Taking Out A Loan For A Car: Your Ultimate Guide to Smart Auto Financing

Taking Out A Loan For A Car: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

The dream of a new set of wheels is a common aspiration for many. Whether it’s the freedom of hitting the open road, the convenience of daily commuting, or the necessity of reliable transportation, owning a car opens up a world of possibilities. For most people, purchasing a vehicle isn’t a cash transaction; it involves taking out a loan.

Navigating the world of car loans can seem daunting, with terms like APR, loan terms, principal, and interest often swirling around. However, understanding the process of taking out a loan for a car is crucial for making a financially sound decision. This comprehensive guide will break down every aspect of auto financing, empowering you to secure the best deal and drive away with confidence.

Taking Out A Loan For A Car: Your Ultimate Guide to Smart Auto Financing

Understanding the Basics of Car Loans

Before diving into the application process, it’s essential to grasp what a car loan entails and why it’s a popular financing option. A car loan is a secured loan, meaning the car itself acts as collateral. If you default on your payments, the lender has the right to repossess the vehicle.

This security for the lender often translates into more favorable interest rates compared to unsecured loans, like personal loans, because the risk to the lender is reduced.

Why Take Out a Car Loan?

Taking out a loan for a car serves several practical purposes. Firstly, it makes vehicle ownership accessible to a wider population, as most individuals don’t have tens of thousands of dollars readily available for a direct purchase. It allows you to acquire a significant asset without depleting your savings.

Secondly, a car loan can be an excellent tool for building or improving your credit history. Consistently making timely payments on a secured loan demonstrates financial responsibility, which can positively impact your credit score over time. This can then open doors to better rates on future loans, such as mortgages or other significant purchases.

Types of Car Loans

Not all car loans are created equal. Understanding the different types available will help you choose the one that best fits your situation. Each option comes with its own set of advantages and considerations.

New Car Loans vs. Used Car Loans

The distinction between new and used car loans is straightforward. New car loans are for brand-new vehicles straight from the dealership. They typically offer lower interest rates and longer loan terms due to the car’s higher value and perceived reliability. However, new cars depreciate rapidly the moment they leave the lot.

Used car loans, on the other hand, finance pre-owned vehicles. While they might come with slightly higher interest rates or shorter terms because of the car’s age and mileage, the overall cost of a used car is significantly less. This can make monthly payments more affordable and reduce the total interest paid over the life of the loan.

Dealership Financing vs. Bank/Credit Union Loans

When you’re ready to buy, you’ll encounter two primary sources for taking out a loan for a car. Dealership financing is convenient; you can often secure a loan directly at the dealership, sometimes even benefiting from manufacturer-backed special interest rates. However, these rates might not always be the absolute best available, and the focus can sometimes shift from negotiating the car price to negotiating the monthly payment.

Banks and credit unions offer direct loans that you secure before you even step foot on a dealership lot. This approach provides you with a pre-approved loan, giving you significant negotiating power and a clear budget. Credit unions, in particular, are known for offering competitive rates and more personalized service to their members.

Private Party Loans

If you’re buying a car from a private seller rather than a dealership, you’ll need a private party auto loan. Not all lenders offer these, as the car doesn’t go through the same inspection and valuation processes as a dealership vehicle. These loans might require more legwork in terms of documentation and appraisal, but they allow you to tap into the often-lower prices of private sales.

Refinancing Options

Sometimes, after taking out a loan for a car, circumstances change. You might find yourself with a better credit score, or interest rates might drop significantly. Refinancing involves taking out a new loan to pay off your existing car loan, ideally at a lower interest rate or with more favorable terms. This can reduce your monthly payments, lower the total interest paid, or shorten your loan term, saving you money in the long run.

Preparing for Your Car Loan Application

Preparation is key to securing the best possible terms when taking out a loan for a car. Rushing into the process without understanding your financial standing can lead to higher interest rates or even rejection. A little groundwork can save you thousands over the life of your loan.

Assessing Your Financial Health

Before you even start looking at cars, take an honest look at your finances. This critical step will define your budget and determine what you can realistically afford. Overextending yourself on a car loan is a common pitfall that can lead to financial strain.

Budgeting for a Car Loan

Your budget should encompass more than just the monthly loan payment. Consider the total cost of car ownership, which includes insurance, fuel, maintenance, and potential repair costs. A good rule of thumb is that your total car expenses, including your loan payment, should not exceed 10-15% of your take-home pay.

Lenders will assess your debt-to-income (DTI) ratio, which compares your total monthly debt payments to your gross monthly income. A lower DTI ratio indicates you have more disposable income and are less of a risk. Keeping this ratio healthy is vital for loan approval.

Understanding Your Credit Score

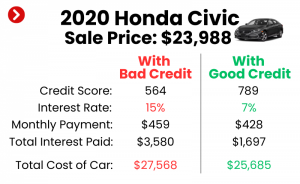

Your credit score is arguably the most significant factor lenders consider when you’re taking out a loan for a car. It’s a numerical representation of your creditworthiness, reflecting your history of managing debt. A higher score signifies lower risk to lenders and, consequently, qualifies you for better interest rates.

Based on my experience, a good credit score is your most powerful tool in securing favorable loan terms. Scores typically range from 300 to 850, with anything above 700 generally considered good to excellent. Lenders use these scores to quickly assess your reliability as a borrower.

Checking Your Credit Report

Before applying for any loan, obtain a copy of your credit report from all three major bureaus (Equifax, Experian, TransUnion). You are entitled to a free report from each annually via AnnualCreditReport.com. Review these reports carefully for any inaccuracies or errors.

Disputing and correcting errors can significantly improve your credit score, potentially qualifying you for a much lower interest rate. This proactive step can save you substantial money over the life of your auto loan.

The Down Payment Dilemma

A down payment is the initial sum of money you pay upfront towards the purchase of your car. While not always mandatory, making a substantial down payment offers several significant advantages. It reduces the amount you need to borrow, which directly translates to lower monthly payments and less interest paid over the life of the loan.

Why a Down Payment Matters

A larger down payment also reduces your loan-to-value (LTV) ratio, which is the amount you borrow compared to the car’s value. A lower LTV makes you a less risky borrower in the eyes of lenders. Furthermore, since cars begin depreciating immediately, a healthy down payment helps prevent you from being "upside down" on your loan, where you owe more than the car is worth. This situation can be problematic if you need to sell or total the car.

How Much Should You Put Down?

While there’s no magic number, financial experts often recommend putting down at least 10% for a used car and 20% for a new car. This range typically provides a good balance between reducing your loan burden and keeping your upfront costs manageable. Of course, if you can afford to put down more, you will reap greater financial benefits.

Trade-In Value

If you have an existing car, trading it in can serve as a form of down payment. Before heading to the dealership, research your car’s value using online tools like Kelley Blue Book (KBB) or Edmunds. Knowing its approximate trade-in value empowers you to negotiate effectively. Selling your car privately might fetch a higher price, but trading it in offers the convenience of a single transaction.

The Car Loan Application Process: Step-by-Step

Navigating the application for taking out a loan for a car can be a straightforward process if you follow a logical sequence. Each step builds upon the last, ensuring you remain in control and make informed decisions.

Step 1: Get Pre-Approved

This is perhaps the most crucial step in the entire car buying journey. Getting pre-approved for a loan means a lender has reviewed your credit and financial situation and has provisionally agreed to lend you a specific amount at a particular interest rate. This approval comes with an expiration date, usually 30-60 days.

What is Pre-Approval?

Pre-approval provides you with a powerful tool: a clear budget and an interest rate firmly in hand before you start car shopping. It transforms you from a mere shopper into a cash buyer in the eyes of a dealership. This removes the mystery around what you can afford and allows you to focus purely on the car’s price.

The advantages are numerous: you gain significant negotiating power, as you already have a financing offer. You also avoid the pressure of in-dealership financing discussions and can walk away if a dealer’s offer isn’t competitive.

Where to Get Pre-Approved

You can obtain pre-approval from various sources. Banks, both national and local, are common options. Credit unions are often excellent choices, typically offering lower interest rates to their members. Online lenders have also emerged as competitive players, providing quick applications and sometimes very attractive rates. It’s wise to get pre-approved from at least two or three different lenders to compare offers effectively.

Step 2: Shopping for Your Car

With a pre-approval in hand, you can now confidently shop for your vehicle. This step focuses on finding the right car within your budget and negotiating the best purchase price.

Sticking to Your Budget

Your pre-approval amount sets your maximum spending limit. It’s crucial to stick to this budget, or even aim below it, to ensure financial comfort. Don’t be swayed by enticing upgrades or features that push you beyond what you’ve determined you can afford.

Negotiating the Car Price Before Mentioning Financing

This is a pro tip from us: always negotiate the car’s purchase price as if you were paying cash. Do not mention your pre-approval or that you’re taking out a loan for a car until you’ve settled on the vehicle’s final price. Dealers often try to bundle the car price and financing terms, which can obscure the true cost of each. By separating these negotiations, you ensure you’re getting the best deal on the car itself.

Step 3: Comparing Loan Offers

Once you’ve settled on a car, it’s time to finalize your financing. Even with a pre-approval, you should always compare that offer with any financing options the dealership presents.

Key Factors: APR, Loan Term, Monthly Payment, Total Cost

When comparing loan offers, several key factors demand your attention. The Annual Percentage Rate (APR) is the most critical; it represents the true cost of borrowing, including interest and certain fees. A lower APR means less money paid over the life of the loan.

The loan term, or duration of the loan (e.g., 36, 48, 60, 72 months), directly impacts your monthly payment and the total interest paid. Longer terms mean lower monthly payments but significantly more interest over time.

Pro tips from us: Always compare at least three offers, including your pre-approval, to ensure you’re getting the most competitive rate. Focus on the total cost of the loan, not just the monthly payment, to understand your true financial commitment.

The Impact of Loan Term

Consider the trade-off between monthly payment and total cost. A 72-month loan might have an appealingly low monthly payment, but you’ll pay substantially more in interest compared to a 48-month loan. Shorter terms, while having higher monthly payments, result in less interest paid and you’ll own the car outright sooner. Balance your budget with your desire to minimize overall costs.

Step 4: Finalizing the Loan

Once you’ve chosen the best loan offer, it’s time to sign the paperwork. This stage requires careful attention to detail to avoid any unwelcome surprises.

Reading the Fine Print

Never sign a loan agreement without thoroughly reading every clause. Understand all fees involved, such as origination fees, documentation fees, or prepayment penalties (though these are less common with auto loans). Ensure the interest rate, loan term, and total amount match what you agreed upon.

Understanding Add-Ons

Dealerships often present various add-ons, such as extended warranties, GAP insurance, paint protection, or VIN etching. While some, like GAP insurance, might be beneficial in specific situations (especially if you have a low down payment), many are high-profit items for the dealership. Do not feel pressured to purchase them.

Common mistakes to avoid are signing without fully understanding every clause and accepting add-ons you don’t need or haven’t thoroughly researched. Each add-on increases the total amount you’re financing and adds to your interest burden. Politely decline anything you don’t want or need.

Navigating Your Car Loan Responsibilities

Taking out a loan for a car is just the beginning; managing it responsibly is key to maintaining your financial health and achieving full ownership. Understanding your ongoing obligations will help you avoid pitfalls and potentially save money.

Making Timely Payments

This might seem obvious, but consistently making your car loan payments on time is paramount. Set up automatic payments or calendar reminders to ensure you never miss a due date. This simple habit is crucial for several reasons.

Consequences of Late Payments

Late payments can have severe repercussions. Firstly, you’ll likely incur late fees, adding to your overall cost. More importantly, late payments are reported to credit bureaus and can significantly damage your credit score, making it harder to secure favorable rates for future loans. In extreme cases, repeated late payments can lead to repossession of your vehicle, resulting in not only the loss of your car but also further damage to your credit and potentially a deficiency balance still owed to the lender.

Understanding Interest and Principal

Each monthly payment you make is typically divided into two components: principal and interest. The principal is the amount you borrowed, and the interest is the cost of borrowing that money.

How Payments Are Applied

In the early stages of a car loan, a larger portion of your payment goes towards interest. As the loan matures, more of each payment is applied to the principal, gradually reducing the amount you owe. Understanding this amortization schedule can help you visualize your progress and motivate you to pay down the loan faster.

Early Payoff Strategies

Some individuals aim to pay off their car loan sooner than the agreed-upon term. This can be a smart financial move, as it reduces the total amount of interest you pay.

Is It Always a Good Idea?

Paying off your loan early can free up cash flow and reduce your debt burden. However, before making extra payments, check your loan agreement for any prepayment penalties. While rare in auto loans, some lenders might charge a fee for paying off the loan ahead of schedule. Ensure that any extra payments are applied directly to the principal to maximize the interest savings.

Refinancing Your Car Loan

As mentioned earlier, refinancing can be a powerful tool for optimizing your car loan. It involves taking out a new loan to pay off your current one.

When and Why It Makes Sense

Refinancing makes sense if you can secure a lower interest rate than your current loan. This could be due to an improved credit score, a general drop in market interest rates, or finding a more competitive lender. A lower rate will reduce your monthly payment or allow you to pay off the loan faster while keeping the payment similar. You might also refinance to adjust the loan term, either shortening it to save on interest or extending it to lower your monthly payments if you’re facing financial hardship.

Common Mistakes and How to Avoid Them

Taking out a loan for a car is a significant financial commitment. Being aware of common pitfalls can help you steer clear of expensive errors and ensure a smoother, more affordable car-buying experience.

- Not Checking Your Credit Score: This is a fundamental oversight. Your credit score dictates your interest rate. Failing to check it means you’re going into negotiations blind, potentially accepting a higher rate than you qualify for. Always review your credit report for errors before applying.

- Focusing Only on Monthly Payments: Dealerships often emphasize the "affordable" monthly payment. While important for budgeting, fixating solely on this figure can obscure the total cost of the loan. A low monthly payment achieved through a long loan term means you’ll pay significantly more in interest over time. Always ask for the total cost of the loan.

- Ignoring the Total Cost of the Loan: This ties into the previous point. The true measure of a loan’s expense is the total amount you will pay over its lifetime, including the principal and all interest. Comparing total costs between different offers gives you a clearer picture of the best deal.

- Skipping Pre-Approval: Going to a dealership without pre-approval from an outside lender puts you at a disadvantage. You lose negotiating leverage and are more susceptible to accepting whatever financing the dealership offers, which might not be the most competitive.

- Buying Unnecessary Add-Ons: Resist the pressure to purchase extended warranties, fabric protection, or other dealership add-ons unless you’ve thoroughly researched them and determined their value. These often come with high markups and inflate your loan amount, leading to more interest paid.

- Not Reading the Loan Agreement Thoroughly: This cannot be stressed enough. The loan agreement is a legally binding document. Every term, condition, fee, and rate should be understood before you sign. If anything is unclear, ask for clarification. Never rush through this crucial step.

Conclusion

Taking out a loan for a car is a significant financial decision, but it doesn’t have to be an intimidating one. By understanding the different types of loans, diligently preparing your finances, and carefully navigating the application and negotiation processes, you can secure favorable terms that align with your budget and goals. Remember to prioritize your financial health over impulse purchases.

Empower yourself with knowledge, compare multiple offers, and always read the fine print. With these strategies, you’ll not only drive away in the car of your dreams but also do so with the confidence of a smart and informed borrower. Make every mile count, knowing you made the best financial choice for your auto financing.