cover it comfortably.

- Automate Payments: Set up automatic payments from your checking account. This ensures you never miss a due date, avoiding late fees and negative impacts on your credit score. Many lenders even offer a small interest rate discount for autopay.

- Pay More Than the Minimum (If Possible): If your financial situation improves, consider paying a little extra each month. Even small additional payments can significantly reduce the total interest paid and shorten your loan term.

- Communicate with Your Lender: If you anticipate difficulty making a payment, don’t wait until you’re overdue. Contact your lender immediately to discuss potential options, such as deferment or a modified payment plan. Open communication is always better than defaulting.

- Avoid New Debt: While repaying your car repair loan, try to avoid taking on unnecessary new debt. Focus on getting this loan paid off first to free up your financial resources.

Things to Consider Before Taking Out a Loan

Before you commit to a personal loan for car repairs, take a moment to ask yourself some critical questions. This reflection can prevent future financial regret.

- Is the Repair Truly Necessary? Sometimes, an old car might need a repair that costs more than the car is worth. In such cases, putting the loan money towards a down payment on a newer, more reliable used car might be a wiser decision.

- What is the Car’s Value vs. Repair Cost? Calculate if the repair cost is a significant percentage of your car’s current market value. If a $3,000 repair is needed for a car only worth $4,000, it might be time to reconsider.

- Can You Afford the Monthly Payments? Be realistic about your budget. Don’t let the urgency of the repair push you into an unsustainable payment plan.

- Have You Explored Cheaper Repair Options? Get multiple quotes from different mechanics. Sometimes, a smaller independent shop might offer better rates than a dealership.

- What’s the Long-Term Plan? Is this a one-off repair, or is your car constantly breaking down? If it’s the latter, a personal loan for a down payment on a new vehicle might be a better long-term strategy than repeatedly fixing an unreliable car.

Common Mistakes to Avoid When Financing Car Repairs

Based on my observations in the financial world, certain pitfalls can turn a temporary car repair solution into a long-term financial headache. Being aware of these common mistakes can help you steer clear of them.

- Not Comparing Offers: This is a major misstep. Accepting the first loan offer without comparing APRs, terms, and fees from multiple lenders can cost you hundreds or even thousands of dollars in extra interest.

- Borrowing More Than Needed: While it might seem tempting to borrow a little extra "just in case," every dollar borrowed incurs interest. Only borrow the exact amount required for the repair.

- Ignoring the Fine Print: Loan agreements can be complex, but it’s crucial to understand all terms, including fees, penalties for late payments, and what happens if you default.

- Defaulting on Payments: Missing payments not only incurs late fees but also severely damages your credit score, making it harder and more expensive to borrow money in the future.

- Not Considering Alternatives: As discussed, personal loans are just one option. Failing to explore alternatives like credit cards (if used strategically) or a strong emergency fund can lead to suboptimal financial decisions.

- Overlooking Your Budget: Taking on a loan without a clear plan for repayment is a recipe for disaster. Always ensure the monthly payment fits comfortably within your existing budget.

Building a Financial Safety Net for Future Repairs

Dealing with an unexpected car repair highlights the importance of financial preparedness. While a personal loan can solve an immediate crisis, building a safety net prevents future ones.

- Establish an Emergency Fund: Aim for at least 3-6 months of living expenses in a readily accessible savings account. This fund is your first line of defense against unforeseen costs like car repairs, medical emergencies, or job loss.

- Regular Car Maintenance: Proactive maintenance can prevent many major breakdowns. Stick to your car’s recommended service schedule to catch small issues before they become expensive problems.

- Consider a Vehicle Service Contract or Extended Warranty: For newer cars, these can provide peace of mind by covering certain repairs after the manufacturer’s warranty expires. However, carefully weigh the cost against the potential benefits and read the fine print.

Conclusion: Drive Away with Confidence

A broken-down car is undoubtedly a stressful situation, but understanding your financing options, especially the role of a personal loan, can transform that stress into a manageable challenge. By approaching the problem with careful research, a clear understanding of your financial standing, and a commitment to smart repayment strategies, you can secure the funds needed to fix your car and get back on the road without derailing your financial future.

Remember, the goal is not just to fix your car, but to do so in a way that strengthens, rather than weakens, your financial health. Take the time to compare lenders, understand the terms, and ensure your decision is both practical and responsible. With the right approach, a personal loan can be the engine that gets your car – and your life – running smoothly again. For further details on consumer lending regulations, you can refer to the External Link: Consumer Financial Protection Bureau website.