Taking Out Loans For A Car: Your Ultimate Guide to Smart Auto Financing

Taking Out Loans For A Car: Your Ultimate Guide to Smart Auto Financing Carloan.Guidemechanic.com

Embarking on the journey to purchase a new or used vehicle is an exciting prospect. The open road beckons, and the promise of convenience and independence is powerful. However, for most of us, this dream often involves taking out loans for a car. Understanding the intricacies of auto financing isn’t just about securing a loan; it’s about securing the right loan that aligns with your financial health and long-term goals.

As an expert blogger and professional SEO content writer, I’ve seen countless individuals navigate the sometimes-confusing world of car loans. My mission with this comprehensive guide is to demystify the process, empower you with knowledge, and ensure you make informed decisions. We’ll dive deep into every facet of car financing, from preparation to approval and beyond, making this your go-to pillar content for all things auto loans.

Taking Out Loans For A Car: Your Ultimate Guide to Smart Auto Financing

The Foundation: Before You Even Think About a Loan

Before you set foot in a dealership or click "apply" on an online lender’s website, meticulous preparation is key. This initial groundwork can significantly impact the terms of your car loan and your overall financial well-being. Skipping this crucial step is one of the most common mistakes people make.

Understanding Your Financial Health

Your financial profile is the first thing lenders evaluate. They want to assess your ability to repay the loan reliably. This involves looking at several critical indicators.

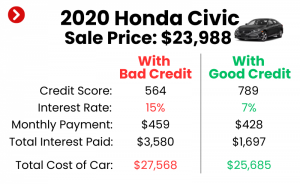

Your Credit Score: The Ultimate Indicator

Your credit score is arguably the most significant factor in determining the interest rate you’ll receive on a car loan. Lenders use this three-digit number to gauge your creditworthiness. A higher score signals less risk, often leading to lower interest rates and better loan terms.

Based on my experience, aiming for a score above 700 is ideal for securing the most competitive rates. If your score is lower, don’t despair; there are still options, but understanding its impact upfront is vital. Knowing your score allows you to anticipate potential loan offers and, if necessary, take steps to improve it before applying.

Debt-to-Income Ratio (DTI): Are You Overextended?

Your debt-to-income ratio (DTI) is another crucial metric lenders consider. It compares your total monthly debt payments to your gross monthly income. For instance, if your monthly debts (rent/mortgage, credit card payments, student loans, etc.) are $1,500 and your gross income is $4,500, your DTI is 33%.

Lenders typically prefer a DTI below 40%, including your prospective car payment. A high DTI suggests you might be overextended, making lenders hesitant to approve additional credit. Calculating this beforehand gives you a realistic picture of your borrowing capacity.

Budgeting for Success: What Can You Truly Afford?

Beyond what a lender thinks you can afford, what can you realistically afford each month? This question often gets overlooked in the excitement of car shopping. Create a detailed budget that accounts for all your regular expenses, savings goals, and discretionary spending.

Remember to factor in not just the monthly car payment, but also insurance, fuel, maintenance, and potential parking fees. Pro tips from us: a car’s true cost extends far beyond its sticker price and monthly loan payment. A realistic budget prevents you from becoming "car poor."

Determining Your Affordability: Total Cost vs. Monthly Payments

It’s tempting to focus solely on the monthly payment, but this can be a dangerous trap. While a low monthly payment might seem appealing, it often comes at the cost of a longer loan term and more interest paid over time. Always consider the total cost of the loan.

A car that costs $30,000 at a 5% interest rate over 60 months will have a lower total cost than the same car at a 7% interest rate over 72 months, even if the latter has a slightly lower monthly payment. Use online car loan calculators to compare different scenarios. This comprehensive view ensures you’re making a financially sound decision.

New vs. Used Car Loan Considerations

The type of car you choose significantly impacts your loan. New cars generally command higher prices and, while they might qualify for lower interest rates from manufacturers, they depreciate rapidly. Used cars, on the other hand, are often more affordable but might come with slightly higher interest rates due to perceived higher risk.

When taking out loans for a car, remember that lenders might have different terms for new versus used vehicles. Some lenders might offer slightly longer terms for new car loans, while used car loans often have stricter age and mileage limits. Researching both options thoroughly allows you to make an educated choice that fits your budget and lifestyle.

Navigating Car Loan Options: Where to Find Your Financing

Once you have a clear picture of your financial standing and what you can afford, the next step is to explore where to get your loan. There isn’t a one-size-fits-all solution; different lenders offer various advantages and disadvantages.

Dealership Financing: Convenience at a Cost?

Many car buyers opt for financing directly through the dealership. This method offers unparalleled convenience, allowing you to handle the car purchase and loan application all in one place. Dealerships often work with multiple lenders and can sometimes offer promotional rates.

However, based on my experience, dealership financing might not always be the most competitive option. While they might present attractive initial offers, it’s crucial to compare their rates with other sources. Dealers are businesses, and they often mark up interest rates to earn a profit. Always come prepared with outside offers.

Bank Loans & Credit Unions: Traditional & Often Competitive

Traditional banks and local credit unions are reliable sources for auto loans. Banks often offer competitive rates, especially to customers with good credit and existing relationships. They provide structured loan products and clear terms.

Credit unions, being member-owned, often boast some of the lowest interest rates available. They prioritize their members’ financial well-being, often leading to more flexible terms and personalized service. Pro tips from us: always check with your local credit union; their rates can be surprisingly good.

Online Lenders: Speed and Accessibility

In today’s digital age, online lenders have emerged as a popular option for car loans. These platforms offer a streamlined application process, often providing quick pre-approvals and competitive rates. They cater to a wide range of credit profiles, from excellent to those seeking bad credit car loans.

The main advantage here is speed and the ability to shop around from the comfort of your home. However, it’s essential to ensure the online lender is reputable and transparent about their terms and conditions. Always read reviews and verify their credentials.

Pre-Approval: Your Secret Weapon

One of the most powerful strategies when taking out loans for a car is getting pre-approved before you even visit a dealership. Pre-approval means a lender has reviewed your credit and financial information and tentatively agreed to lend you a specific amount at a certain interest rate.

This process gives you several advantages. First, it establishes a clear budget, so you know exactly how much car you can afford. Second, it transforms you into a cash buyer at the dealership, giving you significant leverage in price negotiations. You can then compare the dealership’s financing offer against your pre-approval, ensuring you get the best possible deal.

The Application Process: What You Need to Know

Once you’ve chosen your lender and found your desired vehicle, it’s time for the formal application. This stage requires attention to detail and a clear understanding of the terms involved. Common mistakes to avoid here include rushing through documents or not fully grasping the implications of your loan agreement.

Required Documents: Be Prepared

Lenders require specific documents to process your application. Being prepared can expedite the approval process. You’ll typically need:

- Proof of Identity: Driver’s license or state ID.

- Proof of Income: Pay stubs, W-2 forms, or tax returns.

- Proof of Residency: Utility bill or lease agreement.

- Social Security Number: For credit checks.

- Vehicle Information: If you’ve already chosen a car (make, model, VIN).

Having these documents ready ensures a smooth and efficient application, minimizing delays.

Understanding Interest Rates (APR): Beyond the Percentage

The interest rate is the cost of borrowing money, expressed as a percentage of the loan amount. However, it’s crucial to look at the Annual Percentage Rate (APR), which includes the interest rate plus any additional fees or charges associated with the loan. The APR provides a more accurate picture of the total cost of borrowing.

A difference of even one percentage point in your APR can translate to hundreds or thousands of dollars over the life of the loan. Always compare APRs, not just quoted interest rates, when evaluating different loan offers. This ensures you’re comparing apples to apples.

Loan Terms (Length of Loan): The Balancing Act

The loan term refers to the duration over which you will repay the loan, typically expressed in months (e.g., 36, 48, 60, 72, or even 84 months). A shorter loan term means higher monthly payments but less interest paid overall. A longer loan term results in lower monthly payments but significantly more interest over time.

While a longer term might seem more affordable monthly, it also means you’ll be paying for the car for a longer period, potentially even after its value has significantly depreciated. Based on my experience, aim for the shortest loan term you can comfortably afford to minimize the total cost of ownership.

Down Payments: Why They Matter

Making a down payment is highly recommended when taking out loans for a car. A larger down payment reduces the amount you need to borrow, which in turn lowers your monthly payments and the total interest you’ll pay. It also helps you avoid being "upside down" on your loan, where you owe more than the car is worth.

Pro tips from us: aim for at least 10-20% of the car’s purchase price as a down payment if possible. This not only saves you money but also demonstrates financial responsibility to lenders, potentially leading to better loan terms.

Trade-Ins: A Smart Way to Reduce Your Loan

If you have an existing vehicle, trading it in can act as a de facto down payment, reducing the amount you need to finance. However, be strategic about your trade-in. Research its value beforehand using reputable sources like Kelley Blue Book or Edmunds.

Negotiate the price of the new car and the value of your trade-in separately. Some dealerships might offer a good trade-in value but inflate the new car price, or vice-versa. Clear, separate negotiations ensure you get the best deal on both ends.

Common Pitfalls and How to Avoid Them

Even with all the preparation, the car loan process can present pitfalls. Being aware of these common mistakes can save you a lot of money and stress.

Not Shopping Around for Rates

This is perhaps the biggest mistake car buyers make. Settling for the first loan offer, especially from the dealership, often means missing out on better rates elsewhere. Just as you shop for the best car, you should shop for the best loan.

Apply for pre-approvals from multiple lenders – banks, credit unions, and online lenders. Each inquiry might cause a slight, temporary dip in your credit score, but multiple inquiries within a short period (typically 14-45 days) are usually treated as a single inquiry by credit bureaus for rate shopping purposes. This strategy ensures you secure the most competitive rate available to you.

Focusing Only on Monthly Payments

As mentioned earlier, fixating solely on the monthly payment can lead to longer loan terms and higher overall interest costs. A low monthly payment can disguise a much more expensive loan over time. Always ask for the total cost of the loan, including all interest and fees.

Think of it this way: a lower monthly payment might feel good in the short term, but it could mean you’re paying for a car you no longer own or enjoy. Prioritize the total cost and a manageable loan term.

Ignoring the Total Cost of the Loan

Beyond the interest, consider other costs associated with the loan. These might include origination fees, documentation fees, or prepayment penalties. While many auto loans don’t have prepayment penalties, it’s crucial to confirm this in your loan agreement.

Understanding the true total cost means looking beyond the monthly payment and the interest rate to every single fee and charge. Transparency is key, and if a lender isn’t upfront about all costs, that’s a red flag.

Add-ons and Extras: Are They Worth It?

Dealerships often present a variety of add-ons at the time of purchase: extended warranties, GAP insurance, paint protection, fabric protection, and more. While some of these might offer value, many are overpriced or unnecessary.

When taking out loans for a car, remember that these add-ons are often financed into your loan, increasing your principal, your monthly payment, and the total interest you’ll pay. Critically evaluate each add-on. Can you get it cheaper elsewhere? Is it truly necessary? For example, GAP insurance can be valuable, but you might find it at a lower cost through your auto insurer.

Understanding the Fine Print

The loan agreement is a legally binding document. It details your interest rate, loan term, payment schedule, late payment penalties, and any other conditions. Common mistakes to avoid include signing without thoroughly reading and understanding every clause.

Don’t hesitate to ask questions if something is unclear. A reputable lender will be happy to explain any aspect of the contract. Pay close attention to clauses about early payoff penalties or default conditions. Your financial future depends on this understanding.

Special Situations & Post-Loan Management

The journey doesn’t end once you drive off the lot. There are unique situations and ongoing management considerations that can further optimize your car loan experience.

Bad Credit Car Loans: Strategies and Expectations

If you have a lower credit score, securing a car loan can be more challenging, and you’ll likely face higher interest rates. However, it’s not impossible. Specialized lenders cater to individuals with less-than-perfect credit.

Strategies include:

- Saving a larger down payment: This reduces the risk for the lender.

- Finding a cosigner: A cosigner with good credit can help you qualify for better terms, but they become equally responsible for the debt.

- Seeking out subprime lenders: Be cautious and thoroughly research their reputation and terms.

- Focusing on affordable vehicles: Avoid stretching your budget.

While the rates might be higher, making timely payments on a bad credit car loan can be an excellent way to rebuild your credit score.

Cosigners: When and Why

A cosigner is an individual with good credit who agrees to take on legal responsibility for your loan if you fail to make payments. This can be a lifesaver for those with limited or poor credit, as it often helps secure approval and better interest rates.

However, a cosigner takes on significant risk. Their credit will be affected if you miss payments, and they could be sued for the debt. Only consider a cosigner if you are absolutely confident in your ability to repay the loan and have a clear understanding with them.

Refinancing Your Car Loan: When It Makes Sense

Your car loan isn’t necessarily set in stone for its entire term. Refinancing involves taking out a new loan to pay off your existing one, typically to secure a better interest rate or a more favorable loan term.

It makes sense to consider refinancing if:

- Your credit score has improved: A higher score could qualify you for a lower rate.

- Interest rates have dropped: Market rates might be lower than when you initially financed.

- You want to lower your monthly payment: By extending the loan term (though this means more interest overall).

- You want to shorten your loan term: To pay it off faster and save on interest (though this means higher monthly payments).

Pro tips from us: research refinancing options periodically, especially a year or two into your current loan, as your financial situation or market rates might have changed.

Early Payoff Considerations

Paying off your car loan early can save you a significant amount in interest, especially if you have a high-interest loan. Before making extra payments or a lump-sum payoff, check your loan agreement for any prepayment penalties. Most auto loans do not have them, but it’s always wise to confirm.

If you have multiple debts, strategically prioritize. Paying off a high-interest car loan might be a better use of extra funds than, for example, a low-interest mortgage. Consult with a financial advisor to determine the best strategy for your individual circumstances. For more insights into managing various types of debt, you might find our article on Smart Debt Management Strategies helpful.

Conclusion: Drive Away with Confidence

Taking out loans for a car is a significant financial decision that impacts your budget for years. By approaching the process with knowledge, preparation, and a strategic mindset, you can navigate the complexities of auto financing with confidence. Remember to understand your financial health, shop around for the best rates, read the fine print, and avoid common pitfalls.

The goal isn’t just to get approved for a loan; it’s to secure a loan that serves your best interests and contributes positively to your financial journey. Drive away not just in a new car, but with the peace of mind that comes from making an informed, intelligent financial choice. For further reading on personal finance, consider exploring resources like the Consumer Financial Protection Bureau’s auto loan guide.

We encourage you to share your experiences or questions about car loans in the comments below. Your insights help others make better decisions!